2025 has begun with a bang for those who love “volatility,” as we have been bogged down with insane cross-asset moves in the past month, especially since the Trump administration took office.

Let’s look at what transpired in the global financial markets in January!

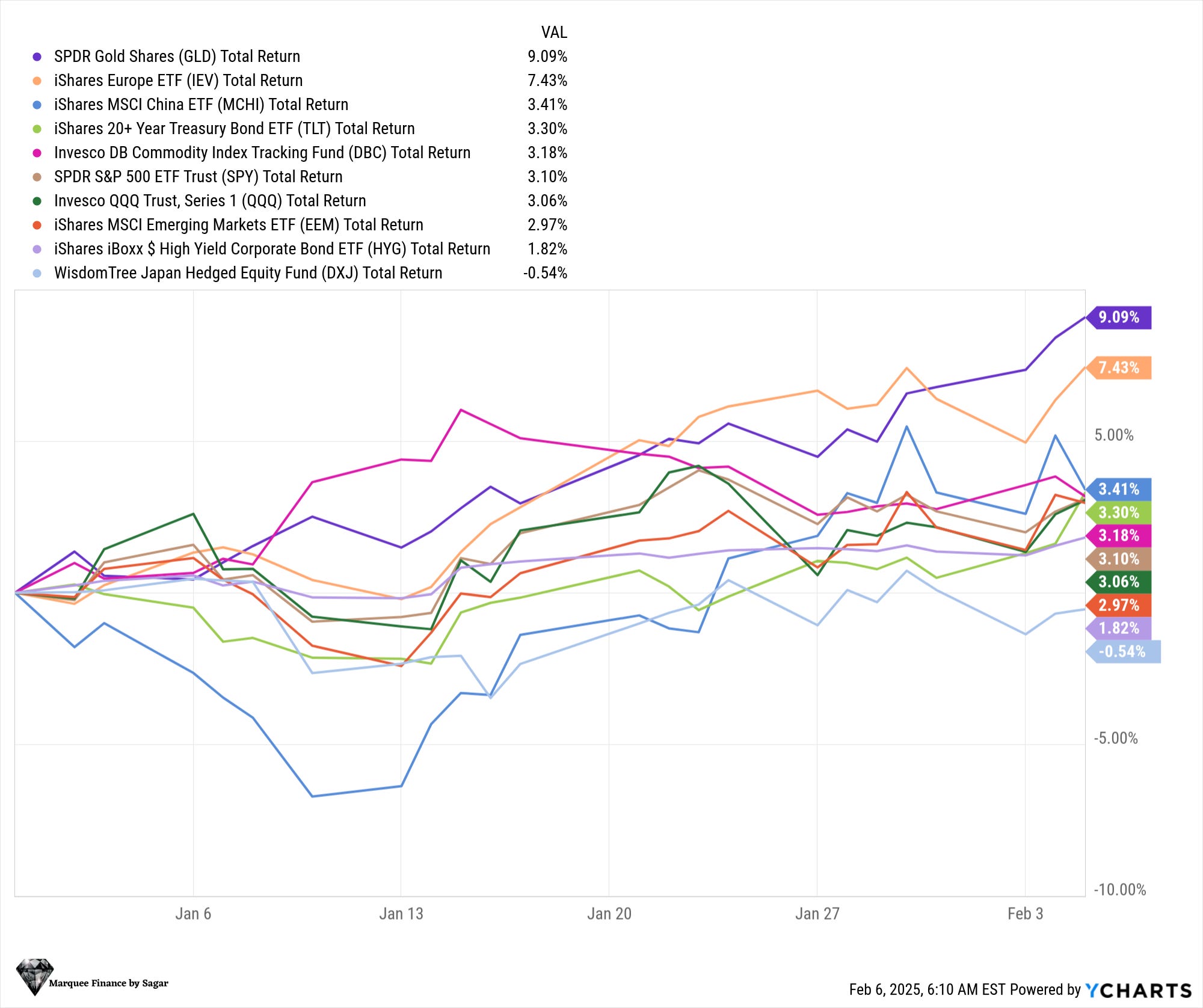

While everyone piled onto Mag 7 post-Trump win in November, January was one of those months when the market bid up the under-owned and most hated stocks. You will be surprised to know that up to 5th February, Europe and China outperformed the US indices by massive margins.

