A "New Era" Amid "Chaos"!

With globalisation behind us, we have now entered into uncharted territories with the world’s largest economy using its clout to impose draconian tariffs.

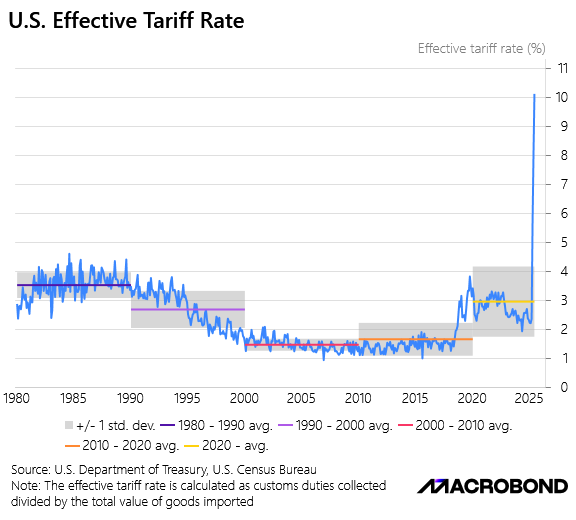

As a result of the enormous tariffs, the US effective tariff rate has jumped to more than 12% (some estimates say 15%+), the highest in the last 100 years.

Furthermore, under Trump, trade has been weaponised to punish countries such as Brazil, Switzerland and India.

As the new era of a deglobalised multi-polar world begins, investors must assess the geopolitical trends along with the global macro developments.

We are witnessing historic structural changes, or in other words, these are once-in-a-lifetime events.

There is no dearth of chaos in the Trump presidency. The latest transpired in the bullion market when reports circulated about 39% tariffs on 1KG Gold bar.

This led to a short squeeze in the Gold futures.

However, the WH later clarified that the concerned tariff will not be applicable, leading to insane swings in the shiny yellow metal.

