"Buy On Rumour, Sell On News"

“No one should look at today and think this is the new pace.”- Jerome Powell.

Since the concept of efficient markets came into existence, the famous adage has always prevailed: “Buy/Sell On Rumour, Sell/Buy On News”.

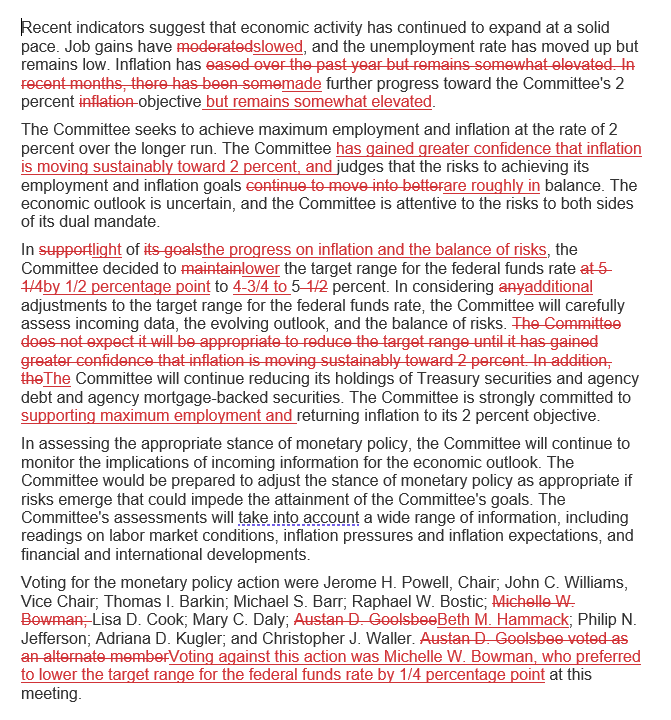

Once again, the bond markets sold on the news of the “hawkish” 50 bps cut by the world’s largest central bank.

Interestingly, for the first time since 2005, one Fed member (Bowman) dissented, preferring a 25 bps cut rather than a jumbo 50 bps cut.

Furthermore, there was no change in QT, as some market participants expected.

Why was the cut termed as hawkish?

Simply put, market expectations had grown significantly in the run-up to the policy as Mr Market was pricing in massive 120 bps of cuts (in 2024), and long-duration trade had become overcrowded.

Thus, the Fed’s SEP projections of 50 bps more cuts by the end of the year (most probably 25 bps each in November and December), totalling 100 bps in 2024, disappointed the bond markets.

On the contrary, after a knee-jerk reaction, the stock markets reacted positively on continued hopes of a “soft landing.”

Commodities rallied due to oversold conditions (they were pricing in a hard landing), lower DXY, and prospects of a soft landing.

In other news, the BOE surprised us by holding rates steady, as we expected a cut of at least 25 bps.

The Bank Of Japan (BOJ) maintained the status quo, while some market participants termed it as a “dovish” hold (though we have a different take- Check The East section)

Let us examine the macro data and our predictions for the future.

US!

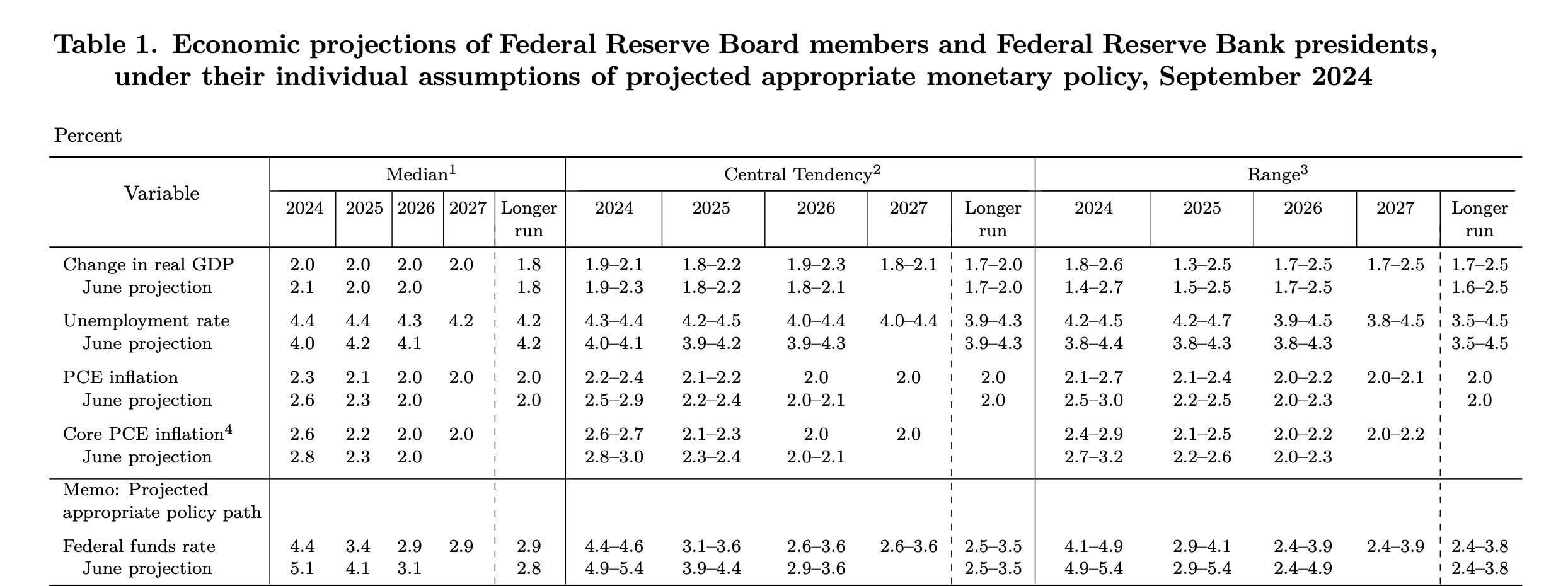

Let us begin with the dot plots, which were an eye-opener for many market participants.

While the year-end Unemployment Rate (UR) was raised higher from 4% to 4.4%, growth was lowered from 2.1% to 2%.

We still believe that the Fed is behind the curve, and the UR will continue rising exponentially once it begins rising unless the Fed can steer a miraculous “soft landing.”

The highlight of the dot plots was the rise in the longer-run Fed Funds Rate (FFR), which has gradually risen from 2.5% to 2.9% (in the last two years).

This is indeed a big deal and indicates that the neutral rate has shifted significantly higher.

As a result, we may be at the cusp of a shift in the inflation target from 2% to 3% and structurally higher interest rates for this decade unless we get a big credit event that leads to the rates going back to 0.

Interestingly, JayPo mentioned the following in his statement:

“As inflation has declined and the labor market has cooled, the upside risks to inflation have diminished and the downside risks to employment have increased.

We now see the risks to achieving our employment and inflation goals as roughly in balance, and we are attentive to the risks to both sides of our dual mandate.”

Undoubtedly, the Fed’s focus has entirely shifted to the labour market, and JayPo also talked about the downward revisions to the Non-Farm Payroll (NFP)/ Jobs number.

While the dot plot suggests only 50 bps more rate cuts in the next two FOMC meetings in November and December, we believe that: