An INFLECTION Point in the AI Story Soon?

The internet has been abuzz since yesterday about a serious issue in GPT 5.56 SOL, as multiple reports indicate that Sol accidentally deletes “ALL” the Mac files.

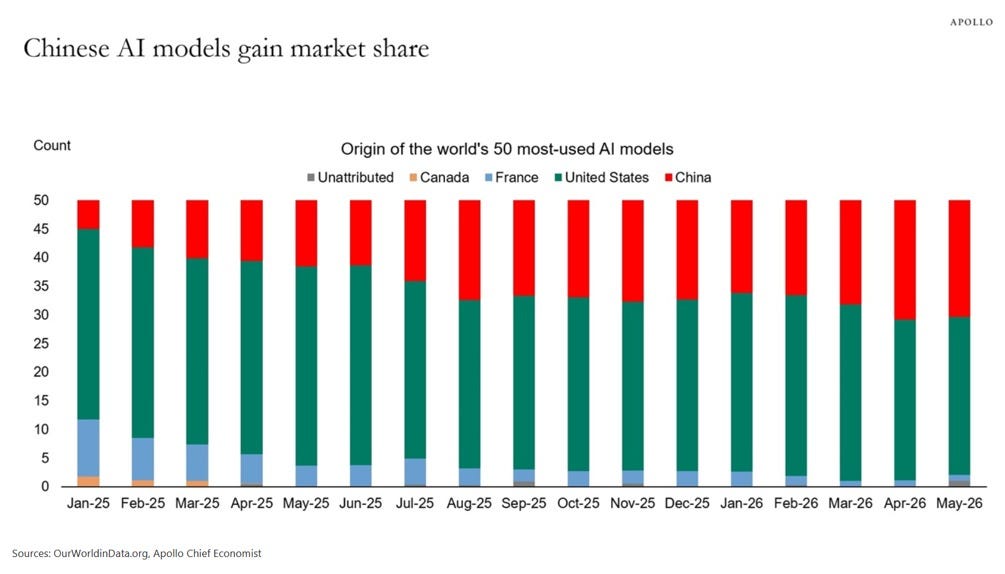

Furthermore, as costs in US Frontier models become unbearable, Chinese LLMs are gaining market share at an unprecedented pace.

In a stunning development, token usage among the top 20 Chinese AI models surged by 113% MoM to 98 trillion tokens in June, compared with a 43% jump in US model token usage to 53 trillion tokens.

As portrayed weeks ago, the competitive advantage of Chinese models will trigger a price war among frontier US models, which will likely be the inflection point in the AI story.

As a result, we believe we are at the forefront of major announcements from US hyperscalers in the upcoming earnings season.

We have already seen ORCL’s debt rating downgraded to BBB- (just one notch above junk status). If capex is not moderated, hyperscaler stocks will likely enter “severe” bear-market territory.

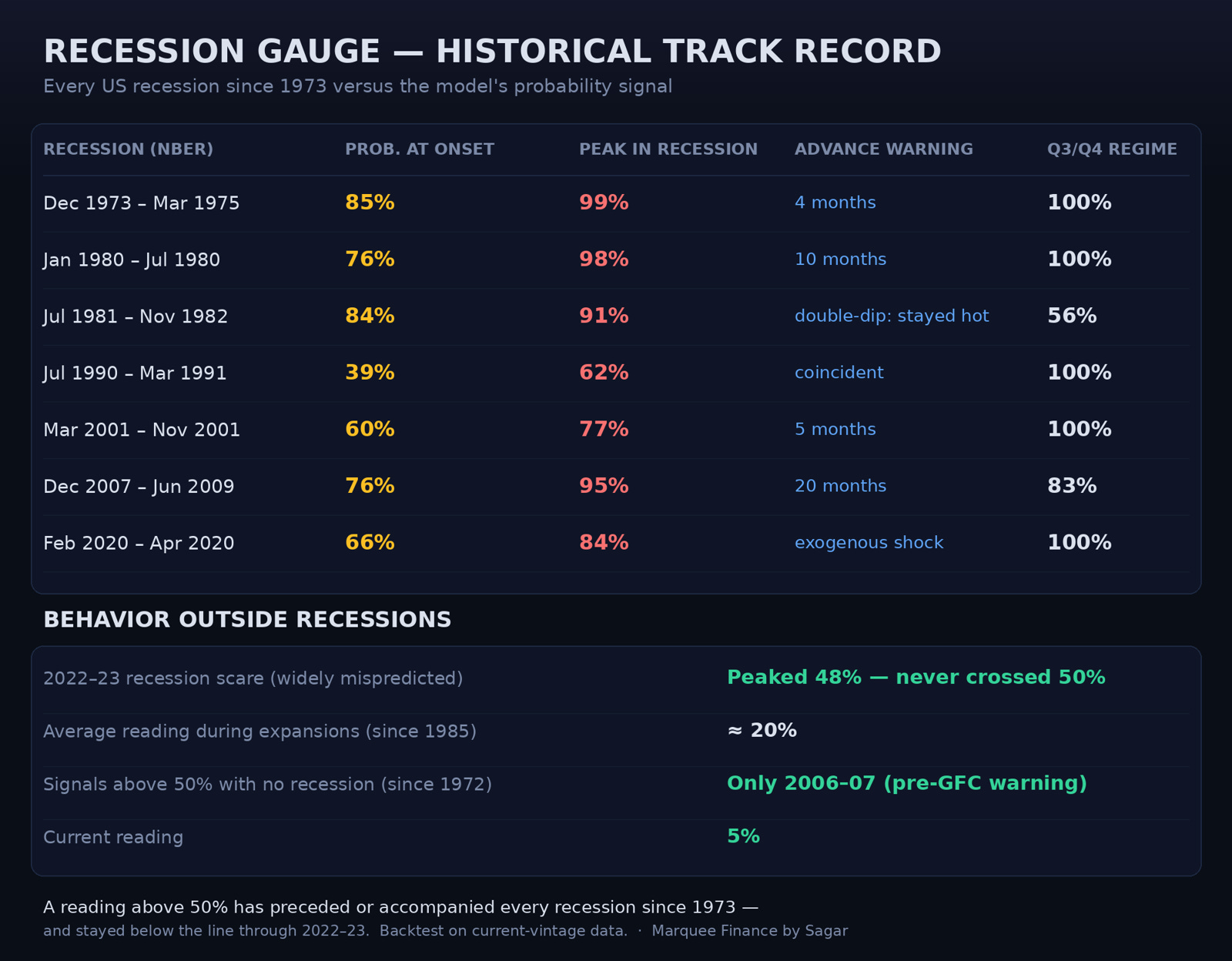

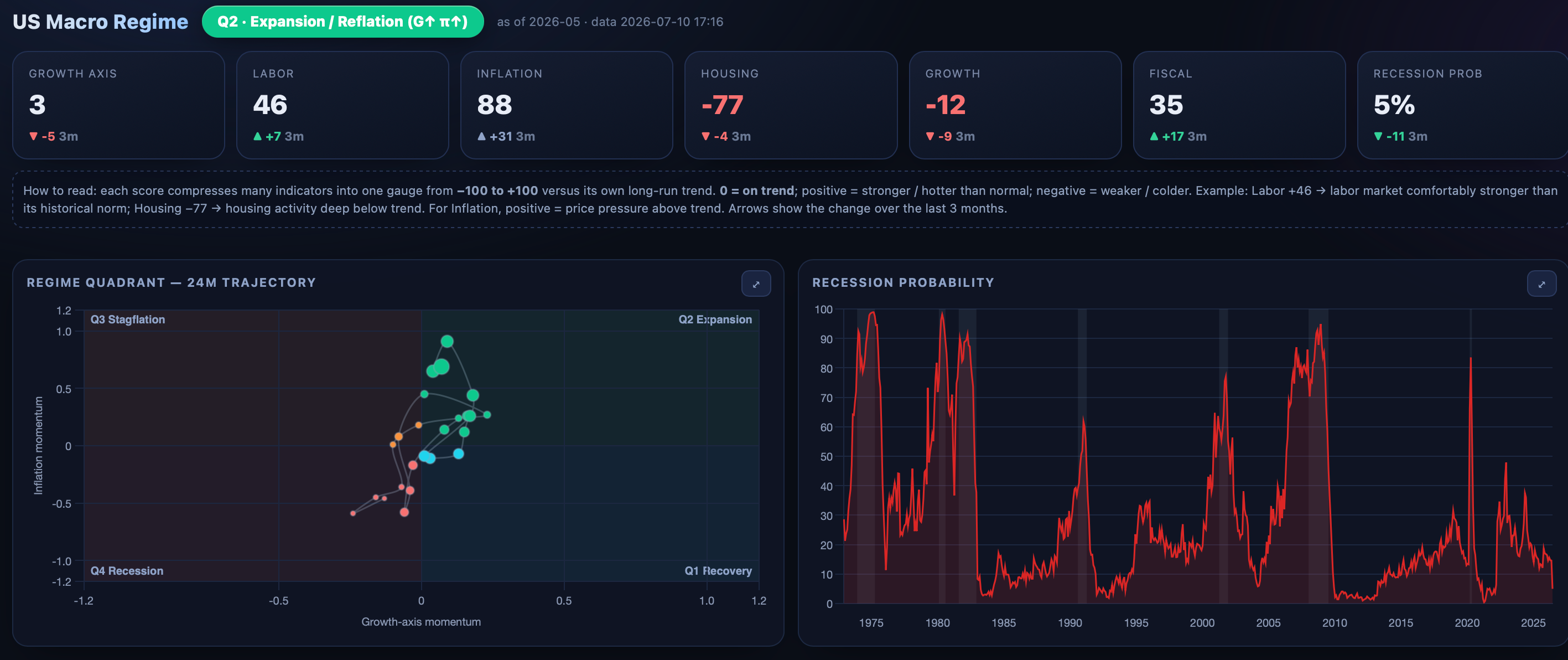

We also launched our US macro dashboard this week.

It uses more than 60 proprietary indicators across labour, housing, inflation, and growth to devise the growth/inflation regime and the recession probability.

Whenever the recession gauge rose above 50%, a recession was followed in the next 5-10 months.

Note that in all previous recessions (ex-COVID), the NBER declared a recession 3-5 quarters after the recession began.

Since our model places significant weight on the housing sector, there was a false call in 2022.

We investigated the issue and added a new variable to the model (fiscal impulse).

The calculations remain proprietary; however, one can view the fiscal score, along with the others, in the dashboard.

PS: Note that Growth tells you what the goods/activity side is doing, whereas Growth axis tells you where the overall cycle classification stands once labour gets its vote. When the two diverge sharply, watch labour — if it rolls over and converges downward, the axis follows, and the regime flips.

Link to the dashboard: https://dashboard.marqueefinancebysagar.com

We are also building European, Chinese, and Japanese dashboards to help us join the dots and create a global macro dashboard to gauge economic activity.

The US dashboard will be free for all subscribers until 15th August. After that, it will be reserved for paid subscribers only.

We are announcing a price increase for our subscription plans, driven by significant new features and upcoming updates. Starting August 15th, the monthly plan will increase from $ 29.99 to $ 39.99, and the annual plan will increase from $ 299.99 to $ 399.

Existing subscribers will “NOT” see any changes and will remain on their current plans.

We are up 5.54% YTD, and barring March, we have had all positive months this year.

Note that we hit YTD highs of 6.5% on Tuesday but gave up the gains amid a broad-based sell-off midweek.

We expect to deliver significant alpha and double-digit gains this year as well.

Let us now take a deep dive into the macro universe and analyse the cross-asset price action.

