Cracks In The AI Story?

Given the equity price action in recent weeks, you will be astonished by today’s title.

Well, folks, we have always believed that AI is a game-changer; however, we have always been wary of the trillions of dollars in capex spending by the hyperscalers, as such gargantuan amounts of spending are only “justified” if they can generate high returns (historically, these companies have generated 20%+ ROCE) on their investments.

This week, we saw what we've been warning about for months. The AI “revolution” was expected to cut costs and boost productivity, but companies using AI for automation are experiencing increased expenses.

Microsoft cancelled its internal Claude Code licenses this week after token-based billing made the cost untenable, even for a company with effectively infinite cloud resources. Uber's CTO sent an internal memo warning that the company burned through its entire 2026 AI budget in just four months. American AI software prices have jumped 20% to 37%, and GitHub (owned by Microsoft) is switching from flat-rate plans to usage-based billing across its products.

Token-based billing will make it challenging for enterprises to adopt AI at scale if AI Labs continue to raise prices.

The so-called “doomsday” scenario suggested by some prominent Substack writers cannot occur if you believe in unit economics.

Additionally, the claim that “Software is Dead” was propagated by short-sellers, and we are on the verge of seeing a strong resurgence of software as hardware gets a reality check due to the multiple constraints of a large-scale AI rollout.

Nonetheless, AI is the future, and thus, one needs to incorporate AI into their workflow. We use MacroMicro for our macro analysis, and they have also launched the MM AI Bubble, where you can chat with their AI.

Furthermore, they will be launching the first-ever “Macro Terminal” in July.

The full MM AI experience will be available only with the MM Max Annual plan. This link gives you a 14-day trial of the discounted Max Annual plan (you can change the language to English). You can also lock in the current annual pricing before the official AI launch price adjustment takes effect.

Click on the link to lock in a significant discount!

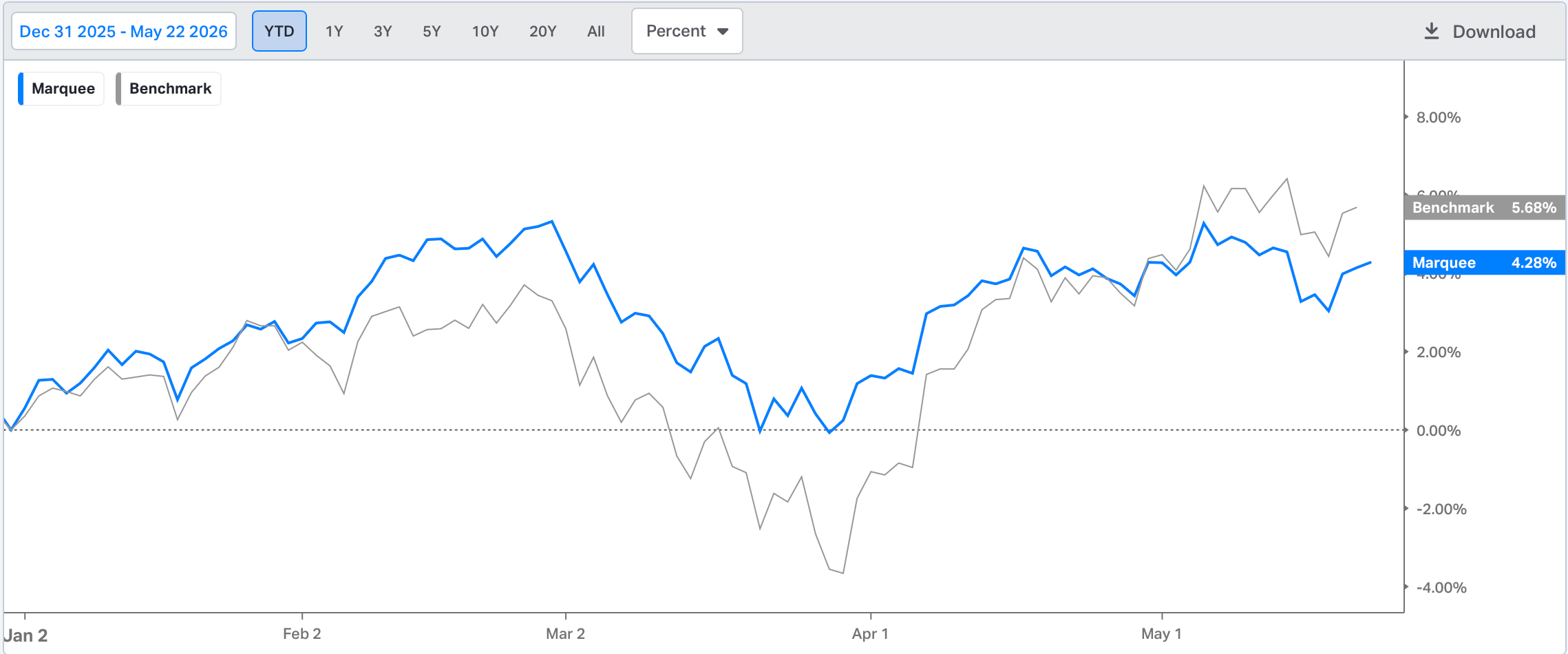

We recouped some of the underperformance this week; however, our exposure to China has weighed on the portfolio.

Nonetheless, we are pretty confident that we will once again outperform the benchmark as we head into June.

Let us take a deep dive into the macro universe and decipher the cross-asset price action!

US/Equities/Bonds/Oil/Dollar/Gold!

While it was a quiet week for US macro data, we will closely monitor consumer health in this week’s update.

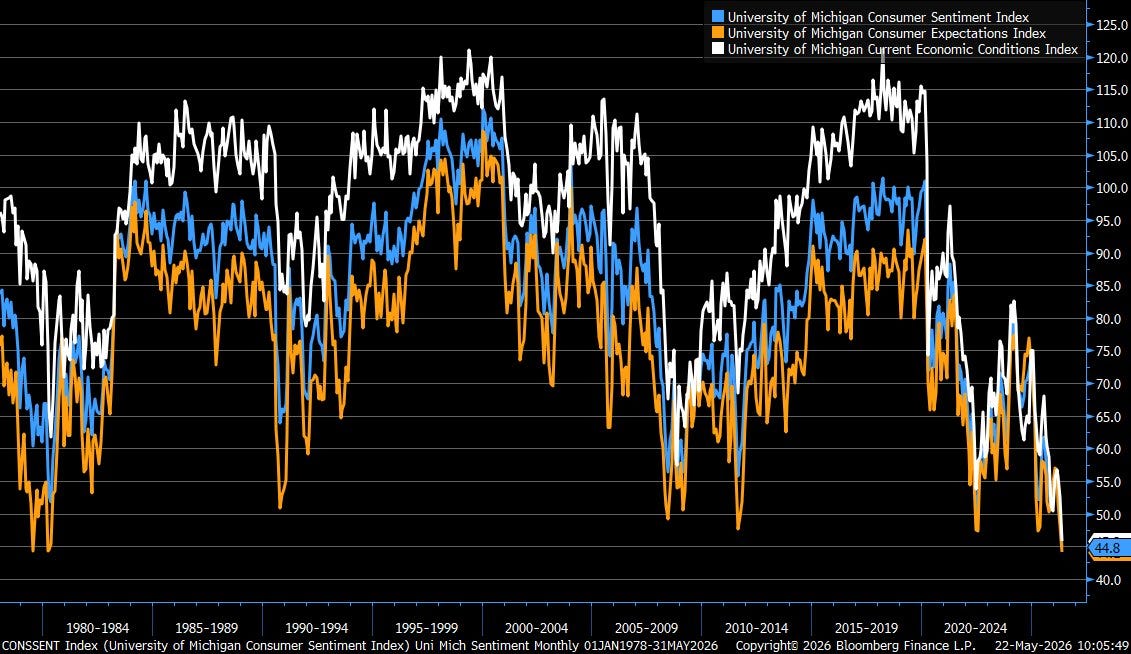

By far, the biggest talking point of the week was the Michigan Consumer Sentiment Index.

We rarely talk about this because we don’t incorporate this soft data release into our process; instead, we use other data points to gauge consumer health.

Consumer Sentiment Index plunged to a record low of 44.8, current conditions to 45.8, and expectations to 44.1. The whole survey was revised lower.

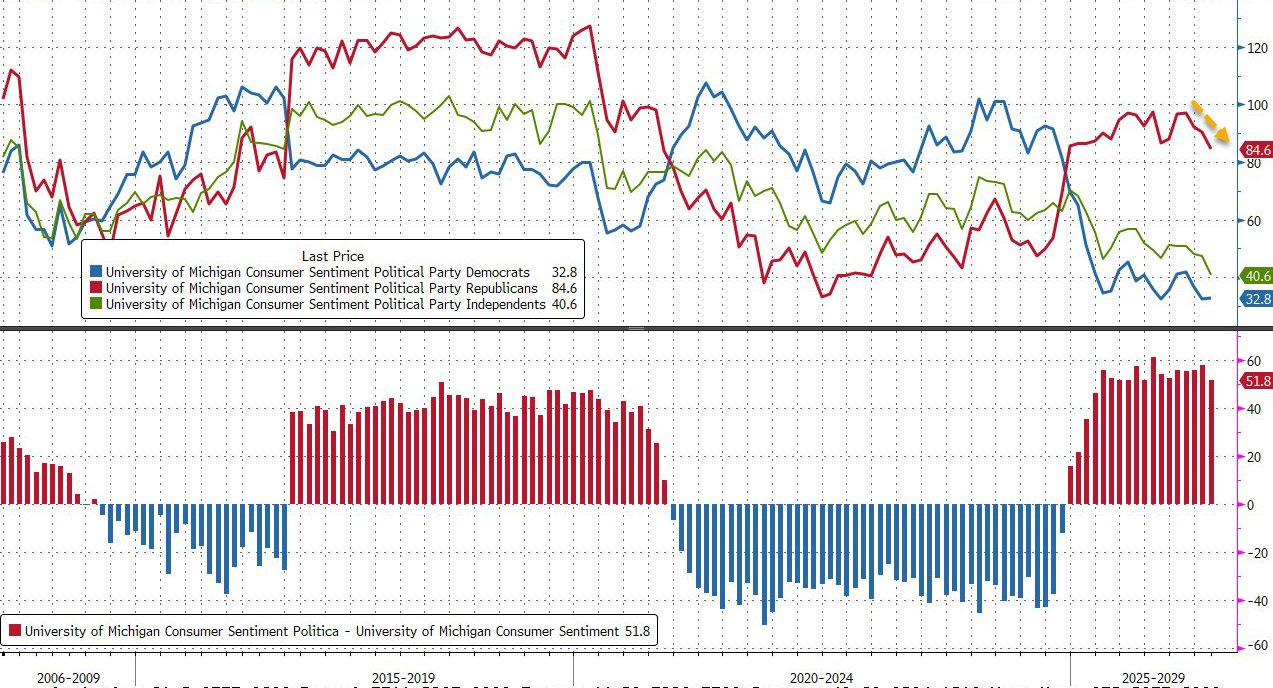

The Survey can be divided into different parties, and since we have a Republican President, the Sentiment (Democrats) is abysmally low at 32.8, while the Republican Sentiment is at 84.6 (but trending lower).

Nevertheless, undoubtedly, consumer health is fragile, and lower-income households are struggling the most.

This week's Walmart earnings also indicated that stress is now building among middle-income consumers. Notably, Walmart has been targeting households with an annual income of> $100k.

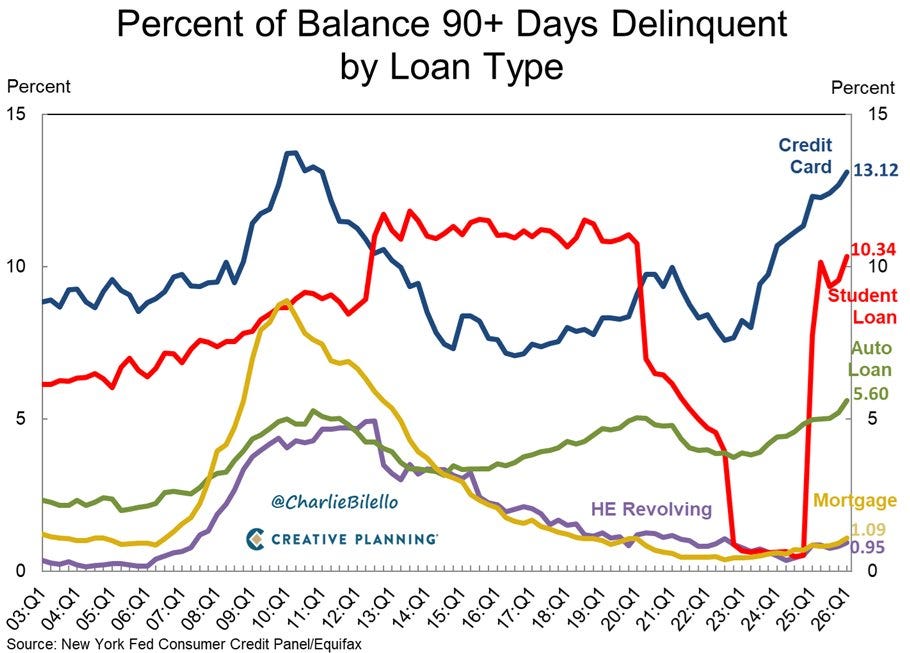

One of the reasons for stress has been the high APR on the credit card debt.

When we look at the Delinquency rates, the credit card delinquency rates are nearing GFC highs.

Note that auto loan delinquency rates are already at ATHs.

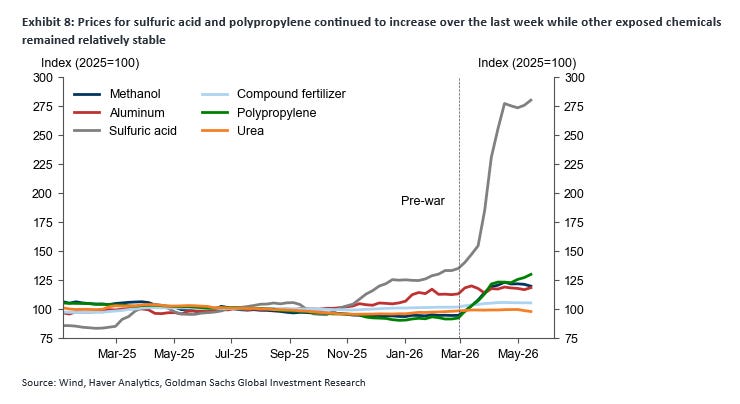

Before we end the macro section, we came across an alarming chart.

Sulfuric Acid is one of the most widely used raw materials in the chemical industry and in almost every other industry, especially in the fertiliser industry.

Post-war, China halted the export of Sulfuric Acid, and its price has nearly doubled.

Thus, inflation is not going away easily.

We also received the Fed minutes this week, and, as everyone is aware, the Fed is divided due to the twin shocks (tariffs and geopolitical).

Once we start hearing from Warsh, we will know the Fed's direction (hawkish or dovish).

Equities!

It has been 32 trading days since SPX