It's Beginning!

Last week, we mentioned the trio of Elections, Geopolitics, and Macro. We also predicted this trio would lead to elevated volatility in the coming weeks.

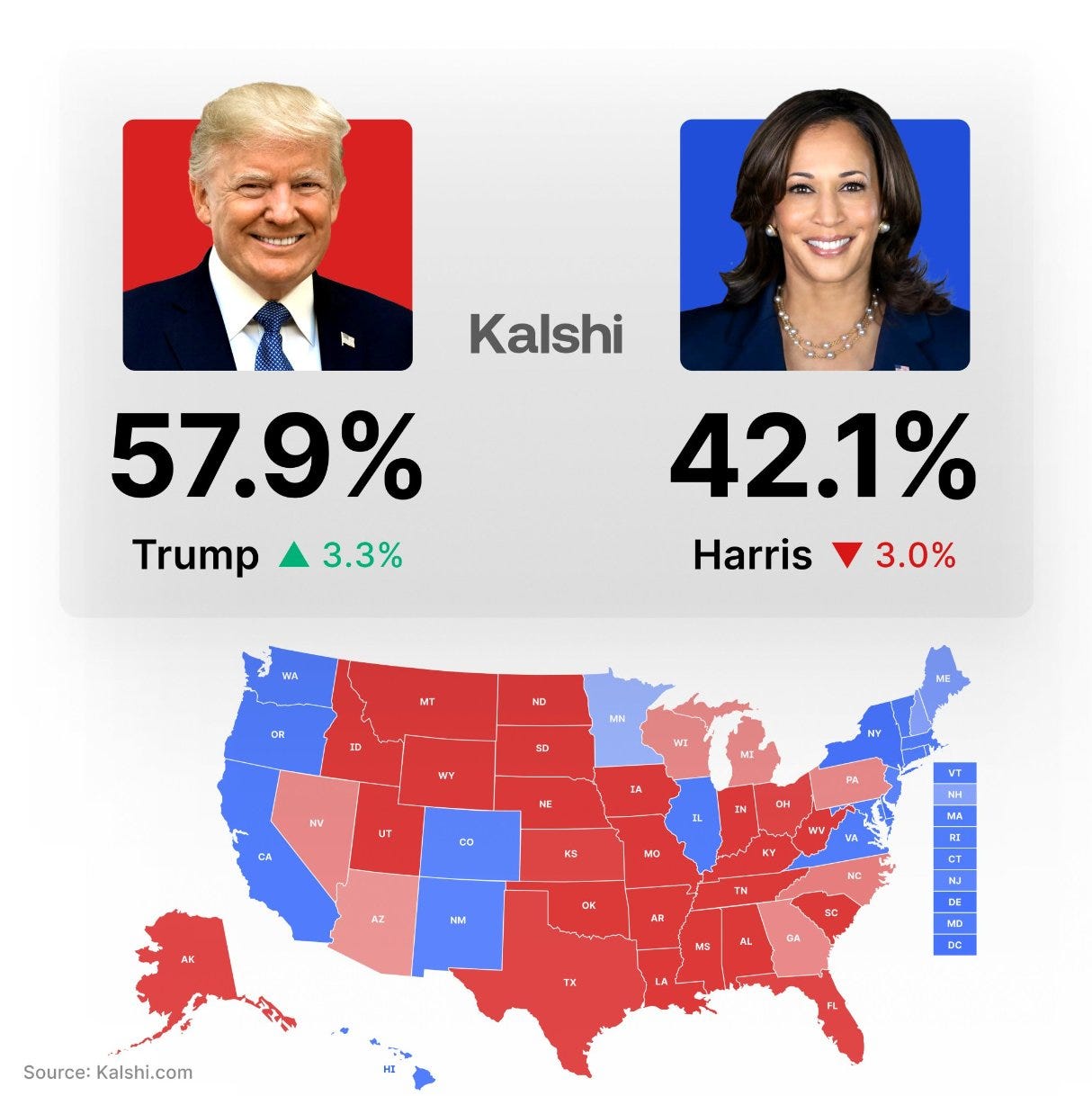

As expected, volatility in some asset classes has risen significantly as the prospects of a Republican victory in the US presidential elections skyrocket.

As per Kalshi, Trump is now leading by record margins.

As a result, we saw BTC breaking the $67k mark. Furthermore, the volatility in the bond markets, as measured by the MOVE Index, has also climbed in the last few days.

On the other hand, geopolitical space is getting murkier with every passing day.

In an explosive revelation today, the South Korean spy agency revealed that the North Korean troops are on the ground in Ukraine fighting on behalf of Russia. These troops have received Russian Military uniforms, arms, and even fake Russian Ids.

Israel successfully eliminated Hamas Chief Yahya Sinwar while it received the critical THAAD System from the US. Everyone is keenly awaiting the attack on Iran as Netanyahu has likely finalized plans.

Thus, depending on the extent of the Iran-Israel conflict, geopolitics will profoundly impact the asset classes (Gold, Oil, and other risk assets) in the coming weeks.

On the macro front, the action was muted this week as there was a lack of market-moving data in the US. Nonetheless, elsewhere, the ECB cut rates by 25 bps as expected and the macro data in the UK was relatively dovish.

Let’s dig in deeper.

US!

This was a lighter week regarding macro data, but we got the retail data, which has always led to wild cross-asset moves (depending on the degree of beat/miss).

Our paid subscribers will appreciate that we have mentioned how elections have influenced the data in the past few weeks.

Every important data piece is now doctored in some way to portray the economy as booming after the NFP debacle a month ago.

Nonetheless, we look at data other than government sources, primarily surveys with large sample sizes, to gauge the true strength/weakness of the economy.

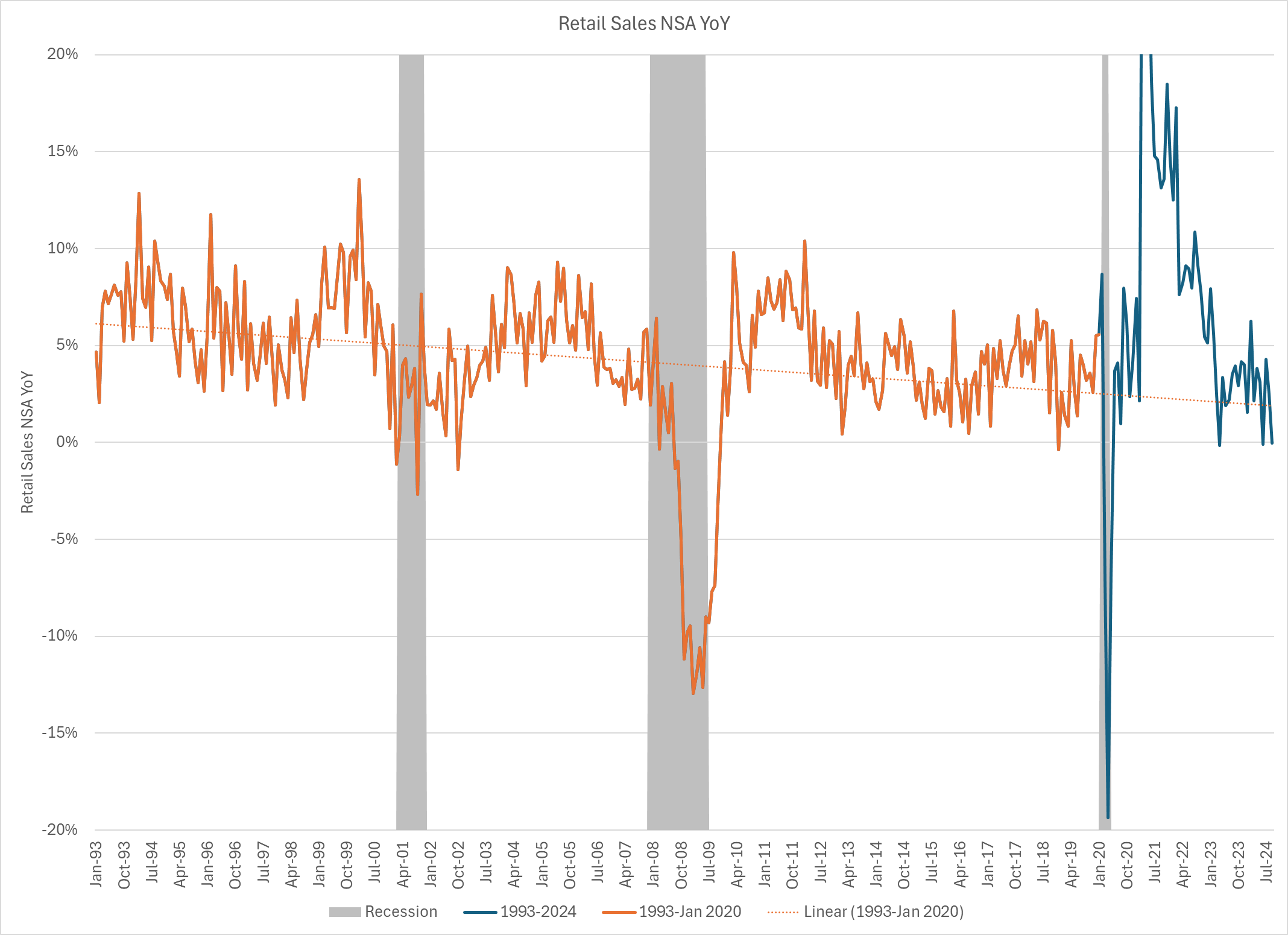

The retail sales on the face of it were a big beat especially the core retail sales. However, when we remove the “seasonal adjustments”, the non-seasonal (NSA) Retail Sales were in fact negative, a rare occurence outside of recessions.

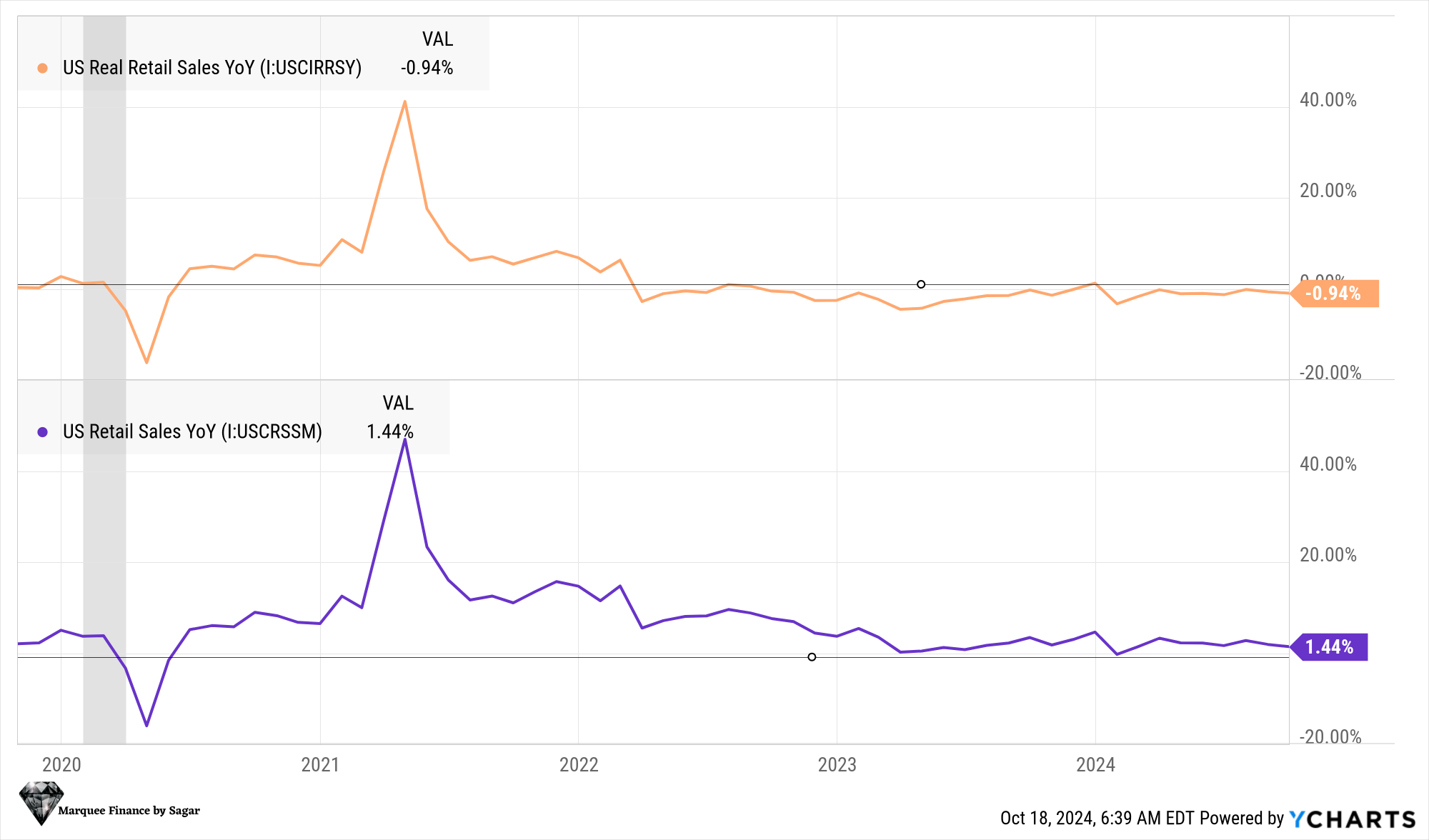

Furthermore, we always emphasize real retail sales or inflation-adjusted retail sales, enabling us to assess American consumers' health.

The trend here is alarming, as there is still no recovery in real retail sales, which are down 0.94% YoY.

We won’t pay much attention to the coincident indicator, Industrial Production, as it was impacted in September by the Boeing strike and the hurricane.

Thus, industrial production data for November (October will be even more volatile and impacted by the hurricane) must be looked into.

Nonetheless, we have some other vital pieces of data which we would like to share.

One of the surveys is a new addition to our macro framework.