It's Time To Be......Cautious!

As we near the end of a historic year where the US benchmark indexes led by the Magnificent 7 gave stupendous returns, the “everything rally” of the last two months indicates early signs of fatigue.

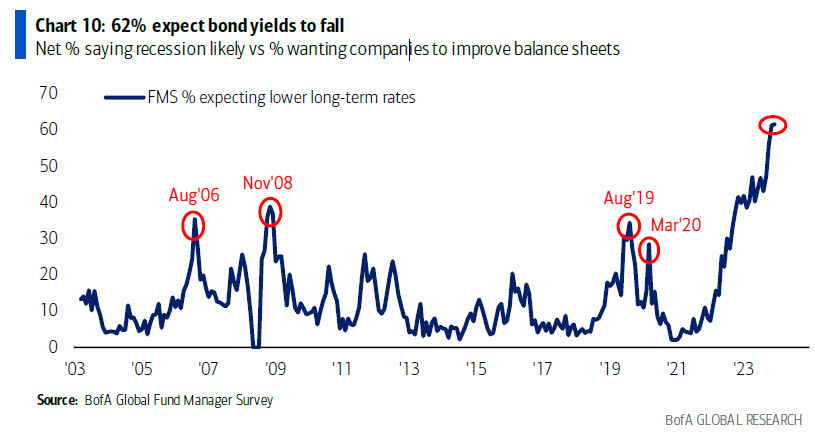

On the contrary, fund managers across the world are now prepared for a perfect “soft landing”, with a majority of them overweight bonds (duration) at a time when the markets are pricing more rate cuts than even the dovish Federal Reserve (In fact, the March rate cut is a done deal as per markets).

Furthermore, a lot of cash from the MMFs in recent weeks moved to equities and bonds as funds globally chase the meltup across various asset classes.

As a result, the cash at major fund houses is below 5%, indicating extreme bullishness.

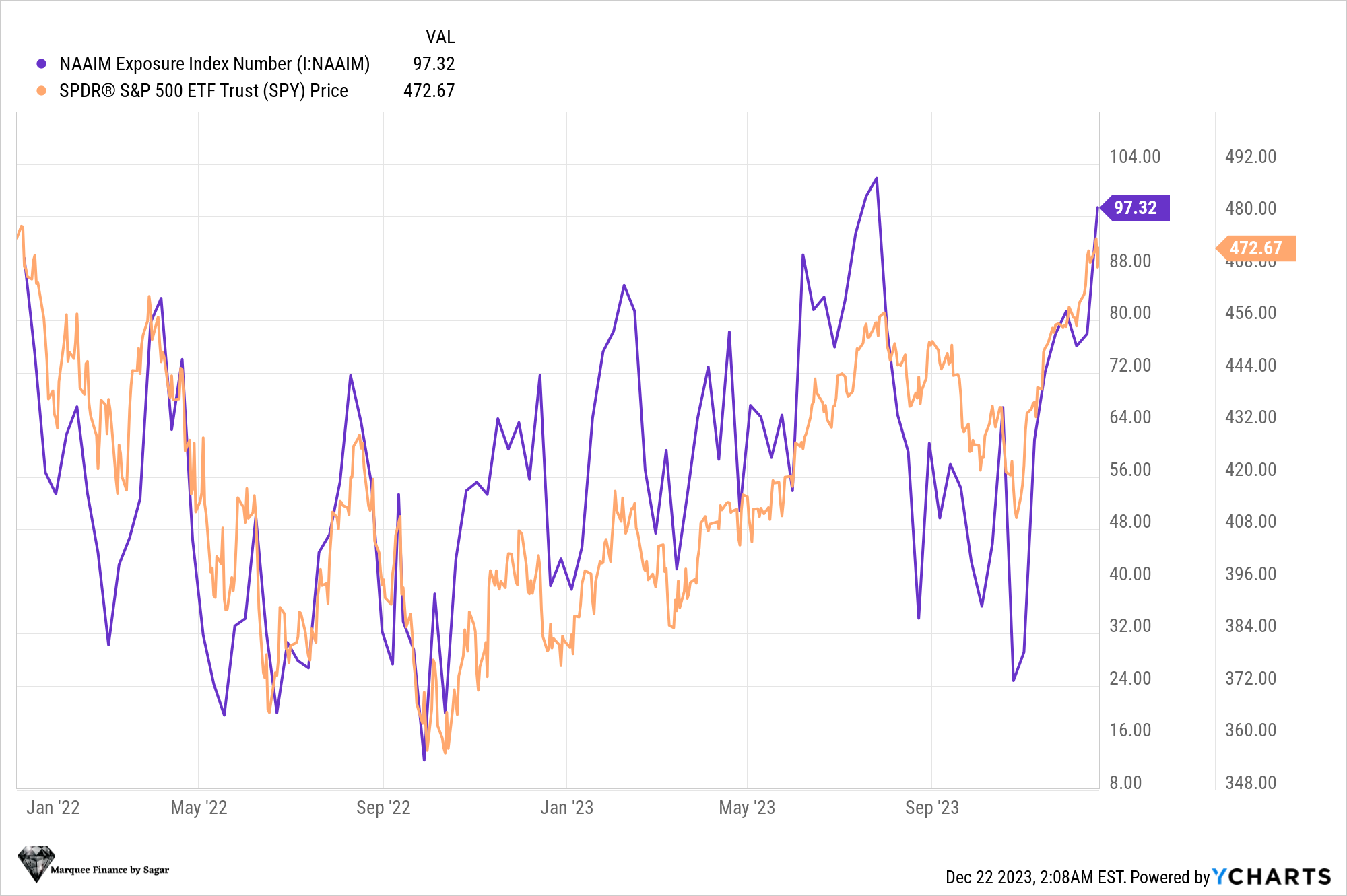

One can observe that active managers had less than 25% of exposure to equities (calculated via NAAIM) in late October; however, the current exposure stands at 97.3%, the highest since the markets peaked in August.

Nevertheless, as a systematic macro investor/trader, one needs to stay focused (and data dependent) and doesn’t need to fall for the innumerous narratives floating around.

In the past few days, we have churned a lot in line with our “Global Outlook 2024” and our macro thesis with prudent position sizing to manage risk (the top priority).

Let us take a deep dive and understand what this week’s macro data tells us (and justify the position that we initiated this week).

US!

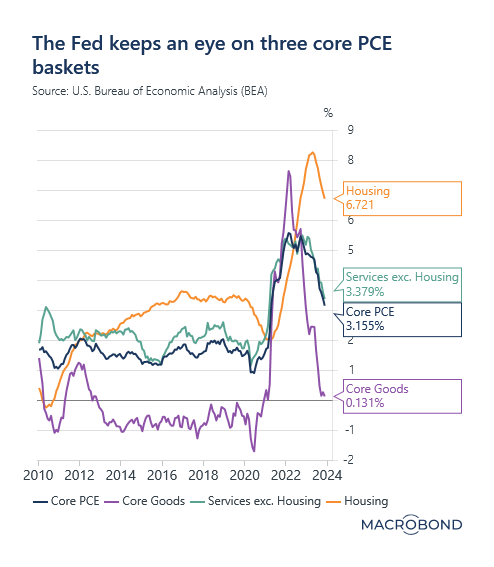

Federal Reserve’s preferred inflation gauge was the biggest data point of the week, which witnessed low volumes of trading at bourses as the year-end approaches.

The PCE came in line with the expectations with core goods inflation plunging due to benign used car prices.

Nonetheless, the services ex-housing, which JayPo popularized last year, remains sticky.

The reason for the stickiness of this component of inflation has been none other than the