Furthermore, the most hated asset class of the last two years saw an enormous rally, as long-duration bonds are now outperforming stocks YTD.

Commodities have also been rallying hard, with the shiny yellow metal shattering all records as it gained by more than 9% in just one month.

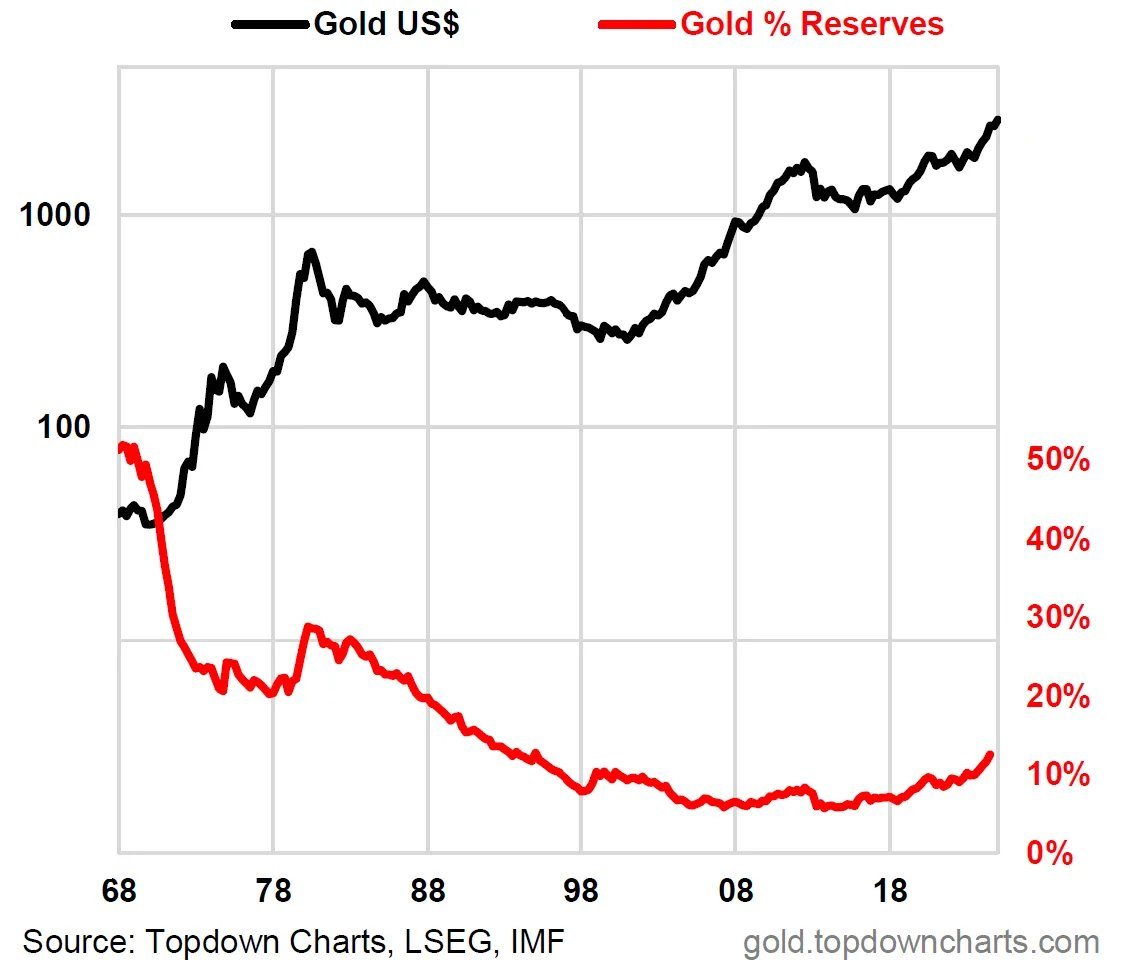

Since Gold is on everybody’s mind, let’s begin with it. One of the reasons for this super bull market in Gold has been the persistent buying by the Central Banks.

In fact, global reserve allocations to gold have doubled over the past 10 years, with Russia, China and India being the top buyers of the shiny yellow metal.

The rise in January in Gold prices was due to a mad scramble by the institutions to repatriate the Gold to New York due to fear of tariffs.

As a result, the COMEX warehouses saw a massive surge akin to COVID-19 and the price spread between COMEX and LBMA surged.

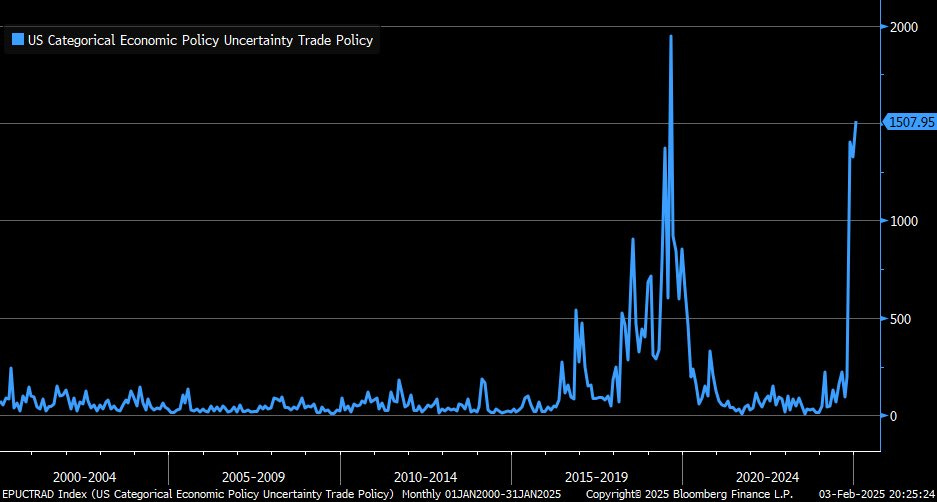

With a lot of flip-flops on tariffs amid last-minute deals and extensions, the uncertainty about the US Trade Policy has shot up dramatically.

The Economic Policy Uncertainty (Trade Policy) Index is now up to the levels last seen during the peak of the US-China Trade war in the last Trump administration.

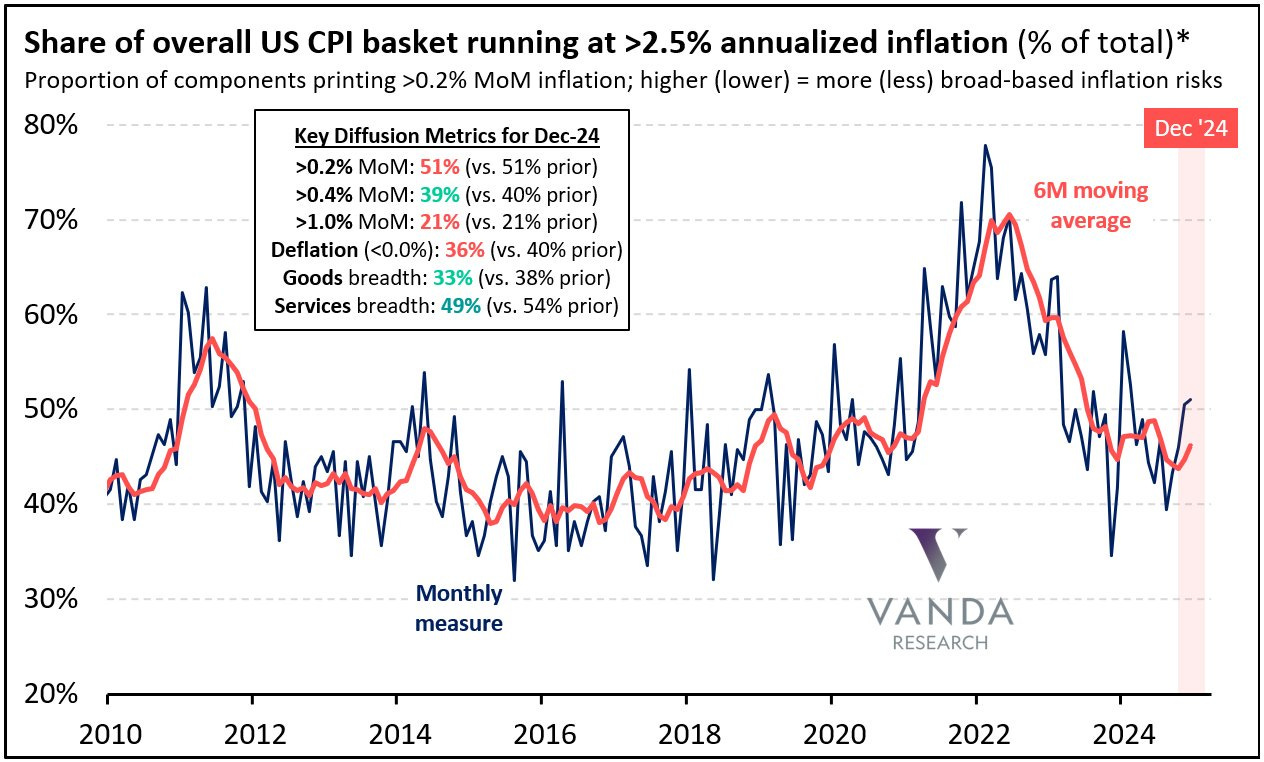

Trump wants lower inflation and, hence, lower yields, but he has a cause for worry. There are initial signs of inflation bottoming out, especially across Goods, as the diffusion metrics indicate that the items running at >0.2 % MoM have bottomed out at 51%.

Last month, we wrote that European stocks are at an extreme discount to their US peers as the “US Exceptionalism” narrative took fund managers by storm.

Nonetheless, we saw a sea change in January as European stocks were on a tear. In fact, we saw the second largest-ever monthly rotation into EU stocks in the past 25 years.

A wild, wild move!

One asset class with a super roller coaster ride in January was the Dollar, as the tariff U-turns led to highly volatile moves.

MXN and CAD were the worst-performing currencies due to tariff fear, and many market participants predicted that both countries would enter into a recession if 25% tariffs were implemented.

Source: Hourly Chart DXY

Many market participants expected the Fed to announce some tapering in its QT program in January, but this didn’t transpire, as JayPo categorically mentioned that they would continue to reduce their balance sheet as planned.

Notably, the Fed’s balance sheet has already contracted more than 24% from the peak (which is, in fact, the highest-ever drawdown).

We had the UK bond scare in January when the yields on the 10Y in the UK jumped sharply after fears about the government's fiscal deterioration rose.

The bond sell-off deepened worldwide, with the US bond yields rising as well. Nonetheless, there has been a significant cooling off in the yields, and they have filled the gap of 16th December.

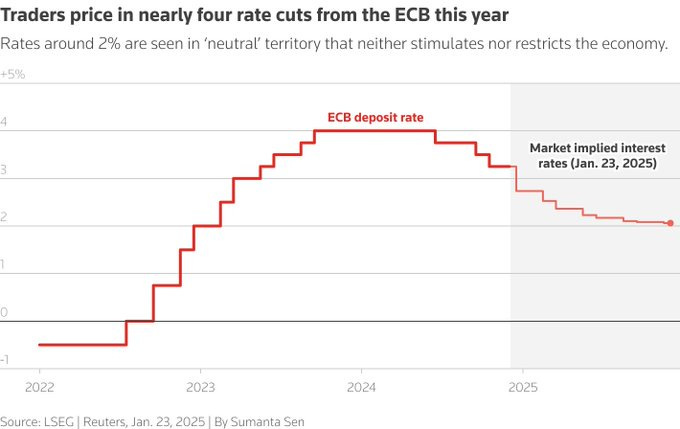

The European economy seems to have recovered from the cyclical slowdown. Furthermore, the ECB and BoE cut rates in January and today, respectively.

Traders are pricing in four more ECB cuts this year, which is supporting European stocks in their ride-up.

China has been under severe stress due to a balance sheet recession. Thus, CCP and XI are very well aware that they can’t afford a full-blown out trade war.

We are witnessing early signs of bottoming out in the Chinese housing market. However, we will look for further cues to ascertain whether the recovery is sustainable.

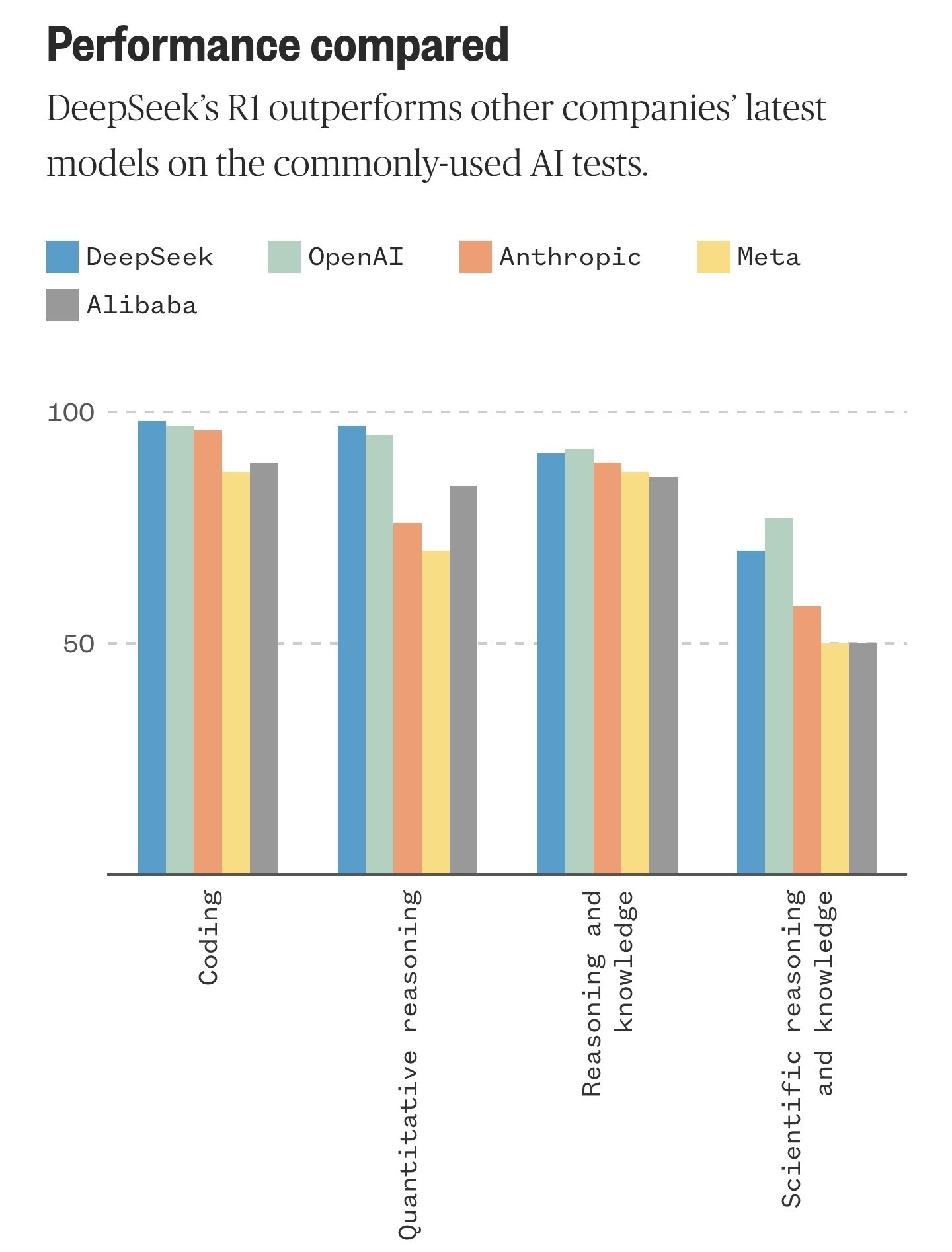

While China doesn’t want to enter a trade war, they are eager to win the AI race. After the launch of Deepseek, huge comparisons have been made between OpenAI’s ChatGPT and Deepseek models, which were built at a fraction of the cost.

We are entering into unchartered territory.

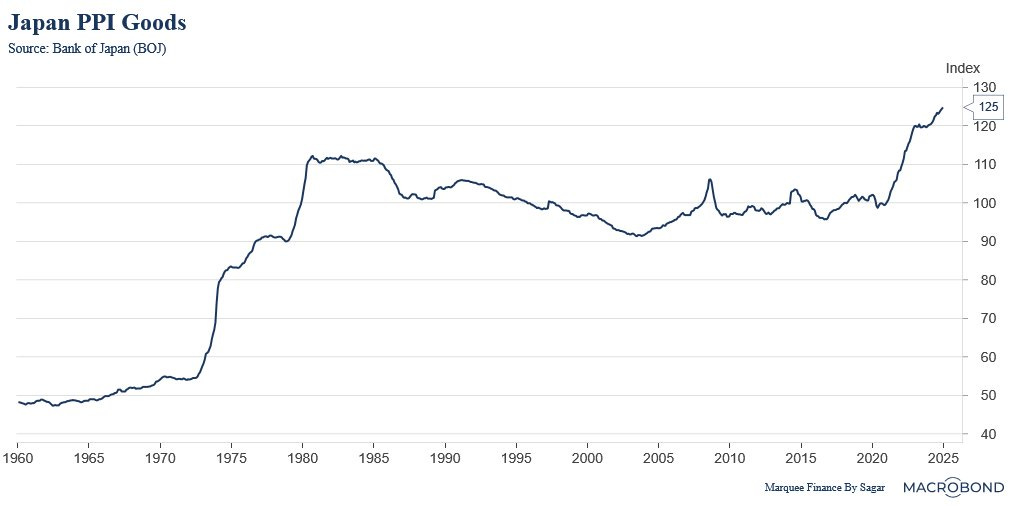

Chart: NBC

The last time the PPI Goods Index rose 25% was from 2003 to 2008 when oil prices spiked to $150 (and other commodities also rallied).

This time, the index is up 25% in only three years due to the decimation of JPY, and oil prices have been stagnant.

Is it safe to say Japan has exited deflation?

