Buy The Rumour, Sell The News?

There were some murmurs about right-tail risk while the war was at its peak in March, but only a few expected the equity markets to rip higher without taking a breather.

While we were “cautious” (cautious≠bearish) until last week, we became more confident midweek that the markets are entering a “Buy The Rumour, Sell The News” event.

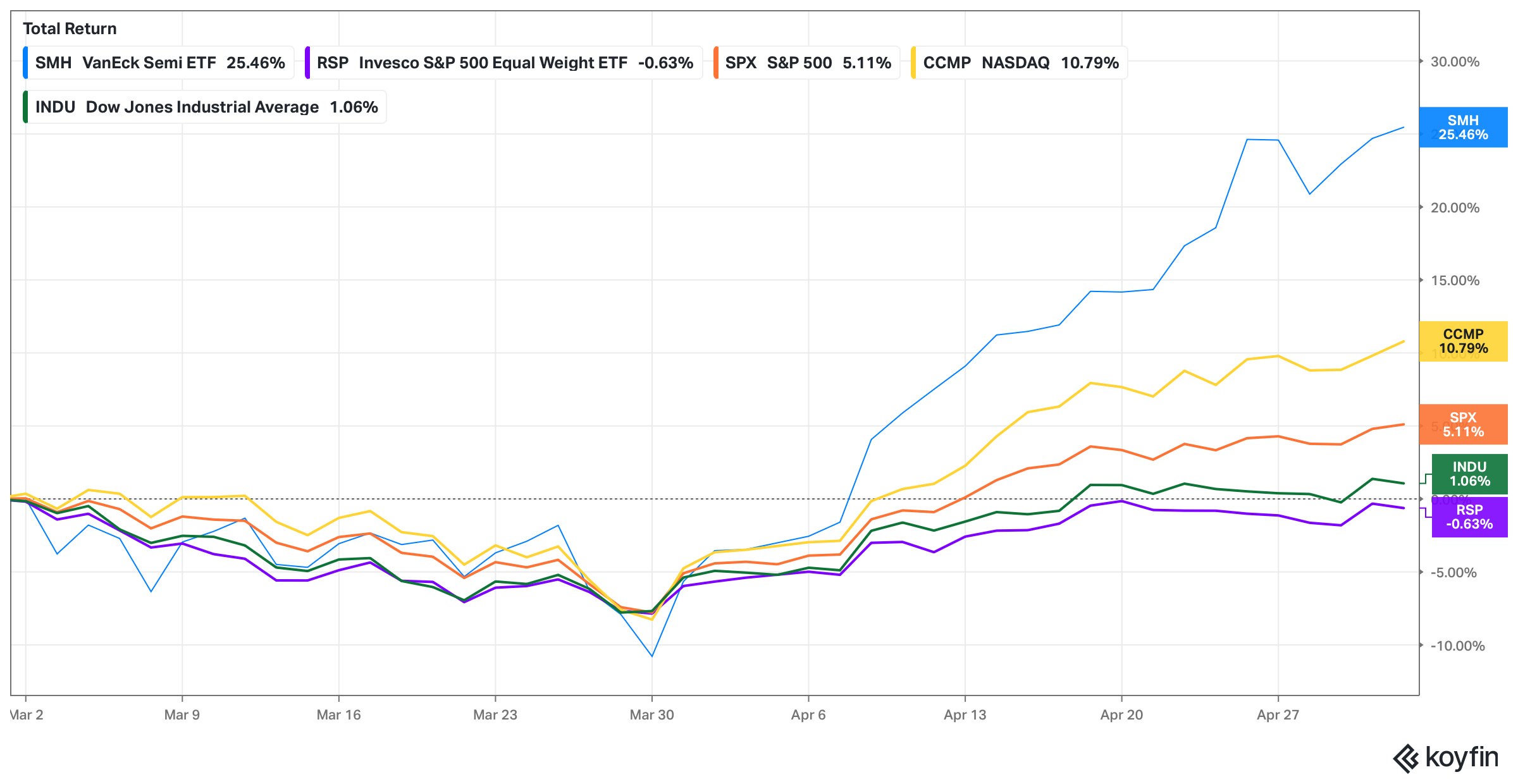

However, the rise in US equity markets was driven by a handful of AI Capex beneficiaries, while “real” economy stocks have lagged globally (since the war began).

Nevertheless, the US seems to be the least affected by the war, and, in fact, its net energy-exporter status will likely benefit the competitiveness of the US industrial base as it aims to reindustrialise.

This week, we saw major central banks reiterate their commitment to suppress inflationary pressures despite sluggish growth projections. The global hawkish tilt, as the war drags on, shouldn’t come as a surprise to seasoned macro watchers.

