Explosive Setup Part 4.0?

As the war intensifies in the Middle East, the world is grappling with the worst energy crisis since the 70s.

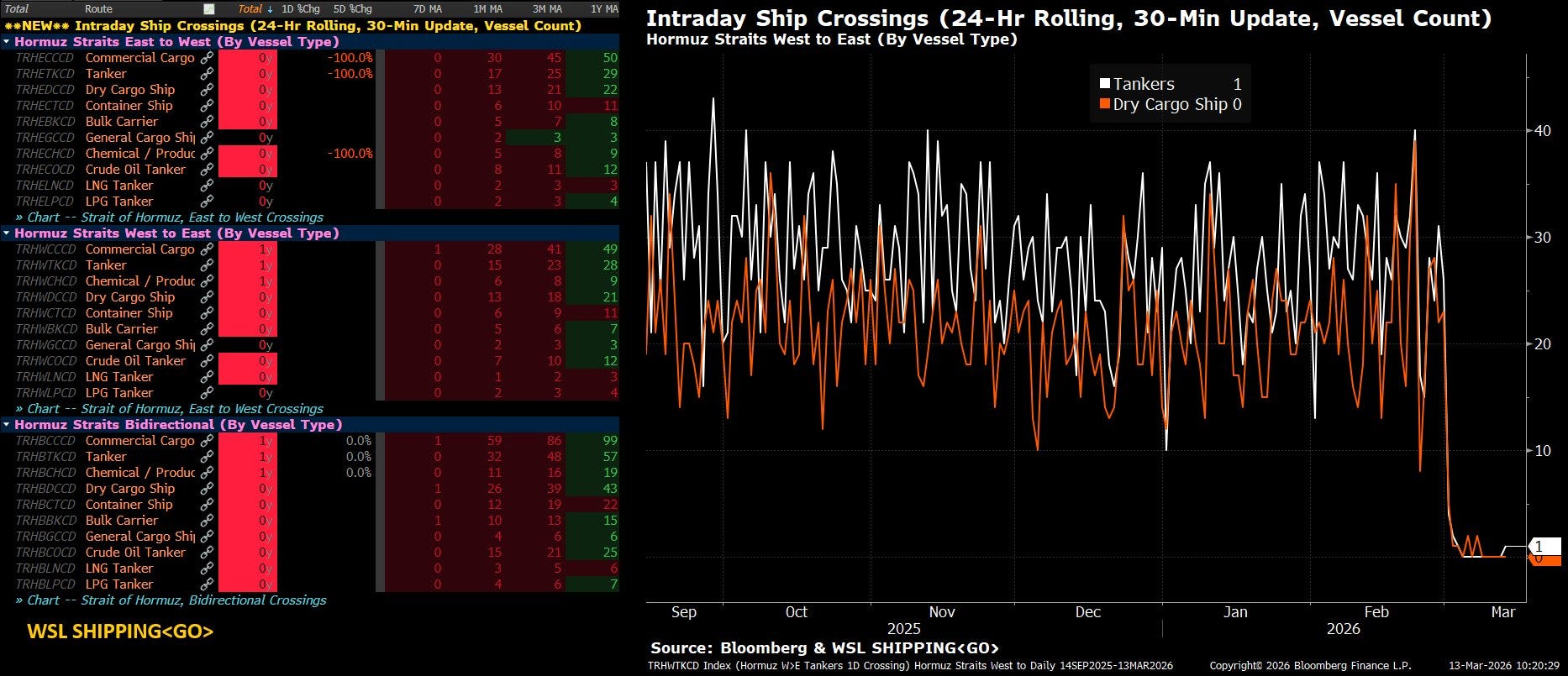

We might be in the middle of a “man-made” black swan event as Iran throttles the Strait of Hormuz and has choked the supply chain of a whole host of commodities, fertilisers, chemicals and other raw materials.

It has been nearly two weeks since the Strait of Hormuz was closed, and we are already witnessing enormous shortages across Asia (80% of all the flows from the Strait of Hormuz go to Asia).

While the paper market is trading around $100, there is absolute panic in the physical market, with the Dubai Physical Swaps trading at a mind-boggling $140/b.

The last six years have been extremely challenging for the global economy, as we have been bombarded by various exogenous shocks: COVID-19, the Russia-Ukraine War, the Trade War, and the US-Israel-Iran War.

Note that these shocks have upended the global financial markets and the geopolitical setup.

As a result, we have seen multiple 6-7 sigma moves across financial markets over the past few years.

Therefore, there is a need to develop a robust risk management system as wild, volatile moves become more common and tail risks become harder to predict.

While there is uncertainty about how the war will progress, we have always believed that the charts don’t lie and the price action is supreme.

The cross-asset charts indicate that the market is poised for significant moves, and thus, we may be ready for an “Explosive Setup”.

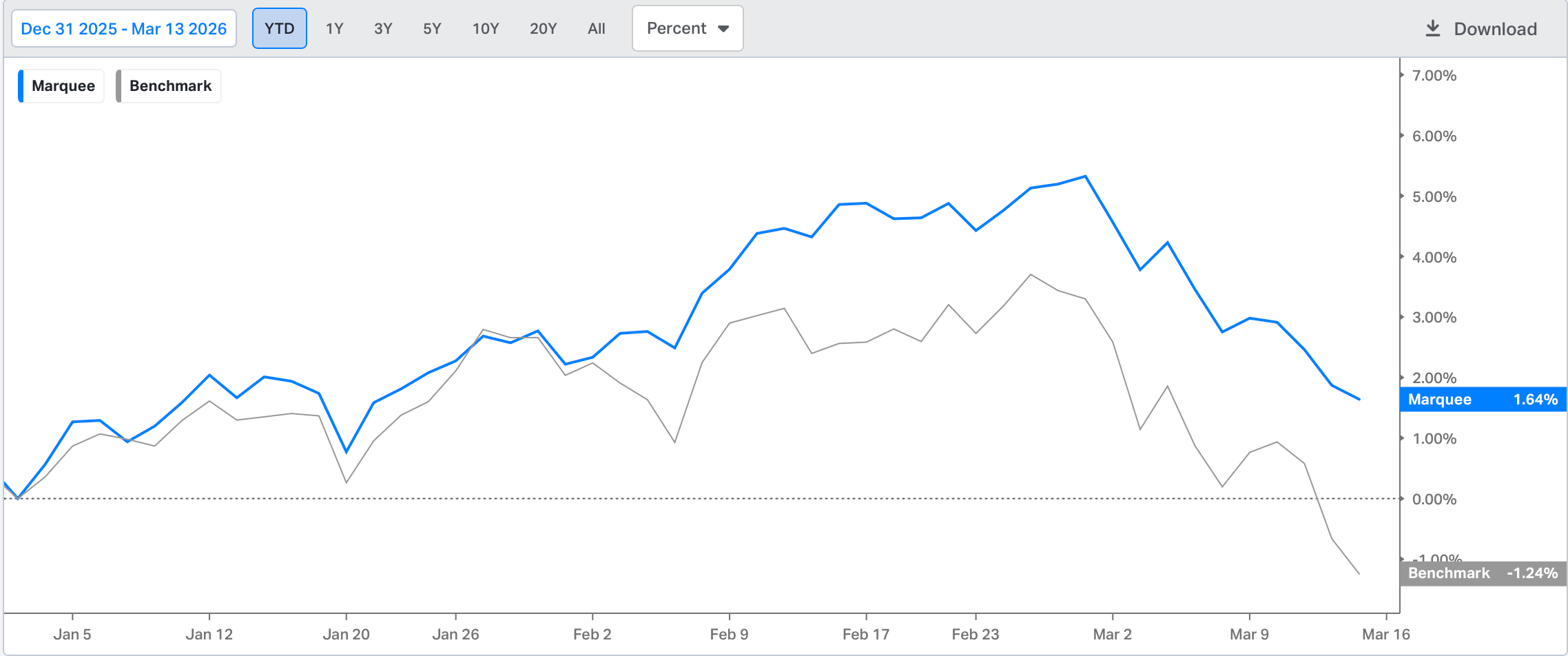

We are up 1.64% YTD against the benchmark performance of -1.24%, thus outperforming the benchmark by 288 bps.

Let us now take a deep dive into the macro and geopolitical landscape and understand the explosive setup we foresee across markets.

US/Equities/Bonds/Oil/Dollar/Gold/Silver/BTC!