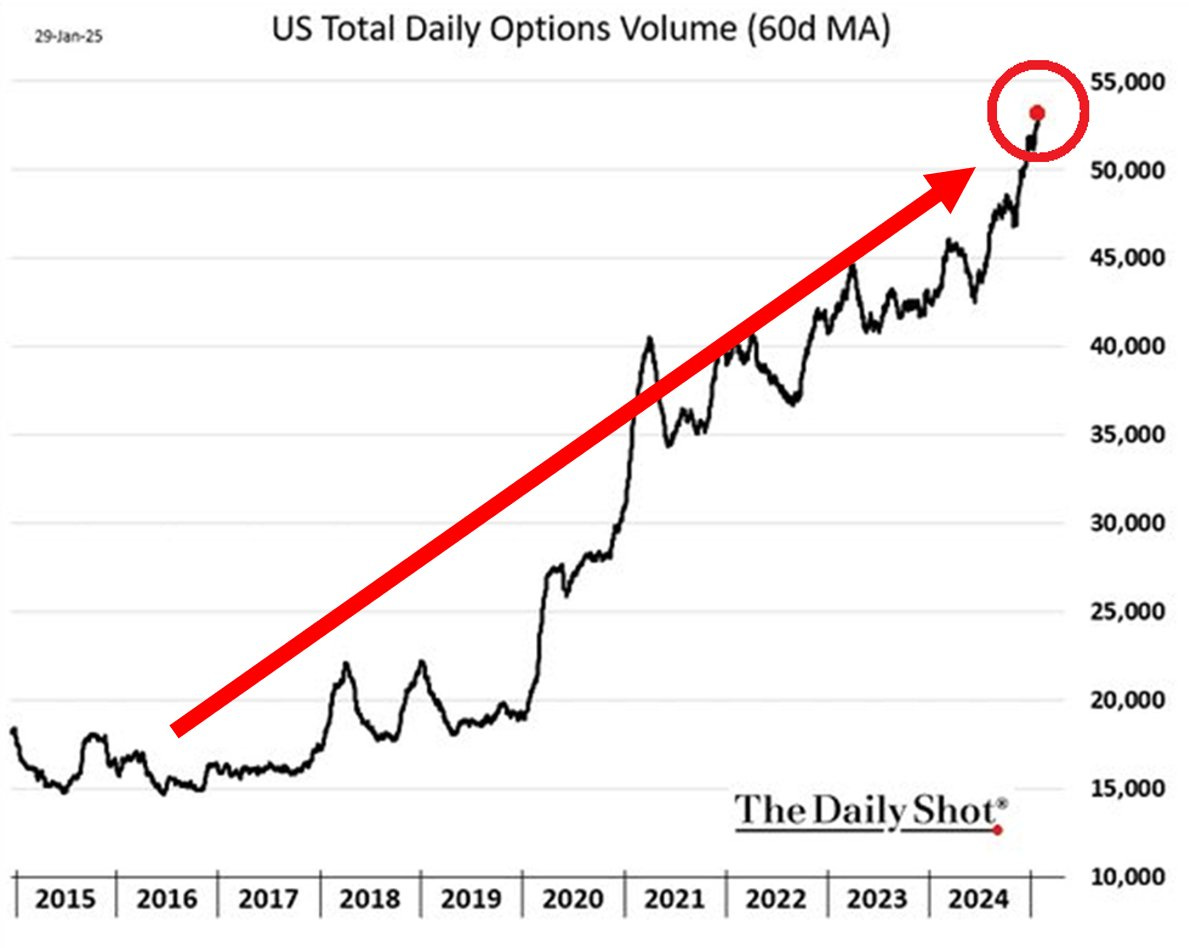

BONUS CHART: Options were introduced so that institutions could hedge their portfolios against extreme drawdowns and generate extra income for those with long-term portfolios. However, post-COVID, options have become a gambling’s den, especially with the launch of 0DTE options, as volumes have exploded.

Disclaimer

This publication and its author is not a licensed investment professional. The author & any other individuals associated with this newsletter are NOT registered as Securities broker-dealers or financial investment advisors with the U.S. Securities and Exchange Commission, Commodity Futures Trading Commission, or any other securities/regulatory authority. Nothing produced under Marquee Finance by Sagar should be construed as investment advice. Do your research and contact your certified financial planner or other dedicated professional before making investment decisions. Investments carry risk and may lose value; Marquee Finance By Sagar LLC, Marqueefinancebysagar.substack.com or Sagar Singh Setia is not responsible for loss of value; all investment decisions you make are yours alone.