D-Day!

Once again, our work has been validated as our guidance and prediction about the US economy and Japan, along with movements in the FX World and the Precious Metals, are coming out to be true.

Our stand since the last few months has been that a slowdown in the world’s largest economy will transpire in late Q4/Q1 2024.

In the past few days, economists from investment banks from Deutsche Bank to UBS have begun to announce the date for a recession.

Mr Market has begun to aggressively price in rate cuts beginning as soon as March, which will be likely in response to the weakening of the labour market and deteriorating economic conditions in Q1, as we have been writing since August.

When the markets were highly bullish on the Dollar, we predicted a top around 107 (and vice versa when DXY was at 99).

In the East, there are early signs that the BoJ is on the path to normalization, which we have advocated for the last few months.

Nonetheless, it would be as challenging in 2024 as 2023 has been.

I am in the process of writing the detailed Global Outlook 2024, which will be out next week.

Let us look at the plethora of macro data released this week and make sense of the global financial markets!

US!

The highlight of the week IMO was Fed member Waller’s statement:

“Good economic arguments that if inflation continues falling for several more months, you could lower policy rate.”

This statement led to rate-cut bets and aggressive bull steepening of the curve.

Remember that last month, we wrote that the bear steepening will be followed by a flattener and then a bull steepening.

The market’s focus has shifted from any “further” rate hikes to rate cuts bet, and the front loading has happened swiftly.

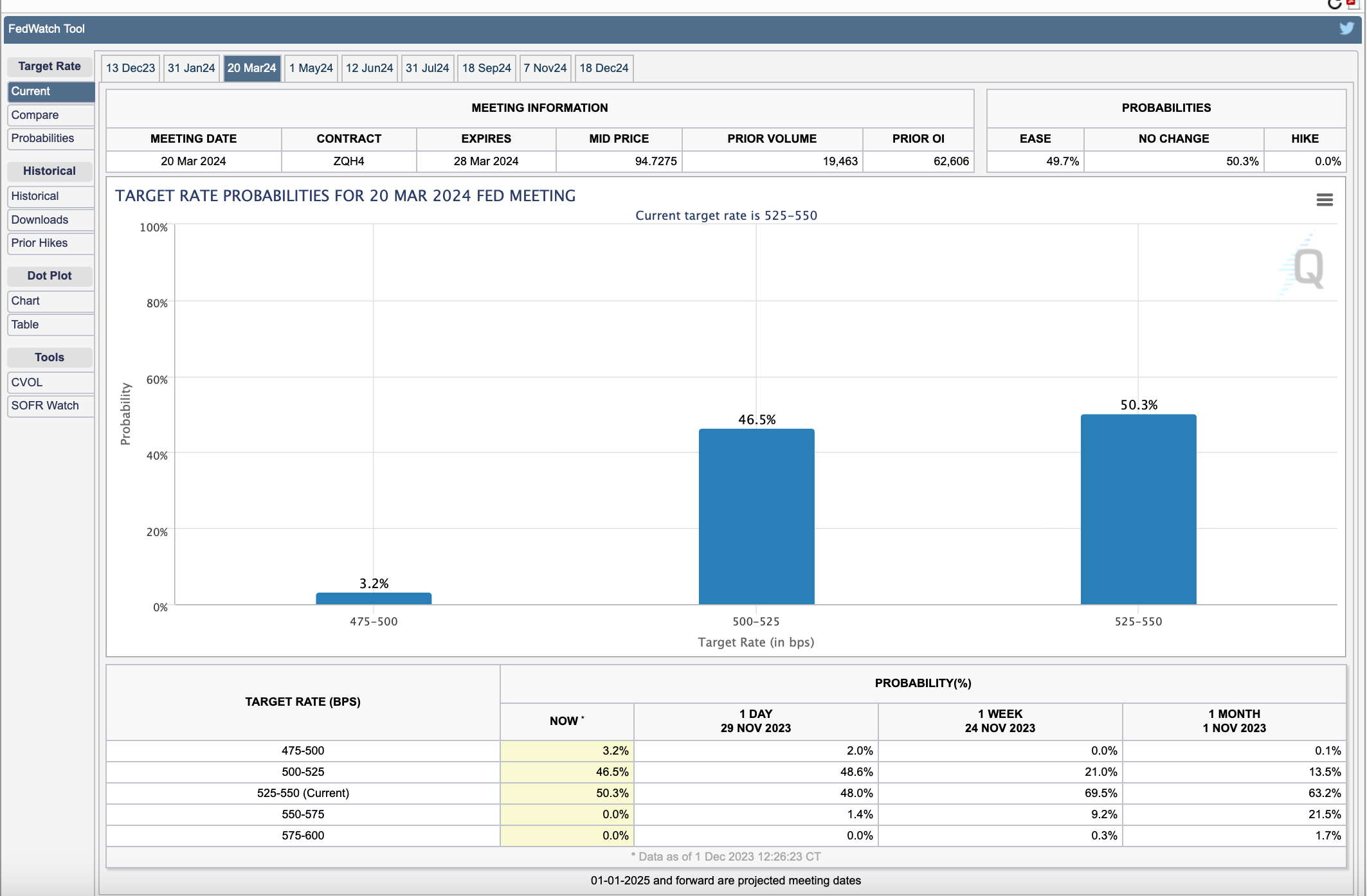

Markets are now predicting a probability of the first rate cut of 25 bps in the March policy which is just four months away.

The last policy was marked by JayPo using higher yields to justify the “tightening” of financial conditions, which has completely reversed in the last month.

While stocks (S&P 500) are up nearly 10%, the 10Y yield has plunged by almost 60 bps from the highs (one of the most significant moves in 3 decades).

Though we had been in the second wave camp (a moderate rise in headline CPI to 4-5%), the disinflationary trends are now becoming more powerful due to the weakening of the consumer and, thus, the economy.

One of the reasons for the strong disinflationary impulse in the global economy has been