Cracks Wide Open!

Hurricanes are one of the most powerful and destructive storms that form over warm ocean waters near the equator. These tropical storms require key ingredients, such as sufficient moisture and atmospheric instability, to transform into a powerful force. However, there are rare occasions when, despite favourable conditions, these storms fail to materialise into a hurricane.

Last week, we wrote “A Perfect Storm” as we were able to connect the dots and foresee a hurricane hitting the world’s largest economy soon. However, despite the “key ingredients,” there is always a probability that the economy will avoid a hurricane.

Today, we dig deeper and look at the following macro variables to conclude our assessment of the US economy. We will comprehend:

Lending Standards and Credit Conditions.

Consumer Credit.

Economic Surprise Index

Liquidity

Note that we have already churned our portfolio in the past few days in accordance with our expected outcome of the current business cycle in the US.

In Europe, the BOE delivered a “dovish” hold, and Riksbank cut rates for the first time since 2016 as markets gear for the rate cuts in the developed world.

In the East, the FX market upheaval continues as USDJPY, which is literally trading like a meme coin, hovers around 155 levels despite the BOJ intervening twice last week and burning $60 billion of precious FX reserves.

Let us begin one of the most important newsletters of 2024!

US!

This week was a data “light” week, with markets obsessed with the Fed, moving primarily as the Fed speakers put on their diverse views about growth and inflation trajectory.

Thus, today, we will look at some intriguing macro data points that indicate the “true” picture of the US economy.

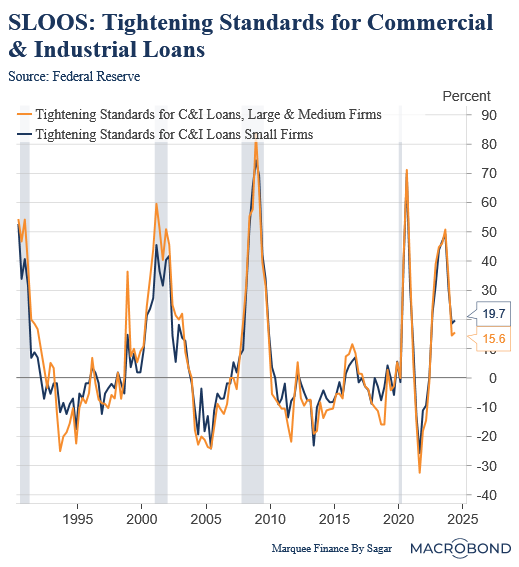

Let us start with the quarterly Senior Loan Officer Survey (SLOOS), which has an incredible track record of predicting recessions. During economic turmoil, banks become wary of lending to the economy (especially to vulnerable sectors), thus choking the economy's lifeline (credit).

Note that the spike we saw last year was due to the one-off unprecedented event in which SVB and Credit Suisse failed, leading to banks tightening lending standards across the board.

However, one man's loss is another man’s gain, which led to the private credit filling the void. As a result, private credit boomed, which has its own repercussions (tighter HY/IG spreads leading to low vol regime)

The latest SLOOS Survey demonstrates that banks are slowly tightening the lending standards again after easing them for Q423.

Nonetheless, we have a brand new indicator (other than SLOOS) which portrays a scarier picture of the