MELTUP!

Nobody in their playbook had fresh All Time Highs (ATHs) for equity markets in after what transpired in April.

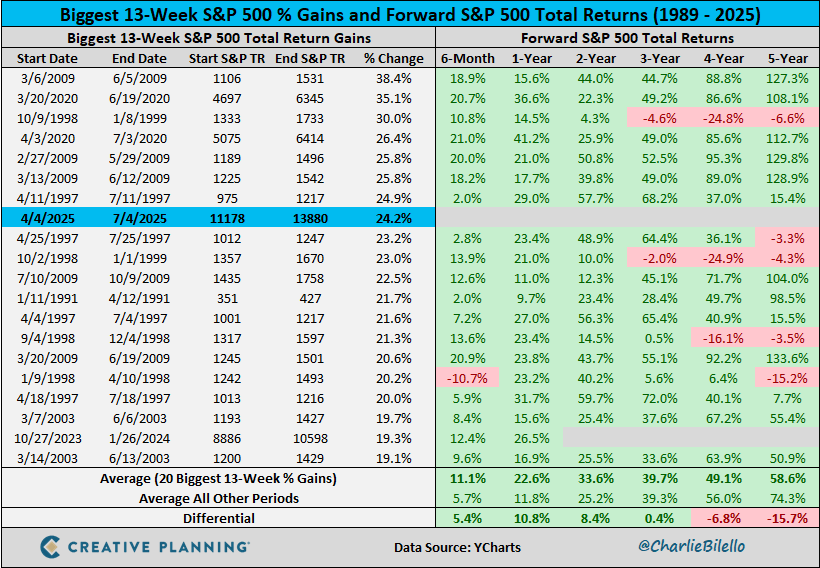

In fact, the current rally has been one of the fastest 13-week rallies in history, with the S&P 500 up by more than 24.2% since April 4, 2025.

The “meltup” intensified this week, as POTUS signed the OBBB (One Big Beautiful Bill), and a big upside beat on Non-Farm Payrolls data led to exuberance with a fresh breakout and ATHs in equity markets.

Furthermore, a deal with Vietnam was announced which favoured the US and was likely a win for the Trump administration as it launched an indirect attack on China with 40% tariffs on “transhipping”.

We also expect an interim deal with India by Monday or Tuesday.

We continue to excel in our performance, as the PF has hit fresh ATHs thanks to our long equity position and a stellar run by the Thematic Investing names.

Nevertheless, we believe that easy money is over, and we may experience volatile swings as we progress into H2.

Let us begin today’s newsletter and comprehend the plethora of macro data released in the shortened week!

US/Bonds/Gold/DXY/Oil!

The first week of the month is always busy, as we get inundated with macro data.

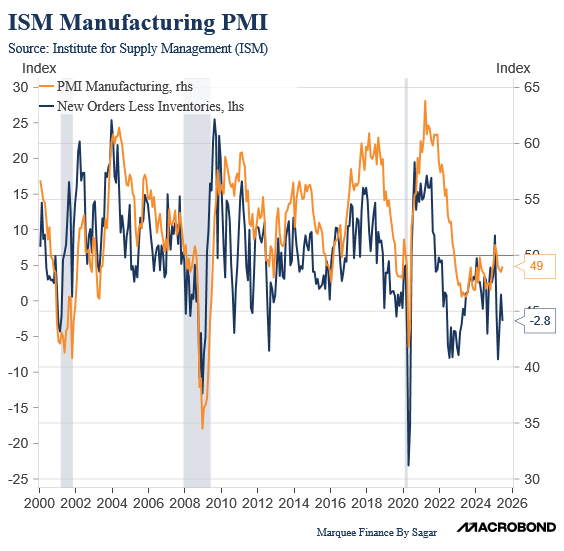

One of our favourite indicators for gauging cyclical activity is the ISM Manufacturing PMI.

Since February, the data have been noisy and marred by volatility, as the tariff front-loading occurred in Q1. As a result, while March and April were stronger, May was weaker than expected.

Nonetheless, we expect normalisation to happen in a month or so. We also expect a trend to emerge in late Q2, which will enable us to determine the direction of the cyclical economy.

