It's Time For The Deadly Trio!

Last week, we wrote extensively about the deteriorating situation in the Middle East, where Israel has been preparing to take revenge on Iran by targeting Iran’s nuclear facilities/ oil facilities.

It has been one week, and there has been no attack yet, but Israel has been building consensus with the US Government about the targets. However, the Biden administration fears that the retaliation might be more extensive than what is discussed.

On the other hand, Iran has threatened the Arab states with widespread attack if they allow Israel to use their airspace for the attack on Iranian soil.

The situation is tense, and since nobody is discussing a ceasefire, we expect significant escalation in the next few days.

Nonetheless, the equity markets have been complacent despite VIX sustaining above 20. Surprisingly, gold is lower, and oil has also hovered around $79.

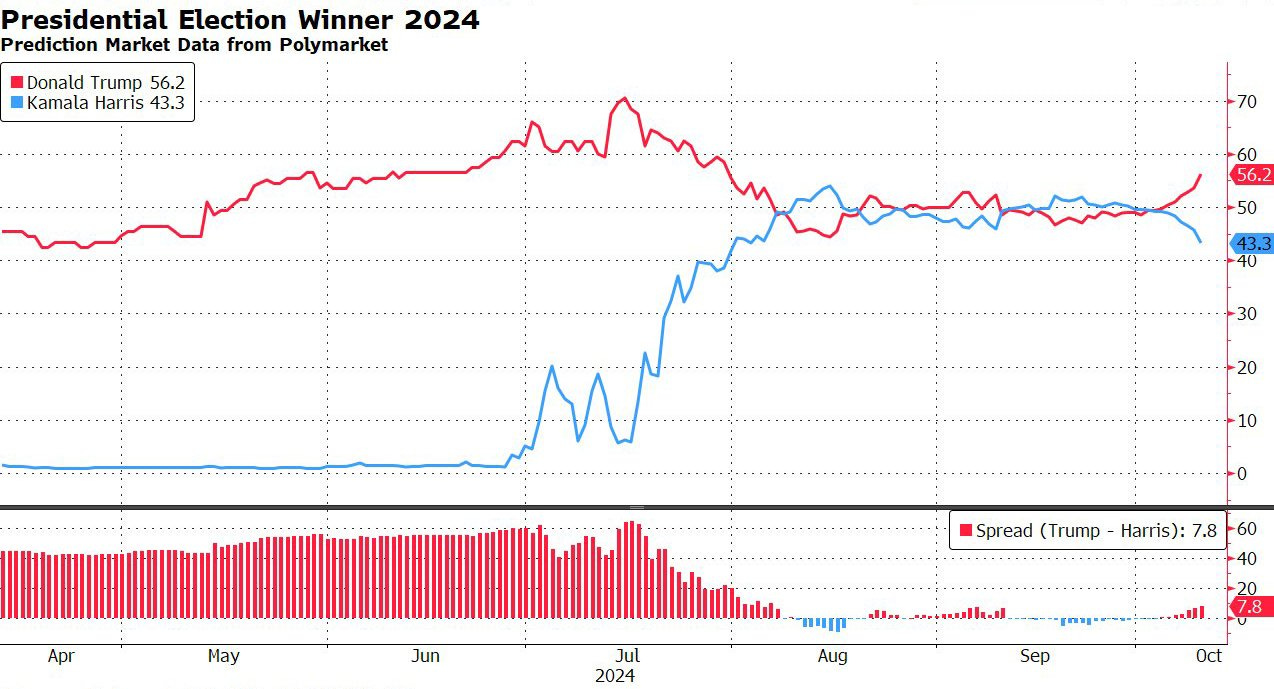

It’s not only geopolitics that can potentially lead to wild swings across assets next week. We are on the verge of a historic election in the US, which is now less than a month away.

The prediction market now favours Trump over Harris by the widest margin in three months.

With a Republican victory looking more likely, a cross-asset reaction will occur if the lead widens further in the next few days.

The deadly cocktail of macro, elections and geopolitics will have a catastrophic effect on the volatility, and we will most likely see wild moves soon.

Let’s recap the macro data released this week and examine the rationale behind some of our positions.

US!

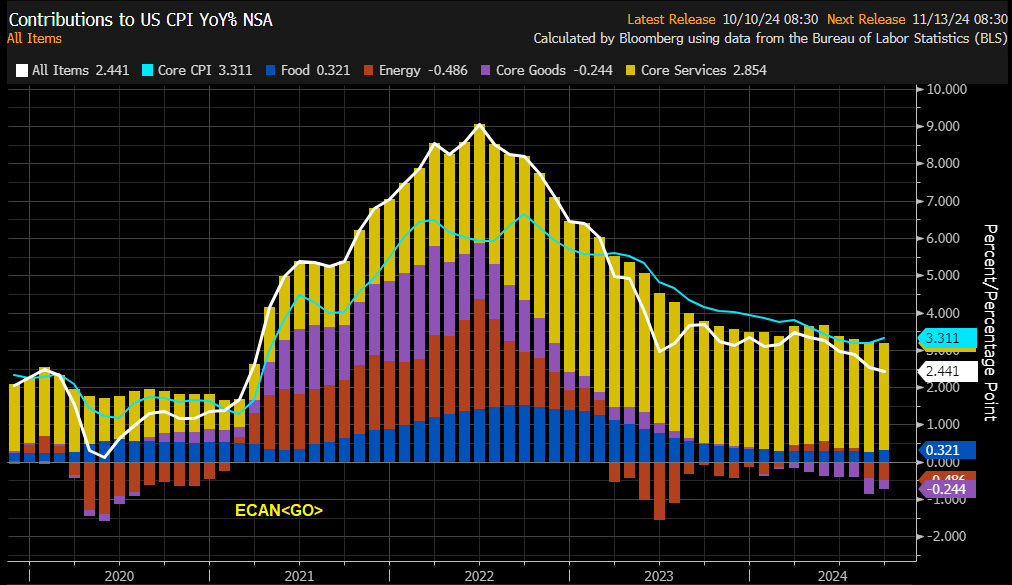

This was the CPI week, as we got the all-important inflation data.

It’s a no-brainer that the Fed’s focus has shifted to the labour market (dual mandate: stable prices and maximum employment).

As a result, the market’s reaction to the “hot” CPI print was muted.

The headline number was in line with expectations, but the surprise was the core CPI, which was hotter than expected (3.3% YoY).

As we can observe, core goods inflation is putting downward pressure on the CPI, which stays in deflationary territory (-0.24% YoY).

Furthermore, the culprit for the higher core inflation was the Core Services CPI, which turned out to be stickier than expected.

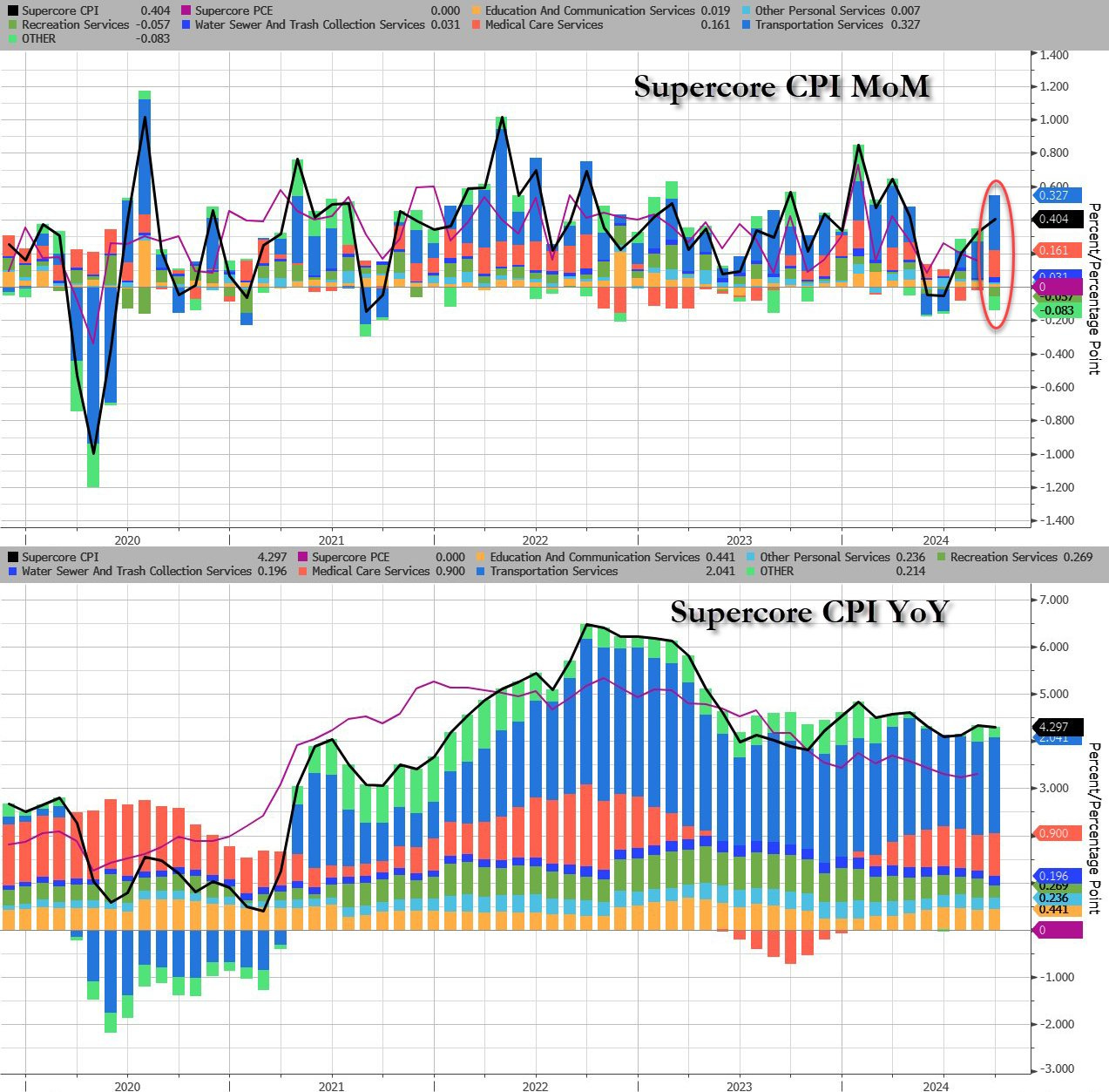

JayPo popularized the Supercore CPI (Services Ex-Shelter), which he justified to raise rates last year.

In what turned out to be a complete shocker, the Supercore CPI is now running at an annualized pace of 6%.

Transportation and medical care services led to the surge in the Supercore CPI, which is becoming stubborn and immune to higher rates.

In fact, we have indicated earlier that the higher transportation services CPI was the result of higher rates (due to high prime rate feeding into the CPI).

Nonetheless, our paid subscribers will appreciate that we had already guided for higher CPI last month.

Furthermore, we believe that by the end of December, CPI will…