Global Outlook 2024!

“Markets Stop Panicking When Central Banks Start Panicking.”

2023 has been a roller coaster ride with the consensus view of a recession, weaker equity markets and a peak in rates going awfully wrong.

The forecasts were revised rapidly after the failure of the multiple regional banks in the US and Switzerland’s second-largest bank in early 2023.

While the markets saw an enormous whipsaw in rates, the equity markets recovered rapidly from a stealth correction led by the Magnificent 7 in hopes of a soft landing.

While the West saw a significant easing of the inflationary pressures as we close the year, the East has seen divergent trends, with the world’s second-largest economy facing severe deflationary pressures. On the contrary, the land of the rising sun cruises out of the three-decades-old deflationary trap.

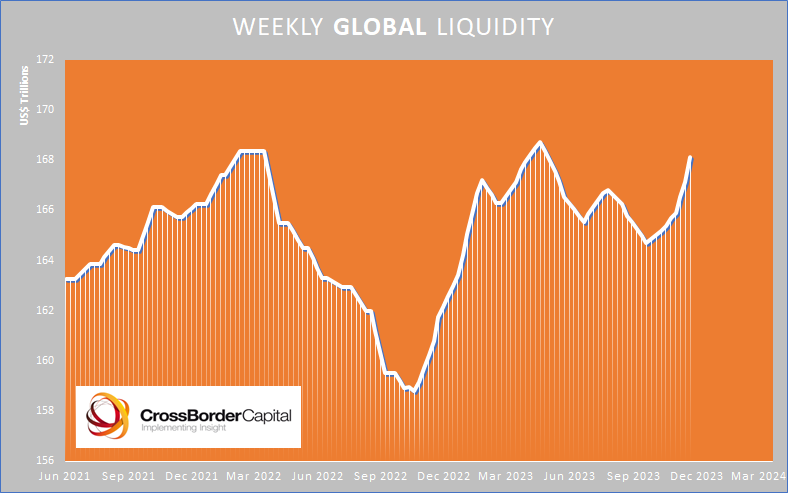

Connecting all the dots, one thing that stands out is the elevated levels of liquidity sloshing around the global financial system, aiding the risk assets and the unhindered speculative mania (crypto).

As we head into 2024, connecting all the dots becomes super important as our “multi-polar” world is facing unprecedented uncertainties on the geopolitical and macro fronts.

Today, we will present a comprehensive overview of the current macro situation; we will also discuss our top 5 macro trades for 2024, look at the appeal of equities, bonds, and commodities, and comprehend the influential FX markets.

PS: Please view this email on a desktop or the substack app if all the charts (around 22) aren’t visible, as the email size is above permissible limits.

The “Global” Macro View!

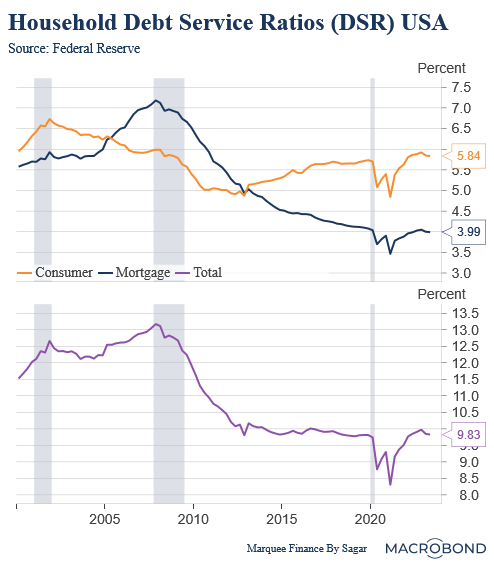

Since the beginning of 2023, we have been in a mild recession camp in the US, as the situation is entirely different from the GFC. Today, the US private sector and households have considerably reduced leverage.

We will look at three metrics and then infer the following:

US Household Mortgage Costs, as % of disposable incomes, are way below the 2008 GFC as HHs were able to lock in lower rates post-pandemic (fixed).

US Household Consumer Debt Service Cost as % of disposable income is at 2008 levels due to skyrocketing APR on personal loans and credit cards. This will be keenly watched as the unemployment rate rises in Q124.

US Household Debt Service Cost as % of disposable income is nearly 300 bps lower than in 2008 due to an enormous deleveraging post-GFC and favourable refinancing of mortgages post-COVID.

This is one of the prime reasons I had been in a “mild recession” camp since the beginning (never been in a soft landing camp).

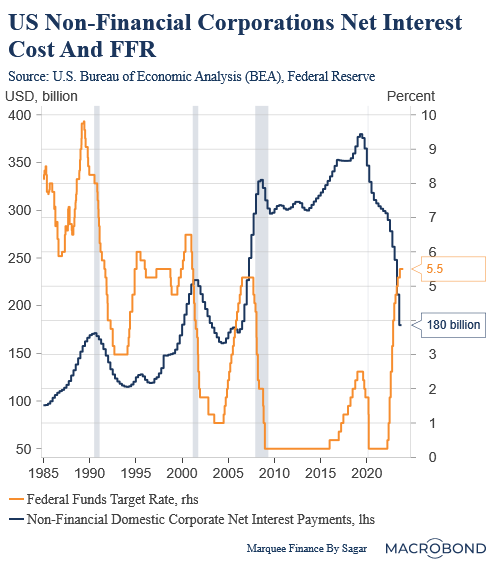

On the other hand, the private sector has successfully refinanced a majority of their borrowings for longer tenure at rock bottom rates post covid and hence has been able to reduce their net interest payments.

This is one of the reasons for the strength of corporate America.

Overall, the US looks in better shape than its European counterpart and will likely witness a mild recession.

However, one of the scenarios with high probability is if