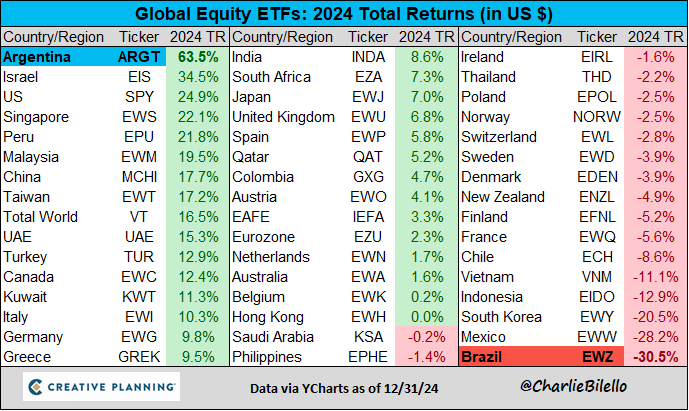

2024 was another year of superior equity returns, with the US markets outperforming the ROW (ex-Israel and Argentina).

Furthermore, there was no recession in the US thanks to the enormous fiscal spending by the US Government in an election year and the positive wealth effect of the exponential rise in the various asset classes ex-bonds.

Let’s look at what transpired in the global financial markets in December!

PS: From this week, the newsletter's timing has changed to Saturday: 7.30 a.m. EST/ 12.30 pm BST/ 6 pm IST.

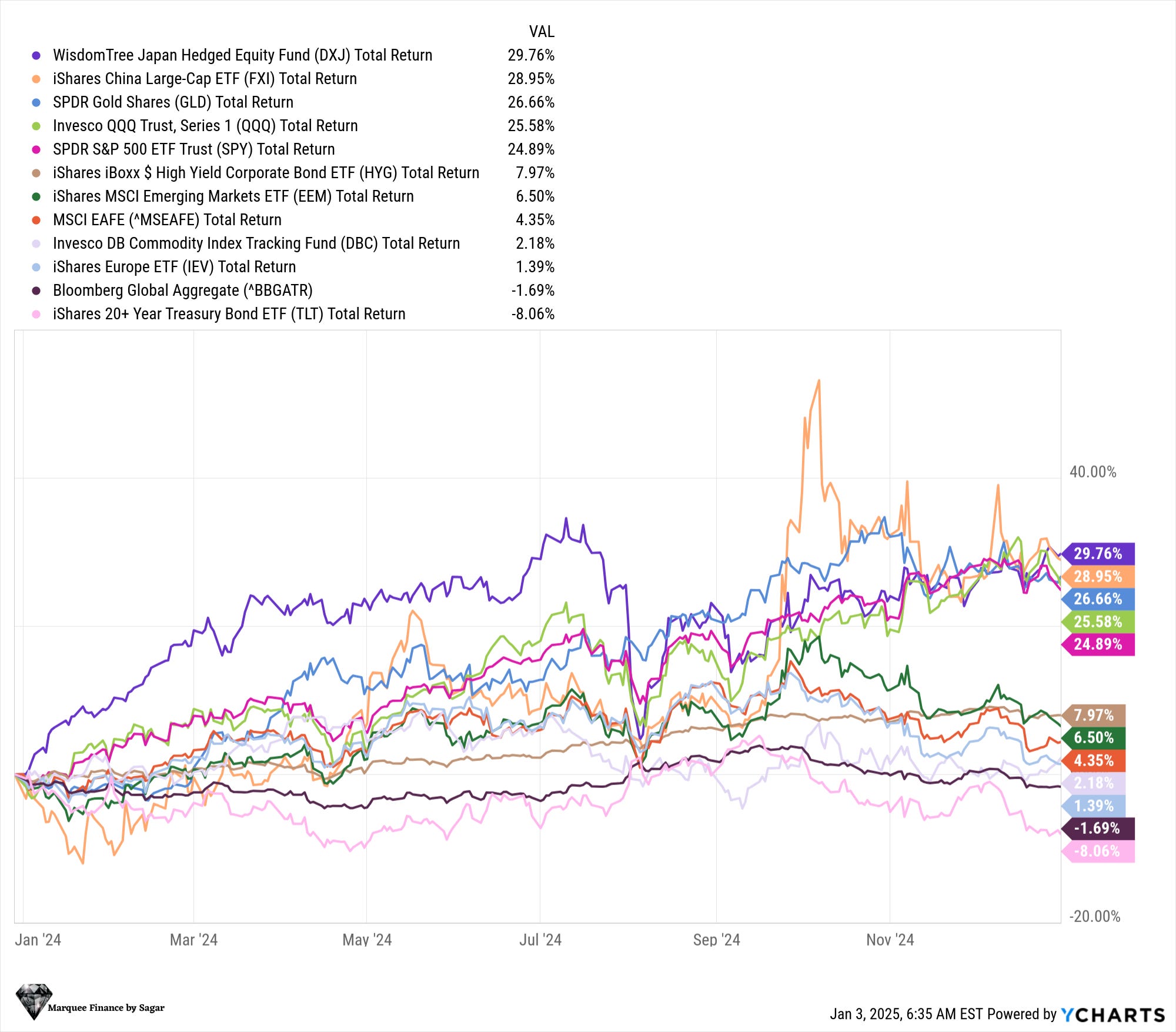

The hedged Japanese ETF (DXJ) was once again the star performer in 2024, with a total return of a whopping 29.76%, beating all the other asset classes (ex-BTC). Furthermore, the Chinese large-cap stocks ETF (FXI) outperformed the major US indices, bewildering most market participants.

The disappointment came from the bond markets, which had another year of negative returns and one of the longest bear markets in history. Nonetheless, if you owned Gold last year, you would have generated significant alpha as Gold was one of the top performers of 2024 with a 26.7% return.

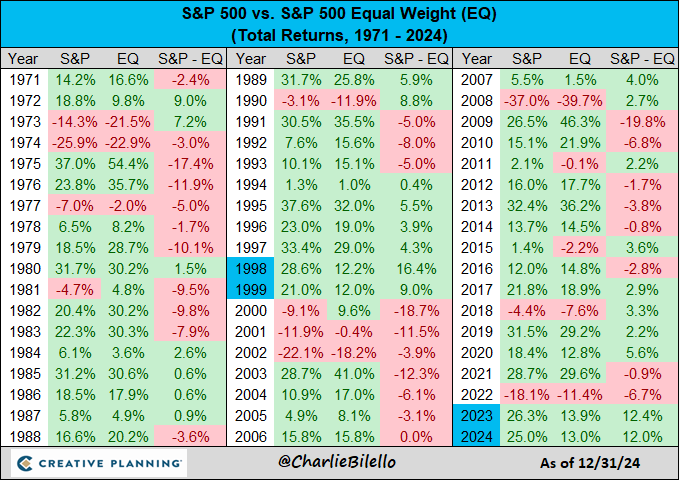

The US “exceptionalism” in equity markets was concentrated in a few names, as the broader market performance measured by the equal weight index underperformed for the second consecutive year (this transpired only once in history: 1998, 1999).

Source: Charlie Bilello Furthermore, the sheer outperformance (more than 120 bps) was mind-boggling.

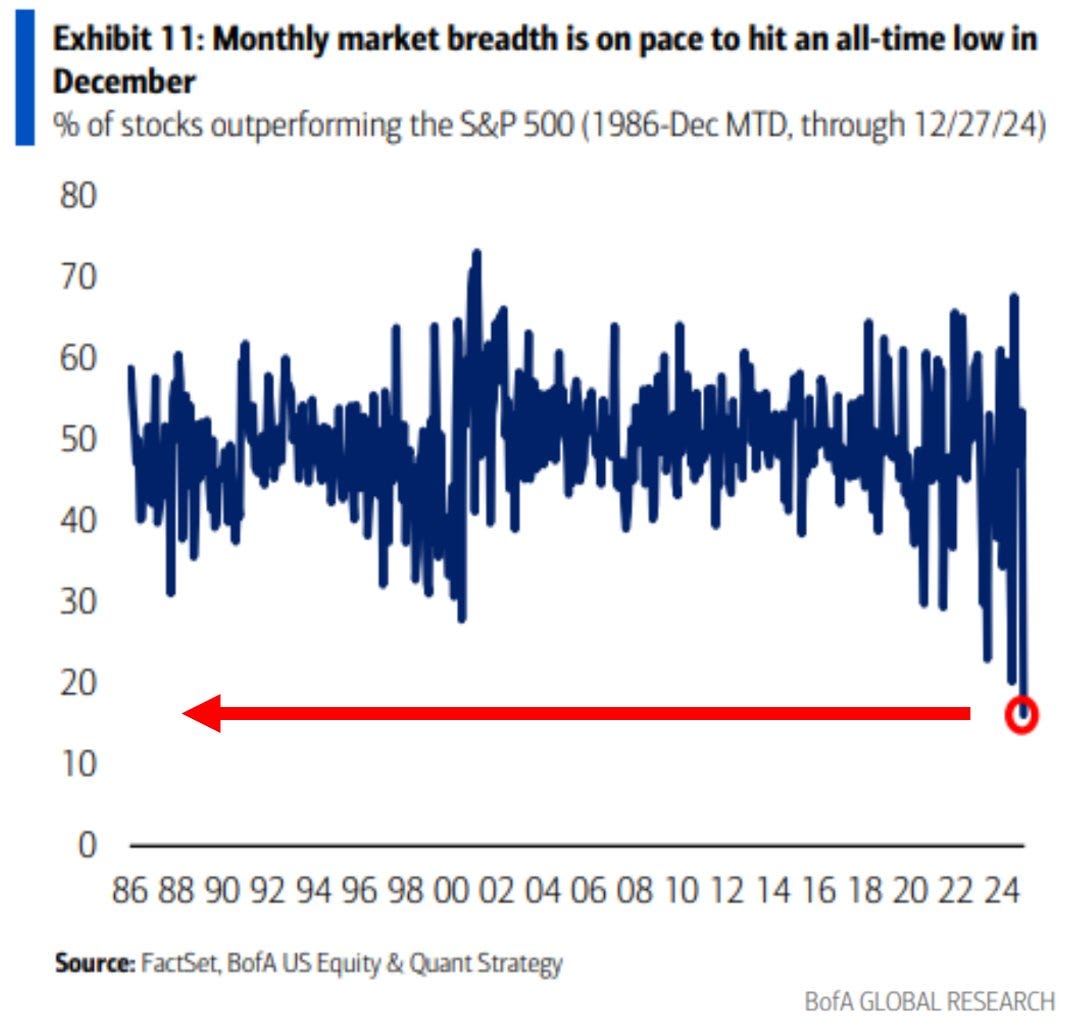

The trend of few stocks dominating the index was further exacerbated in December when the US equity markets witnessed the worst breadth on record. We will not be surprised if the broader market outperforms from hereon and the heavyweights pull down the index as earning season arrives.

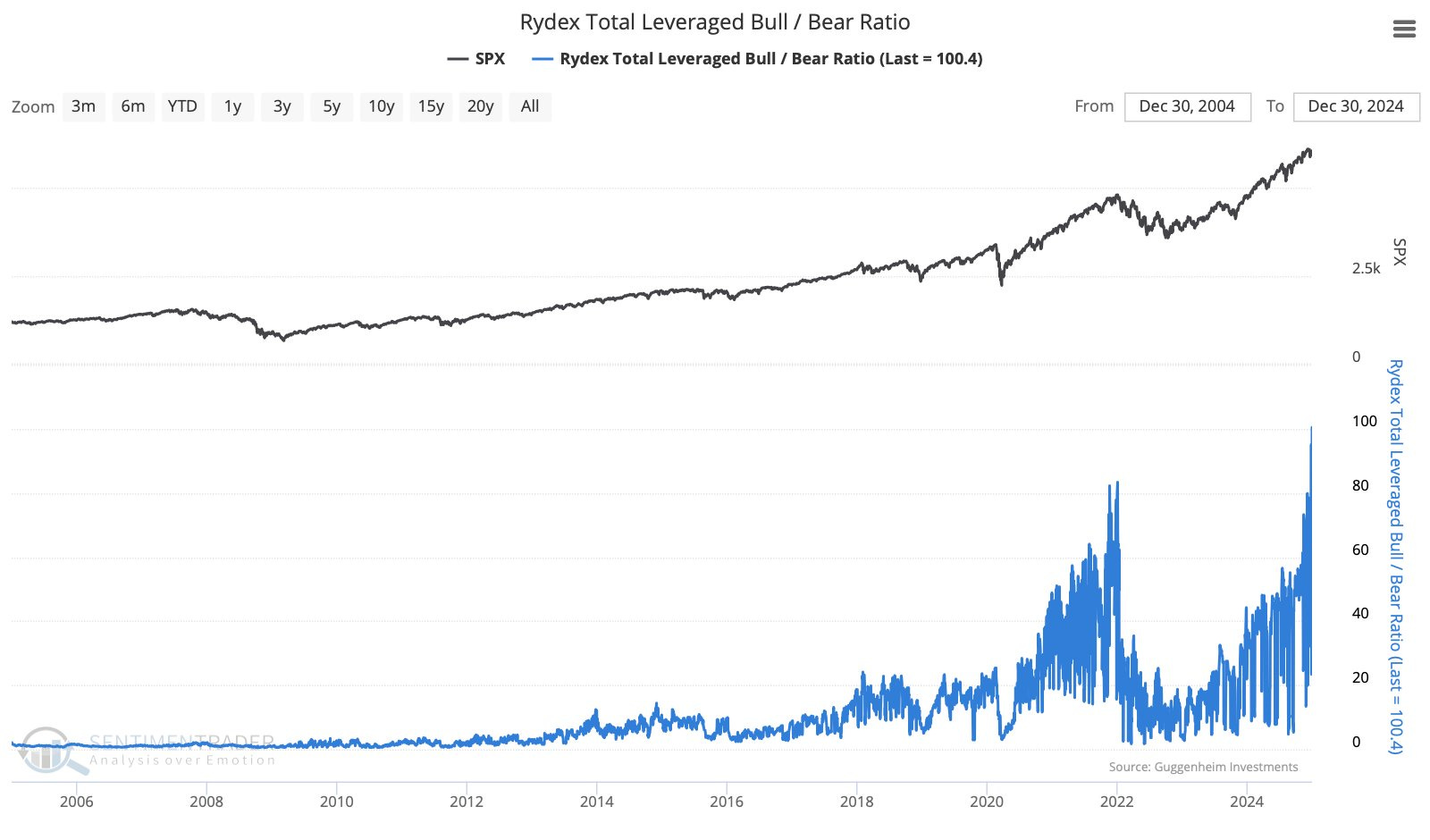

Despite the extremely poor breadth, the euphoria in US equities doesn’t seem to end, with the Leveraged Bull/Bear ratio at a fresh all-time high surpassing the 2021 GME mania.

The levered bull ETFs draw billions of dollars thanks to the speculative activity on NVDA, TSLA, and MSTR.

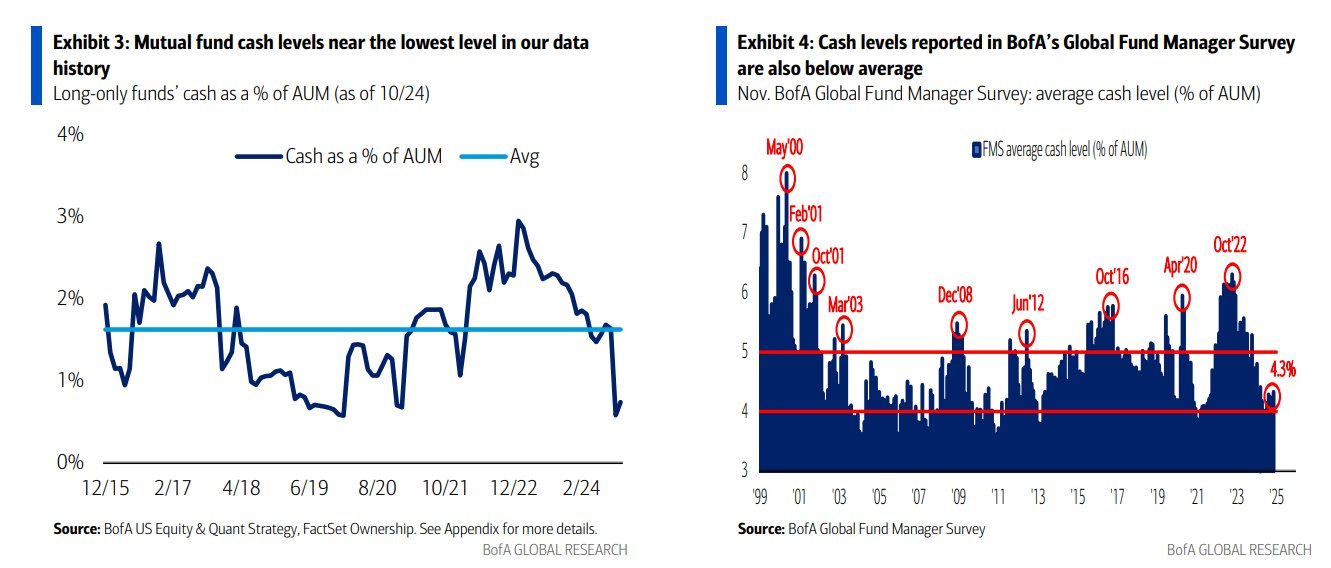

Not only has the retail public been in a frenzy, but the cash levels reported in BofA’s Global Fund Manager survey have also dropped to 11-year lows, indicating extreme bullishness.

Furthermore, the mutual fund cash levels reached a record low of around 1%!

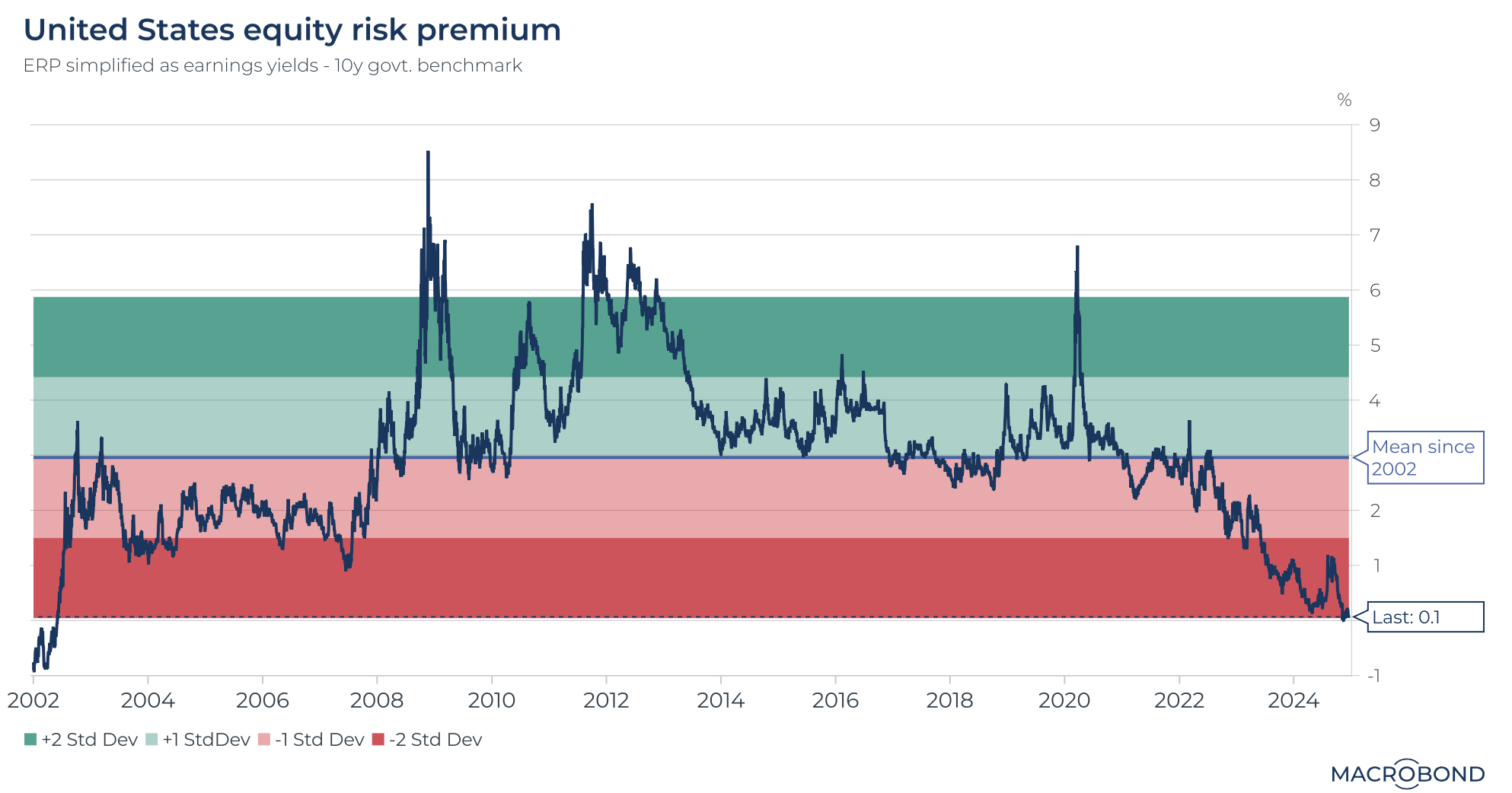

While stocks are back to their pre-Trump levels, the bond markets have acted strangely in the past few weeks.

For the first time in history, yields rose 100 bps after the Fed cut rates by 100 bps, rattling bond investors.

It has been indeed different this time until now!

Source: ZH

Rising yields and bubbly stock markets (extreme valuations) mean the equity risk premium has turned negative for the first time since the dot-com bubble.

Remember, markets can remain irrational longer than you can stay solvent!

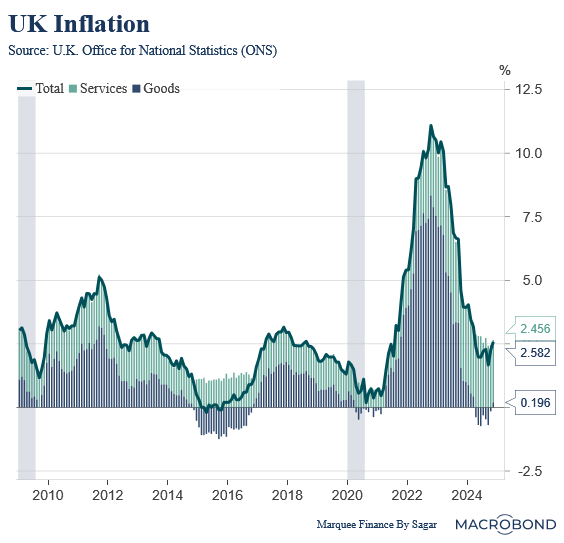

The BOE is the only Western CB (ECB, BOE, BOC and FED) which decided to maintain the status quo and not cut rates in December, as there is enough evidence that the UK’s inflation will rebound in the coming months.

Nonetheless, there are some concerns about the weak labour market and a slowdown in economic activity. Possible stagflation?

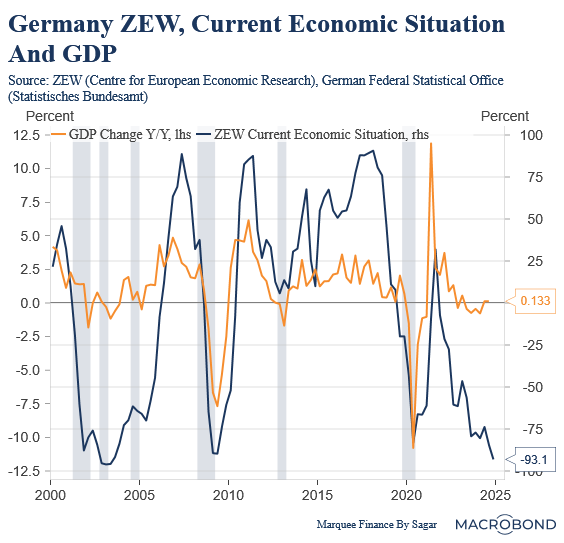

Sentiment in Germany continues to plummet to new lows every month as the European economy struggles to revive after the twin blows of the energy crisis and higher rates.

The ZEW Current Economic Situation is at 2002 lows and below the GFC and COVID levels.

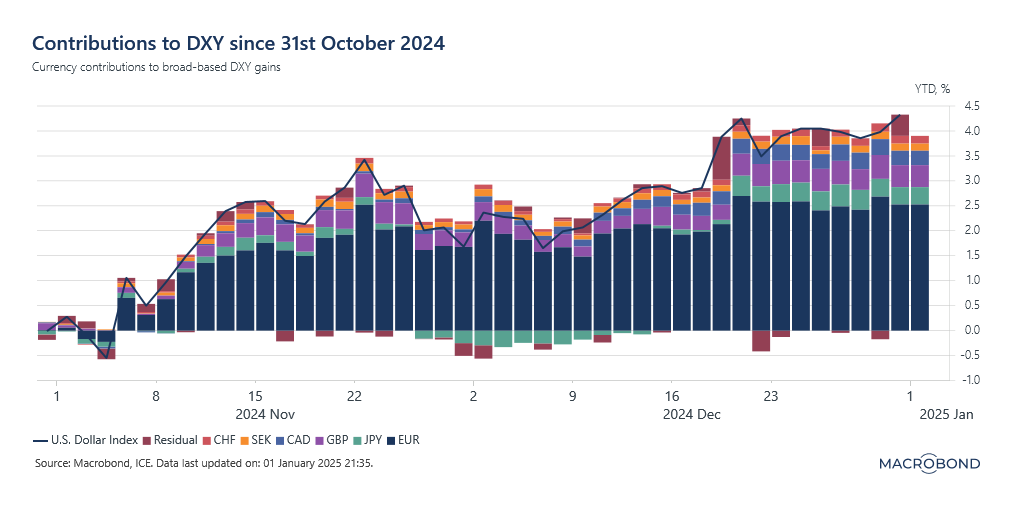

Since 31st October, the Dollar has seen a massive rally, with DXY under breakout territory, mirroring the rise seen in 2016 when Trump won for the first time.

Nonetheless, we have other factors, as the Fed's turning ultra-hawkish in the December policy added fuel to the fire. The biggest gains from DXY have come from the fall in EURUSD, which is getting closer to parity.

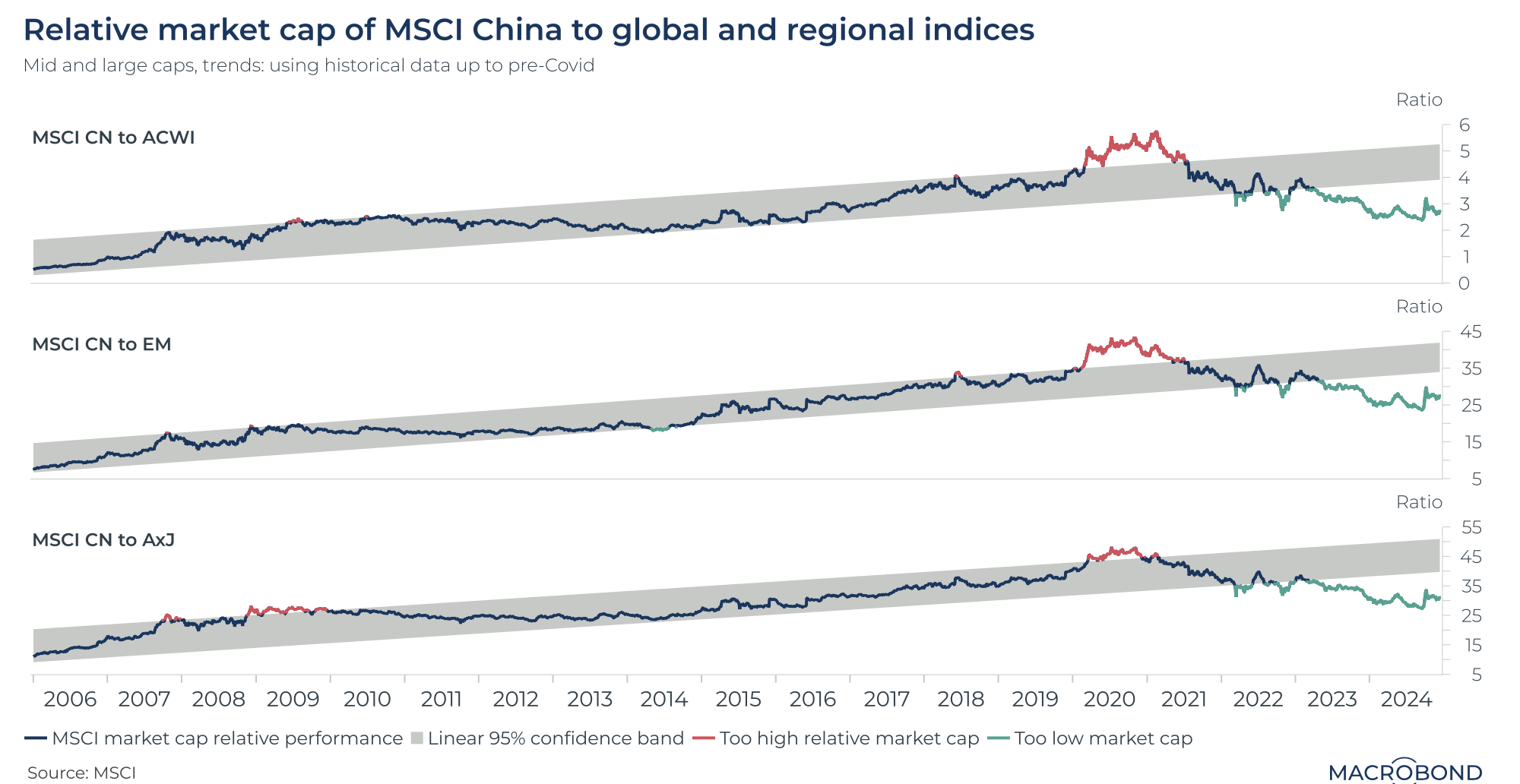

Despite multiple rounds of massive stimulus, China has been facing headwinds on multiple fronts, leading to significant underperformance.

As a result, the ratio of the MSCI China Index relative to the MSCI All Country World Index (ACWI), the MSCI Emerging Markets (EM) Index, and the MSCI All Country Asia excluding Japan (AxJ), which represents EM Asia is now at decadal lows.

With Donald Trump’s inauguration coming closer, China is preparing for escalation.

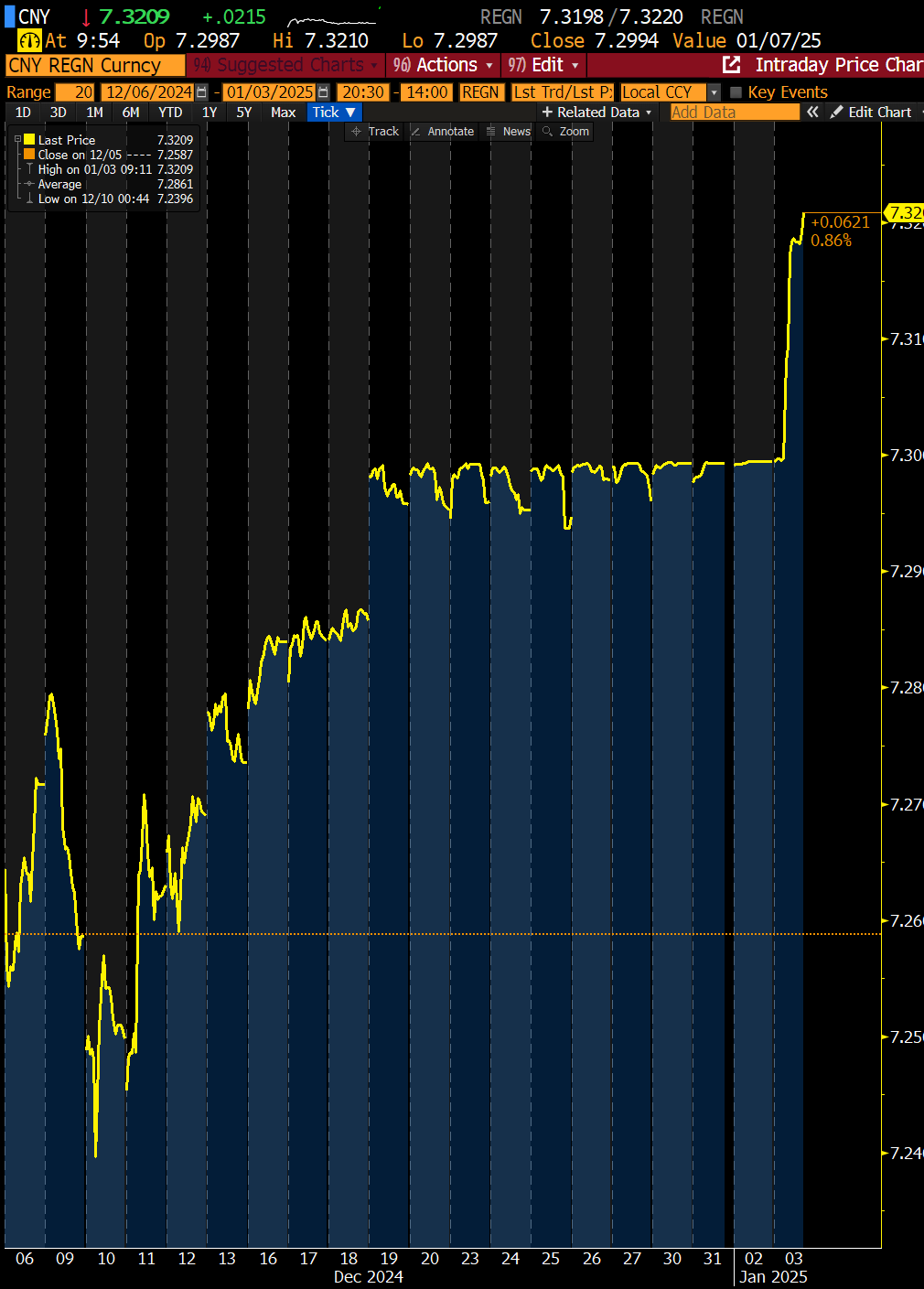

Furthermore, the bond yields have completely collapsed in the last few weeks, with the Chinese 10Y below 1.60%.

As a result, the Chinese government seems more tolerant of officially letting their currency weaken, with the PBOC letting go of the crucial 7.30 levels on CNH.

After retreating from 155 to 149 in November on “hopes” of a BOJ hike in December, USDJPY moved higher to 158 levels in December as the BOJ was as dovish as it could get, with the January hike also not in the picture.

Nonetheless, the last few day'’ move suggests traders are pricing in a more hawkish BOJ in January.