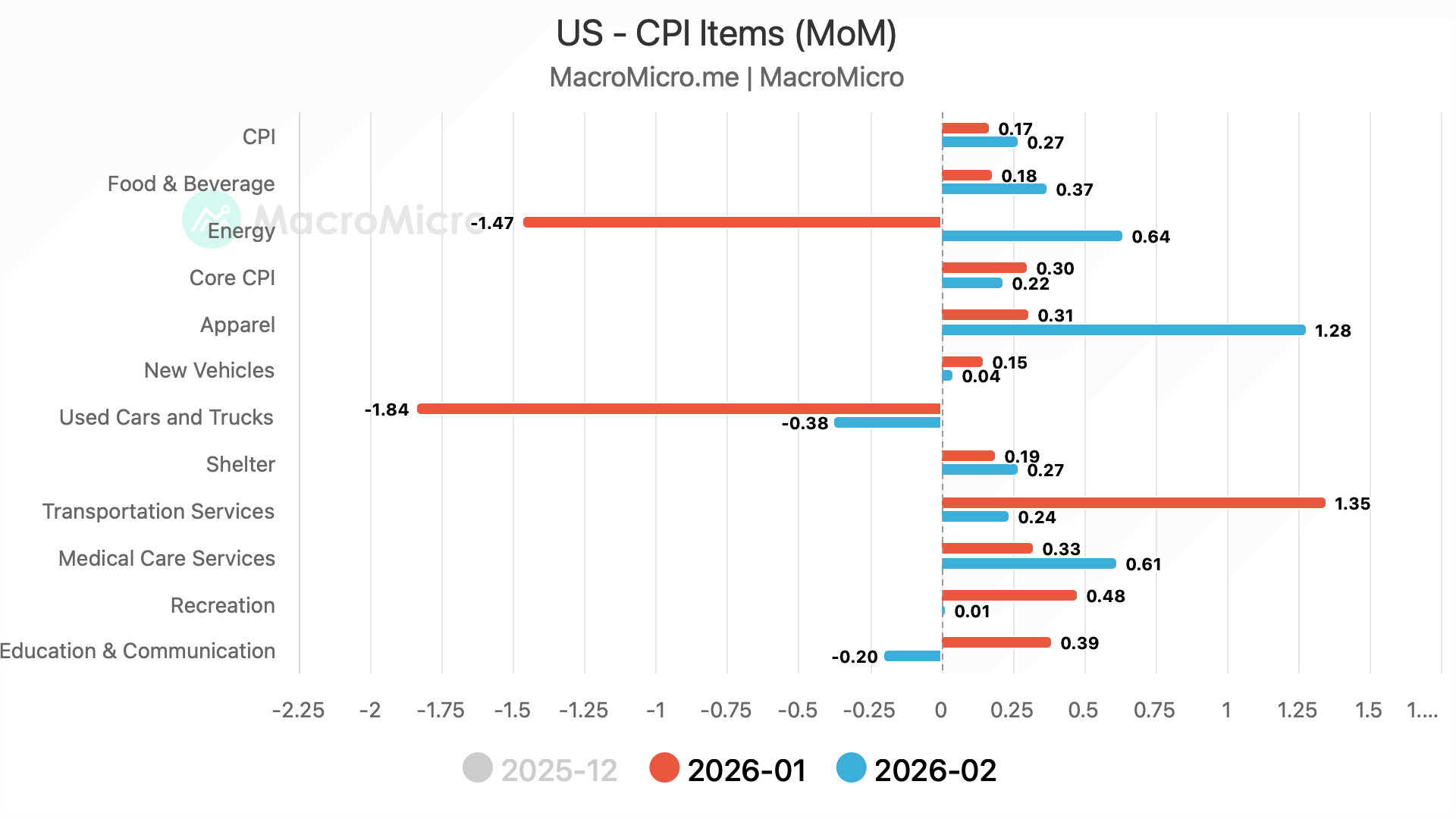

The macro universe was dominated by the CPI data this week in the US.

The Headline CPI (all items) came in at 2.4% YoY/+0.27% MoM, and the core CPI came in at 2.5% YoY/+0.22% MoM, meeting market expectations.

When we dig deeper, while used cars and trucks reported deflation, categories such as Apparel and energy reported positive increases, MoM.

Note that the rise in energy was before the war broke out, and oil crossed $100.

Furthermore, when we zoom out, the segments affected by tariffs (Apparel, household supplies, and other recreational goods) continue to see price increases, putting upward pressure on the CPI.

The disinflationary pressures are seen in Used Cars and Prescription Drugs (thanks to POTUS measures on prescription drugs).

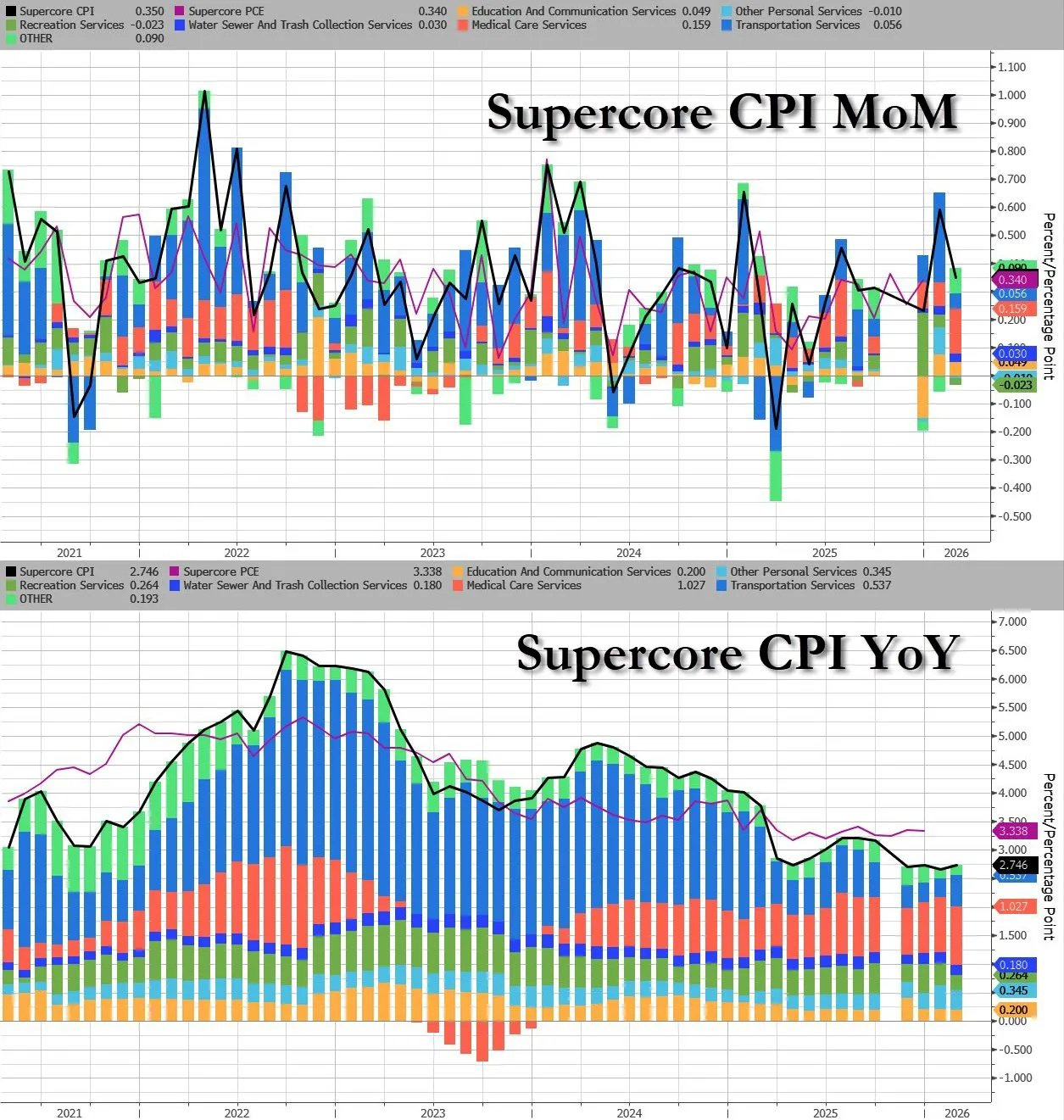

JayPo popularised the Supercore CPI (Services Ex-Shelter), which is still stubborn.

