Welcome to the “Month In Charts” April Edition.

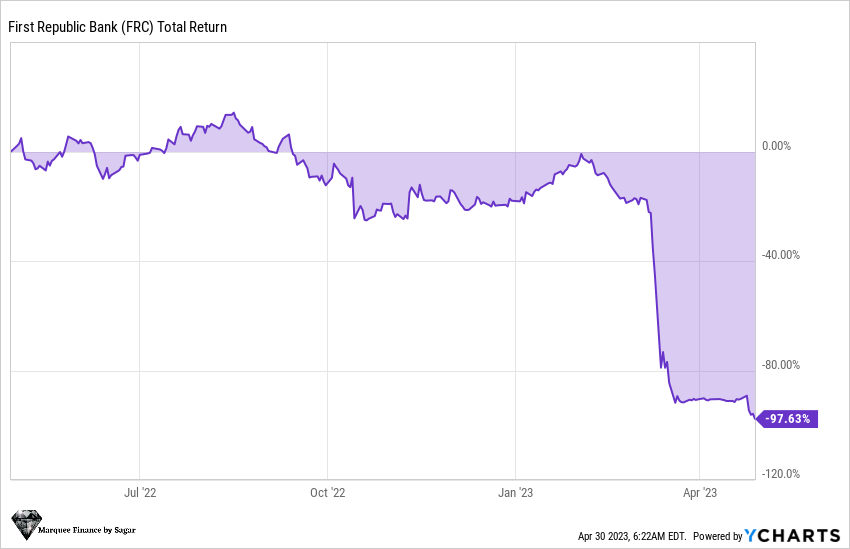

Let us start with the failure of the 14th largest bank in the US. FRC had a dramatic end as the stock price nosedived post earnings, and hopes of a revival were dashed.

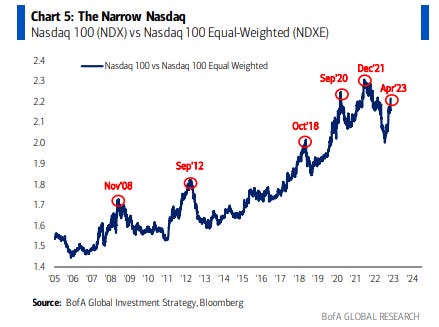

Regardless of the small banks’ fiasco, the equity markets, led by the Megatech names, rallied. The breadth has been really poor lately, and as a result, NDX has massively outperformed NDXE.

