Confusion, Madness And Illusion!

Confusion!

The sordid state of affairs at the world’s largest central bank was again visible this week. Fed has committed a string of policy errors in the last three years.

Ironically, when the economy was resilient, and inflation resurgence was a high probability, the Fed delivered a premature dovish pivot in December 2023 with markets pricing in seven rate cuts for 2023.

Now, when there are signs of a growth slowdown, the Fed came out hawkish with only one cut for the remainder of the year (as per dot plots), committing another policy error.

Undoubtedly, confusion and extreme political pressure reverberate in JayPo and fellow members of the Federal Reserve.

Madness!

The greedy Wall Street has left no stone unturned to turn the markets into gambling dens with companies with trillion dollars of market cap trading like crypto shit coins.

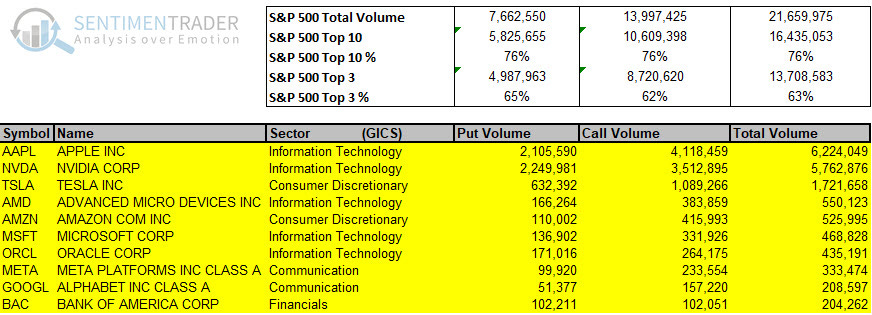

Example: On Wednesday, Apple, Nvidia, and Tesla accounted for 63% of the S&P 500's total option volume. Yes, you read it right. Let that sink in!

We are witnessing history, with all the liquidity in the world chasing 4-5 companies, thus creating a gigantic bubble.

