Q12025 shocked every trader and investor, as the new US President made life miserable by flip-flopping every hour on significant policy decisions.

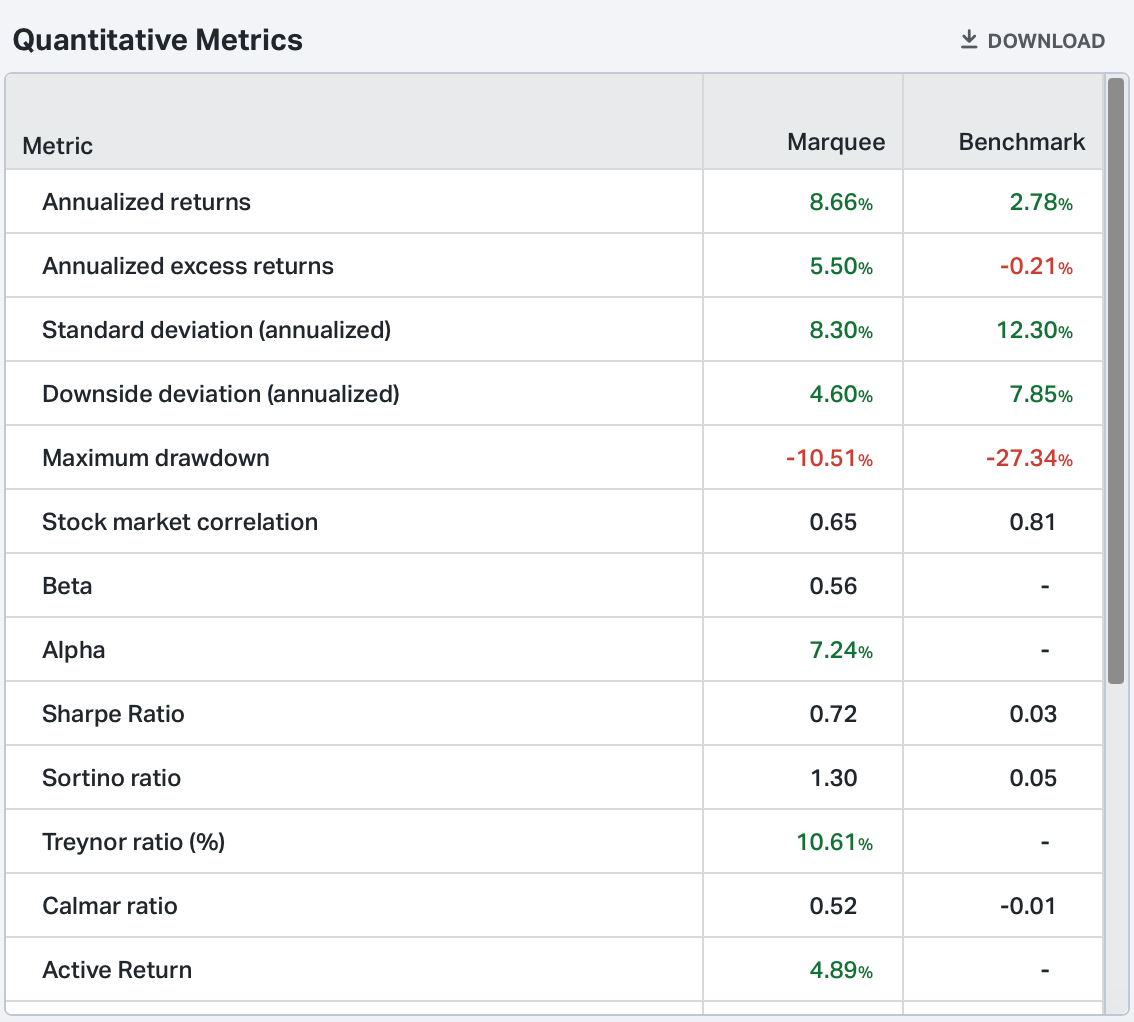

Nevertheless, we navigated through the turbulent times and successfully generated alpha.

Let’s understand what transpired in global financial markets in March with the help of 13 charts!

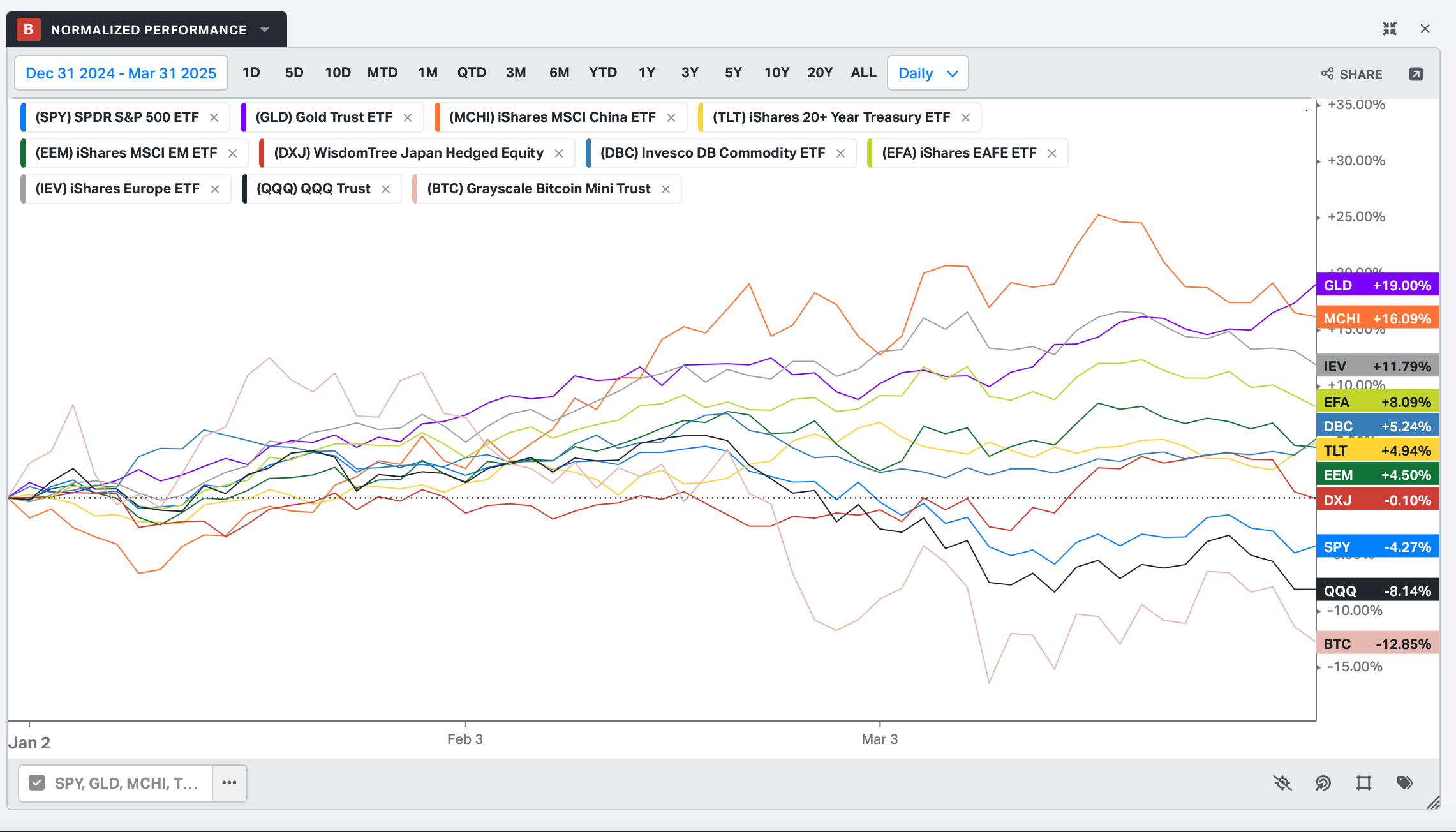

Q1 ended with a scenario that nobody in their wildest dreams had envisioned. Gold decimated all other asset classes with a mind-boggling 19% return (the highest Q1 return since 1986). China was one of the best-performing equity markets, with a stellar return of 16%. The rotation from super expensive US stocks led to a rise in European stocks, which reported a double-digit gain of 11.8% (IEV). The “shocking” disappointment was the QQQ and BTC, which lost 7% and -13%, respectively.

Nevertheless, after a long time, US Long Duration Bonds outperformed the US equities (a trend change or a one-quarter anomaly?)

Despite the dismal performance of the benchmark indices, some of the sectors generated significant positive returns with respect to the benchmark.

The defensive/value stocks outperformed the growth stocks by a wide margin. Lower oil prices failed to dethrone the energy stocks as they were the biggest sectorial gainers in the US in Q1. While consumer discretionary and tech stocks plunged by more than 11%, the utilities, staples and health care outperformed, indicating rotation into defensives.