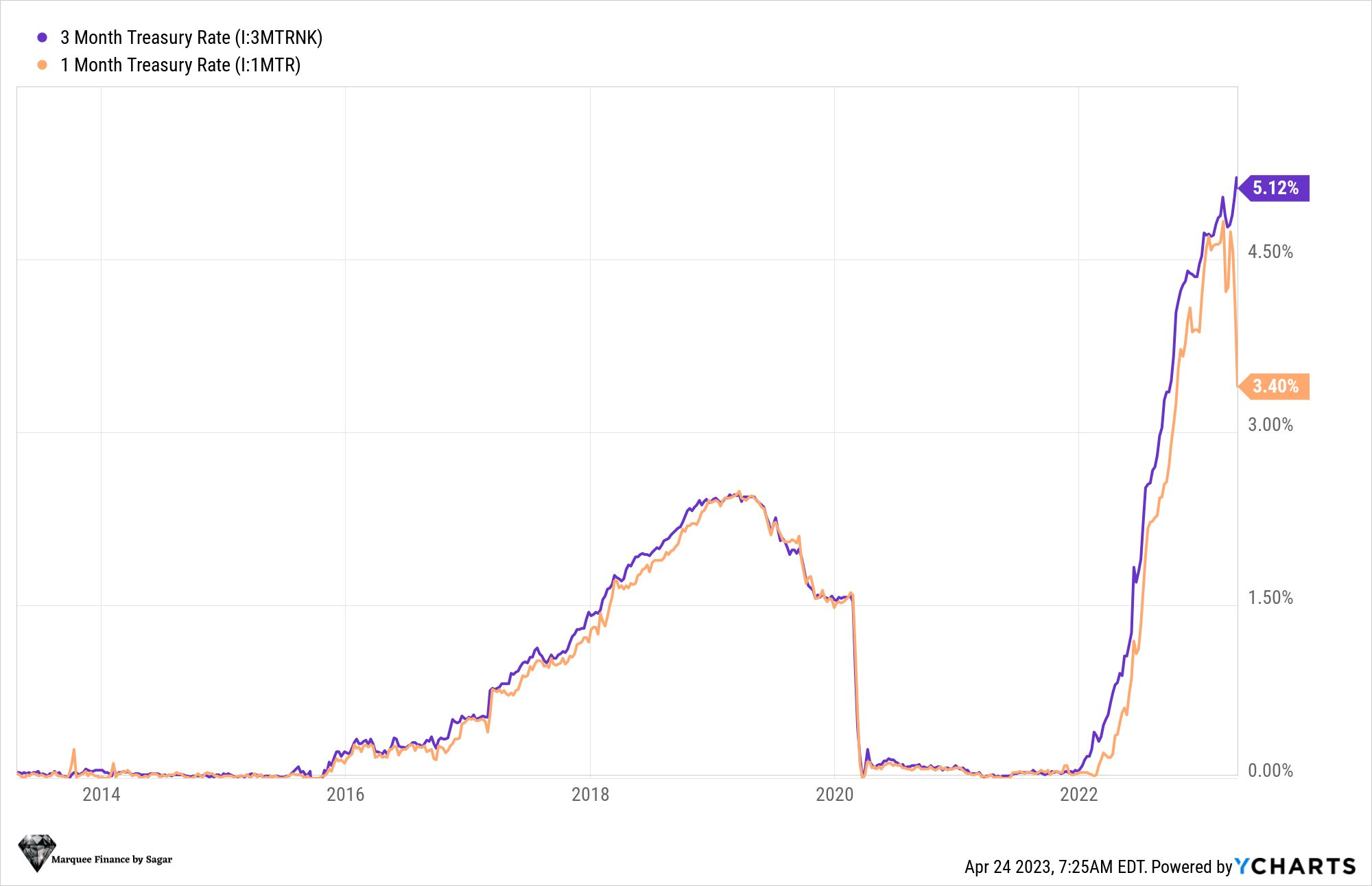

Source: BofA The bond markets got nervous on a likely debt ceiling hangover. As a result, the 1M T-bill and 3M T-bill decoupled, and the spread reached historic highs.

