July marked the “shift” in narrative from a recessionary outcome for the world’s largest economy to a “soft landing” ending.

Equity and credit markets continue to ride on the hopes of a “Goldilocks” scenario.

Let’s understand via charts what’s happening across assets all around the globe!

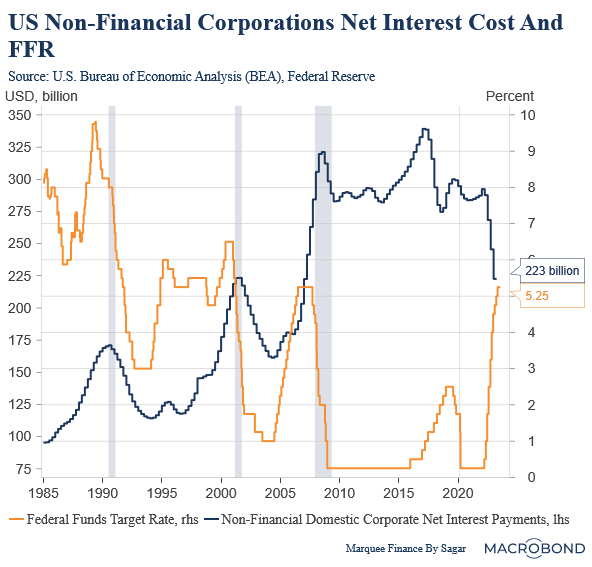

A much-anticipated recession never arrived in the US. While economists continue to scratch their heads for reasons, one of the most plausible reasons is that corporations benefit from lower interest rates (locking in for longer tenors) and earn handsome income from the highest levels of T-bills since 2001.

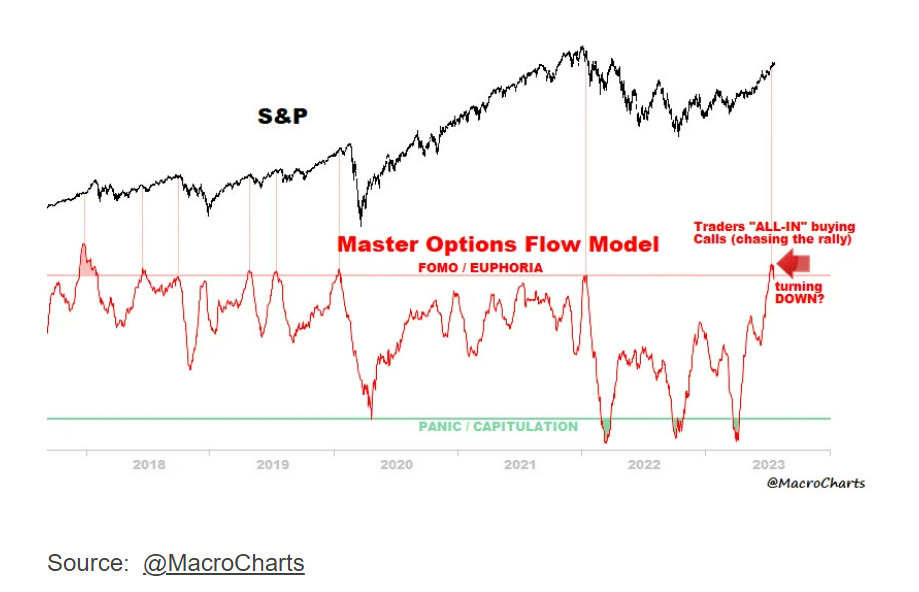

Source: Macrobond As the corporate balance sheet remains healthy and earnings surprise on the upside, equity markets remain buoyant, with traders rushing to chase the rally, indicating no signs of stopping as momentum remains strong.

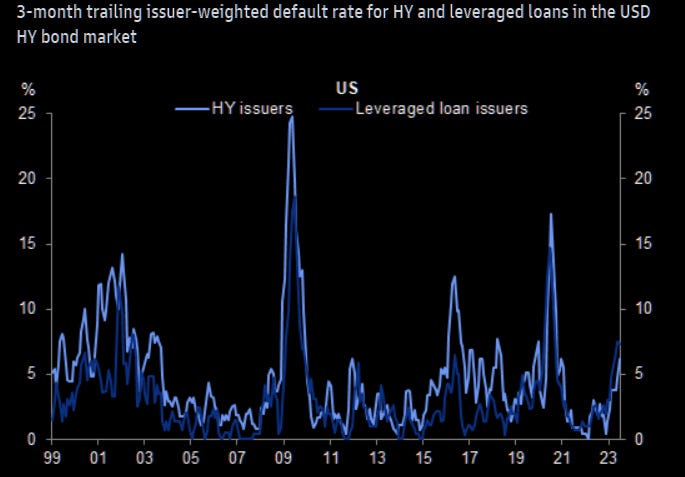

Source: Macrocharts While the sovereign bond markets remain rangebound, HY and IG spreads remain tightest since the covid flare up. However, some of the weakest companies feel the heat of higher rates as defaults have started to jump.

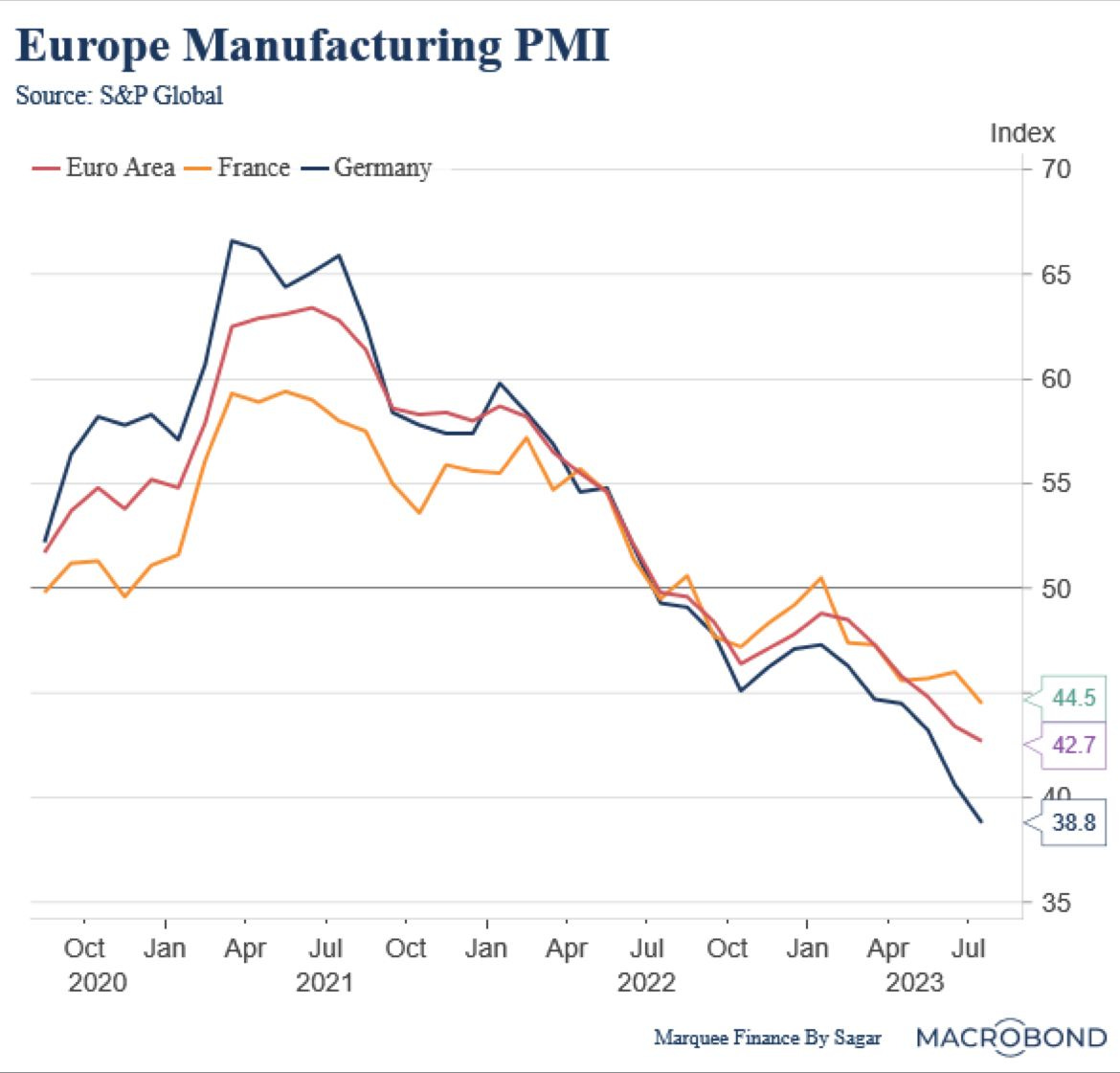

Source: Goldman Sachs The US data is surprising on the upside, but the European data is deteriorating and shocking the market participants. The growth collapse is now visible all across Europe, led by the manufacturing giant Germany.

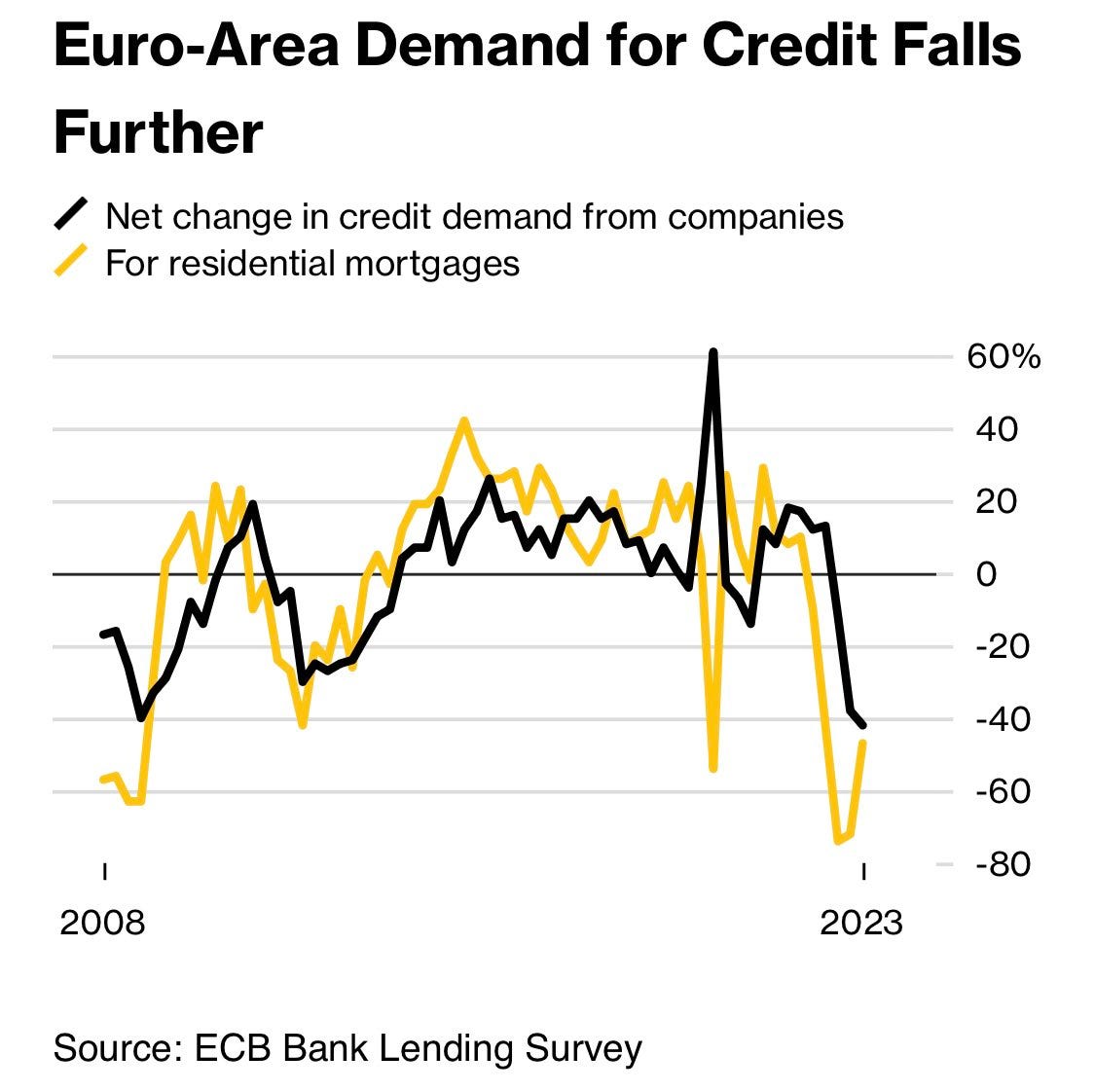

As the growth weakens, the credit demand has collapsed as higher mortgage rates take a toll on consumers and industries.

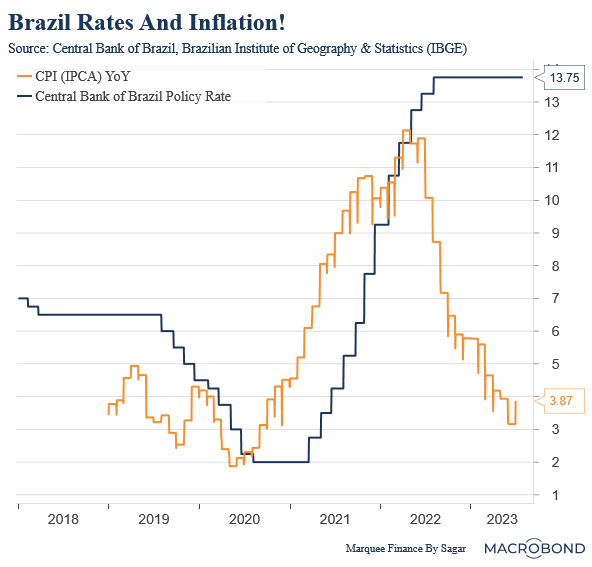

While the major CBs worldwide reach the end of the monetary policy tightening, Brazil will likely become the first country to cut rates which are “highly” in the restrictive territory.

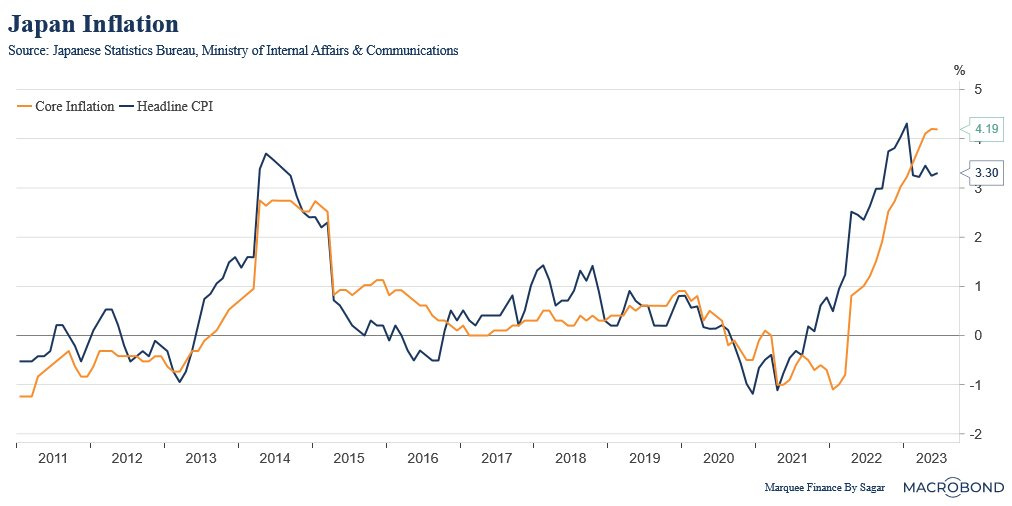

In the East, the “contrarian” central bank surprised the markets by widening the YCC band to 1% as inflation remains stubbornly high and way above the target.

