Make Tariff "Vol" Great Again!

Once again, the world’s most powerful central banker shocked the world in his first post-Trump FOMC meeting.

In a shocking statement, Powell mentioned:

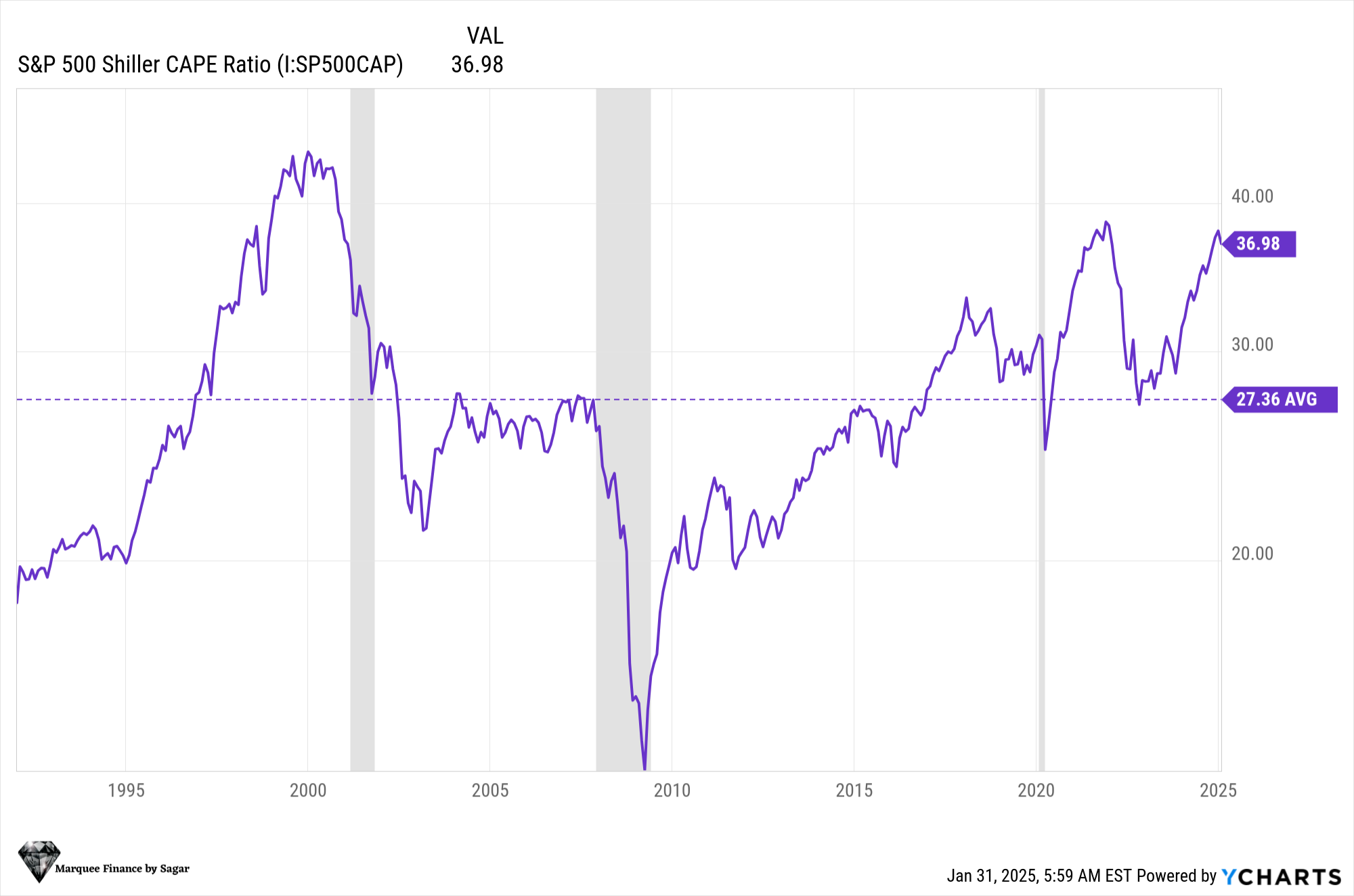

“Asset Prices elevated by many metrics.”

In fact, this will be the first time in decades that the Fed Chair has issued such a statement.

Greenspan famously quoted “Irrational Exuberance” in 1996, just before the mega rally began in equities. Now, after a gap of nearly two decades, we have Jerome Powell stating about the euphoria in asset prices, which has led to sky-high valuations and a likely bubble in credit markets.

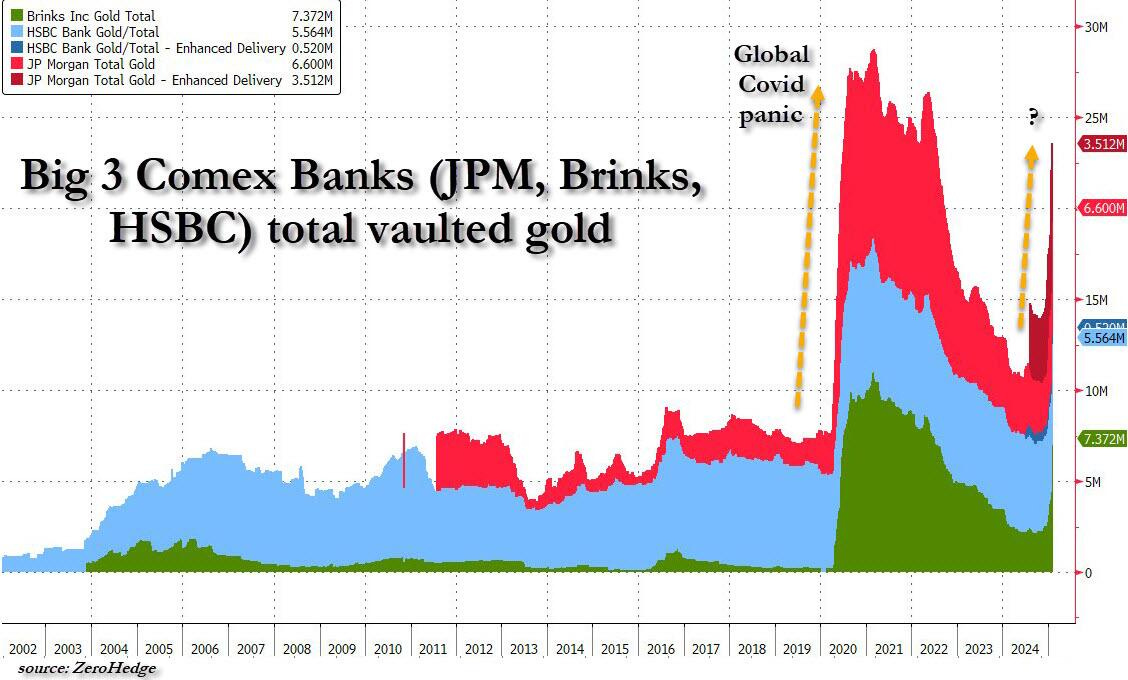

Furthermore, as the Trump administration prepares to implement tariffs globally, there has been a mad scramble to repatriate Gold in the US.

Speculation is rife that universal tariffs will be imposed on all commodities, precious metals, and even semiconductors.

In fact, we are witnessing history as the vaults in London get empty, and an event similar to COVID transpires in full force with deliveries to COMEX shooting up.

Furthermore, the ECB cut rates as expected this week.

Let us comprehensively analyse the macro data released this week.

US!

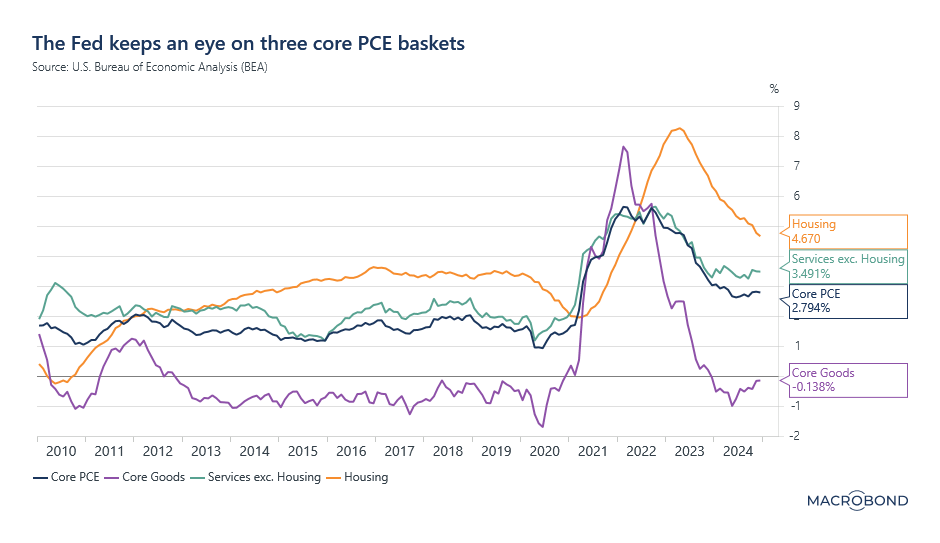

The Fed’s favourite measure to track inflation is the PCE, which came in line with the expectations yesterday.

However, as usual, the devil lies in the detail.

When we dig deeper, we see that the core PCE has been hovering around the 2.8% mark and has indicated early signs of bottoming out in the last three months.

Furthermore, the decline in the PCE is being led by the housing component, which has been in free fall since its peak in 2022.

There has been a lot of chatter lately about the fall in rents, and thus, there is a high probability of further fall in the housing component of inflation beginning Q2/Q3 this year.

Nonetheless, the Services Ex-Housing is still running at 3.5%, and core goods has begun to rise from the bottom as the base effect kicks in.

Thus, a path to 2% looks arduous, and we believe we won’t see it in 2025 (especially for Core PCE) unless we get a drastic slowdown in the cyclical economy.

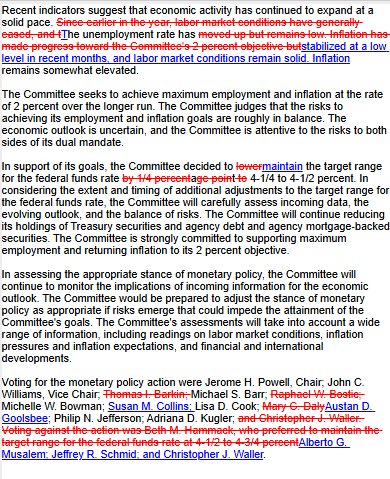

Moving on to the FOMC meeting this week (the first since Trump took over), we got the status quo as expected.

The changes in the policy statement is as follows:

A slightly hawkish touch was the line where they mentioned that the labour market conditions remain “solid” and the inflation remains “somewhat elevated”.

Nevertheless, the presser was on the dovish side or as the markets interpreted it.

Thus, while the Fed meeting this week was uneventful, as asset prices barely moved, some of JayPo's statements were worth noting and, according to us, will have long-term consequences for markets.

Let us dig deeper and analyse in detail: