Global Outlook 2025!

Welcome to the third edition of the Global Outlook, where we discuss our macro view for the year ahead and dig deeper into the expected performance of various asset classes based on our well-researched macro view.

Undoubtedly, the highlight of 2024 was the elections in democratic countries globally. The trend has been clear: either the ruling party lost the elections, or the incumbents returned to power with a “weak”/“fractured” mandate.

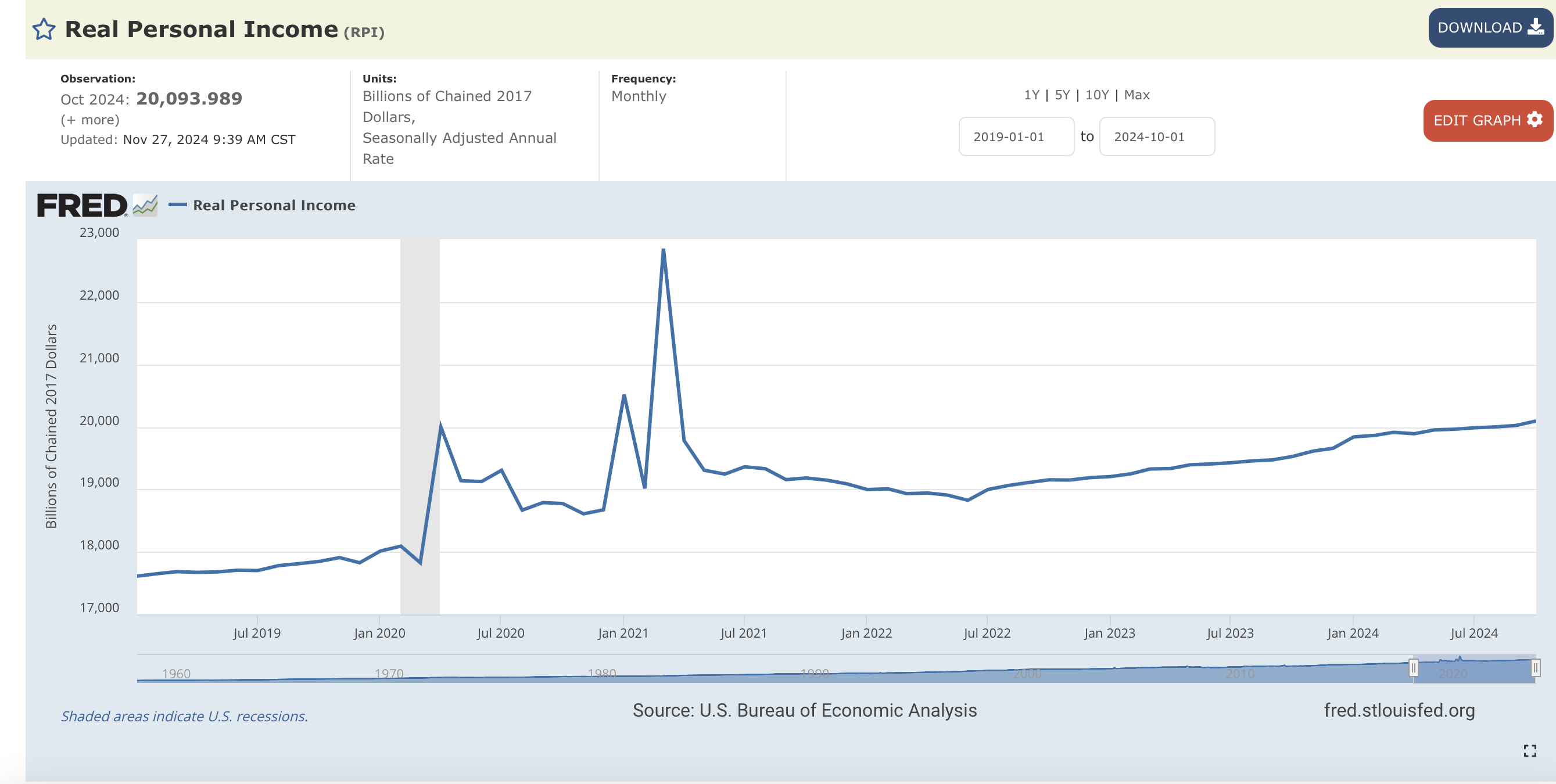

The bottom line is that people worldwide have voted for change as the “real wages” / “real incomes”[adjusted for inflation] are down significantly.

Due to the plunge in real incomes, society's bottom pyramid (those who are not asset owners) has faced maximum suffering, with income inequality reaching unprecedented levels.

When we zoom out and examine the macro view, we can’t ignore the consequences of political change and the promises (populist measures) made by those in office after coming out victorious.

In 2024, the US avoided a recession, as the eco…