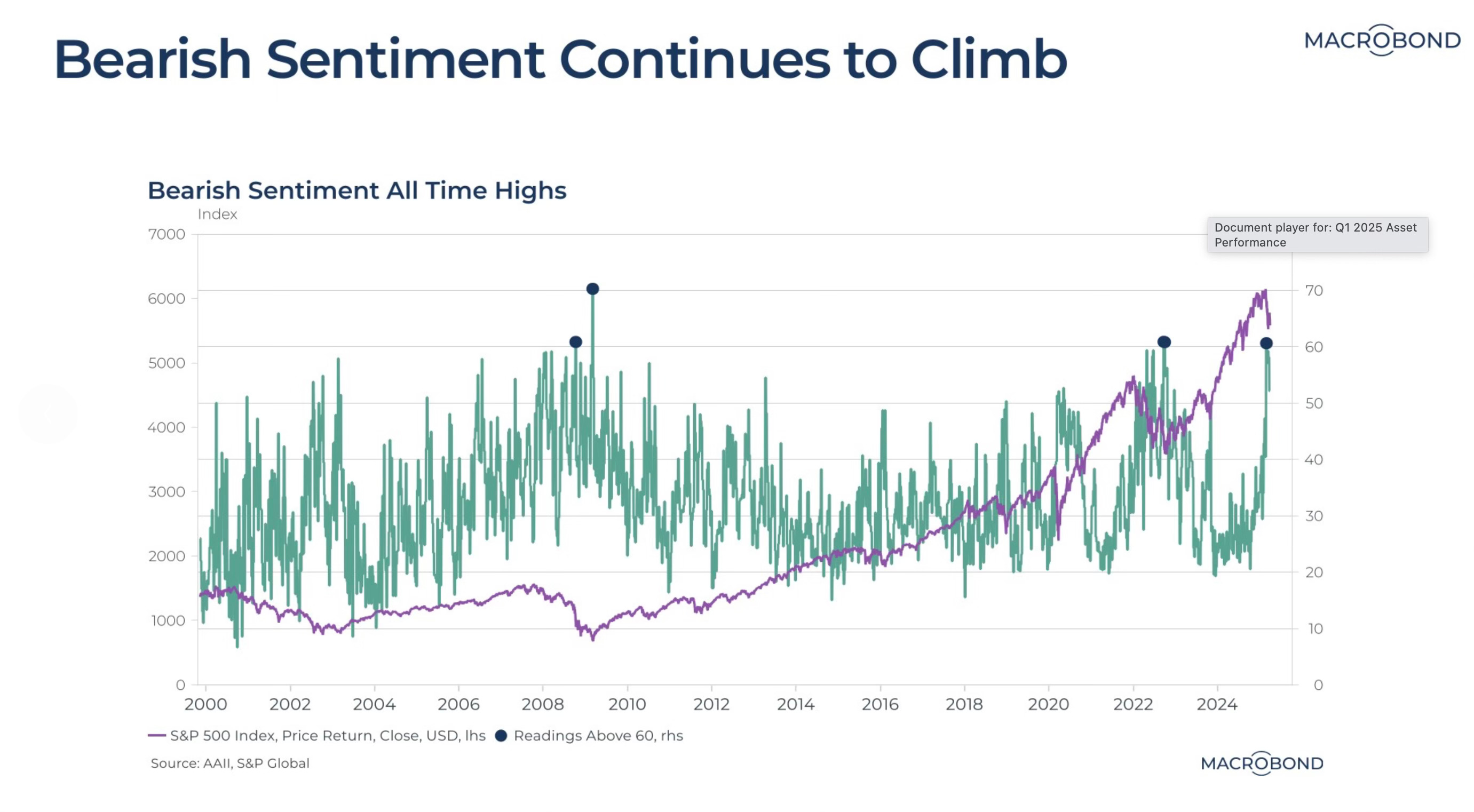

The bearish sentiment continues to climb as the S&P500 enters the correction territory with a drawdown of more than 10%.

The reading from the AAII survey has reached levels consistent with the 2022 bear market/ the GFC crash levels.

Traders focusing on short-term moves can’t ignore the sentiment along with positioning.

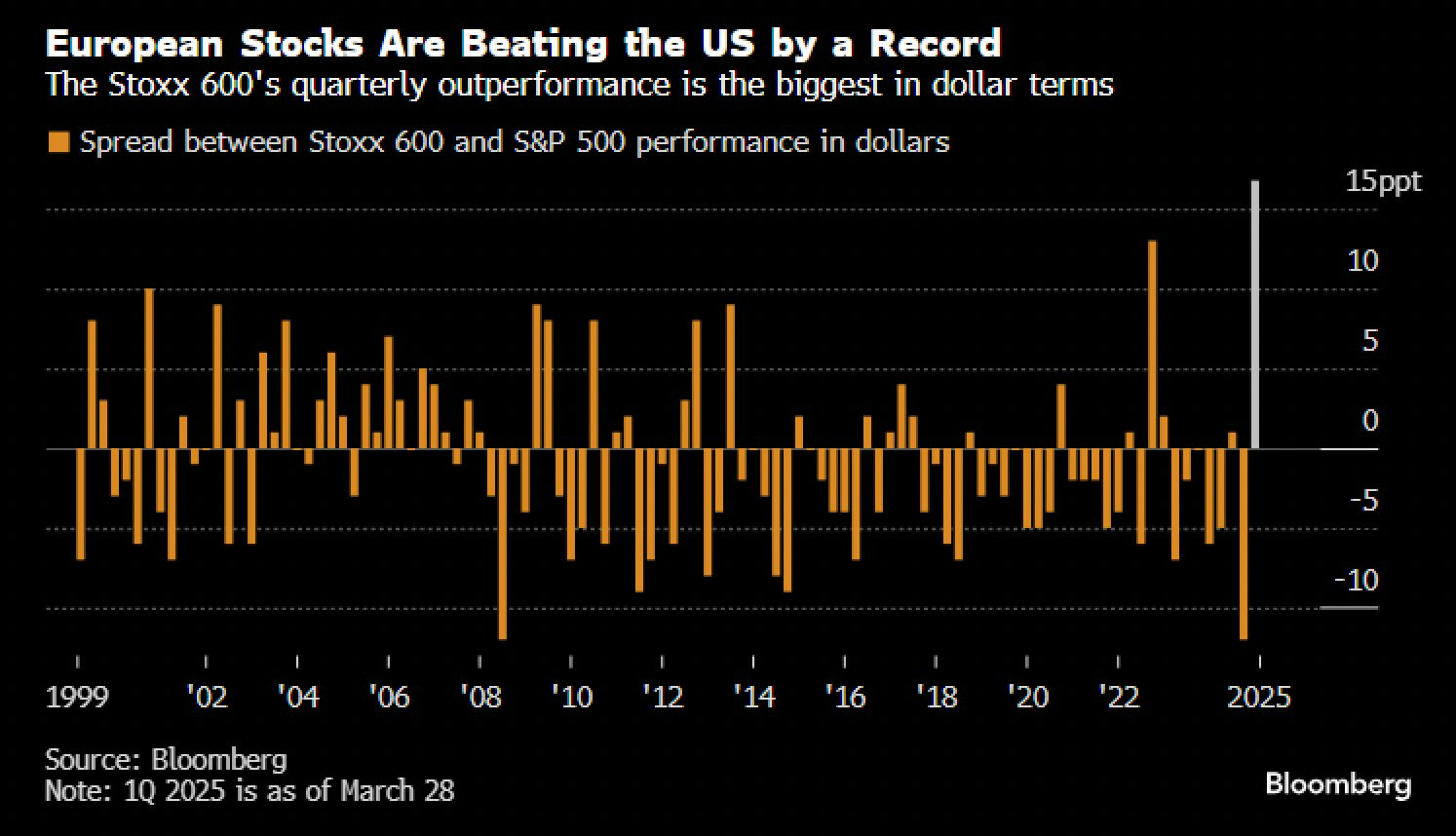

Moving on, Q1 was remarkable, and the equity universe's records were shattered.

The Stoxx 600 outperformed the S&P 500 by a record 14%, rewarding investors who were overweight European equities and underweight US stocks.

The reason the US stocks entered the “detox” period was the policies of the new administration.

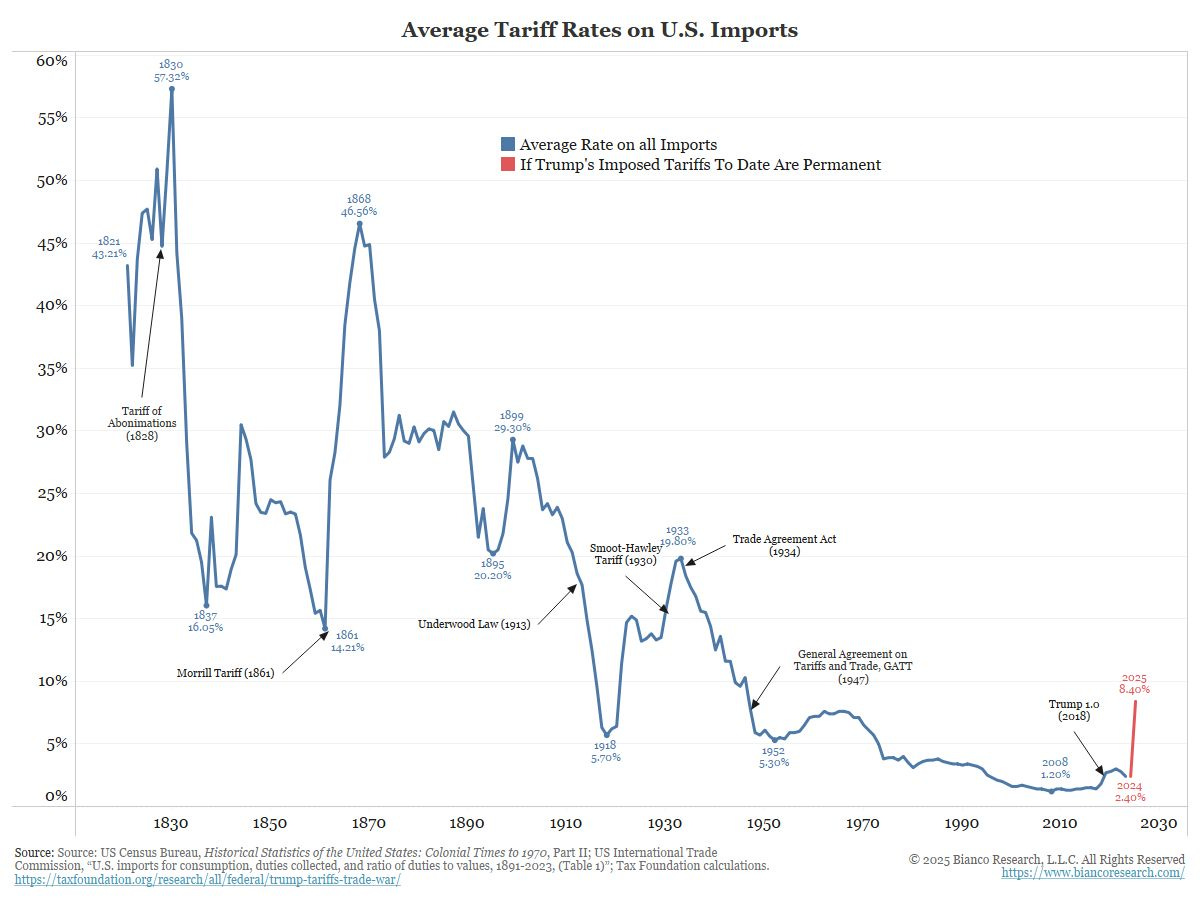

As we head into Liberation Day, universal tariffs are expected to be implemented immediately. Furthermore, if some countries are given relaxation, the reciprocal tariffs route will be taken as intense negotiations are underway.

Nonetheless, Liberation Day will likely lead to a rise in average tariff on all imports to > 8%+, which will be the highest since 1947!!

Source: Bianco Research

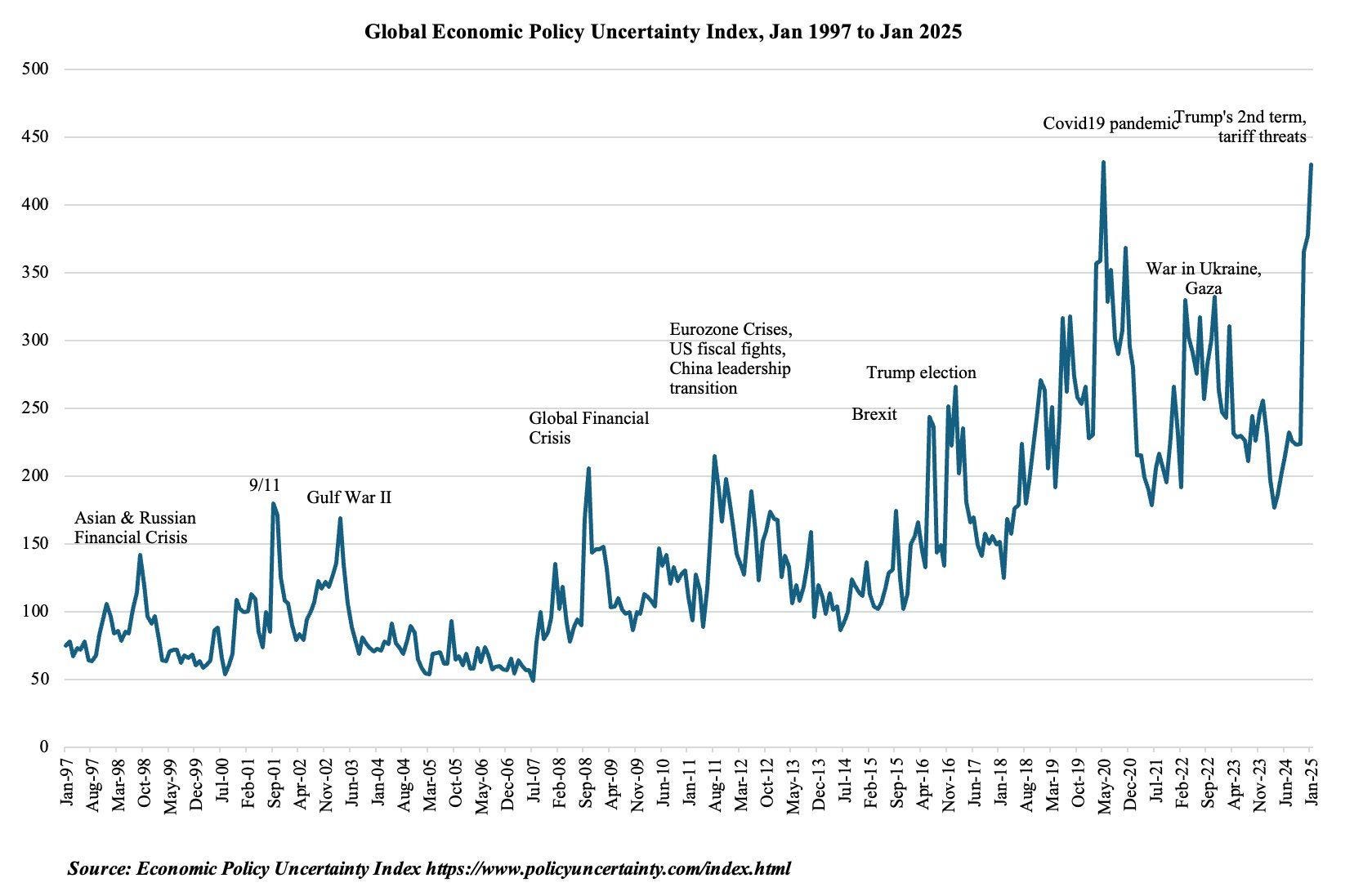

The highly elevated US Economic and Trade Uncertainty is now creeping across the world as fears of a “global” trade war mount.

As a result, the Global Economic Policy Uncertainty Index has surpassed the COVID-19 highs.

In fact, Central Bankers across the world (BoJ, BOE, ECB and Fed) in their meetings highlighted the rising volatility in the global financial markets due to the new US administration policies.

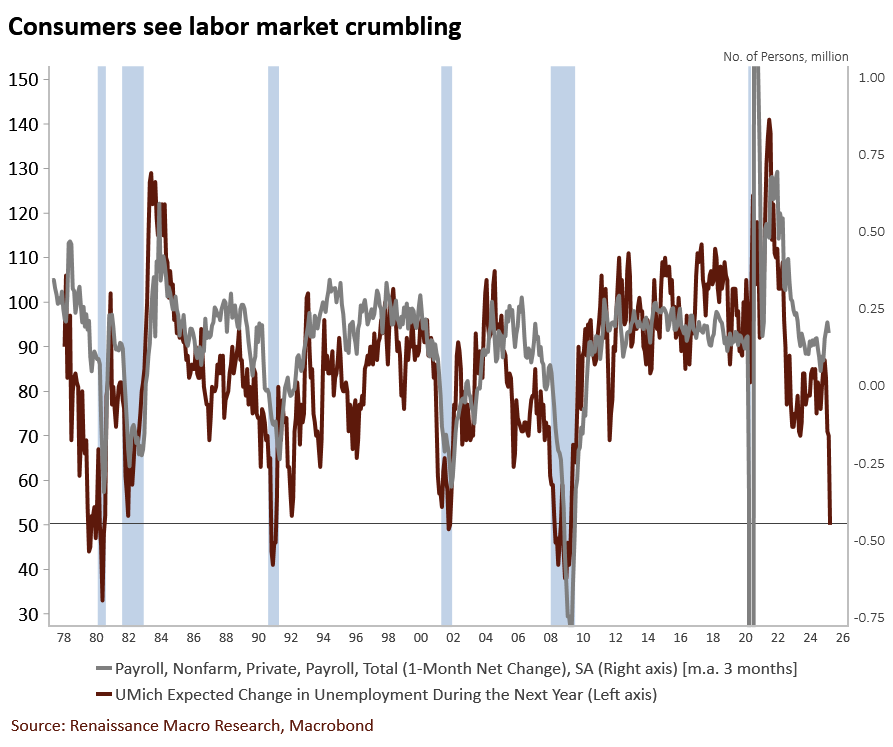

The labour market is crumbling beneath the surface as uncertainty looms on the policy front and the economy enters the “detox” period due to likely reduction in fiscal deficits and large federal layoffs.

The sentiment is turning sour as non-existent hiring coupled with slowly rising layoffs leads to pessimism in the economy.

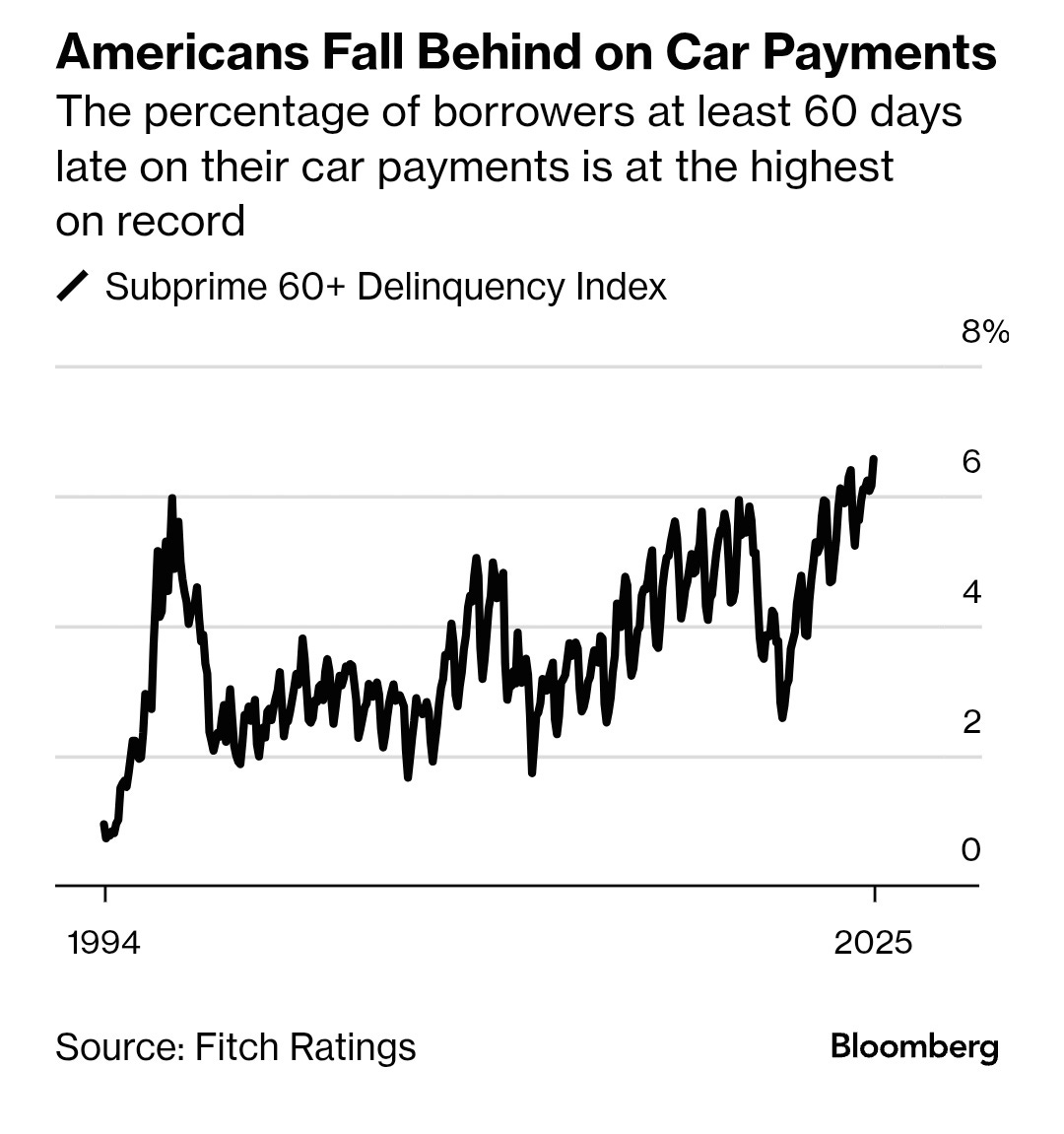

Source: Renmac As the labour market crumbles and the negative wealth effect due to the decline in the equity markets grips consumers, the delinquency rates have begun to rise, with the lowest-quality borrowers (subprime) faring the worst on record in paying their car payments on time.