The result of the mild “hawkishness” by the BoJ was the carnage in the JGB markets as yields across the board responded with violent moves.

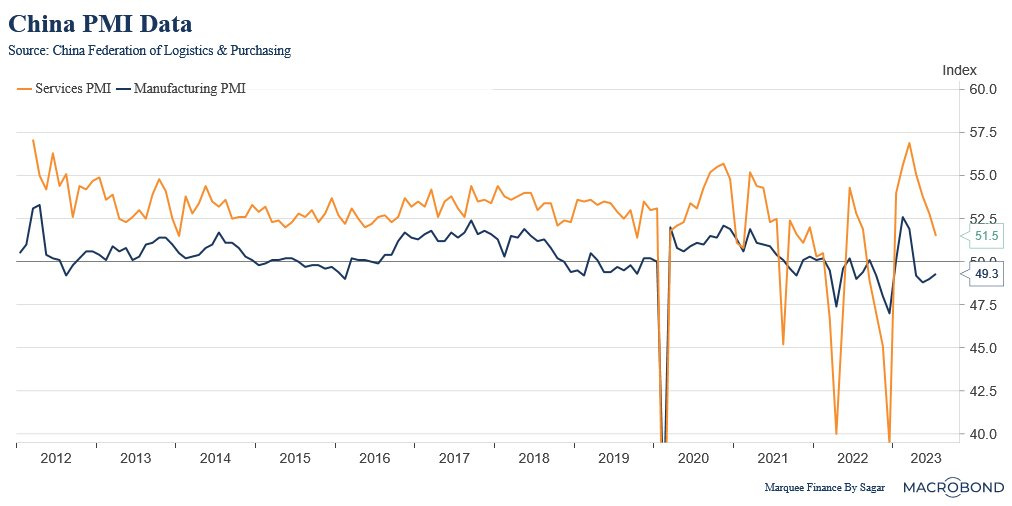

On the other hand, the only “large” economy faced with deflationary pressures remain China. Nevertheless, CCP has vowed to revive the economy and unleash gigantic fiscal stimulus.