US/Equities/Bonds/Gold/Oil/Dollar/BTC!

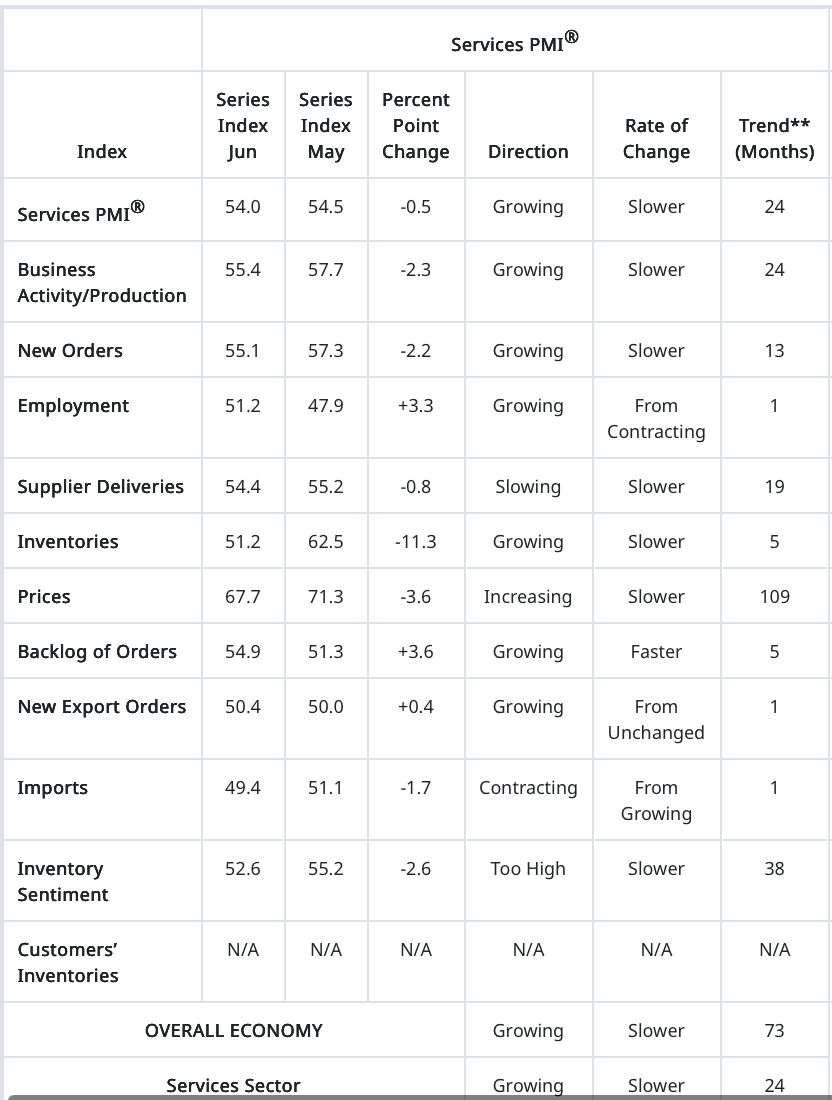

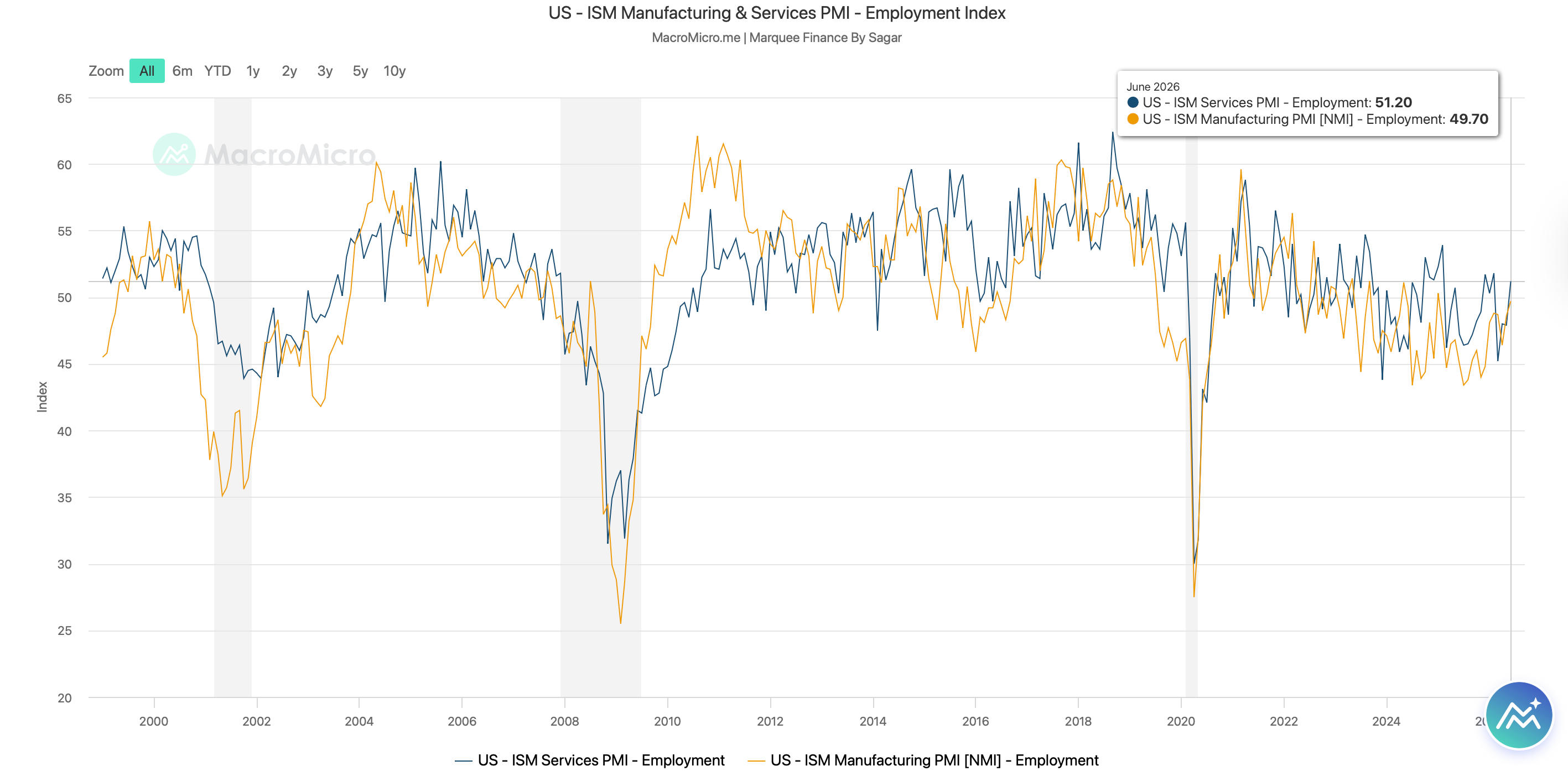

ISM Services came in at 54, in line with expectations.

Overall, it was a strong print with several green shoots.

ISM Services Employment entered expansion territory (>50) for the first time in a long time.

We believe this was partially due to the FIFA World Cup.

Nevertheless, the trend seems to be up.

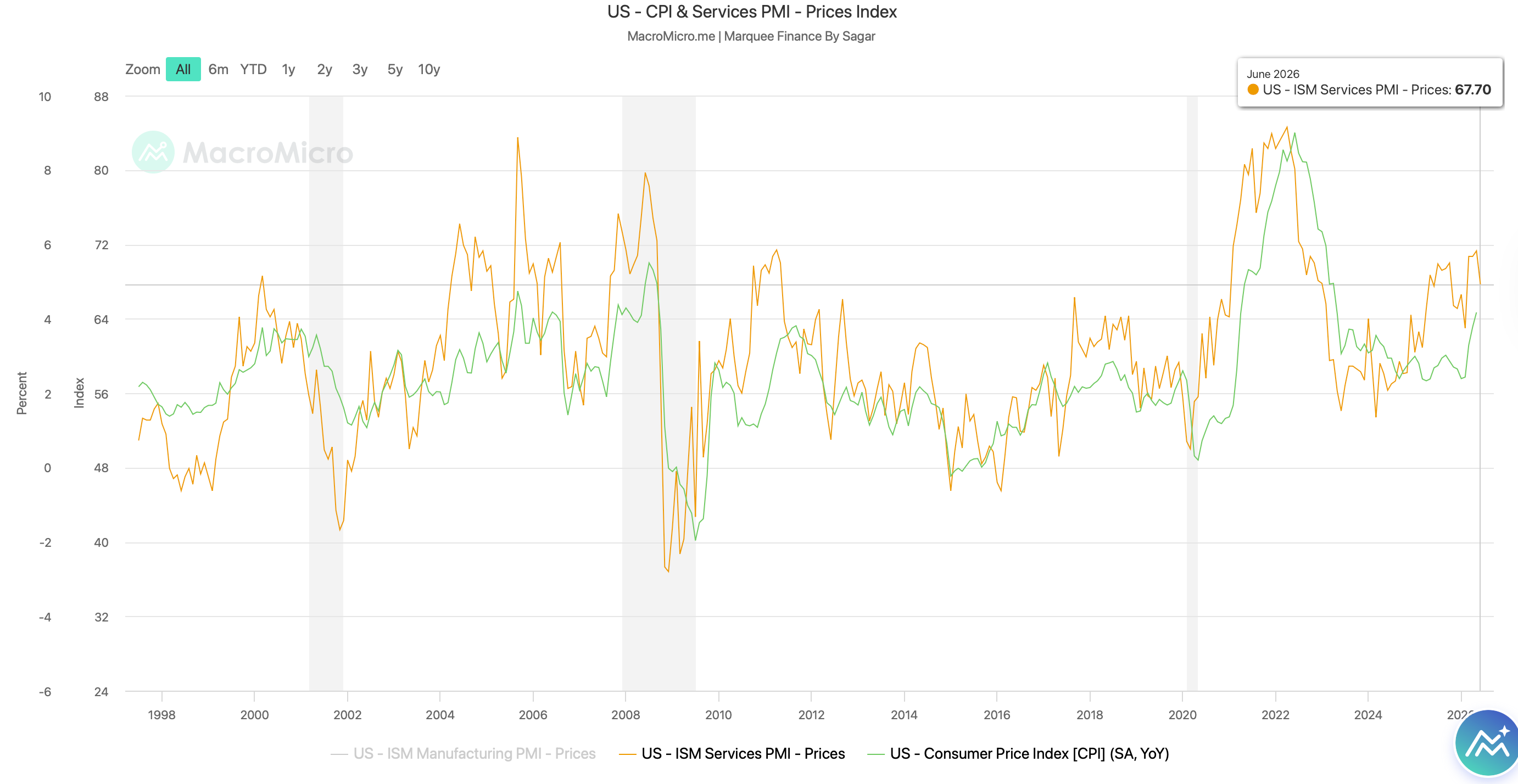

ISM Services Prices Paid have cooled significantly from its peak; however, remain elevated.

Considering the downtrend, we expect the CPI to peak in the next 2-3 months.