Due to our cautious stance, our high cash holding (26%) was a drag on our performance as the PF is up 4.2% YTD compared to the benchmark return of 4.42%.

Note that we significantly reduced cash mid-week and were lucky enough to do so promptly.

Let us take a deep dive into the macro universe and comprehend the cross-asset reactions!

US/Equities/Bonds/Oil/Dollar/Gold/Agri/BTC!

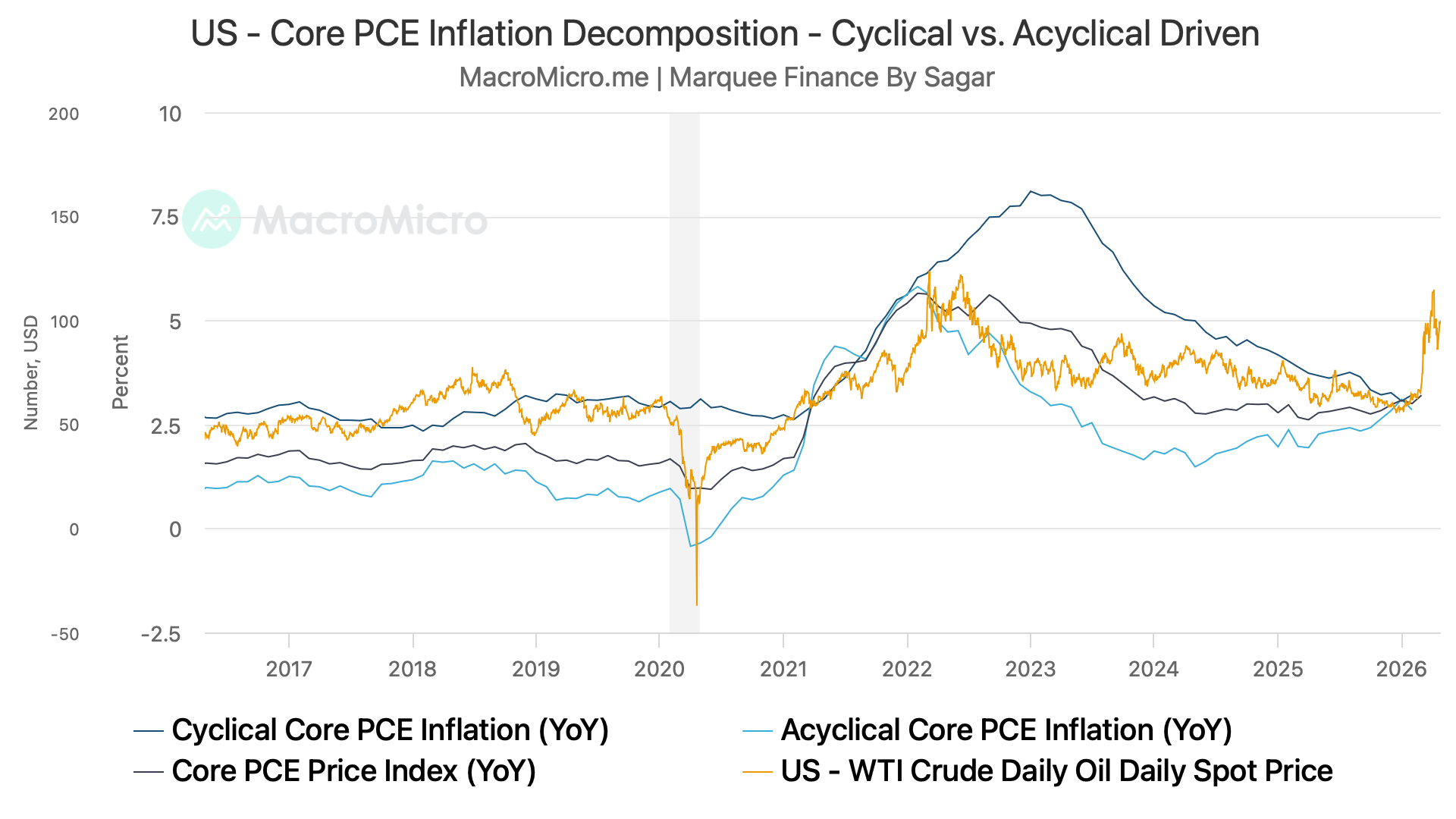

Fed’s preferred inflation measure: the PCE came in bang in line with the estimate.

The headline PCE came in at 0.4% MoM vs 0.4% MoM. Furthermore, Core PCE also came in at 0.4% MoM v/s 0.4% MoM.

The trend is undoubtedly up, as we can observe from the chart. Furthermore, the cyclical PCE is indicating signs of bottoming out.

We can also conclude that CPI is a lagging indicator, and we can predict with certainty that higher oil prices (sustained) lead to higher CPI, albeit with a lag of 2-3 Quarters.

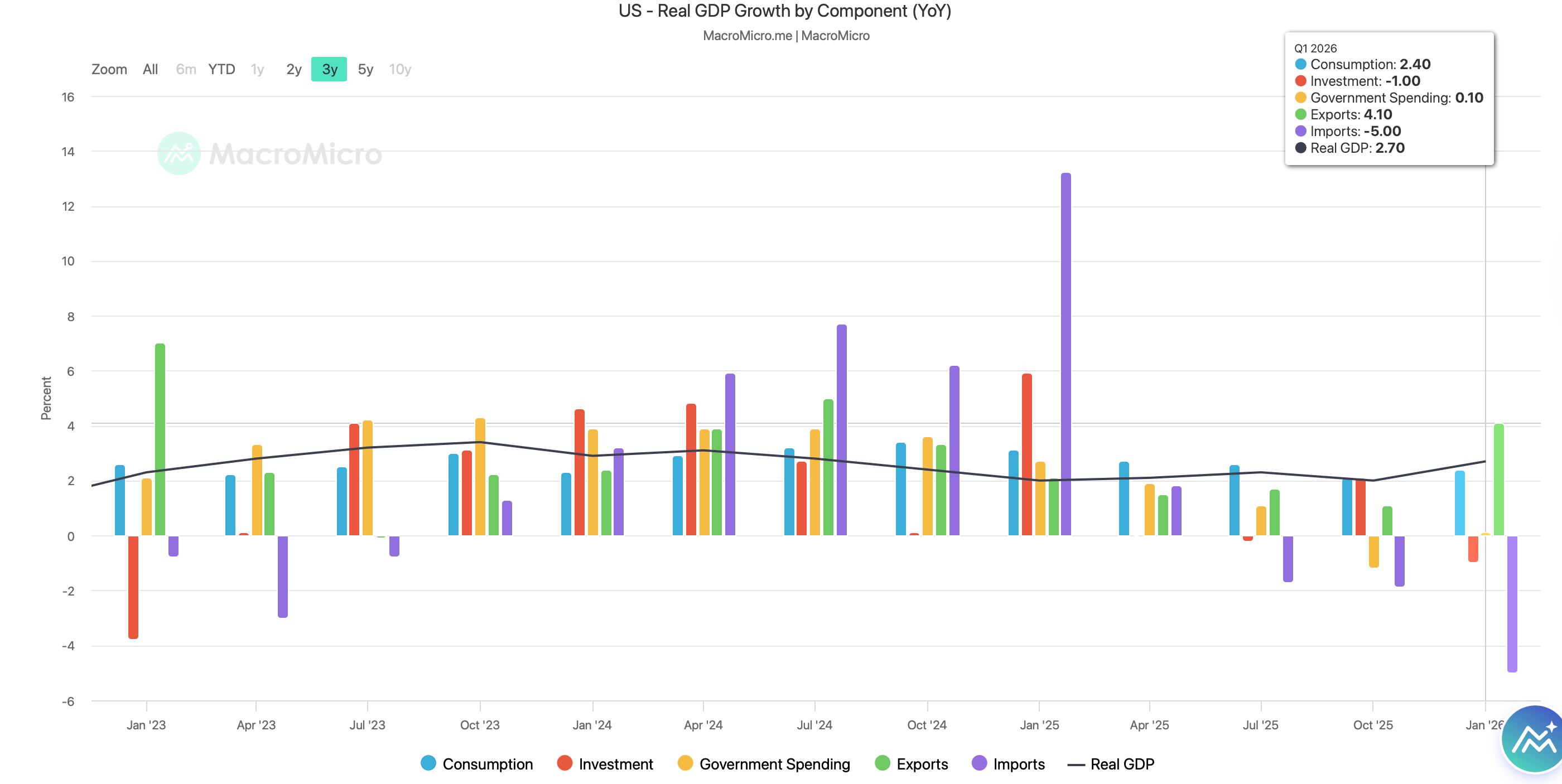

Long-term subscribers will appreciate that we are not big fans of GDP (a backward-looking indicator prone to revisions).

While inventory changes supported growth, net exports were a drag.

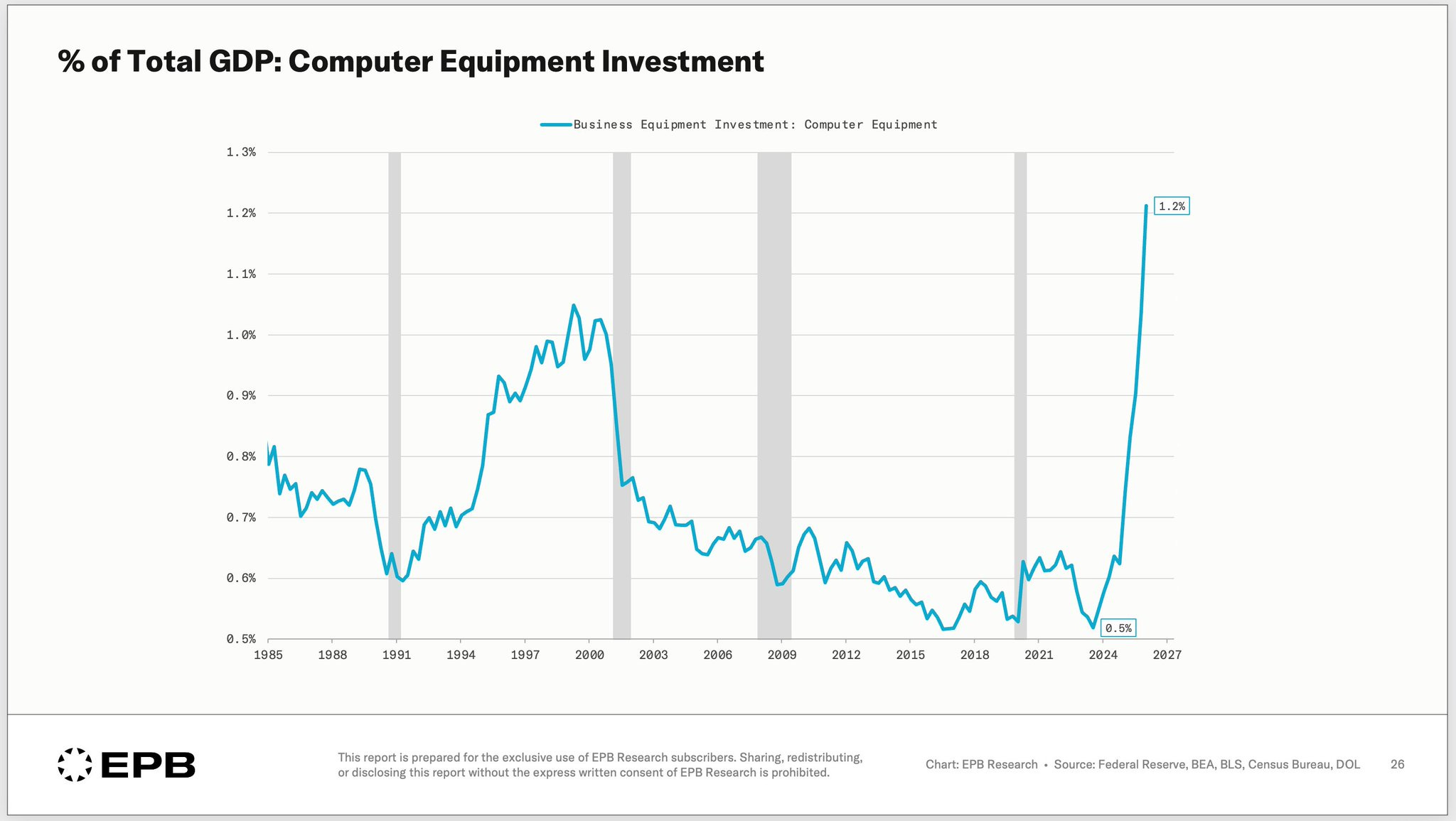

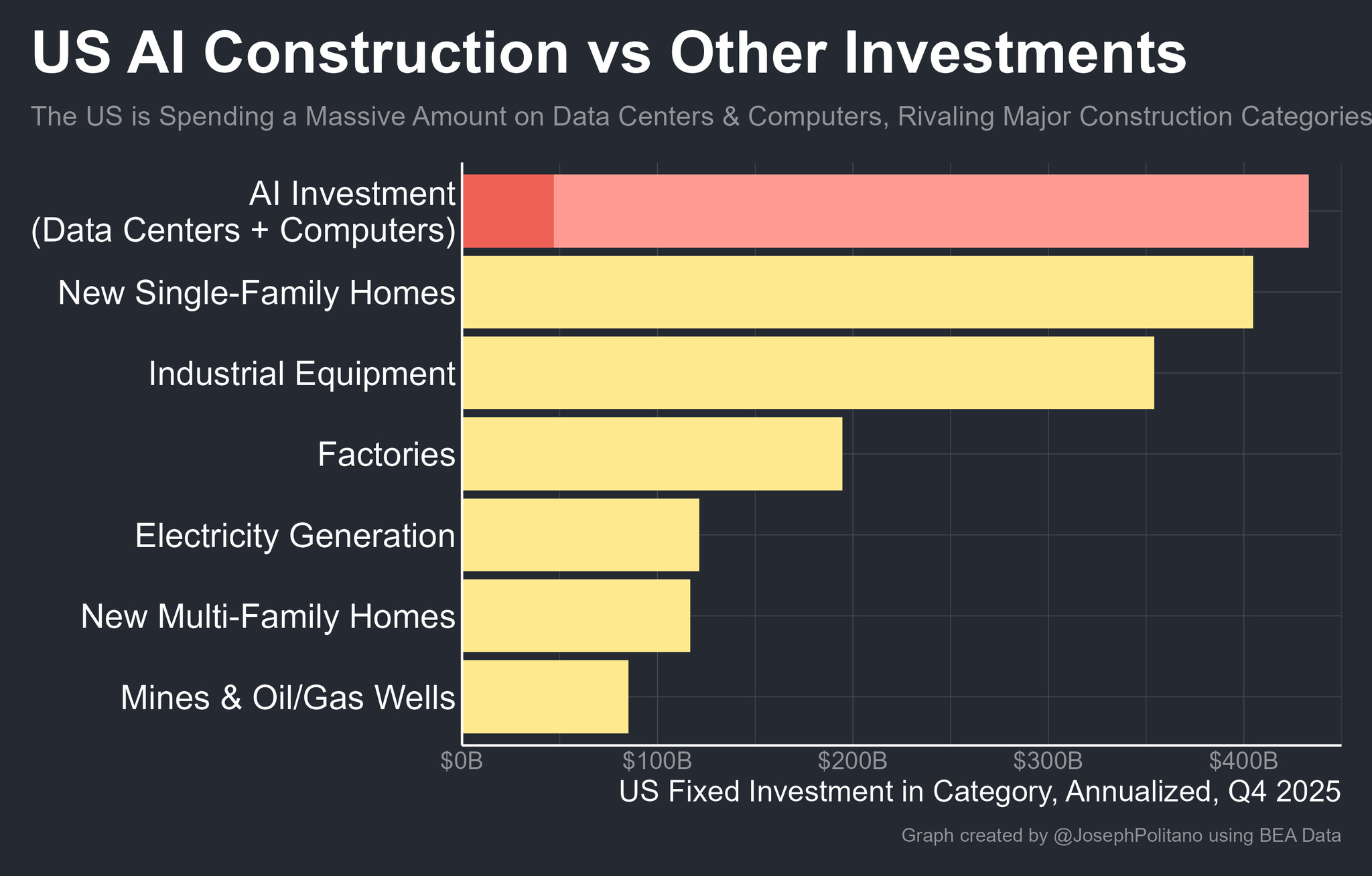

One of the significant takeaways was the explosive growth in the Computer Equipment Investment (AI Capex).

We have now surpassed the dot-com levels, and Computer Equipment Investment as a % of Total GDP has exceeded 1.2%.

In fact, a large proportion of the incremental growth in Q1 came from AI investments, which have now overtaken even New Single-Family Homes investments!

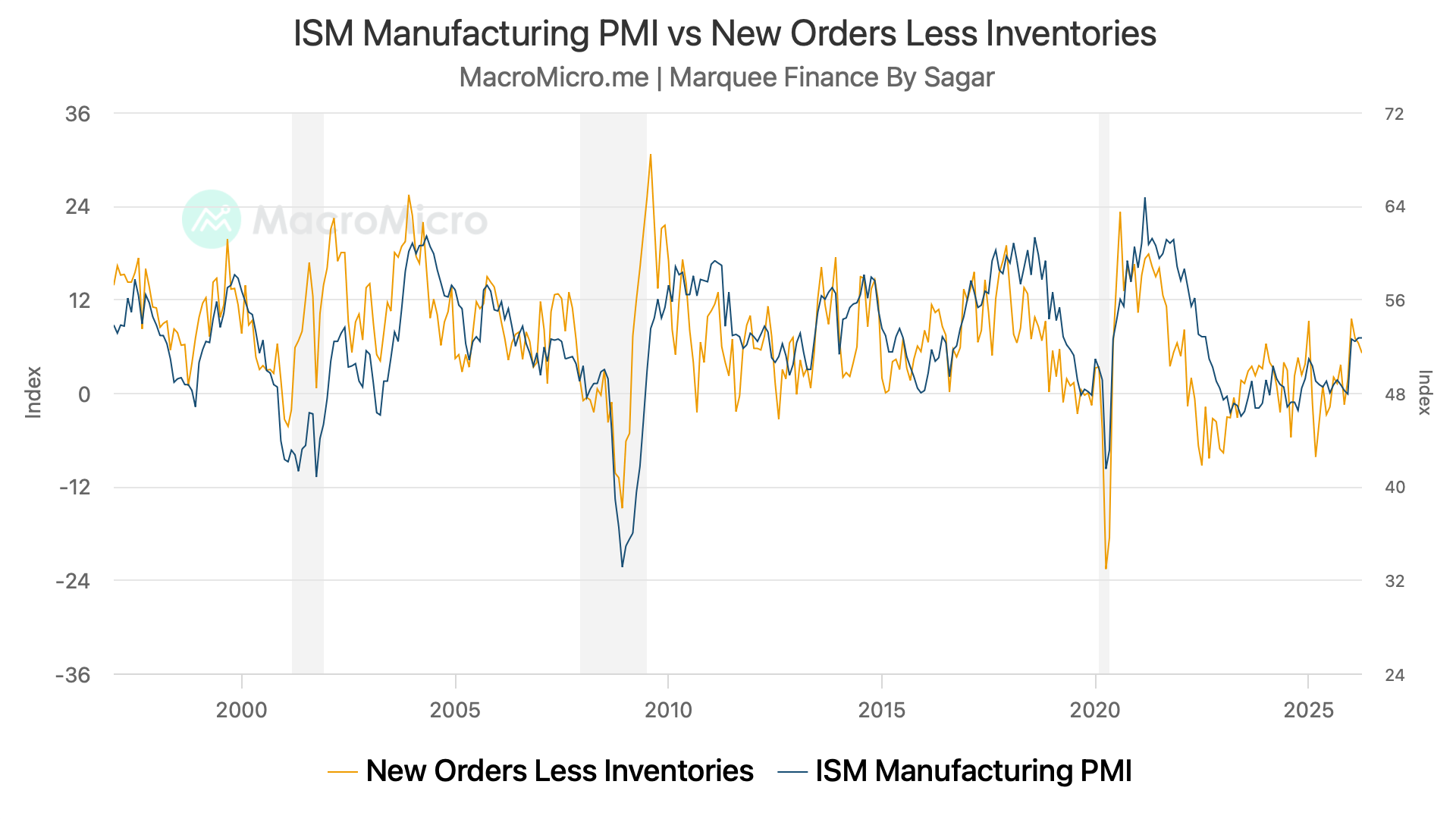

ISM Manufacturing came in slightly below estimates, with the headline index at 52.7 vs 53.2 expected.

Our preferred gauge, New Orders less Inventories, also softened; however, we believe the slight blip is due to the supply chain disruptions arising from the Middle East conflict.

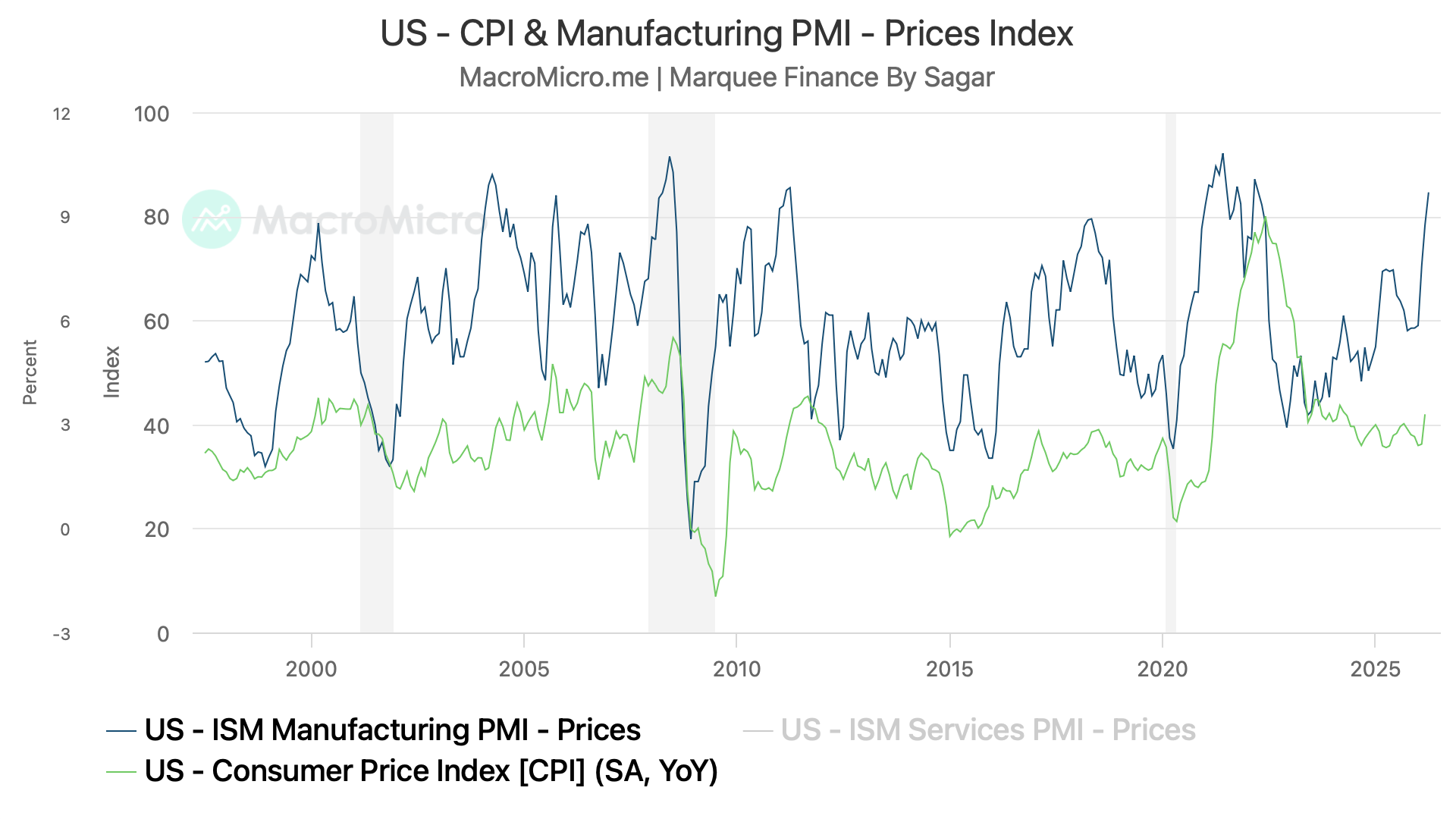

The biggest surprise was the ISM Manufacturing Price Paid, which came in at a whopping 84.6 and is now reaching the levels last seen in 2021.

Note that although correlation with the CPI is weak (ISM Services Prices Paid has a higher correlation), the trend (CPI) can be extrapolated.

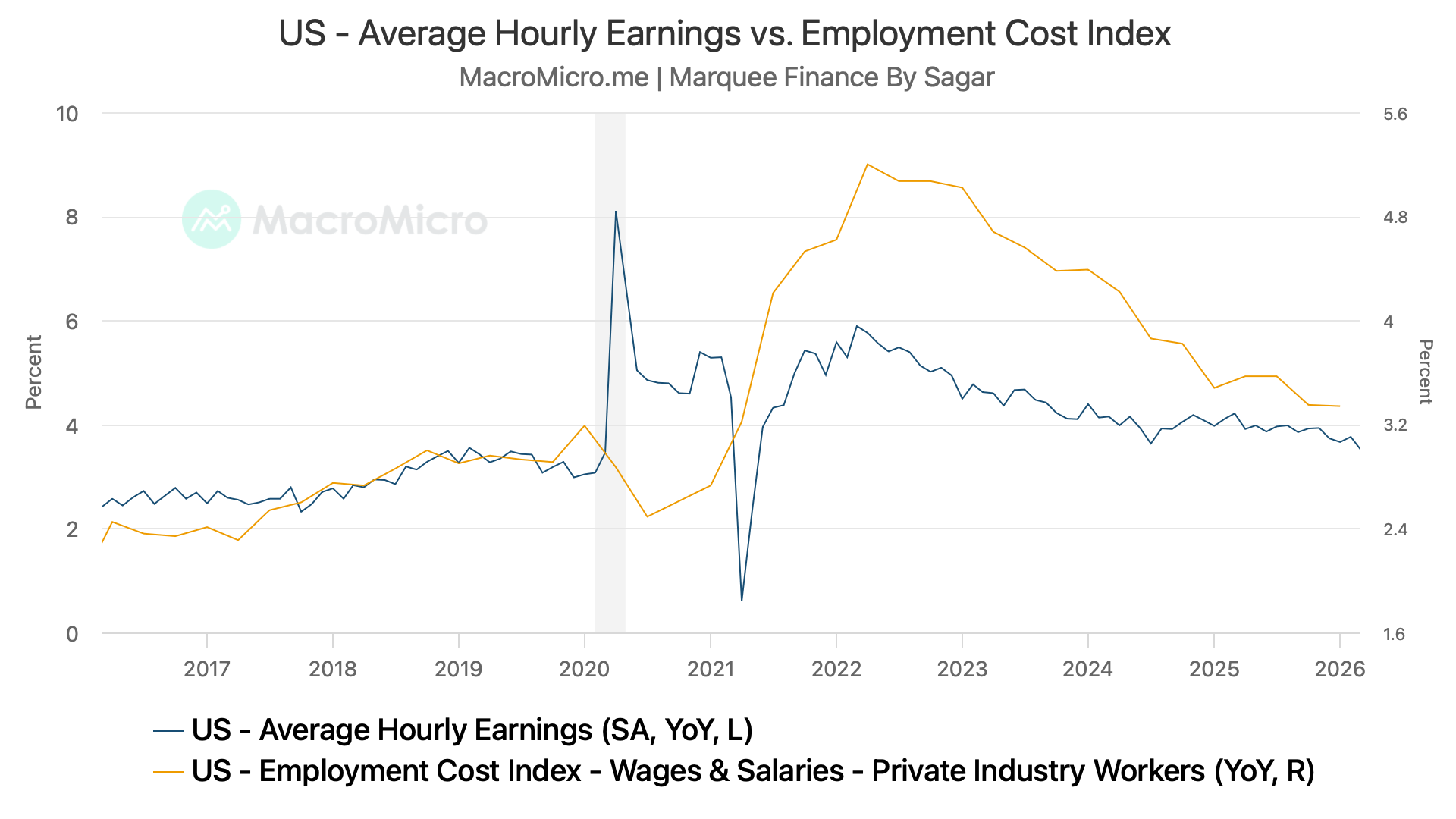

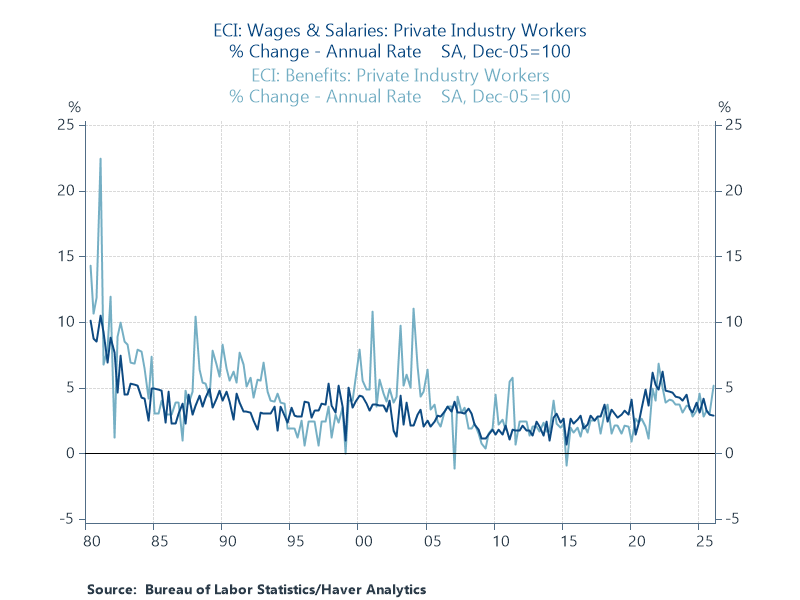

One of our favourite metrics for tracking wages in the labour market is the ECI (Employment Cost Index), which came in higher than expected at 3.35% YoY.

However, higher ECI was driven more by “Benefits” than by wages.

Thus, real wages (adjusted for inflation) are on the verge of turning negative as inflation outpaces them. This will be a significant hit for the consumers.

There was a slight change in the Fed statement, prompting market participants to call the meeting a “hawkish” hold.

“Inflation has moved up and is elevated, in part reflecting the recent increase in global energy prices.”

Furthermore, three Governors dissented from the inclusion of “Easing bias” in the statement. While Miran, as usual, dissented in favour of a 25 bps cut.

The uncertainty arising from the situation in the Middle East is making the Fed cautious, and we don’t expect any change in the language or the decision (on hold) unless absolute clarity emerges from the State of Hormuz.

“You know, we have so much to learn and there’s so much uncertainty about the path ahead, there doesn’t need to be any rush to make that decision now because, you know, what happens in the next 30, 60 days, even by the next meeting, could really change the picture around that -- around that language.”

“And so maybe a little bit of restriction or the high end of neutral is just the right place to be. So, we can wait here and see -- and see how things work out before we act.”

If you have been wondering why the US has outperformed RoW since the war began, JayPo apparently mentioned it explicitly during the presser.

“We’re also -- you know, as I mentioned, we’re an oil exporter so we’re not feeling the same kind of pain, and we’re not likely to feel the same kind of pain that economies in Western Europe and, certainly, in Asia are feeling.”

On the labour market, the dynamics of which we have been indicating for the past few months are “Low Hire, Low Fire”, an unusual market given the wild swings we have witnessed since the pandemic.

Interestingly, JayPo calls this a “balanced” labour market, but we believe it’s a fragile market prone to sudden shocks.

So that’s a -- that’s -- you know, in a sense, the labor market is in balance, but it’s an unusual and uncomfortable kind of a balance where people who don’t have jobs will have a hard time breaking in unless somebody quits their job.