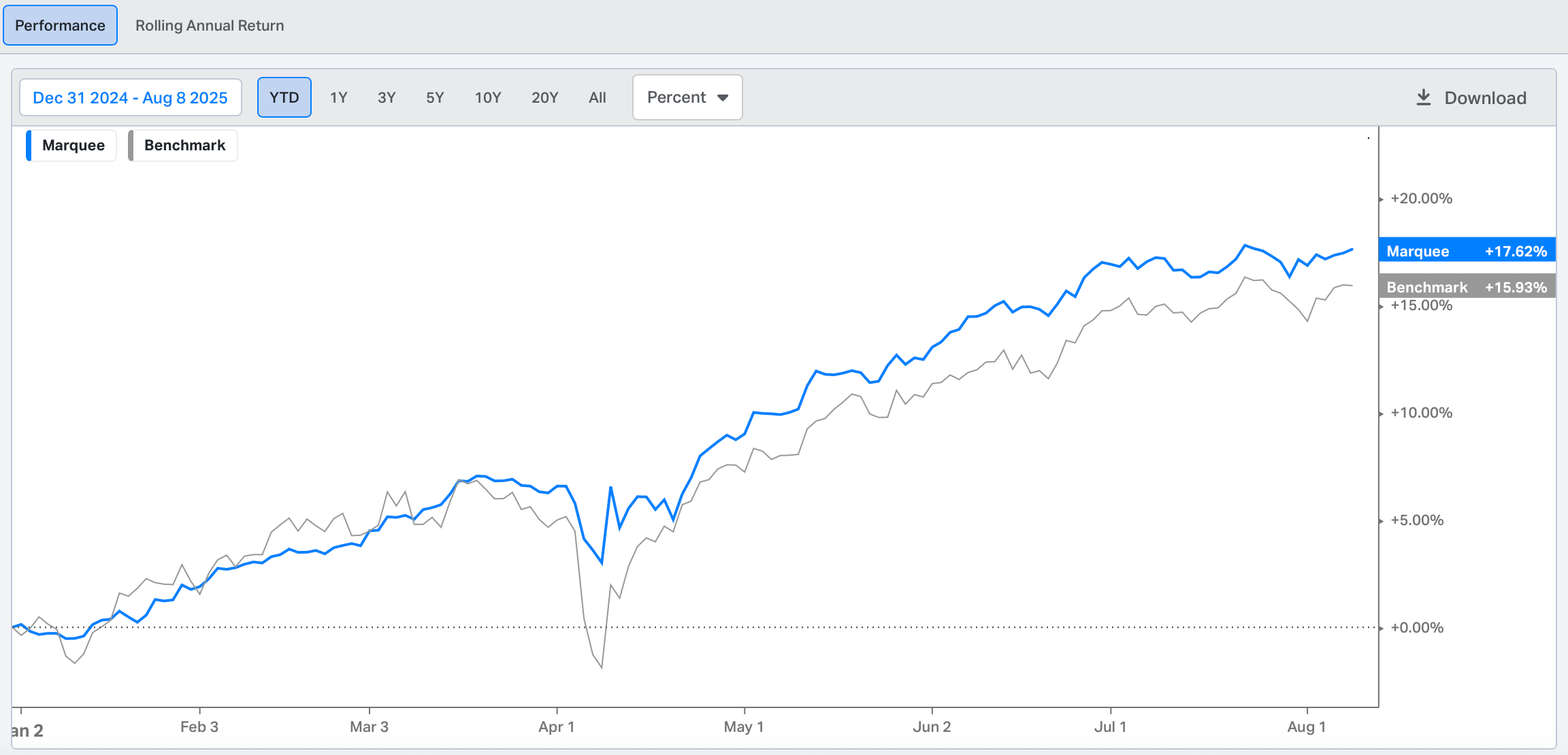

Despite all the chaos that we have witnessed this year, we have had a stupendous year, and the outperformance continues unabated.

PS: Before we begin, we will increase our paid subscription prices to $29.99/M or $ 299.99/Yr starting 1st September 2025.

Note that subscribers who are currently enrolled or will enrol by September 1st will be subscribed at the mouth-watering current prices ($24.99/$249.99) “FOREVER”.

Furthermore, those who have subscribed at the original price of $14.99/$149.99 two years back will see no change in their plans.

Therefore, anyone who wants to take advantage of a 16% lifetime discount can subscribe until midnight on August 31st at the current prices.

PS: Please avoid Apply Pay while you pay for your subscription as it charges very high fees. Also, do check your invoice for any discrepancies.

US/Bonds/Gold/Oil

ISM data has been our preferred indicator due to its historical accuracy in predicting the business cycle trough and peaks.