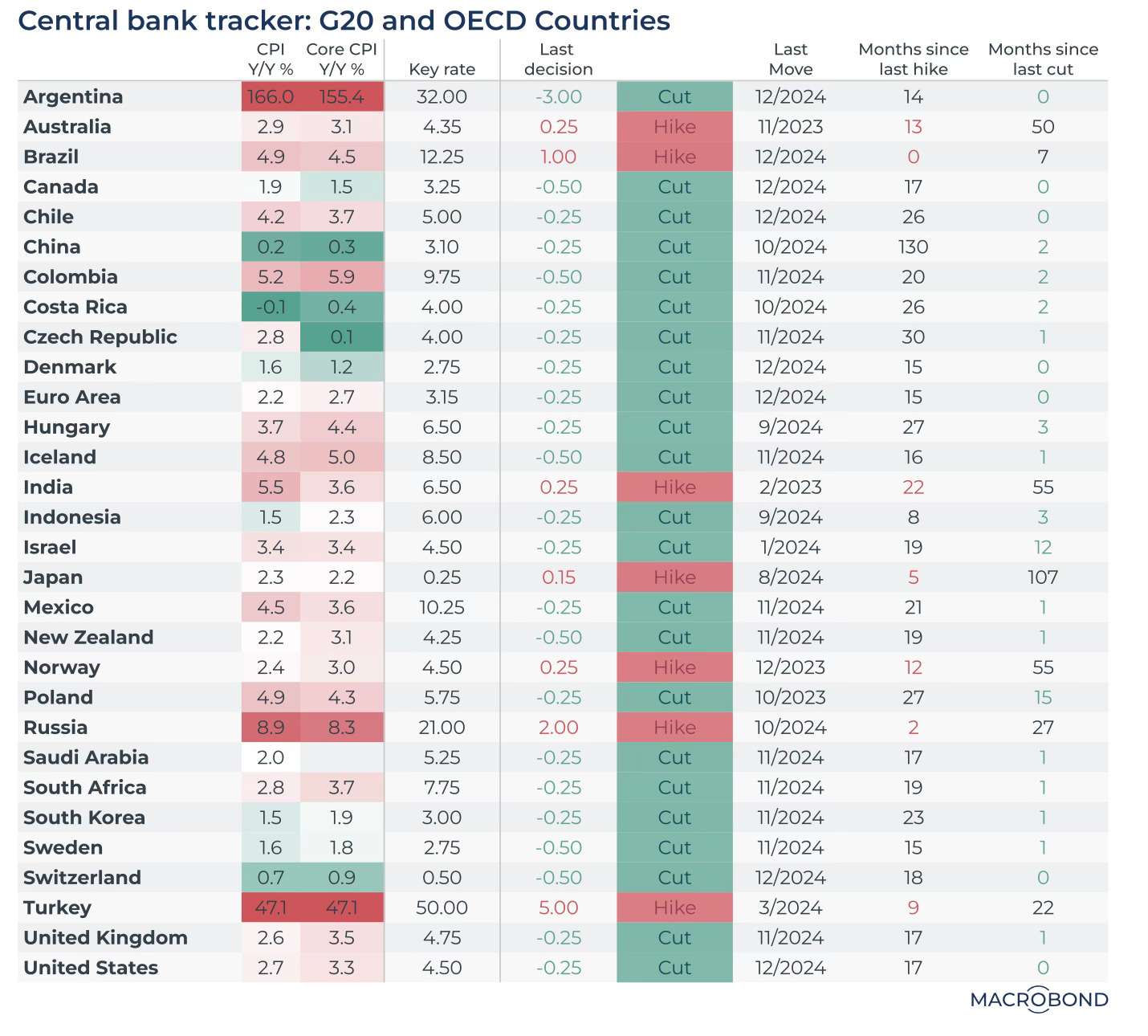

Brazil, Japan, and Russia are the only countries where the central banks have hiked rates. All the other central banks have transitioned into an easing cycle, cutting rates to support growth!

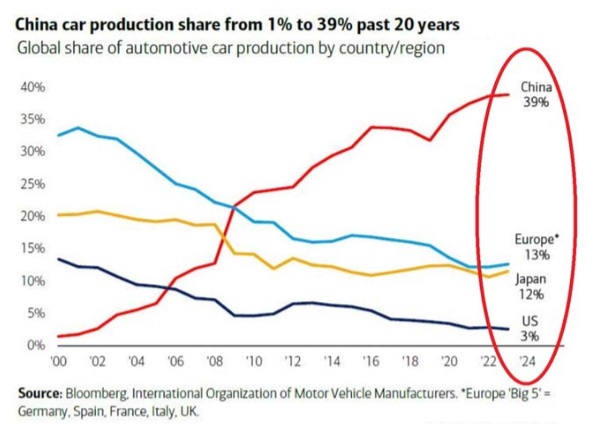

BONUS CHART: Mighty China is flooding the world with cars as Western OMCs struggle to compete. China has cornered the global automotive car production market share, as more than 39% of the vehicles are now produced in China. Furthermore, the US market share has declined from more than 13% to just 3% in the last two decades. We expect this figure to cross 50% as the EV revolution takes the world by storm.

Disclaimer

This publication and its author is not a licensed investment professional. The author & any other individuals associated with this newsletter are NOT registered as Securities broker-dealers or financial investment advisors with the U.S. Securities and Exchange Commission, Commodity Futures Trading Commission, or any other securities/regulatory authority. Nothing produced under Marquee Finance by Sagar should be construed as investment advice. Do your research and contact your certified financial planner or other dedicated professional before making investment decisions. Investments carry risk and may lose value; Marquee Finance By Sagar LLC, Marqueefinancebysagar.substack.com or Sagar Singh Setia is not responsible for loss of value; all investment decisions you make are yours alone.