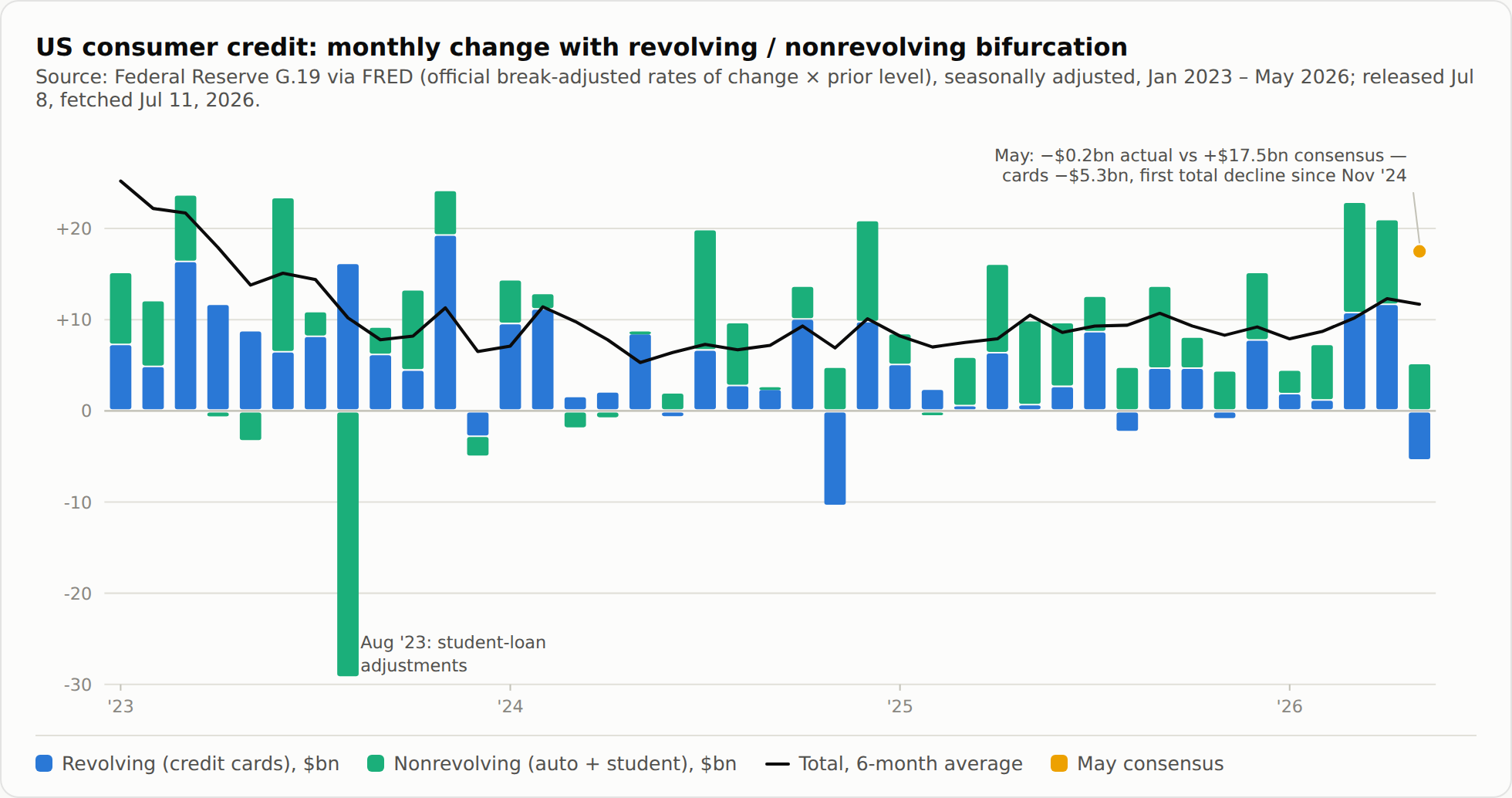

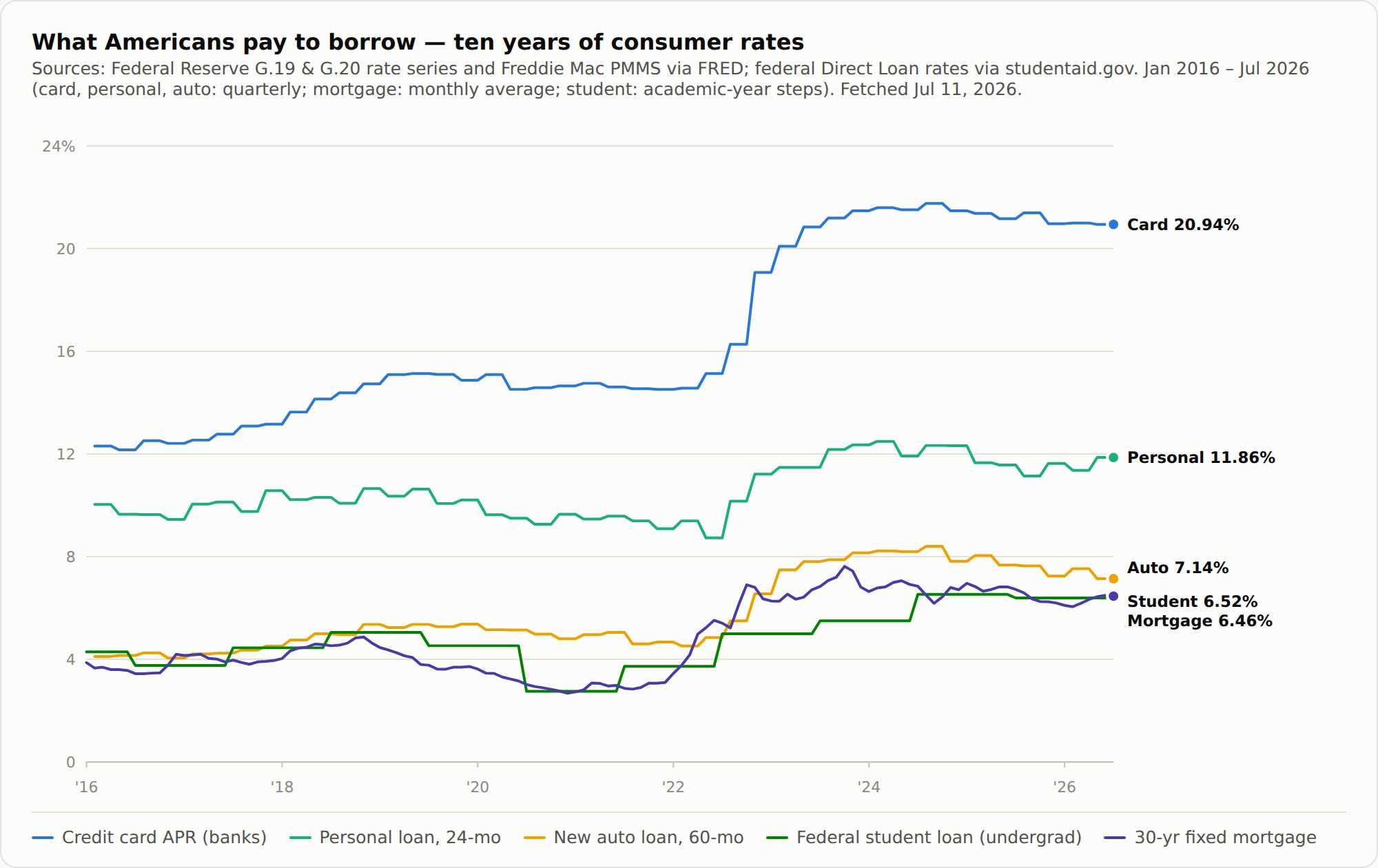

Consumer credit was a big miss, with a -$0.2 billion print vs an expectation of +$17.5 billion.

Revolving credit fell $5.3bn (−4.7% annualised, the biggest drop since Nov '24) while nonrevolving (auto + student) added +$5.1bn (+1.6%).

Clearly, higher credit card APRs along with higher auto/personal loan rates are hurting consumers, and thus we are witnessing tepid demand.

Furthermore, YoY growth remains below inflation, so real consumer credit has been flat or declining, leading to the conclusion that the economy is K-Shaped.