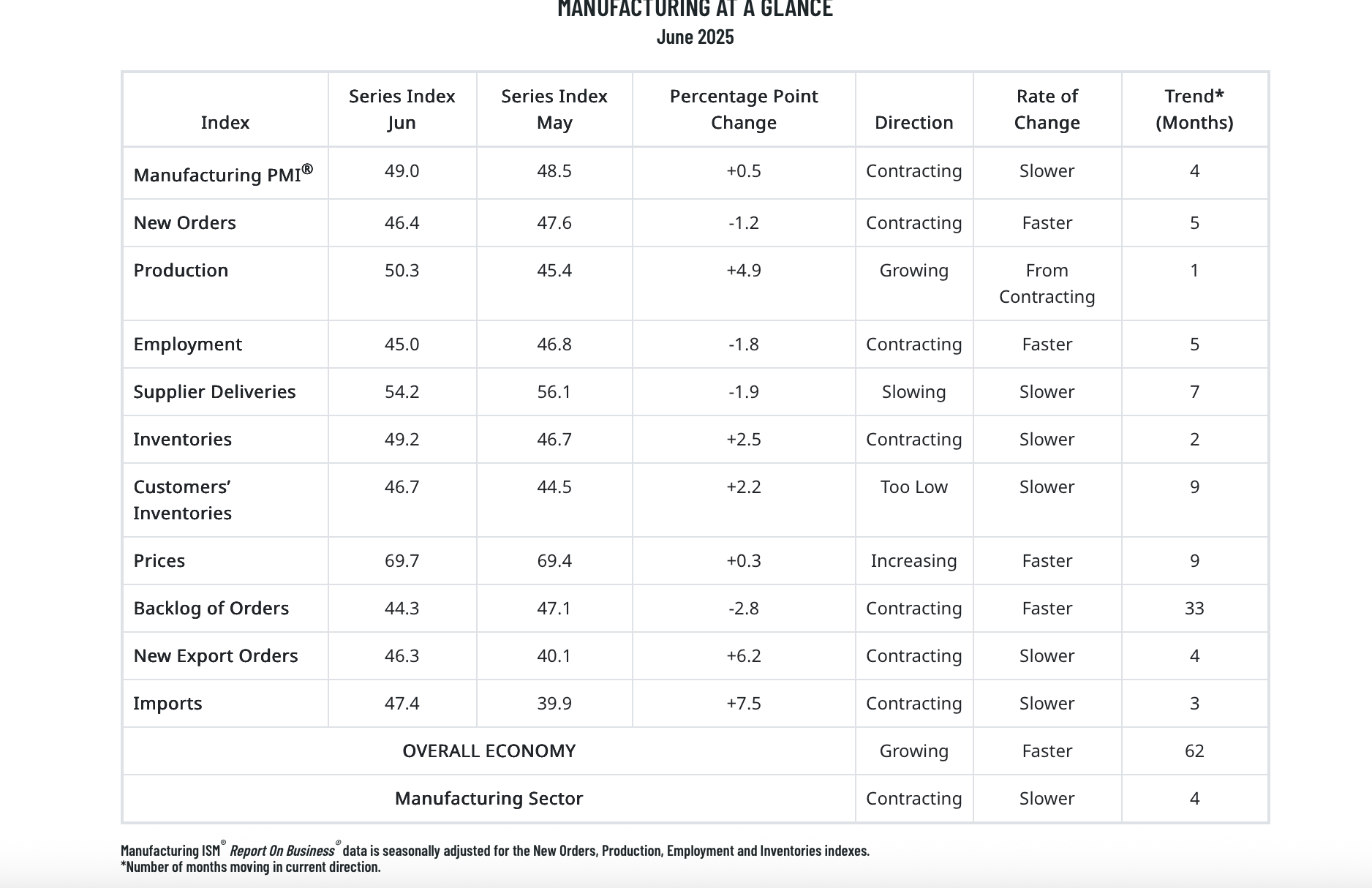

The headline number came in at 49 (just below 50), indicating contraction, while New Orders Less Inventories fell again.

The fall in New Orders Less Inventories, if it continues in August, will indicate that the headline PMI is headed lower, suggesting weakness in the cyclical economy.

While New Orders fell, inventories, though still in contraction, rose from 46.7 to 49. On the contrary, production has risen sharply and is now in an expansionary zone.

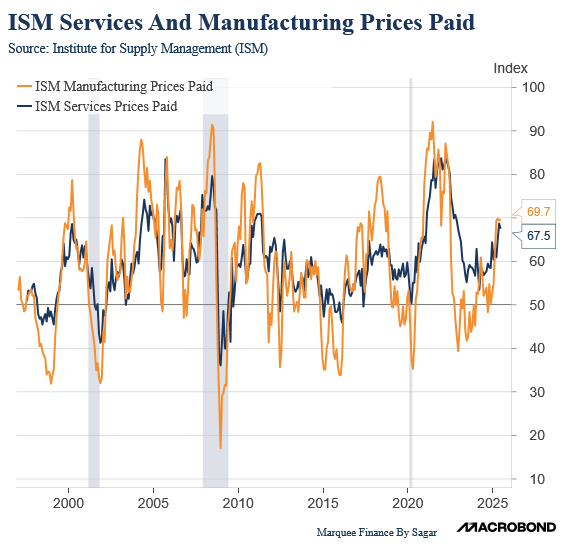

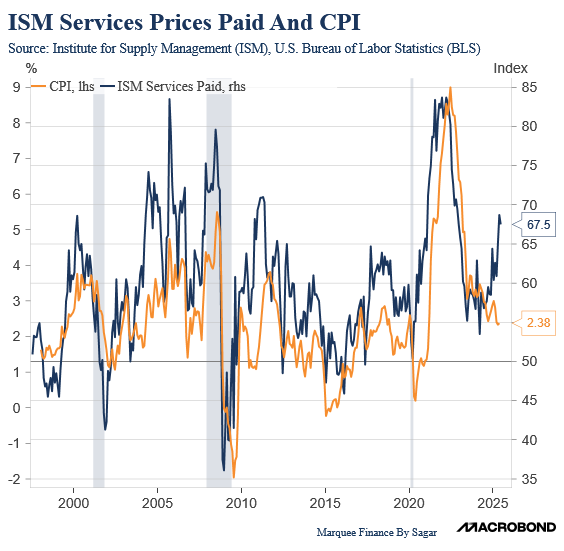

Ironically, the most horrific print across both ISM Manufacturing and ISM Services was the Prices Paid component.

Both of them indicate that the prices are rising at a rapid pace (expansionary above 50).

Last month, we also mentioned that ISM Services Prices Paid has a tight correlation with the CPI.

Thus, although it will come with a lag, we are fairly confident that higher CPI readings are expected by August or September.

Nevertheless, the magnitude of the rise in inflation and how sustained the price increase is will only be known when further macro data is released.

Now, let’s move on to the other pillar of the dual mandate, which could lead the Fed to move the needle on rates.