D-Week Has Arrived!

As we head into the historic Federal Reserve’s FOMC meeting next week and one of the most significant Bank Of Japan (BOJ) meet, the macro will become one of the most significant drivers of the cross-asset movement.

Recently, we have observed that market volatility has risen exponentially, and even an “insignificant” piece of macro data results in outsized intraday moves in the markets.

In fact, the bond market movements are now comparable to the equity market movements, and even the volumes have surged recently.

The recent vol is now widely used by insiders to offload massive chunks of their stocks to the retail public (classic pump and dump). An example of one of the world’s largest companies:

Furthermore, as we get close to the historic elections in the US, the heat is rising. As the odds of winning of the presidential nominees oscillate wildly, financial markets reaction also tends to have extreme reactions.

Though we will not write about politics and stick to our macro expertise, some of the proposals of the Democratic nominee concern us and could have disastrous implications for the bond markets (worst-case scenario, higher long-term yields). The recent promises:

“My economic proposal includes $25,000 for first-time home buyers to help them with a down payment on a home.”- Kamala Harris (Twitter)

“And as president, I will work to cancel medical debt for millions of Americans.”- Kamala Harris (Twitter)

“When I’m president, I will take on corporate landlords that unfairly raise rents on working families.”-Kamala Harris (Twitter)

If fulfilled, the above will be quite inflationary for the economy and may lead to asset price inflation.

Nonetheless, we are still some time away from the election, and according to the betting market, it will likely be an extremely tight contest.

We got the CPI data this week which was the deciding factor for the “confused” bond markets (market pricing was 50:50 for 25/50 bps cut before the CPI data).

As a result, markets now price in a 25 bps cut by the Fed next week. (After yesterday’s Nikileaks article, markets are again pricing in a 50:50 odds for a 25/50 bps cut). Furthermore, the ECB also cut the rates by 25 bps this week.

We will also examine the macro data from the UK and the East to gauge the impact on the global economy and markets.

Let’s dig in!

US!

As we predicted in early May, the Fed’s focus would shift to the labour market and growth (dual mandate), and thus, inflation would take a back seat.

Nonetheless, in the medium term, inflation does matter, as there is a probability (however low) that a resurgence of inflationary pressures will likely occur in the coming months.

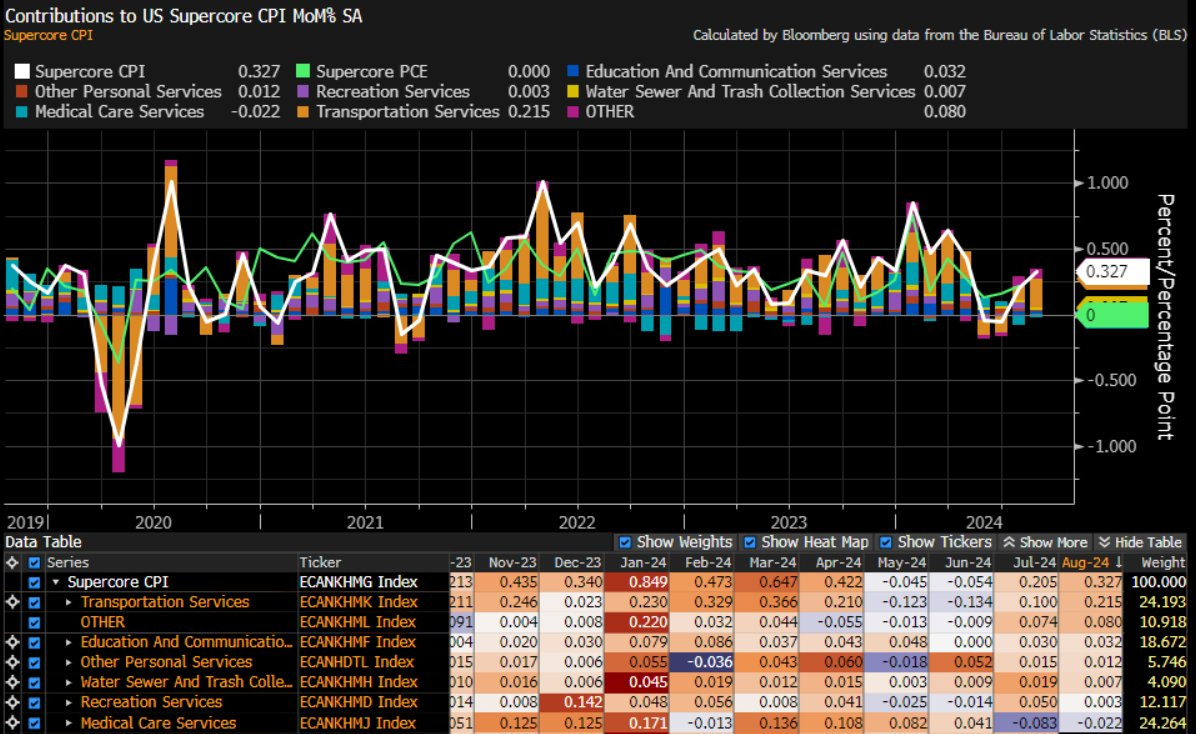

Thus, it is imperative to dig deeper into the CPI report released this week. While the headline number was in line with the estimates, the Supercore, or the Housing Ex-Services, popularized by JayPo, came in hotter than expectations.

In fact, even the core was slightly higher thanks to the surge in one of the CPI’s most lagged components: Owner’s Equivalent Rent (OER).

One can observe a broad-based rise across all the components of the Supercore, especially the Transportation Services, which is turning out to be sticky.

Furthermore, last month, we wrote that the share of components with an annualized inflation of more than 4% has moved down from its highs of 70% to less than 40%. Here, we can also see an alarming trend of bottoming out.

Looking at the above, we now predict that by December, the headline inflation may: