2025 is turning out to be a year of “pain” for those chasing the winners of the past two years as the smart money rotates out of the overcrowded trades and piles into underowned asset classes.

Let’s understand what transpired in global financial markets in February with the help of 13 charts!

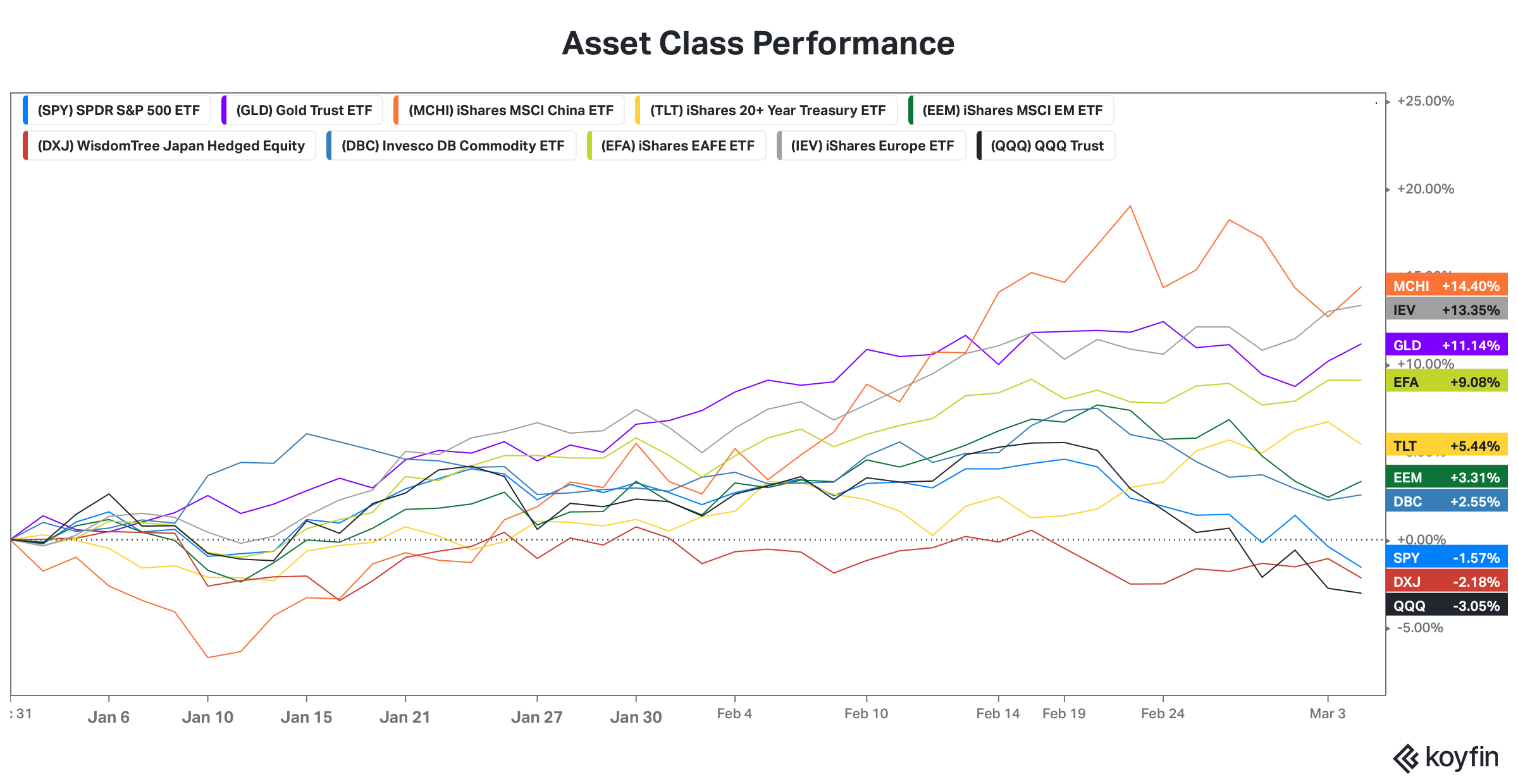

The world’s top-performing equity market for the last two years has seen enormous underperformance YTD as the overcrowded big tech trade unwinds. Furthermore, after Deepseek’s announcement, Chinese stocks have rebounded, with MCHI now the best-performing asset class YTD. Trump’s win has also been a big blessing for European stocks, with the benchmark ETF (IEV), the second best performer YTD, even beating Gold’s YTD returns.

Moreover, the most hated asset class of 2022,23 and 24 (long-duration bonds) is now outperforming stocks. Watch out for the negative correlation here.

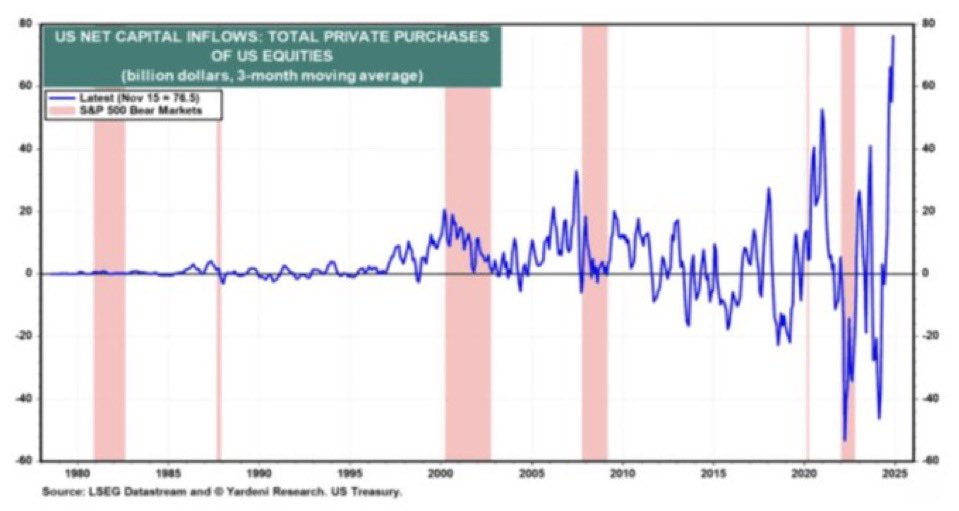

One of the contrary indicators defining a top in the US equity markets with an impeccable historical track record is overseas investors buying US stocks aggressively. Guess what happened in the last three months?

Foreigners bought $76.5 billion worth of U.S. Stocks from Nov 2024 - Jan 2025, the fastest 3-month pace in history. Historically, they have had poor timing, having bought right before the 1987 crash, the 2000 dot com bubble, and the 2008 global financial crisis

Source: Yardeini Research

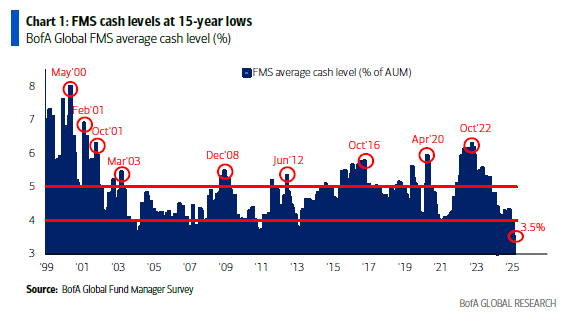

The biggest losers in this unprecedented rotation out of the tech stocks or broadly US equities to RoW have been the fund managers who were significantly overweight the US stocks. Furthermore, the cash levels was at 15 year lows at just 3.5% (one more signal predicting a top).

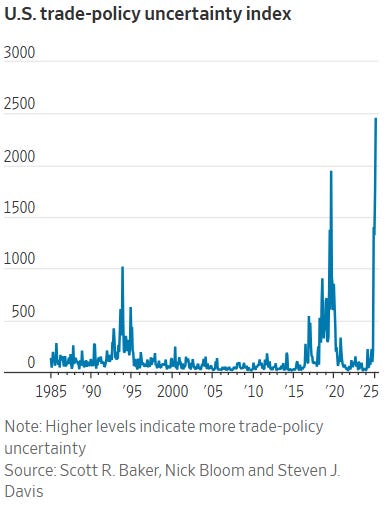

As the tariffs finally kick in on Mexico, Canada and China, the US trade policy uncertainty Index has climbed to all-time highs, making investors nervous about a recession induced by a trade war.

One can’t ignore the disastrous consequences of a massive tariff rise amid an uncertain geopolitical landscape.

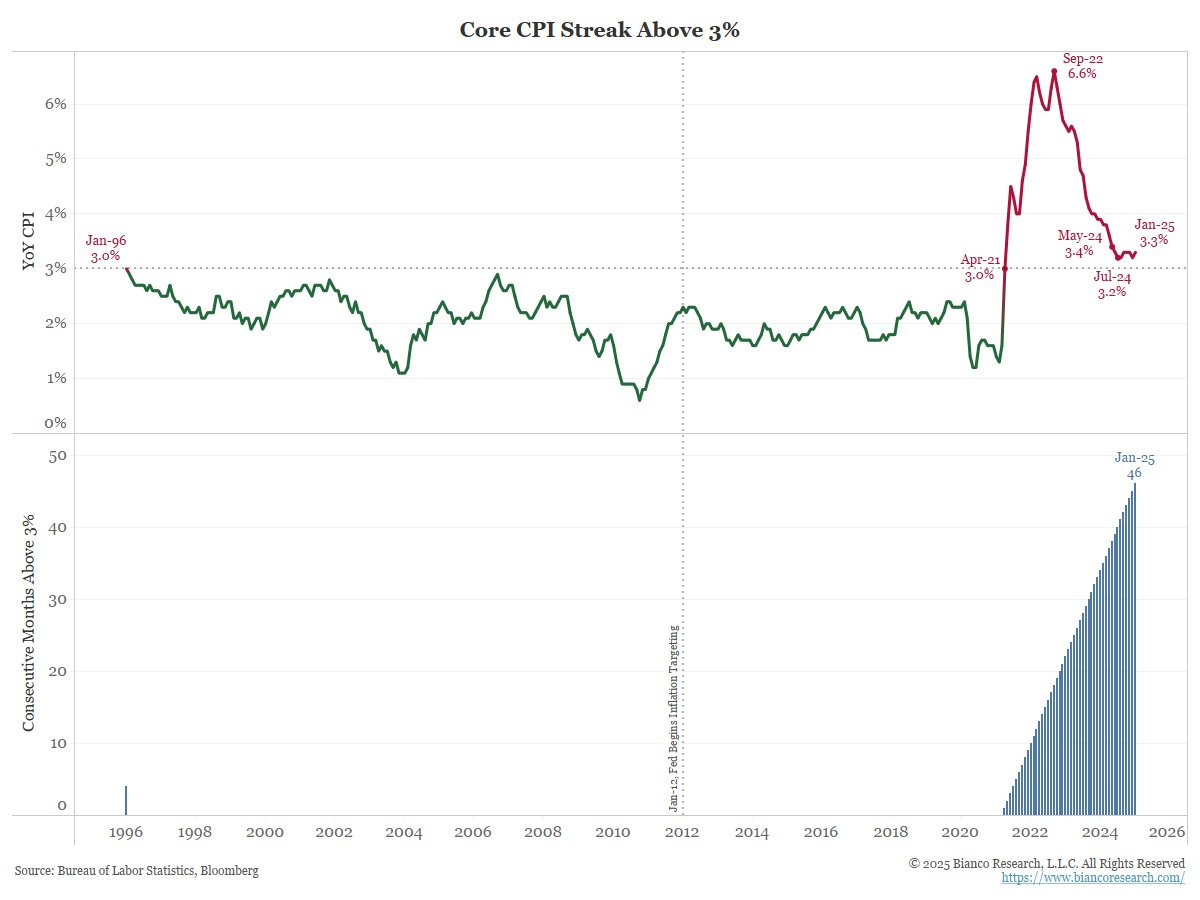

The biggest surprise in February was a higher inflation reading than street expectations. The YoY rise in Core inflation has been above 3% for more than 46 months in a row, a record last seen only during the period of draconian inflation/stagflation in the 1970s and 1980s.

Note that some market participants expect higher readings in the coming months due to higher tariffs.