Supercore CPI came in at YoY 2.75%/ MoM +0.35% .

JayPo’s favourite inflation indicator is PCE.

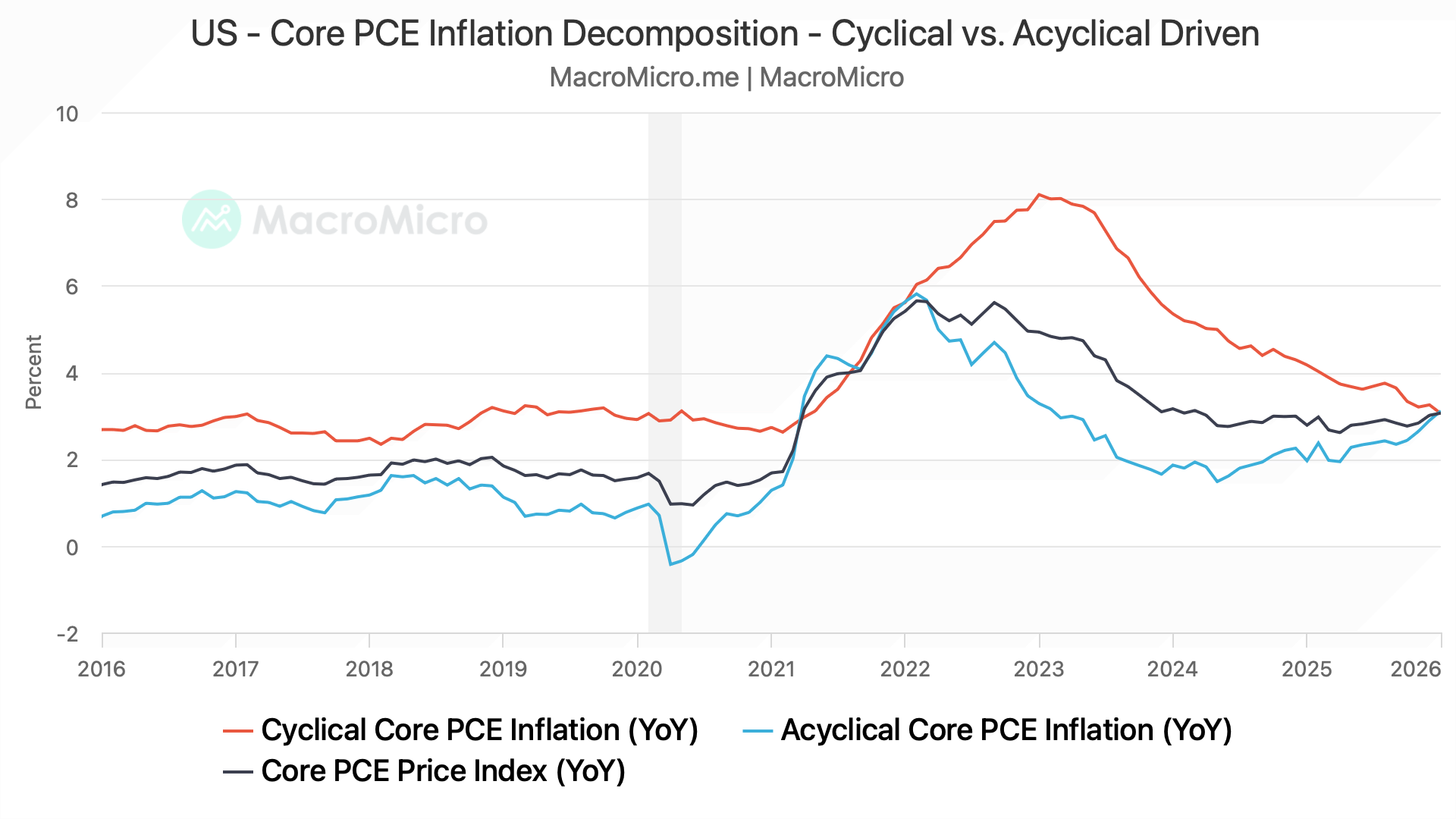

PCE came in at 2.8% YoY v/s Exp. 2.9% and the Core PCE came in at 3.1% YoY v/s Exp. 3.1%.

When we decompose the core PCE, the Acyclical Core PCE (financials, healthcare, clothing, etc) has been rising and seems to have bottomed out.

If energy prices remain elevated for extended periods, expect higher prices to percolate through the economy, potentially causing inflation across all sectors.

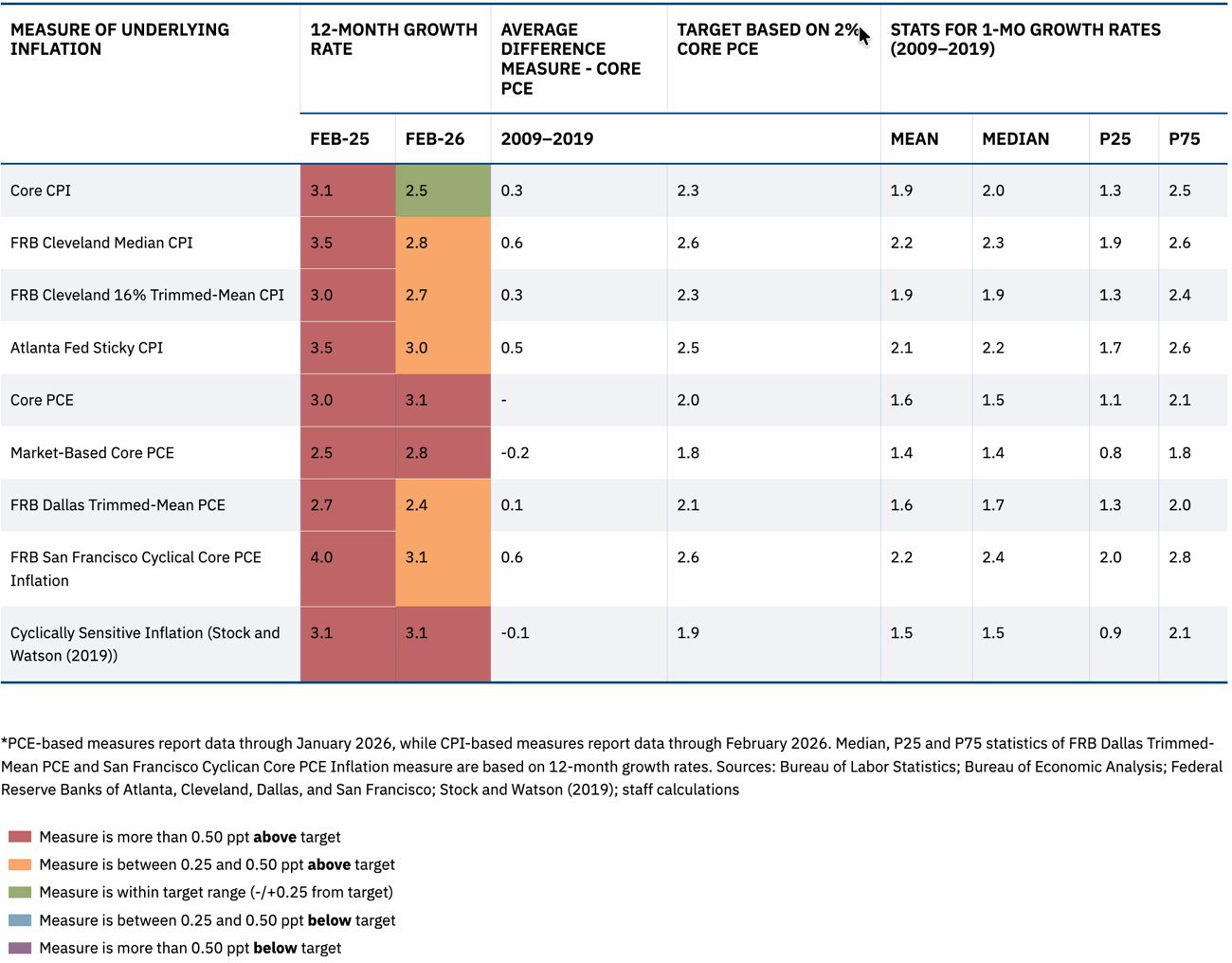

The Atlanta Fed published detailed CPI/PCE data, and although inflation has cooled since last year, it’s still well above the Fed’s 2% mandate.

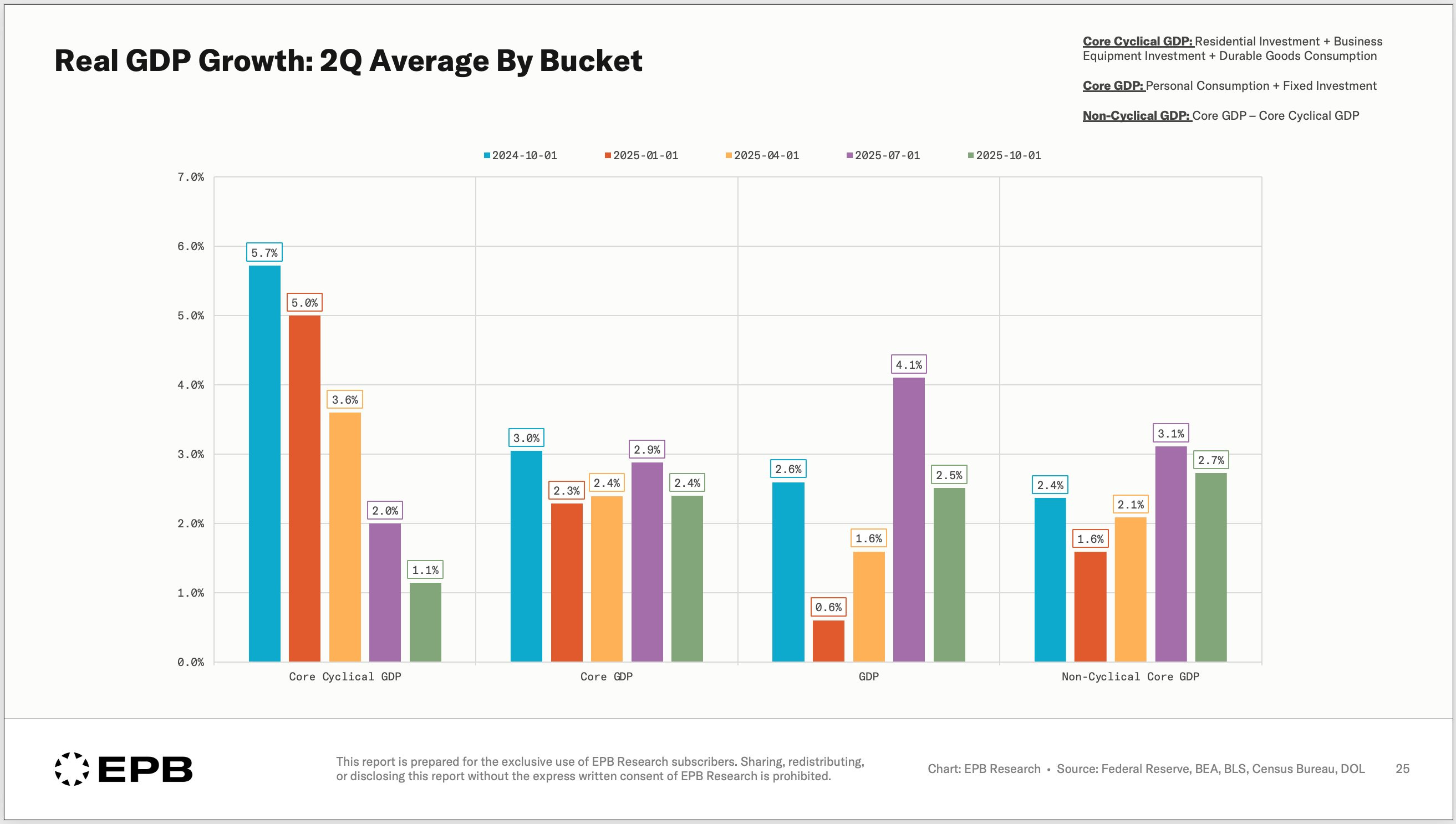

We also got the GDP data for Q4, which was revised lower to 0.7% (estimate of 1.4%).

The culprit has been Core Cyclical GDP, which has decelerated significantly.

The war in Iran will have grave consequences for the economy, and we will assess the implications once it is over.

However, near-term impact will be a spike in inflation even if the war ends in March.

We have historical data to prove it.