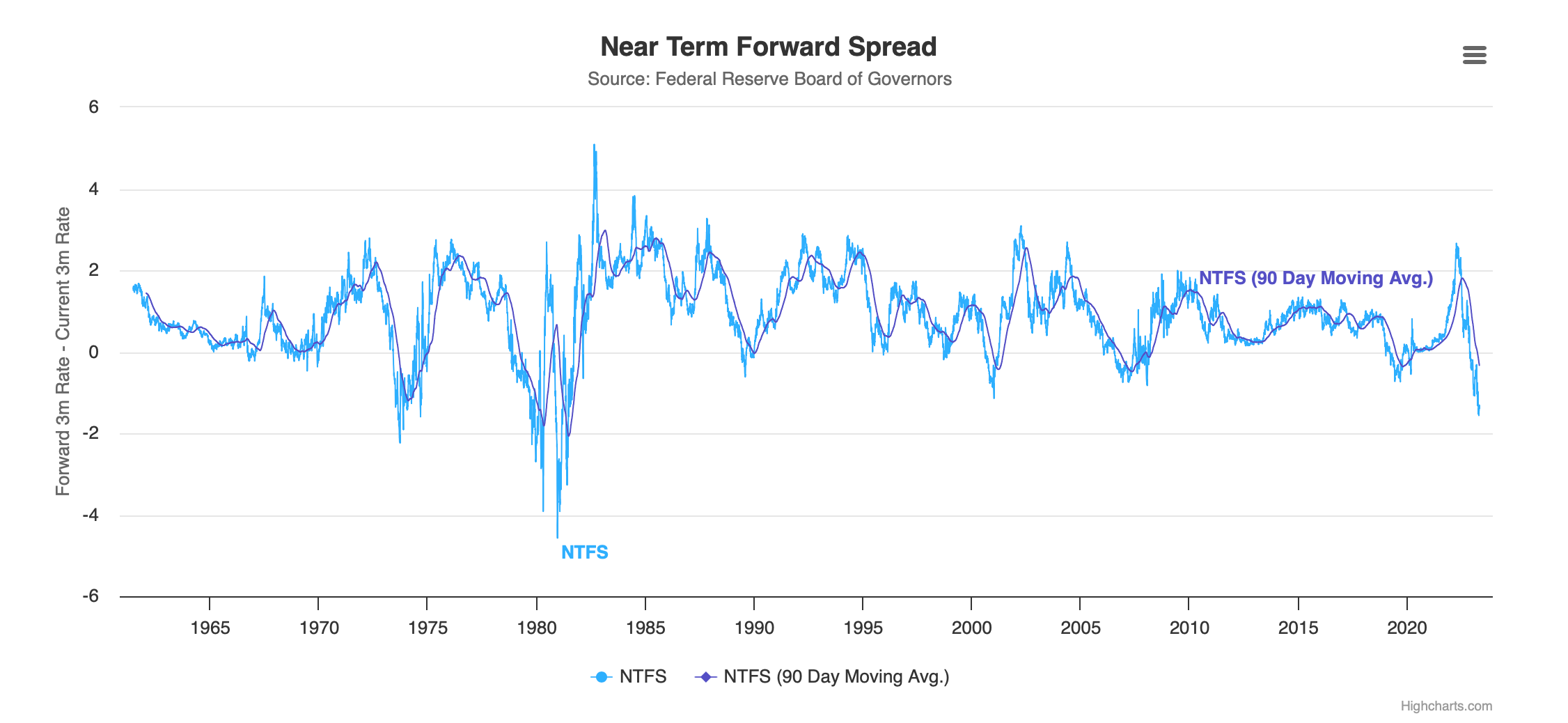

Source: YCharts Digging deeper into the bond markets, the JayPo favourite “recession” indicator (18-Month Forward- 3M rate) is now most inverted since the 80s. So in a nutshell, bond markets are screaming a recession.

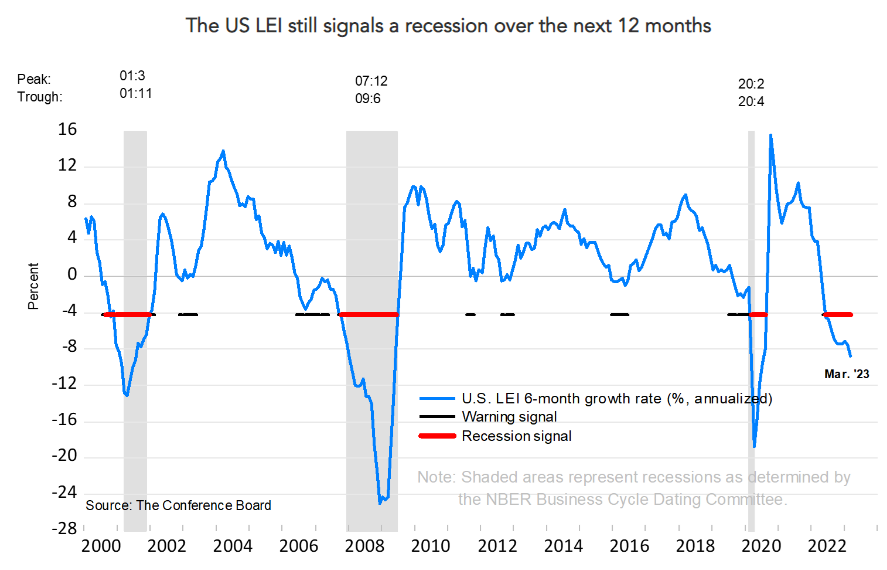

Bond markets are not alone, as the Conference Board Leading Indicator Index (LEI Index) is flashing red and predicting a recession in the next six months.