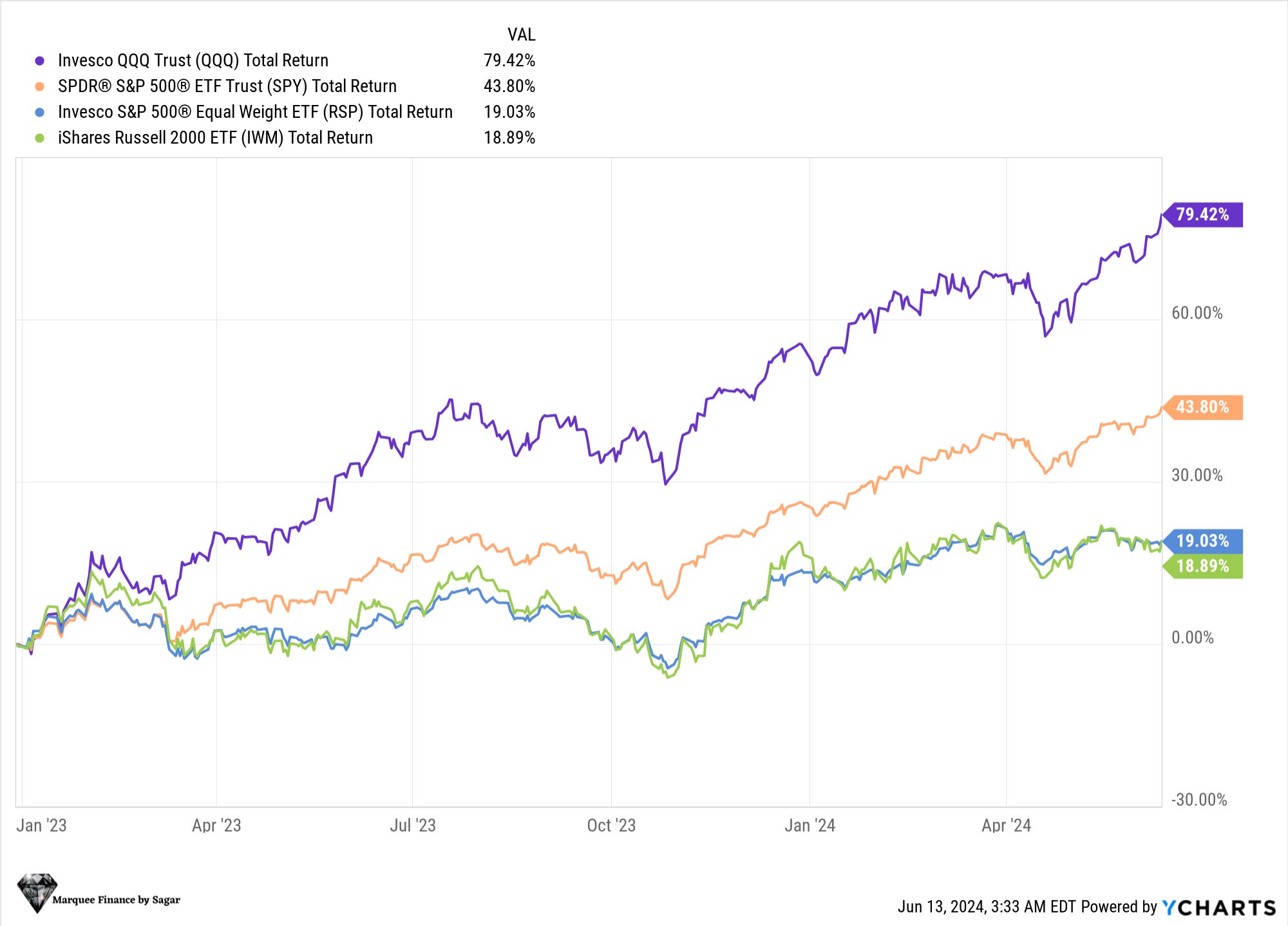

In fact, NDX/QQQ has been up by more than 80% (Total Returns) since bottoming on 29 December 2022, almost mirroring the rise seen in QQQ from June 1999 to March 2000 (100%+).

On the contrary, Small Caps (IWM) and the S&P 500 Equal Weight Index (RSP) have given subdued returns, thus indicating that most of the returns can be attributed to the Mag 6/7.

Illusion!

With confusion and madness, risk assets and credit markets buoyed by abundant liquidity have now reached unprecedented levels of illusion by factoring in a “perfect” soft landing.

However, this is somewhat influenced by the poor data quality, which even the Federal Reserve now acknowledges.

“There is an argument that payrolls may be a bit overstated”- Jerome Powell.

Let us dig deeper at the macro data to infer about the trajectory of the global economy.

US!

It was a data heavy week with a slew of macro data releases. All eyes were on the inflation data as it was the same date as the FOMC policy decision.

The headline number came in lower than expectations as the goods deflation picked up pace.

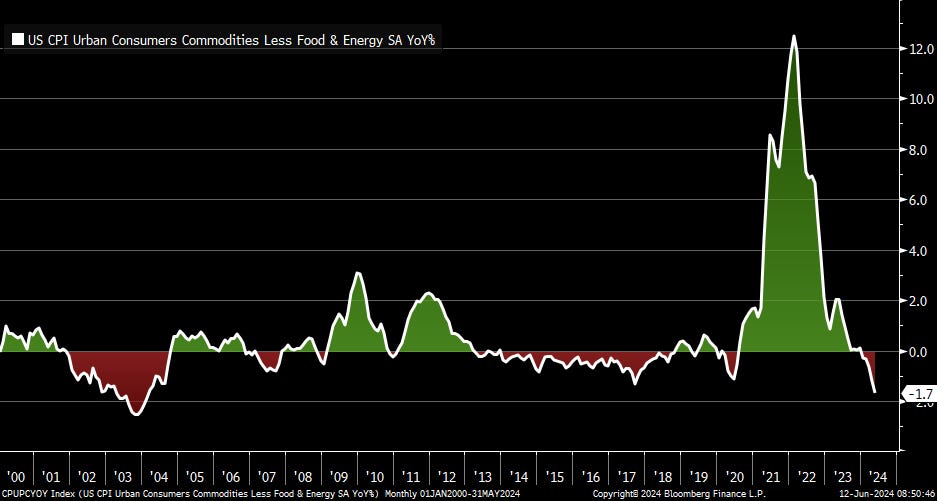

In fact, surprisingly, the core goods deflation is indicating a big red warning signal.

The core goods deflation came in at -1.7% YoY which was the lowest print since Feb 2004.

Nonetheless, one can argue that the base effect will catch pace and there are shipping disruptions which can lead to some upmove in H2.

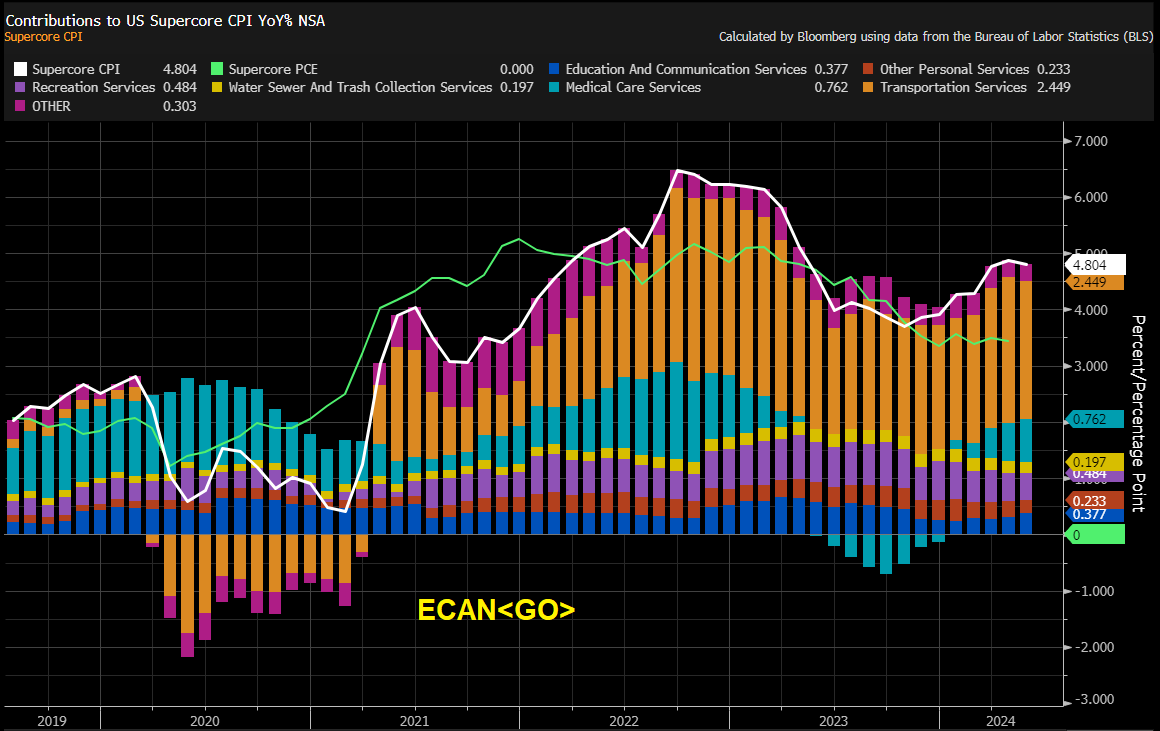

However, the real surprise was the metric that JayPo popularized post covid. Supercore or Services Ex-Housing, though still elevated at 4.8% YoY, came in at the lowest level/ negative MoM print since September 2021.

Overall, the inflation print (including the PPI) was a softer one.

We had earlier guided for a number of somewhere close to 3.5-4% by July (second wave) but had clearly mentioned that if the inflation misses this estimate, then it would mean that