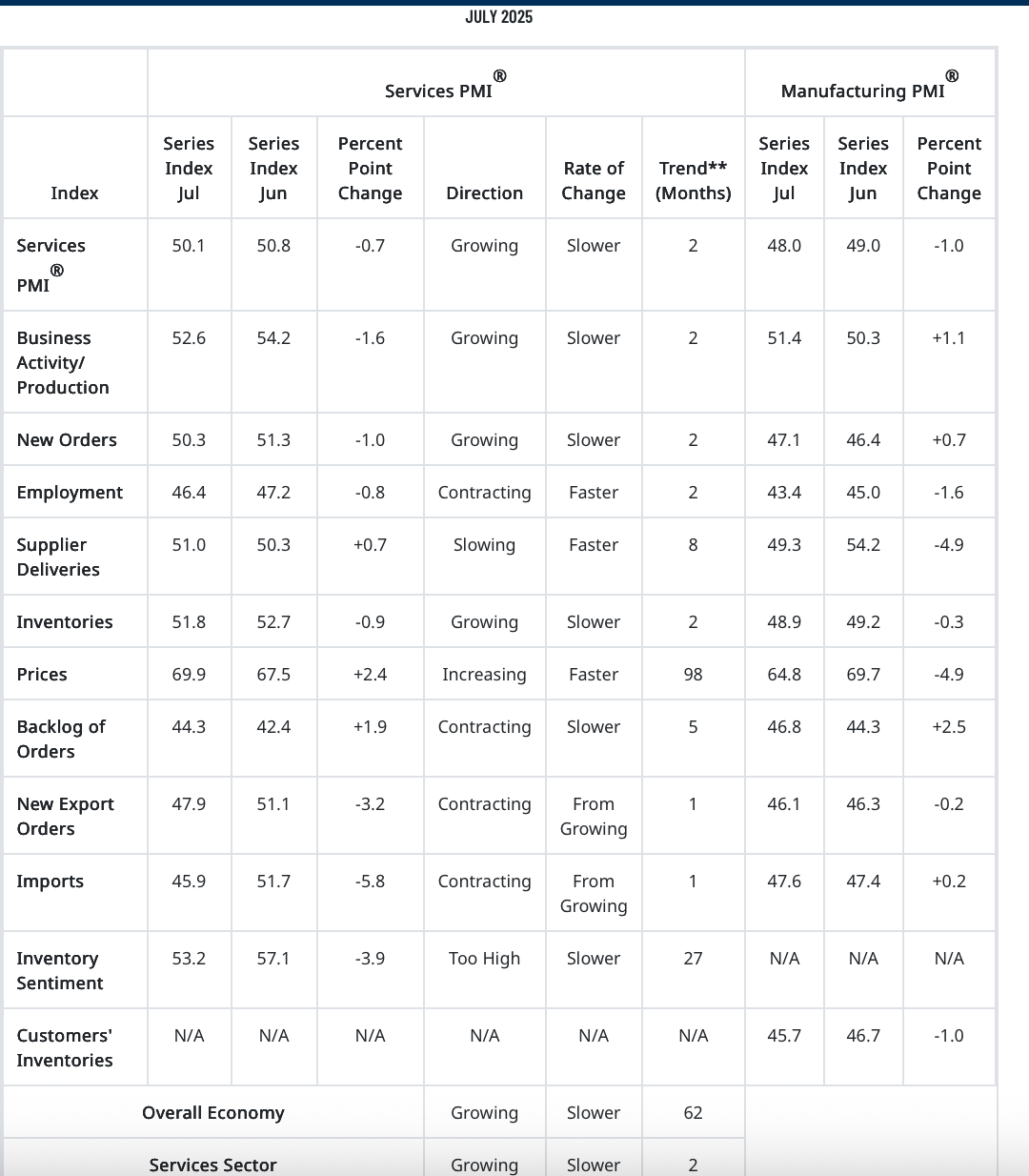

Last week we got the ISM Manufacturing data, and this week the ISM Services was released.

ISM Services has been a critical barometer for general consumer sentiment and consumption, which forms a lion's share of the US GDP.

The latest survey has been horrendous when we dig deeper.

The Export Orders, Import and the Employment component witnessed significant contraction.

When we focus on macro, we give a lot of weight to “imports” as it is directly correlated with the consumer demand.

Though one month of data isn’t enough, as the effect of front loading due to tariffs led to an enormous spike, if the trend continues, it will be a worrisome sign.

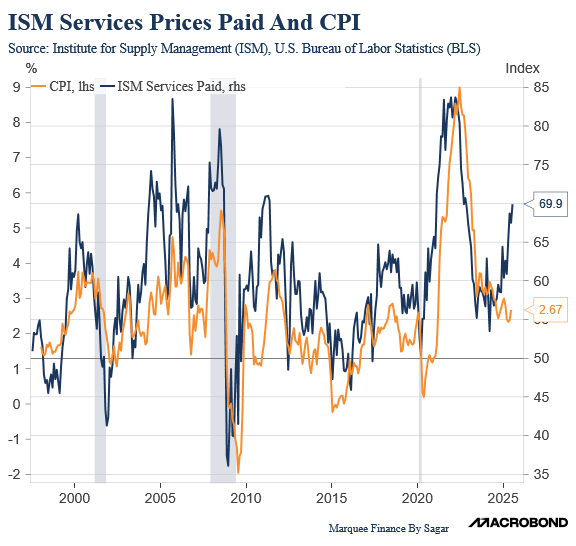

The stunner in the data was the ISM Services Paid, which is now in an uptrend and will raise alarms at the Fed.

The ISM Services Paid and CPI have historically been correlated.

If the ISM Services Paid is to be believed, we are heading to a spike in inflation as early as Q4.

Nevertheless, the extent and duration of rise in inflation are debatable.

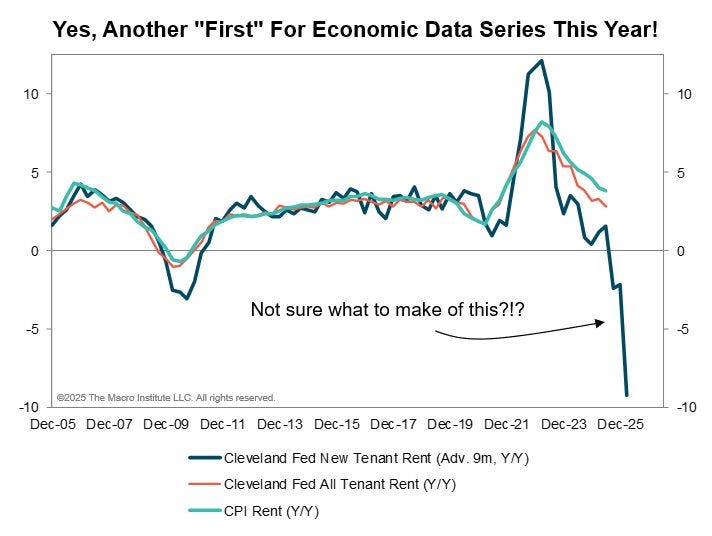

This is because while Core Goods and Services will likely witness a significant surge, there are now indications that the housing/rent will collapse and is entering deflation.

We will have a detailed analysis of the….