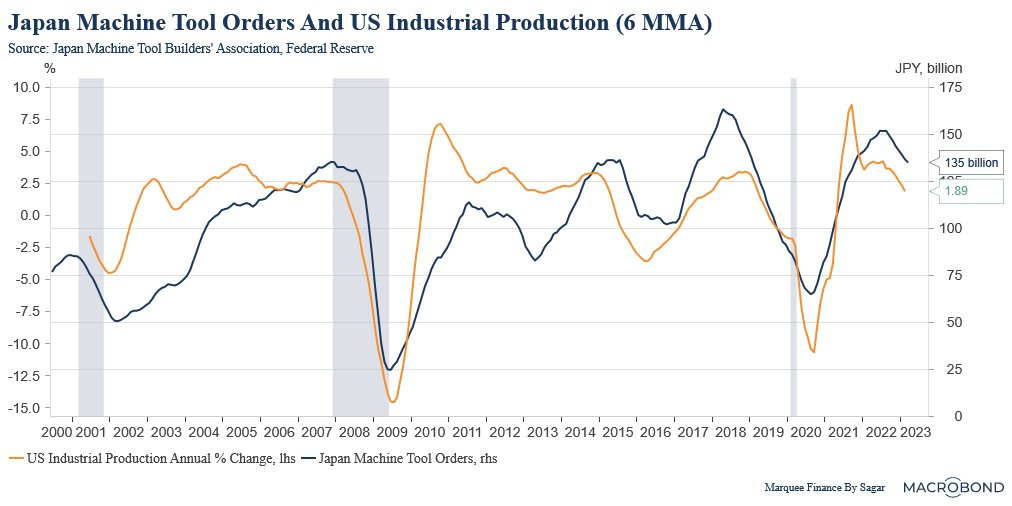

Source: Conference Board When we dig deep, the US cyclical sectors are witnessing a broad-based slowdown. Japanese Machine Tool Orders has an incredible record of predicting the cyclical peak and trough of the business cycles in the US.

Guess what: It has likely peaked!

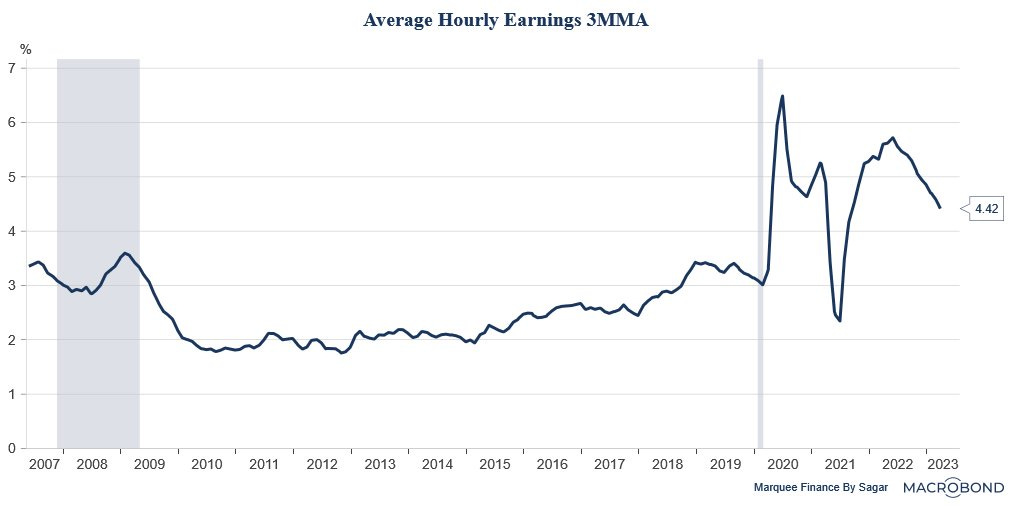

Source: Macrobond As the economy slows down and layoffs become broad-based, the most lagging indicator of the economy: “The labor market”, will likely cool. Wages are showing signs of a modest fall.

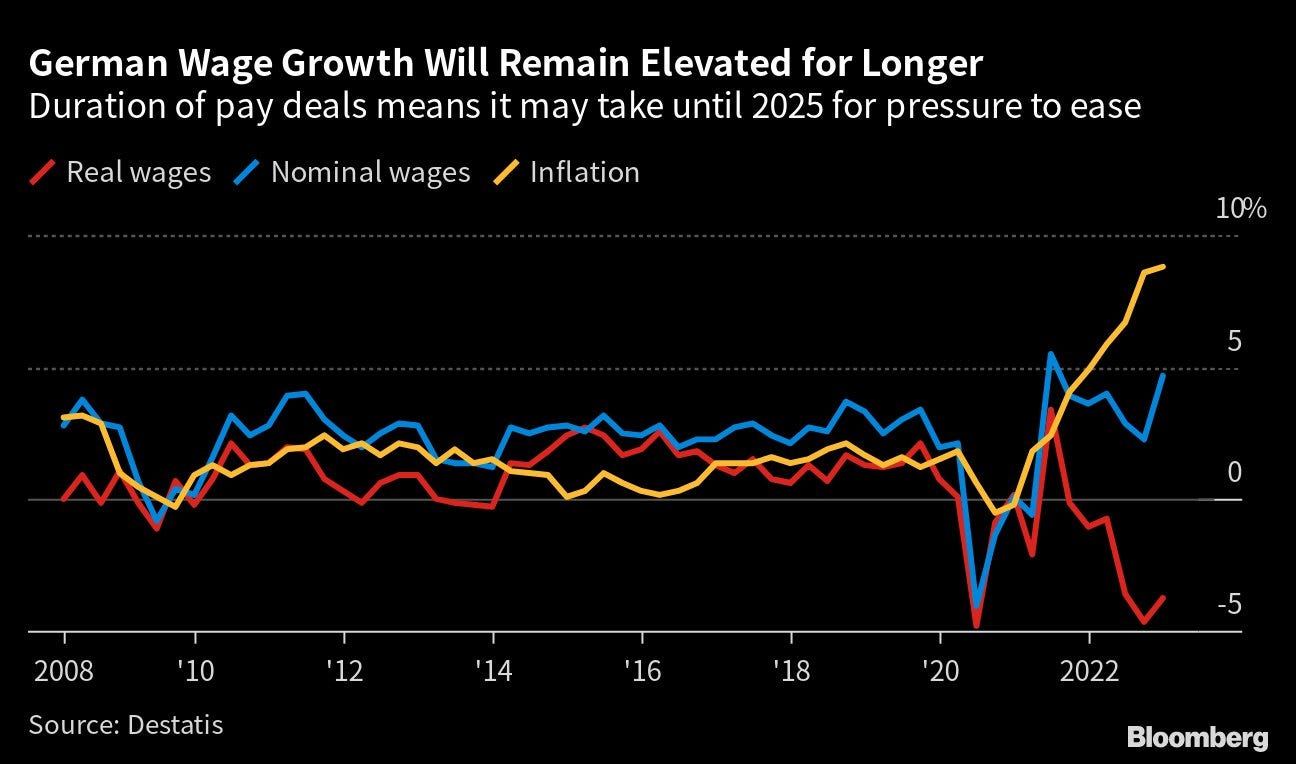

Source: Macrobond On the contrary, nominal wages across Europe are increasing faster. Unionization and sticky core inflation across Europe mean that the path to 2% in Europe will take longer compared to the US.

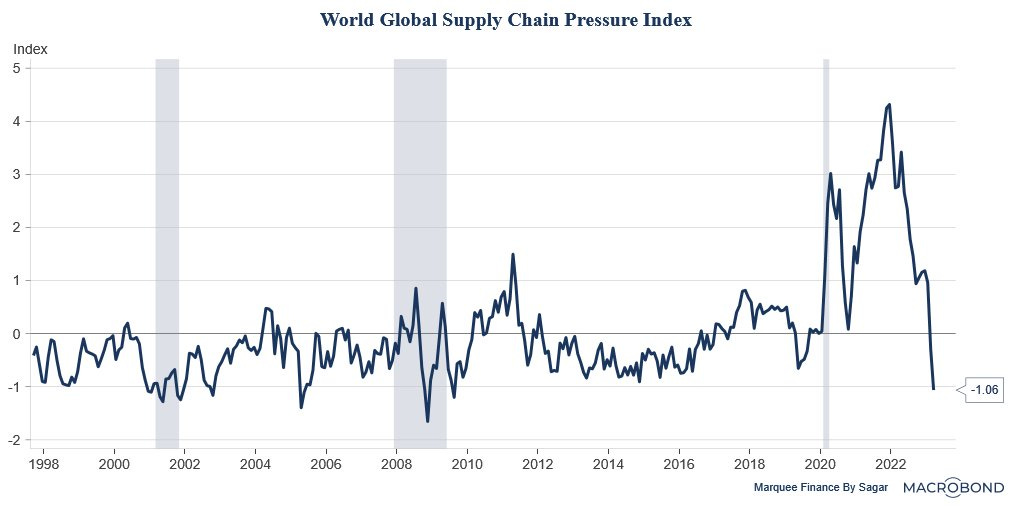

Source: Bloomberg As the global supply chains ease, one of the most significant factors contributing to the inflationary pressures in the West will fade away.

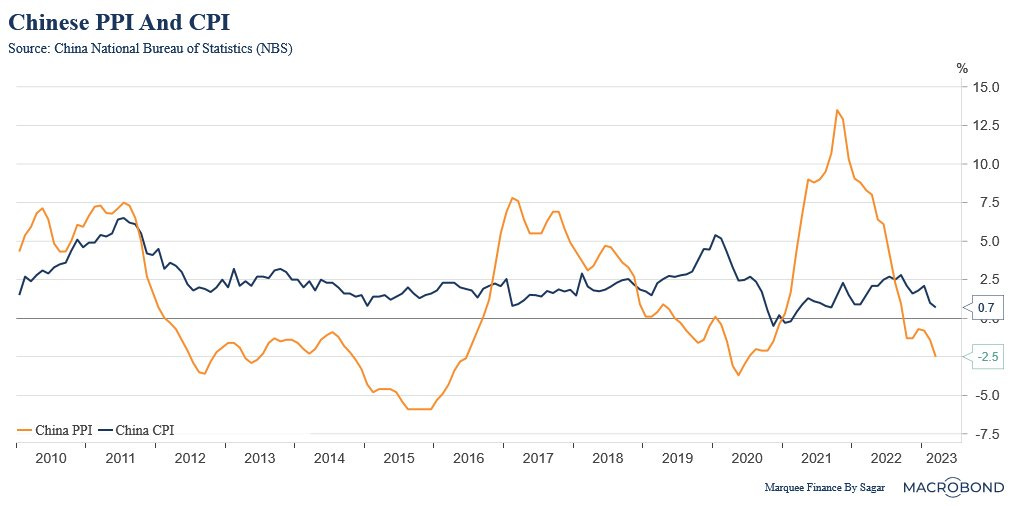

Source: Macrobond When we turn to the East, the world’s second-largest economy struggles as the property sector remains an overhang. Inflation is subdued, giving room to PBoC to further ease policy and provide stimulus to revive the animal spirits.

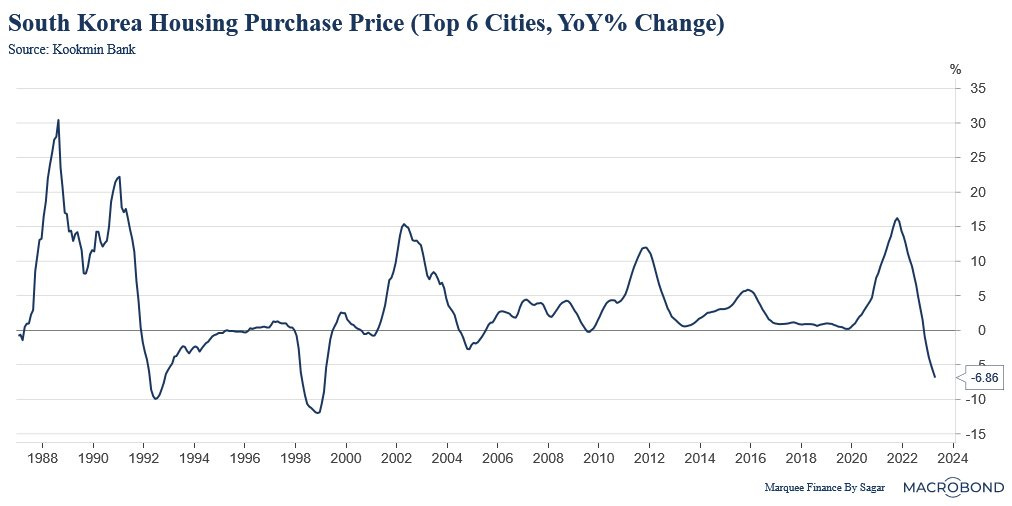

Source: Macrobond Another country in Asia where higher rates are taking a heavy economic toll is South Korea. South Korean assets: Equities and Real Estate have disappointed investors.

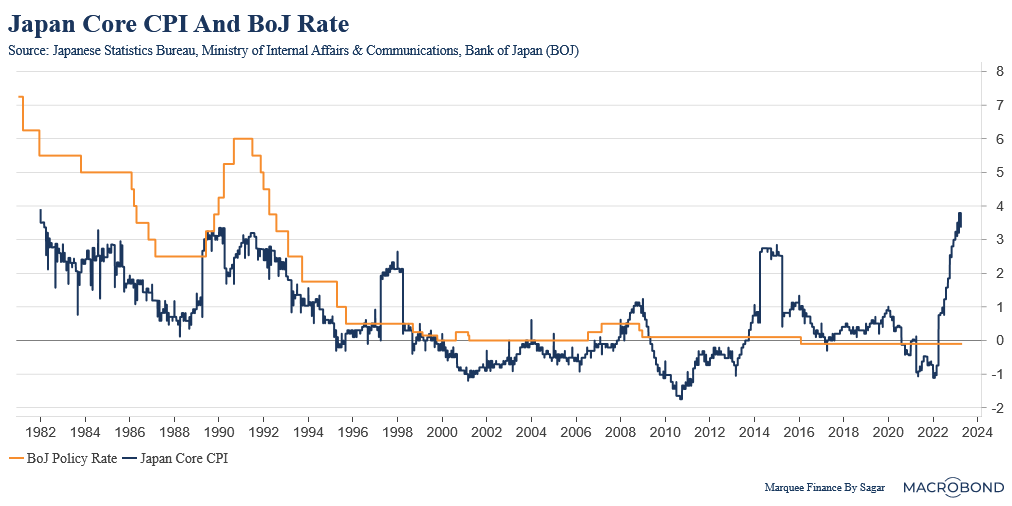

Source: Macrobond The newly appointed BoJ Governor Ueda gave a long time frame (12-18 months) to normalize the monetary policy even though core inflation continues to hit a fresh 40 year high.

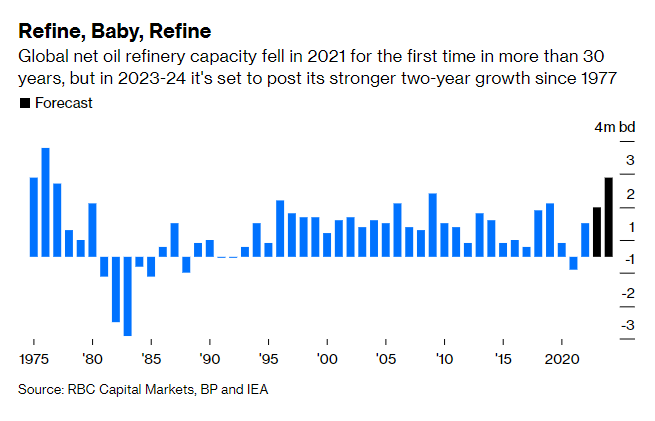

The biggest news in the oil and gas sector in April was that the world will finally add the much-needed oil refining capacity. (BTW, the 3-2-1 spreads have fallen off a cliff).

Source: Bloomberg Elsewhere in commodities, there was a divergent action. The sluggish Chinese RE sector means that industrial metals and commodities are cracking (recession fears in the West are helping).

Source: Bloomberg The commodity of the month was “Sugar” as the rally surprised the market participants. However, an unabated rally would mean the risk of higher food inflation in the coming months.

Source: Refinitiv, Twitter