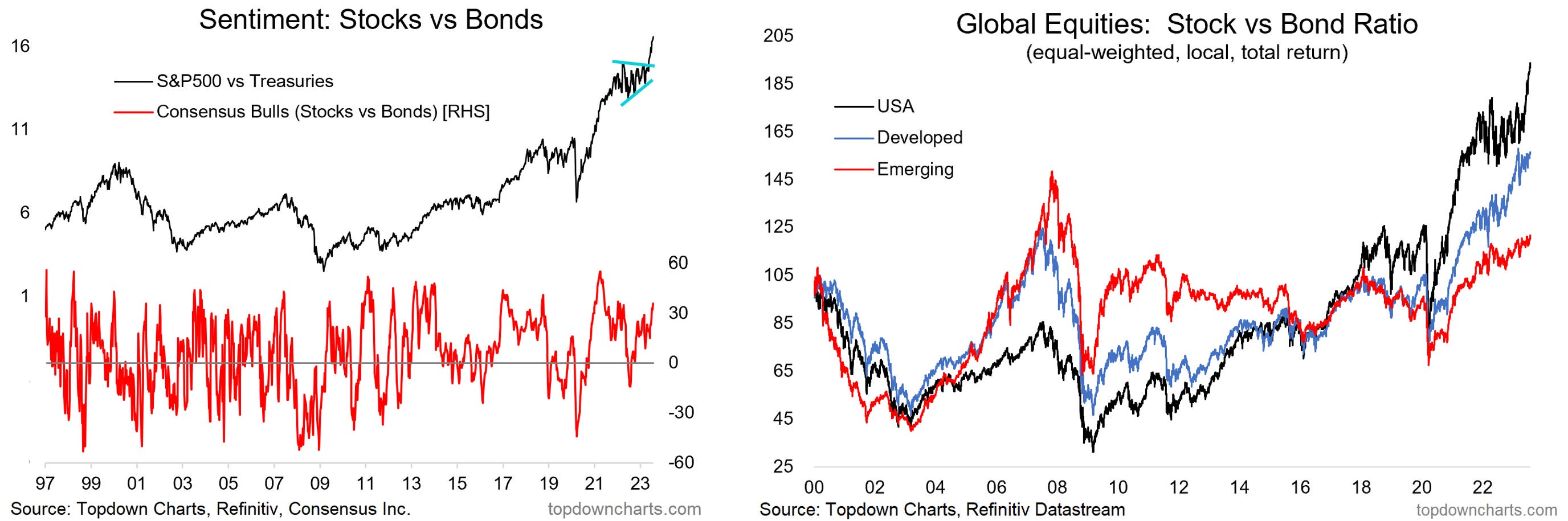

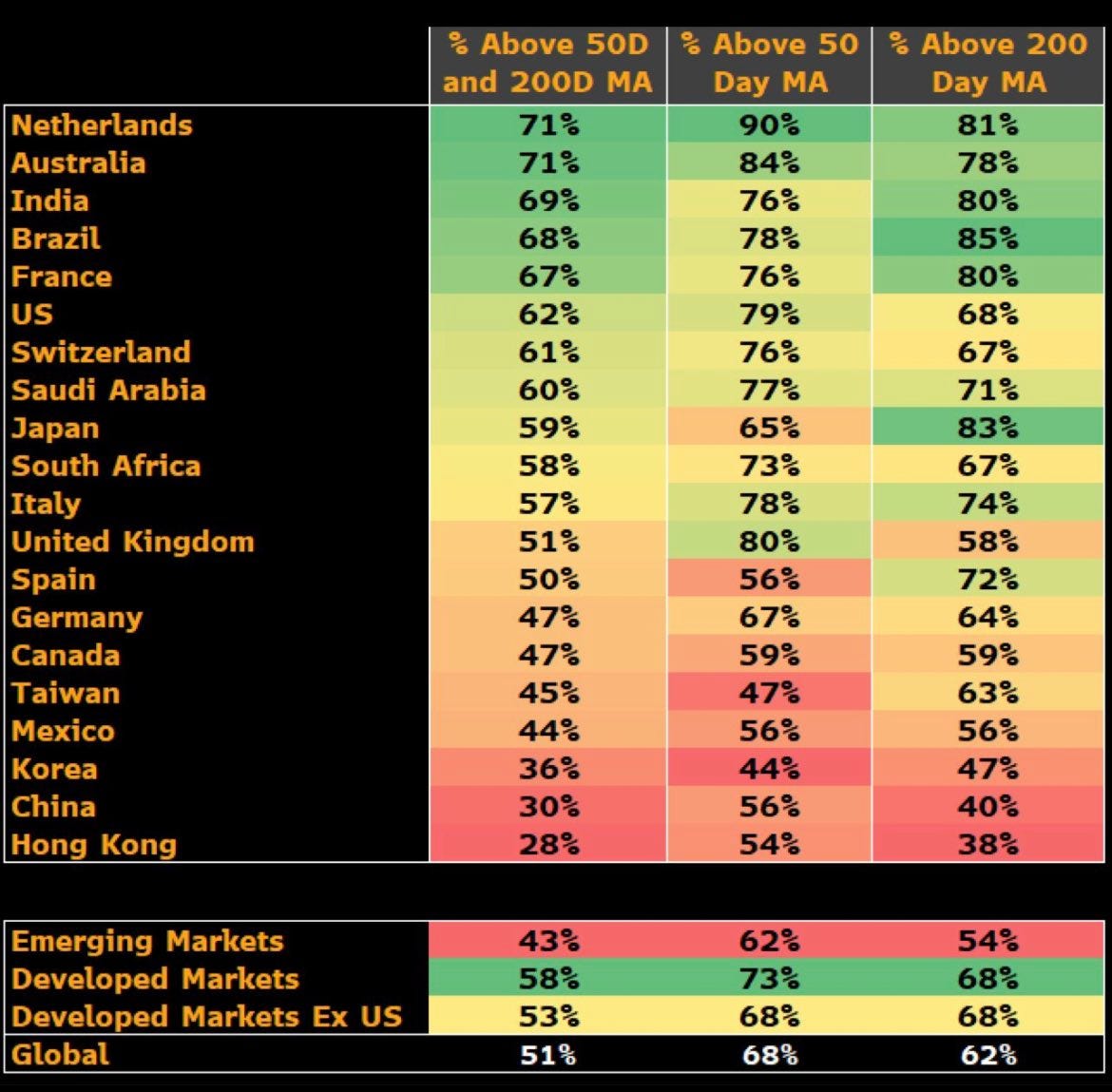

The surplus global liquidity means that stocks remain in a bull market, and sentiment is extremely bullish in favour of stocks compared to bonds.

Source: TopDown Charts Except for China and Korea, the major equity markets portray an extremely bullish picture.

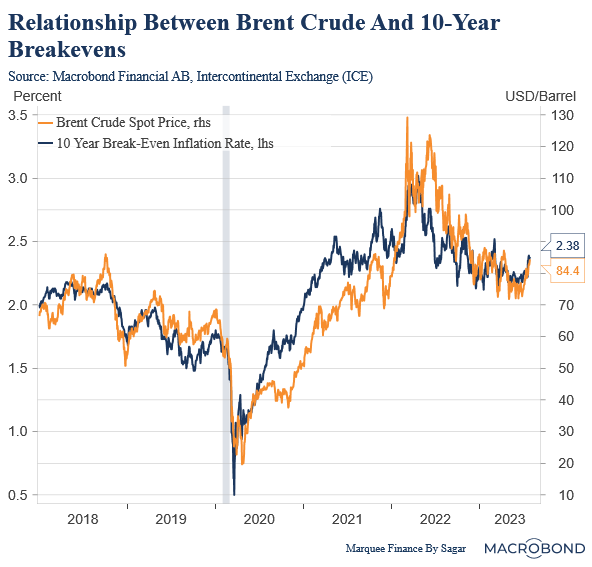

Source: Bloomberg The “Goldilocks” narrative and the Chinese stimulus measures led to a stealth rally in commodities, with Brent crude crossing $80/b and rising 26% from its bottom. Higher crude prices may lead to a second inflationary wave.

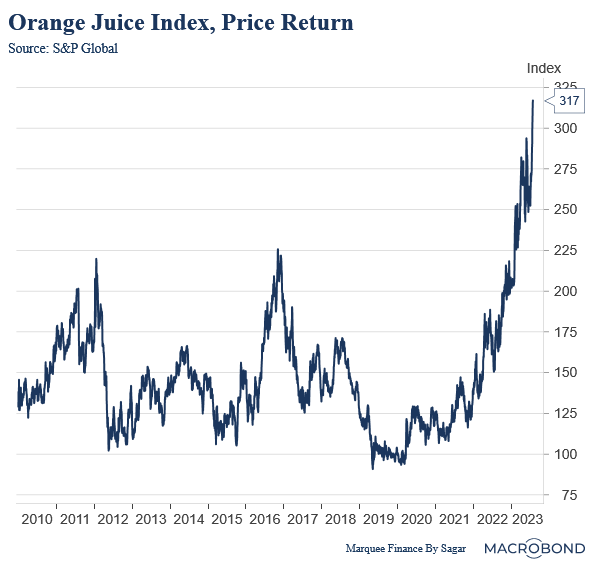

It’s not only crude; the whole commodity basket saw a one-way move up. Some commodities like “Orange Juice” and Cocoa have skyrocketed.

Disclaimer

This publication and its author is not a licensed investment professional. The author & any other individuals associated with this newsletter are NOT registered as Securities broker-dealers or financial investment advisors with the U.S. Securities and Exchange Commission, Commodity Futures Trading Commission, or any other securities/regulatory authority. Nothing produced under Marquee Finance by Sagar should be construed as investment advice. Do your own research and contact your certified financial planner or other dedicated professional before making investment decisions. Investments carry risk and may lose value; Marquee Finance By Sagar LLC, Marqueefinancebysagar.substack.com or Sagar Singh Setia is not responsible for loss of value; all investment decisions you make are yours alone.