The macro data indicates a scenario that we have been discussing for months. Growth is slowing down, the unemployment rate is ready to shoot higher, and the impact of tariffs will undoubtedly be inflationary in the short term.

The Federal Reserve confirmed the stagflationary conditions when they presented their dot plots in the March FOMC.

Source: US FED

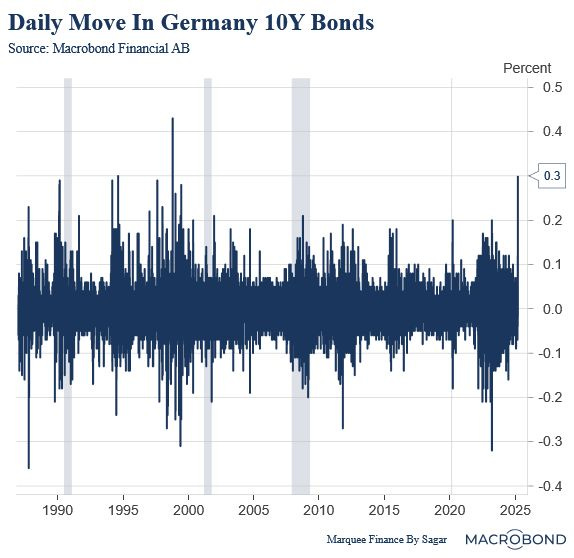

European bond yields had one of the biggest moves in March as Europe announced the upgrade of its shaky infrastructure and spend hundreds of billions of dollars on defence (arms)purchases as the US prepares to leave NATO.

German Bunds saw a move of more than 30 bps in a single day (a 4 SD move), a historic one as it's the largest move in over 3 decades.

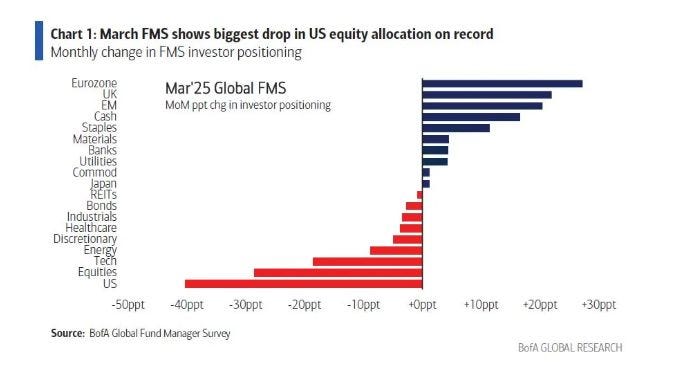

Thanks to the announcements, massive amounts of money moved into European equities, and investors’ positioning rose by more than 30% as fund managers rushed to sell the US equities.

Nonetheless, the rally has cooled off over the last few days as valuations rose and the markets became extrmely overbought.

The Chinese equity markets have ripped since January 20th. However, everybody has been asking whether the Chinese economy has bottomed out.

Our first chart today indicates that the Chinese Consumer Confidence Index has bottomed out with a nascent recovery visible.

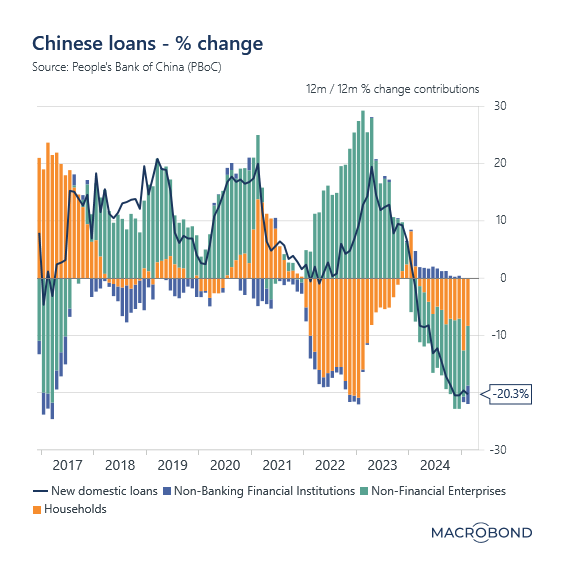

Nevertheless, the second chart demonstrates that despite the lowest rates on record, every institution and household is now deleveraging, indicating no respite in the balance sheet recession.

Even non-banking financial institutions deleveraged in Feb with a negative YoY print for the first time since 2022.

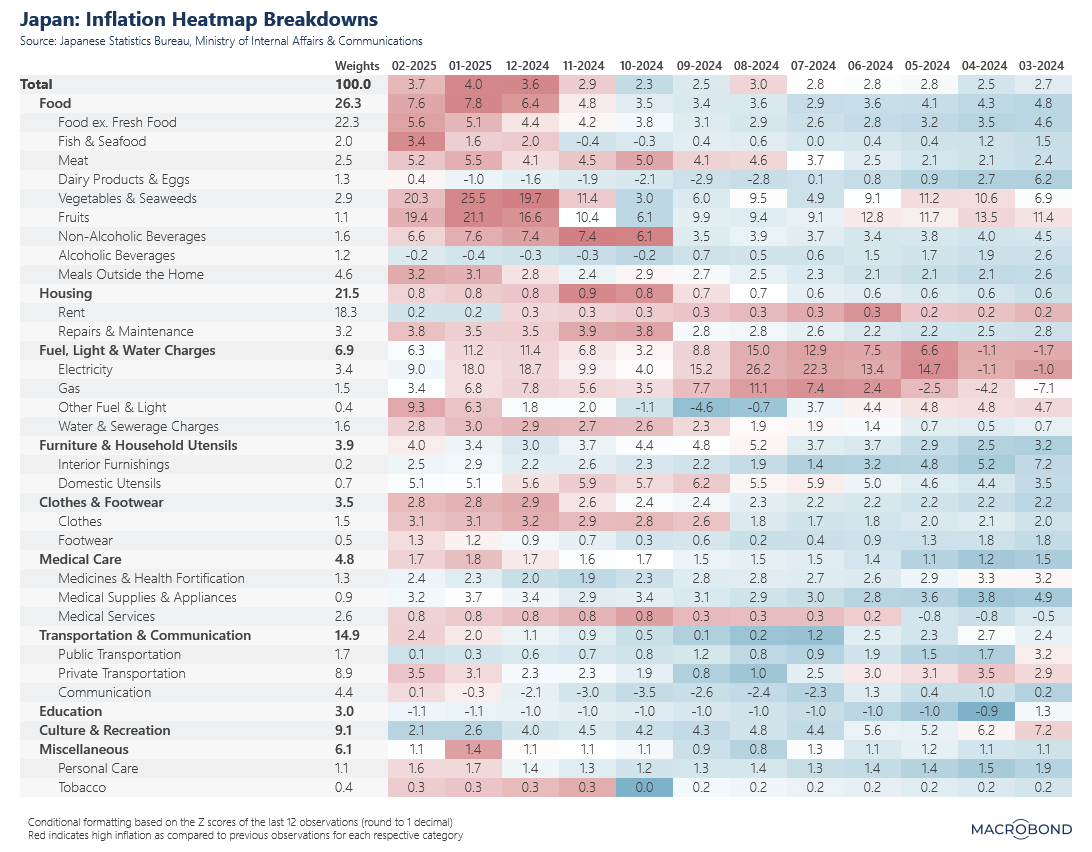

In the land of the rising sun, wage increases (measured by Shunto talks) are transpiring at the highest pace in decades as the cost of living witnesses an unprecedented rise.

The Feb CPI breakup suggests that inflation is broad-based and turning out to be sticky.

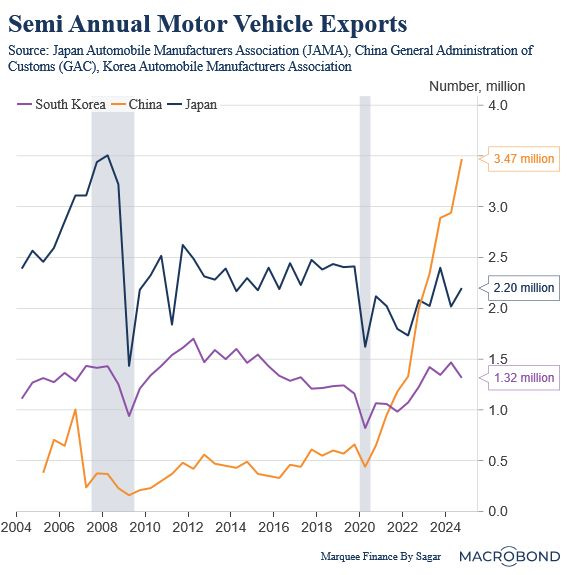

BONUS CHART: The 25% auto tariff imposition will immensely benefit the Chinese OEMs, gaining market share from their German, Korean, and Japanese peers.

Japanese, German, and Korean OEMs will raise prices, probably leading to a fierce price war with Chinese OEMs.

As the EV revolution storms the world, the Chinese have already overtaken the world's auto market thanks to unprecedented innovation and unmatched price advantage.

Disclaimer

This publication and its author is not a licensed investment professional. The author & any other individuals associated with this newsletter are NOT registered as Securities broker-dealers or financial investment advisors with the U.S. Securities and Exchange Commission, Commodity Futures Trading Commission, or any other securities/regulatory authority. Nothing produced under Marquee Finance by Sagar should be construed as investment advice. Do your research and contact your certified financial planner or other dedicated professional before making investment decisions. Investments carry risk and may lose value; Marquee Finance By Sagar LLC, Marqueefinancebysagar.substack.com or Sagar Singh Setia is not responsible for loss of value; all investment decisions you make are yours alone.