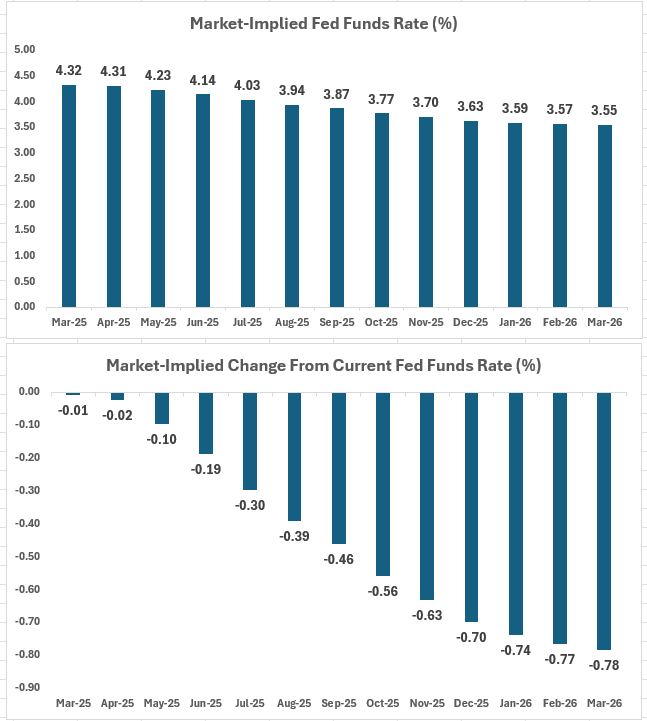

Since the Trump administration took office on January 20th, Bessent’s (Treasury Secretary) focus has been lowering bond yields (and it looks like they don’t care about stocks in the short term).

As a result, despite stagflation concerns and persistent higher inflation, bonds have outperformed stocks as recession fear mounts and markets price in more than three rate cuts this year.

Ironically, the dollar has been in a free fall in the last two days despite the implementation of tariffs. The weakness can only be explained by the deterioration in the US macro data and the rising recession probability.

Nonetheless, it seems Trump gets what he wants (lower yields, lower Dollar, tariffs, etc).

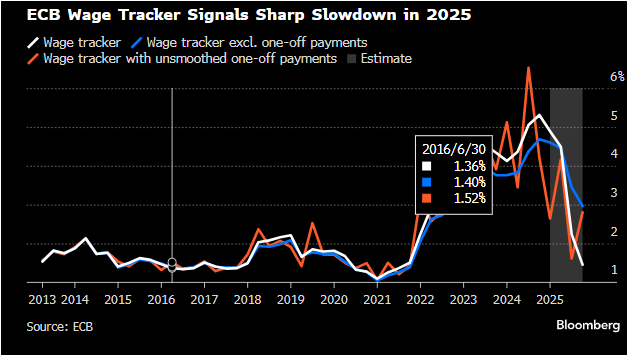

Wages in Europe have plunged to pre-war levels as the disinflationary trend picks up, giving the ECB enough room to cut rates more than the market expects.

Furthermore, as the trade war intensifies, with the US and the EU footing the bill for Ukraine, it’s a no-brainer that the ECB is stuck between a rock and a hard place. It's not a smooth ride here.

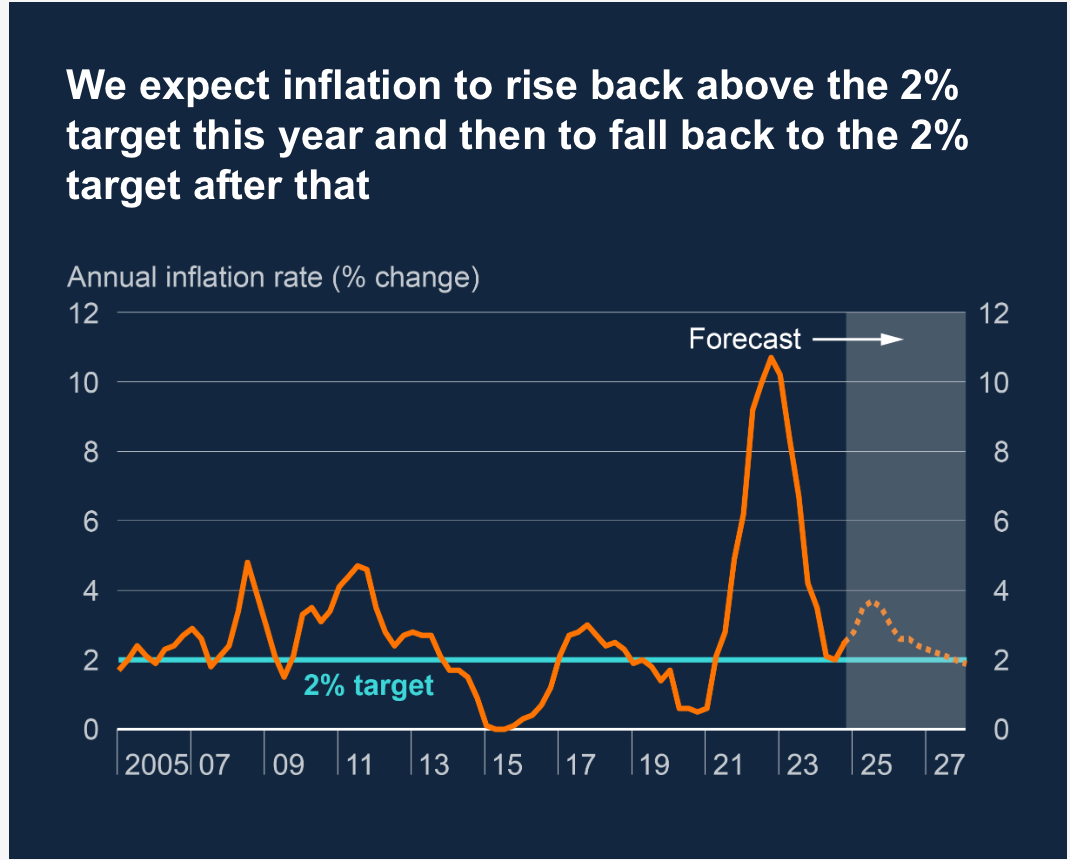

On the other hand, while the BoE cut rates by 25 bps in February, the BOE mentioned that the inflation ride was “bumpy,” and it forecasted that inflation would rise to 3.7% and then fall to the 2% target, but risks remain to the upside.

Note that we expect tariffs to be inflationary and thus must watch the inflationary trend carefully.

Surprisingly, only three countries in Europe (NATO) spend more than 2% of their GDP towards defence. Ironically, most of the European countries that were part of NATO used to spend 5% of their GDP on defence in the 1960s/70s.

The fiscal explosion in Europe is imminent as Europe readies to create a gigantic fund for defence purchases and as the US likely exits NATO.

The Deepseek announcement is likely the “ChatGPT” moment for Chinese equities, as the US drawdown has failed to shake out the Chinese rally.

Though there has been no material improvement in the Chinese macro data, the AI innovation can lead to the re-rating of Chinese stocks.

It's surreal that the inflation data in the land of the rising sun has now surpassed the CPI in the US.

Due to market expectations of persistently higher inflation, Japanese 10-year bond yields have surged to unbelievable levels (1.4%+).

This warning signal must not be ignored, as the reversal of carry trade can move trillions of dollars from the West back to Japan in the next few months.

Furthermore, BOJ has finally turned hawkish, and a further hike is possible in the coming months.

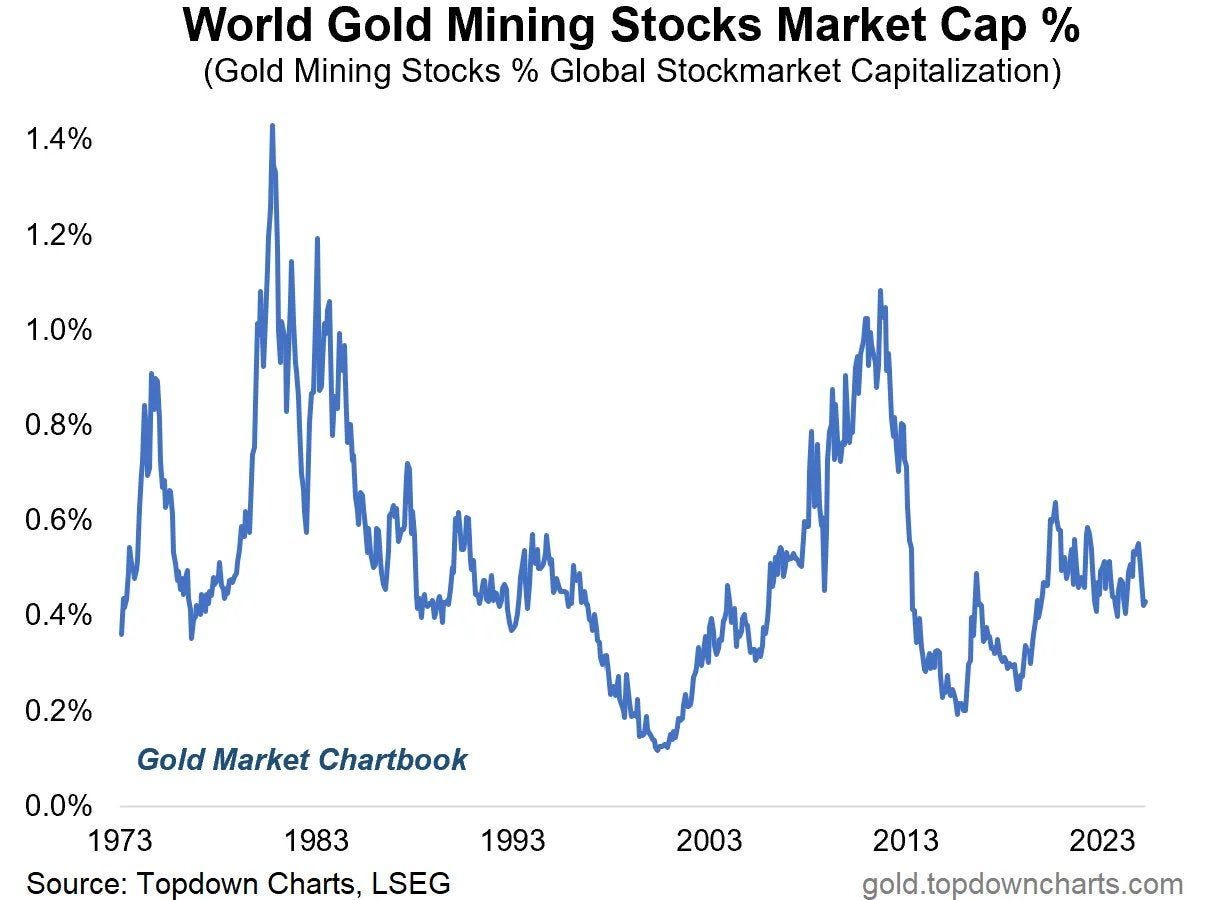

BONUS CHART: While Gold has seen a mega rally in the last 18 months, the mining stocks have been laggards, with the flagship mining ETF, GDX, still far away from ATHs.

As a result of underperformance, the Gold Mining stocks’ Market Cap as % of total Global Stock Market Capitalisation is at 0.4%.

Ironically, in the last Gold bull market (2003-2011), the market cap of Gold mining stocks as a percentage of the Global Stock Market Cap reached 1%.

Furthermore, the most significant cost for the miners has been oil, which has been in a bear market, thus increasing the profitability and margins of the Gold mining companies.

Disclaimer

This publication and its author is not a licensed investment professional. The author & any other individuals associated with this newsletter are NOT registered as Securities broker-dealers or financial investment advisors with the U.S. Securities and Exchange Commission, Commodity Futures Trading Commission, or any other securities/regulatory authority. Nothing produced under Marquee Finance by Sagar should be construed as investment advice. Do your research and contact your certified financial planner or other dedicated professional before making investment decisions. Investments carry risk and may lose value; Marquee Finance By Sagar LLC, Marqueefinancebysagar.substack.com or Sagar Singh Setia is not responsible for loss of value; all investment decisions you make are yours alone.