Controlled Demolition!

“Tariff is the most beautiful word in the dictionary”- Donald Trump.

Most market participants believed Donald Trump would use tariffs as a negotiating tool. However, to everybody’s surprise, tariffs have been implemented at mind-boggling rates.

There is a near consensus that the tariff war will snowball into a global trade war (Trump 1.0 was a China- US trade war; Trump 2.0 will be global).

As a result, markets are extremely worried with cross-asset movement, suggesting a safe haven demand for commodities as a hedge against a “stagflationary” scenario.

Those who have been into markets for years agree that equity markets always need a reason to revert to mean, and they got one with the POTUS policies.

The relentless selling in equity markets has been accompanied by a modest rise in the Voltility Index (VIX), indicating that the selling has not been a panic event but enormous deleveraging by institutions.

As a result of the drawdown, index valuations are now reverting to the mean. Note that we have witnessed no earnings downgrades but just multiple contraction.

If the Trump administration's policies cause a mild recession in the near future, earnings downgrades will occur swiftly, and then there can be an extended drawdown.

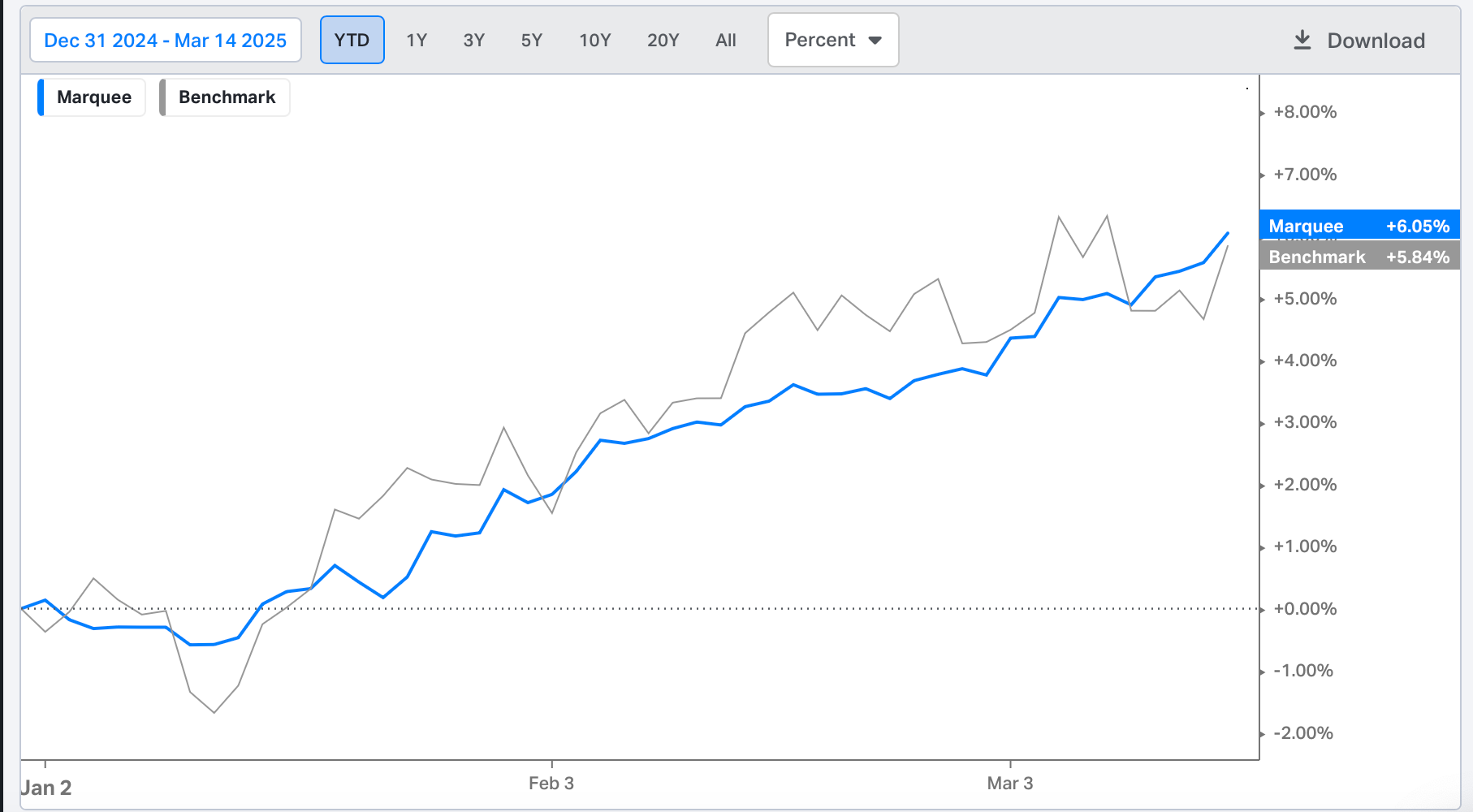

We have been preparing for this scenario in the portfolio, and as a result, we have outperformed our benchmark with a YTD performance of more than 6%.

[Benchmark: 60% (MSCI World EX-US), 40% (Bloomberg Global Aggregate)]

Also, we are happy to inform you that our portfolio continues to hit all-time highs despite market turmoil.

Let’s explore the global macro universe in depth while examining some intriguing technical charts of Mag 7 and cross-asset markets.

US/ Bonds/ Gold!

The week was lined up with a plethora of macro releases. Focusing on the macro data is imperative as the market is extremely concerned about the rising risk of a recession in the world’s largest economy.

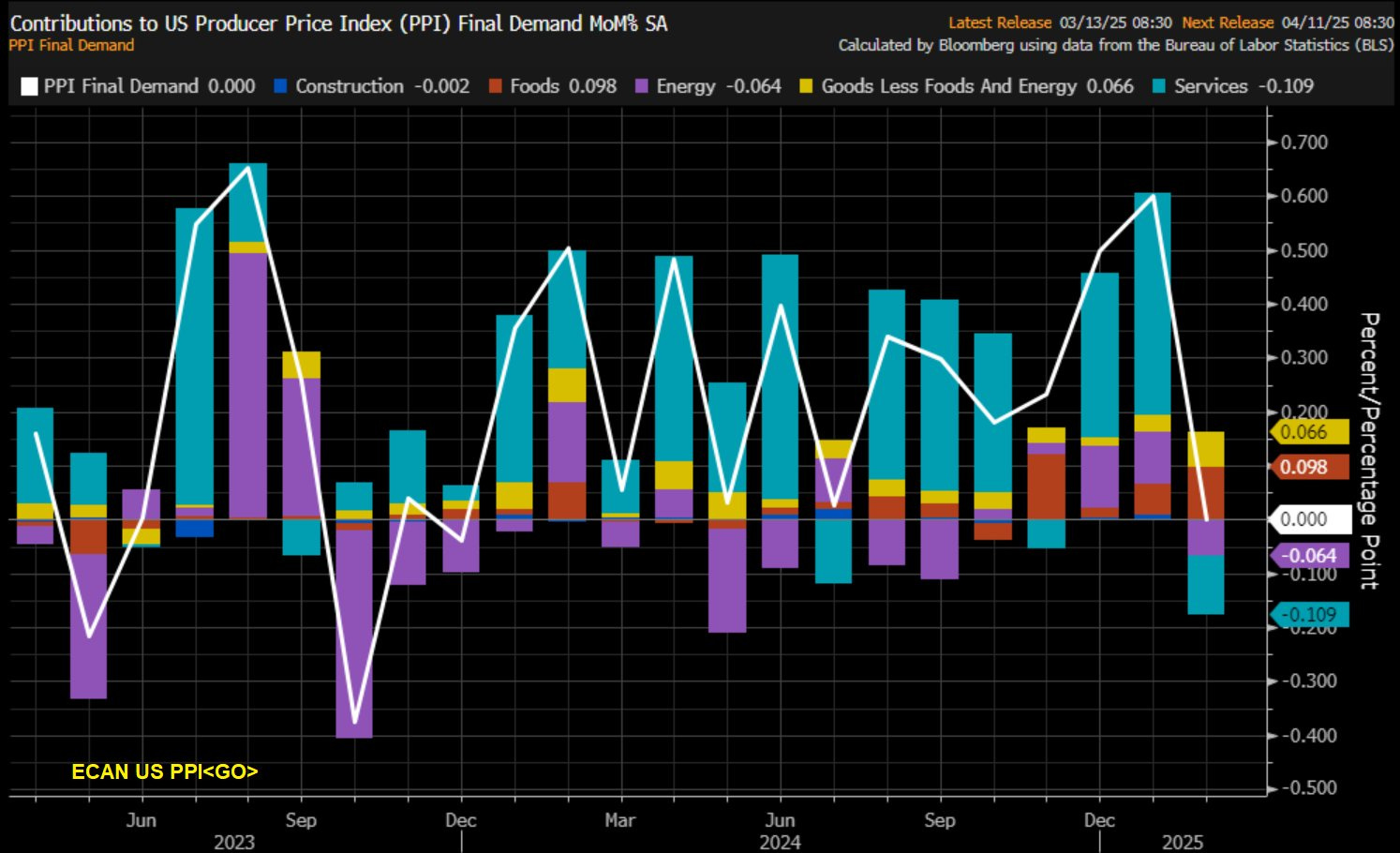

We begin today with Producer Price Inflation (PPI), which was softer than expected. Core PPI came in at -0.1 % MoM, compared to an estimate of a 0.3% rise.

Notably, this was the first negative reading since July. The internals indicate that energy prices and services dragged PPI lower (mainly due to a 1.4% decrease in margins for machinery and vehicle wholesaling).

Nonetheless, the revisions were stark, as last month’s figure was revised up to 0.6% MoM. Therefore, one must watch for the trend, as this report had several one-offs.

The CPI came in softer than expected, with the headline index at 0.2% MoM (2.8% YoY), compared to an expectation of a 0.3% rise MoM (2.9% YoY).

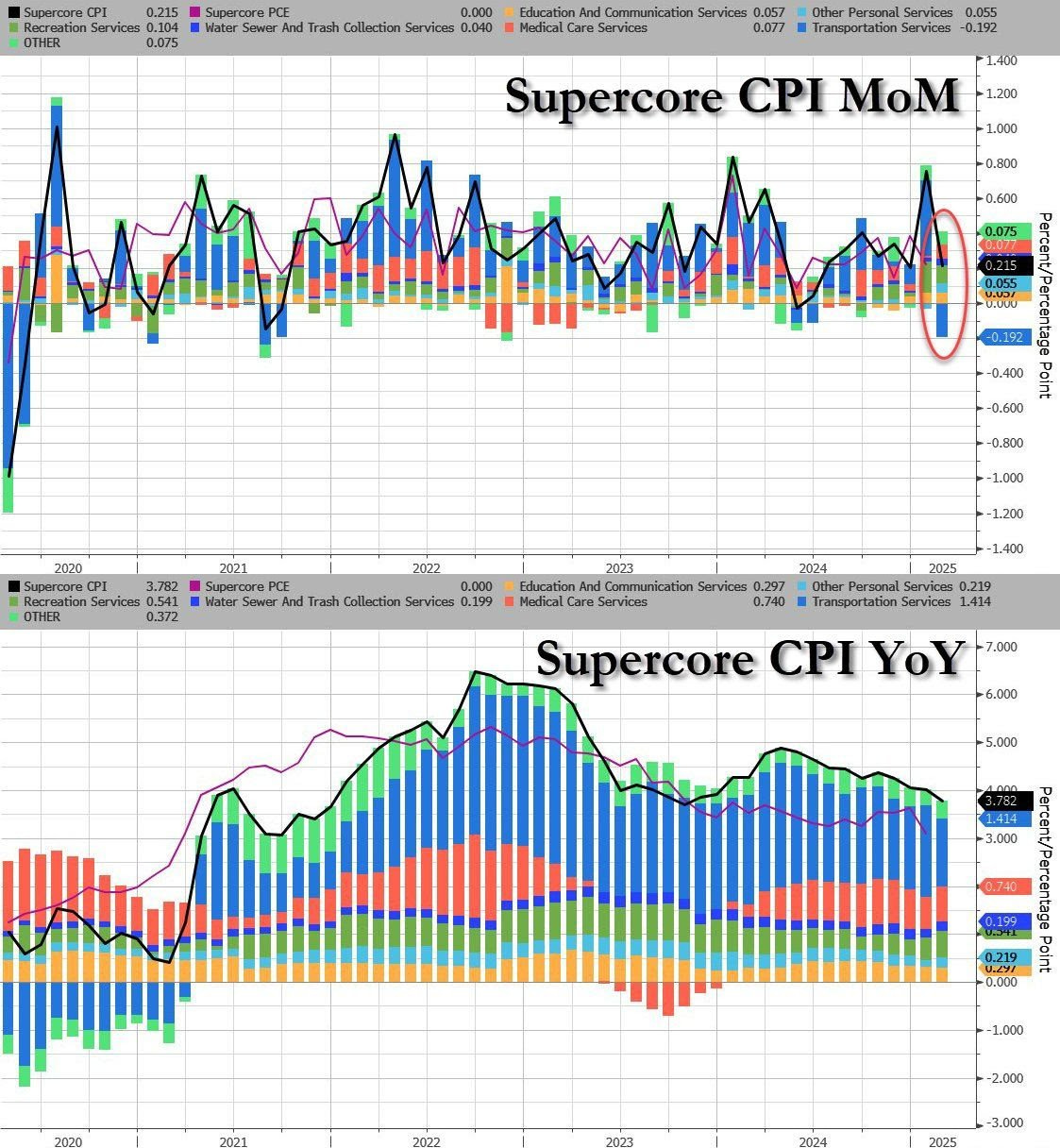

Supercore CPI (Services Ex-housing) was an absolute shocker as it came in at 0.215% against an expected 0.38% (rounding makes it 0.2% vs 0.4%).

Interestingly, the miss was due to the transportation services, a sticky component of the Supercore CPI. Furthermore, the YoY number came in at 3.7% (still elevated).

Nevertheless, if the trend is down, it could be welcome news for the Fed (not for the equity markets, though, as lower inflation means a slowing economy and eventually lower earnings).

As always, we move to our guidance for the next few months.

We believe that there is a high probability that the inflation will..