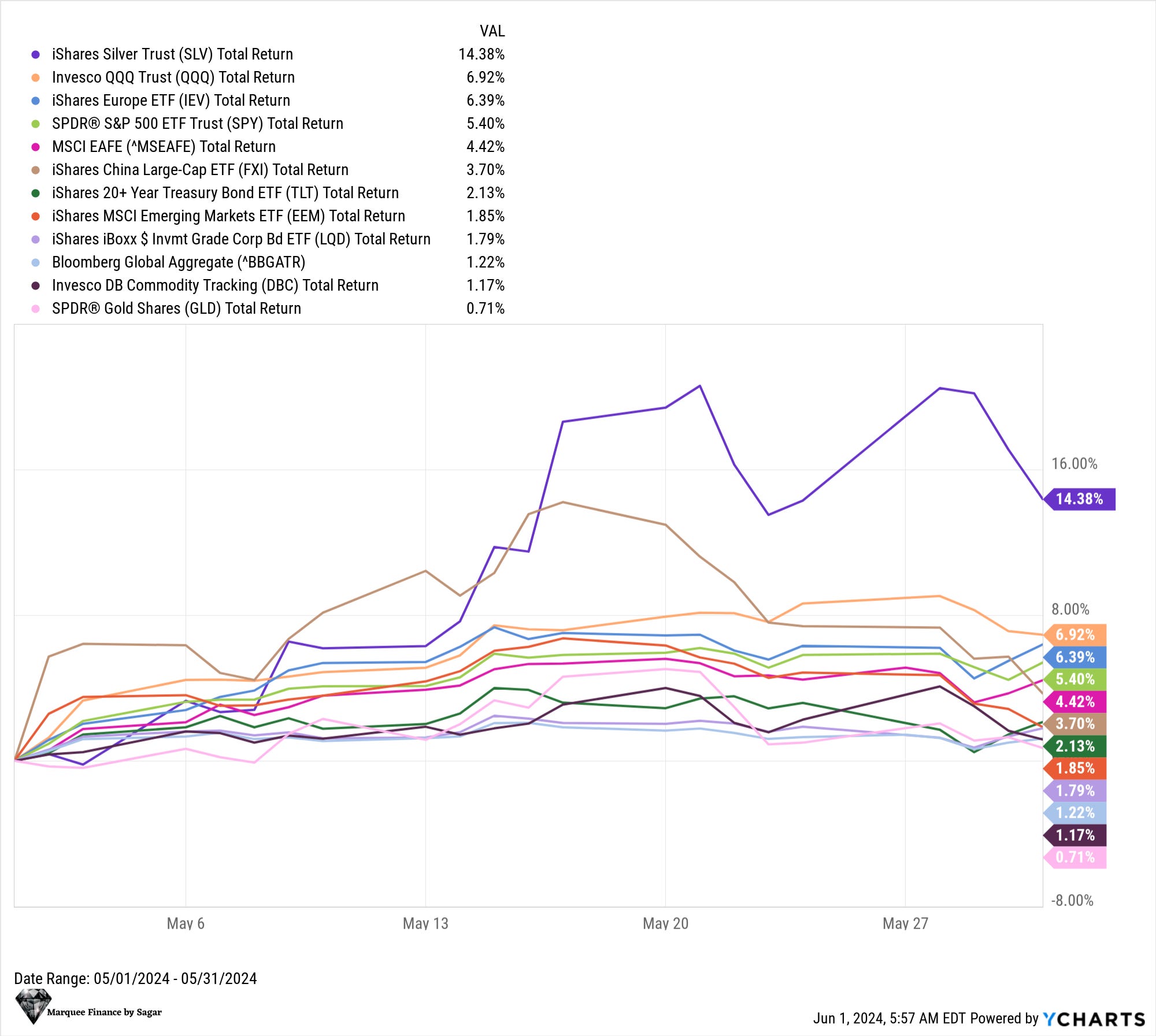

The famous adage, “Sell In May and Go Away,” didn’t work this year as all the asset classes gave positive returns in the last month.

In fact, Silver was the best-performing asset, outperforming Gold by one of the most considerable margins, leading to a collapse in the Gold/Silver ratio.

Furthermore, after a very long time, Long-Term US Bonds outperformed Gold last month, and as a result, the GLD/TLT ratio also fell.

Let us look at the macro events that transpired last month and decipher the cross-asset performance.

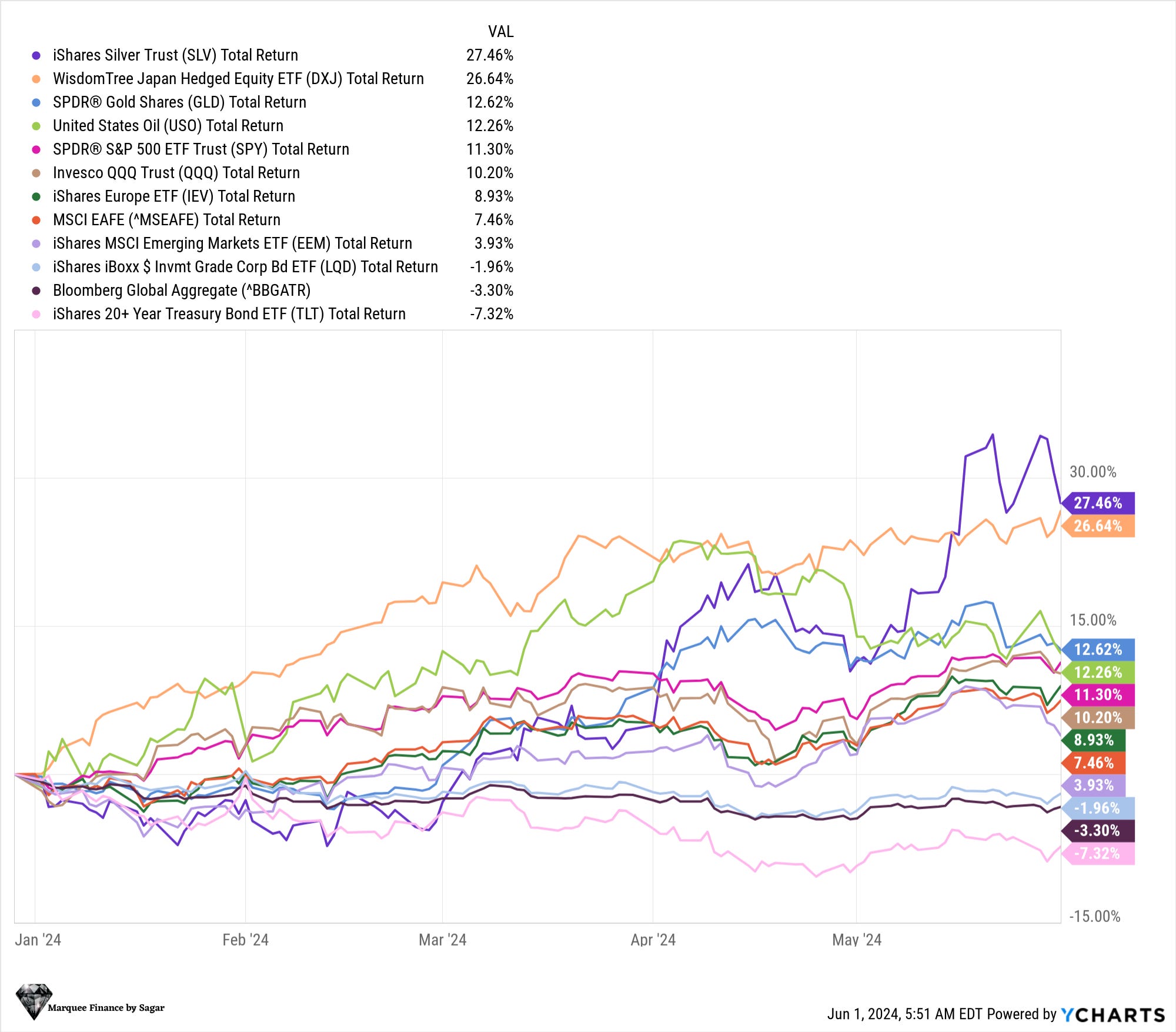

Thanks to inflation reaccelerating and investors' underweight positioning at the beginning of the year, Silver, Gold, and other commodities such as Copper and Oil are the top-performing assets YTD, beating equities and bonds.

Coming to equities, the US has outperformed RoW (ex-Japan), led by NVDA, responsible for one-third of the total S&P 500 returns YTD.

On the contrary, bonds continued their worst rout, with long-duration bonds being the worst performers.

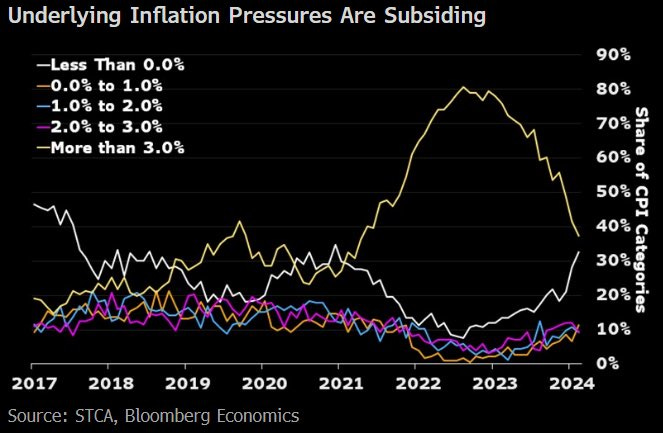

While the first few months were marked by a resurgence in inflation, the data in the latest CPI reading has been encouraging.

The underlying inflation pressures are subsiding as the share of CPI categories with more than a 3% gain has been rolling over rather swiftly. On the other hand, shares with less than a 0% gain have been picking up.

Source: BBG Economics

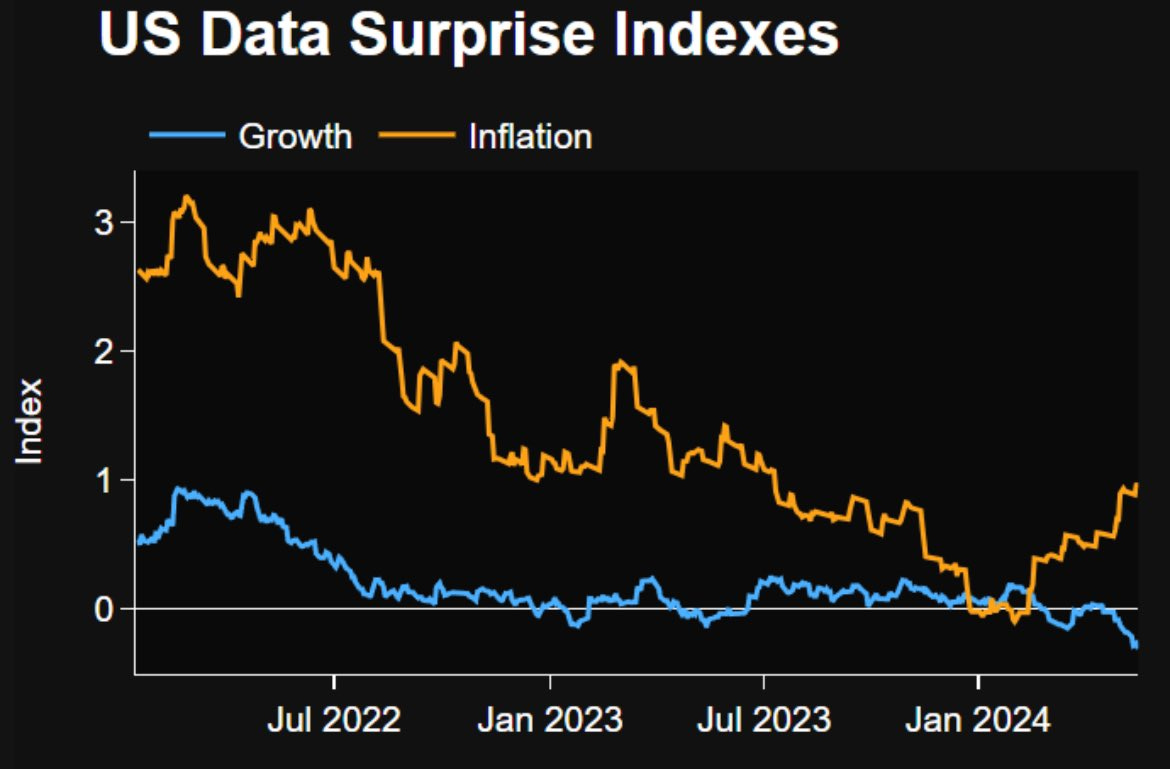

Though the inflation internals are slowly mean-reverting, the inflation surprises are trending higher as the data beat the estimates.

On the other hand, growth has been disappointing, raising stagflation concerns in the world’s largest economy.

Higher liquidity and a demand-supply mismatch have led to an All-Time High (ATH) in home prices as measured by the CASE Shiller Index.

High prices coupled with multi-decadal high mortgage rates have led to a massive plunge in affordability, which has frozen the housing markets for new buyers.

Market participants have been citing loose financial conditions as one reason to justify the “higher for longer” narrative.

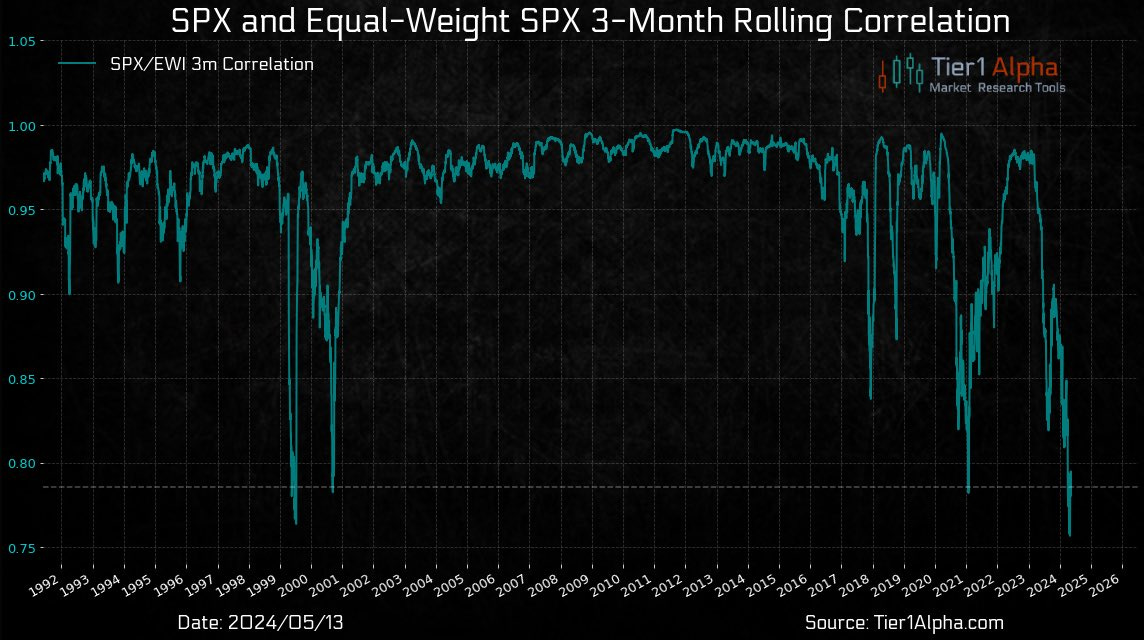

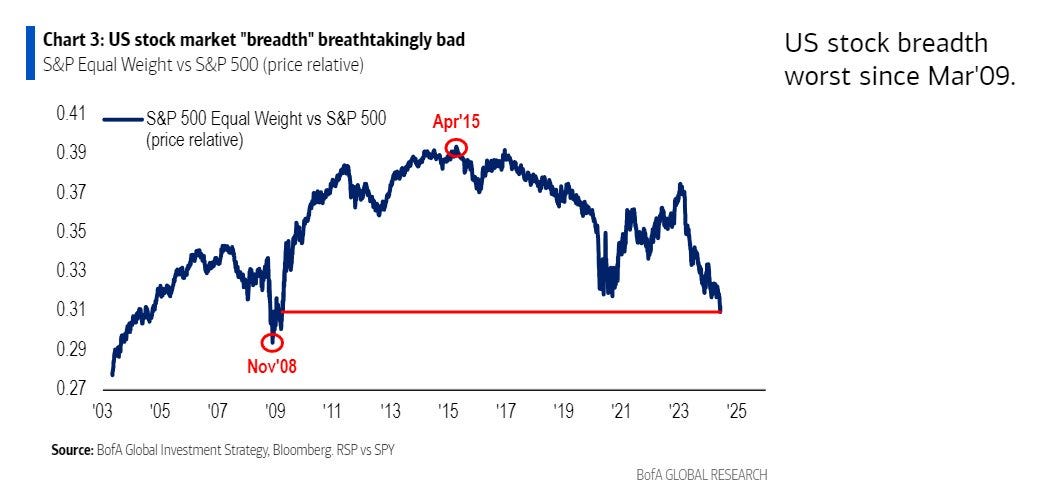

Nonetheless, market internals are broken as higher interest rates have led to the earnings decline of the SPX 497. The resilient Mag 7 has led to one of the most precarious instances in the history of SPX V/S Equal Weighted SPX.

We have been mentioning the concentration risk of Mag 7 as the largest tech companies in the world are becoming too large, leading to distortion in the index.

In fact, the market's breadth has been in free fall since the enormous rally began in October 2022.

Nothing can stop retail investors from gambling as the loose financial conditions lead to insane moves in meme stocks.

The last eight months' rally has been driven by the retail flows, which have now touched the highest level on record. Note that the leveraged ETFs now garner a lot of the flows.

European equities continue to catch up with their US peers as the economic recovery unfolds swiftly in Europe. We can safely conclude that the cyclical sectors have bottomed in Europe.

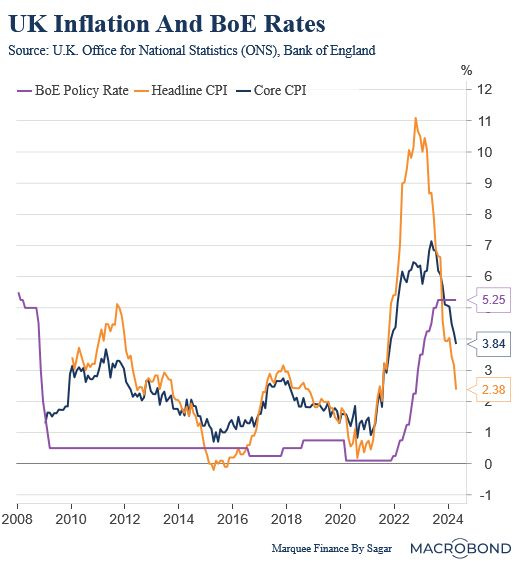

The UK was the worst hit post the Russian invasion of Ukraine as energy costs spiralled out of control and inflation reached double digits.

Though the headline inflation has plunged to 2.4% in the UK, it is proving stickier than most market participants anticipated.

As rates turn restrictive, markets now price the first cut by the BOE in September.

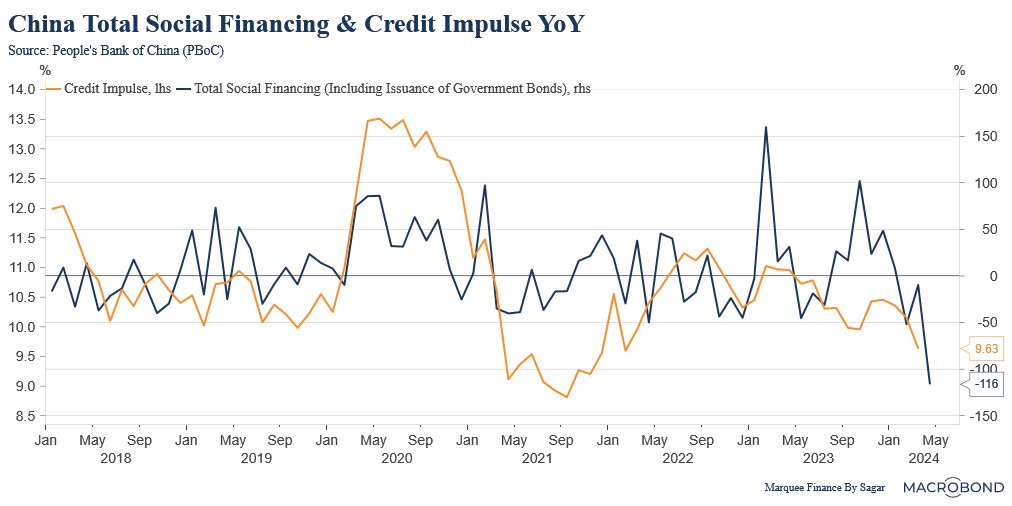

China was again in the news for the wrong reasons on the macro front.

The Total Social Financing (TSF), one of the most tracked macro gauges, turned negative YoY for the first time ever. The horrendous data release led to the Chinese Government resorting to massive stimulus.

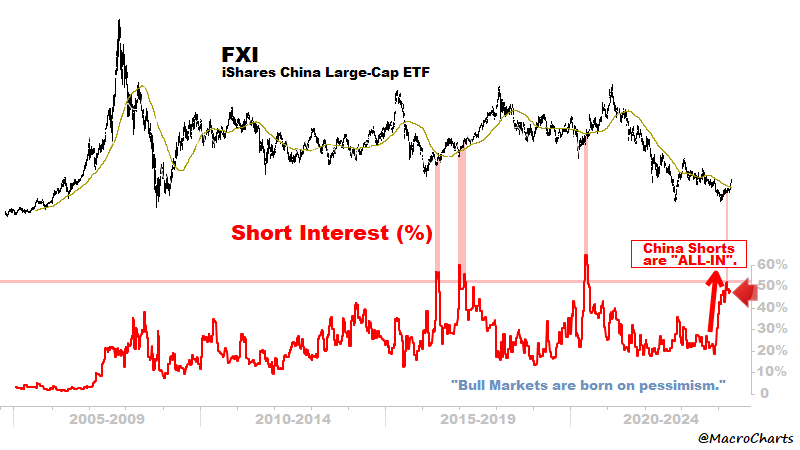

As extreme pessimism flowed from the Chinese macro data, the equity markets witnessed mammoth short covering.

As a result, Chinese equity markets were an outlier in May and recovered sharply from the bottom.

Source: Macrocharts

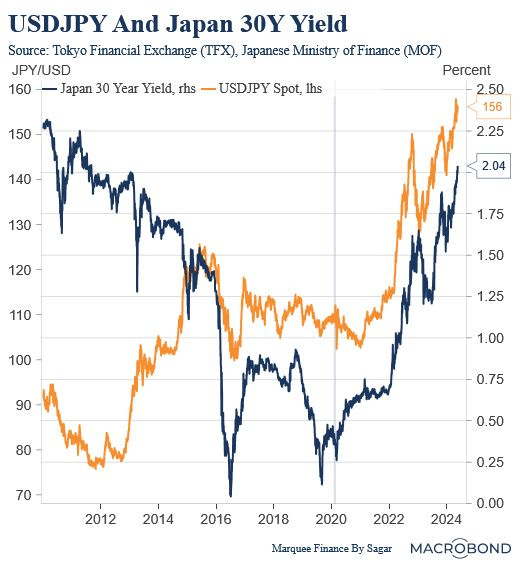

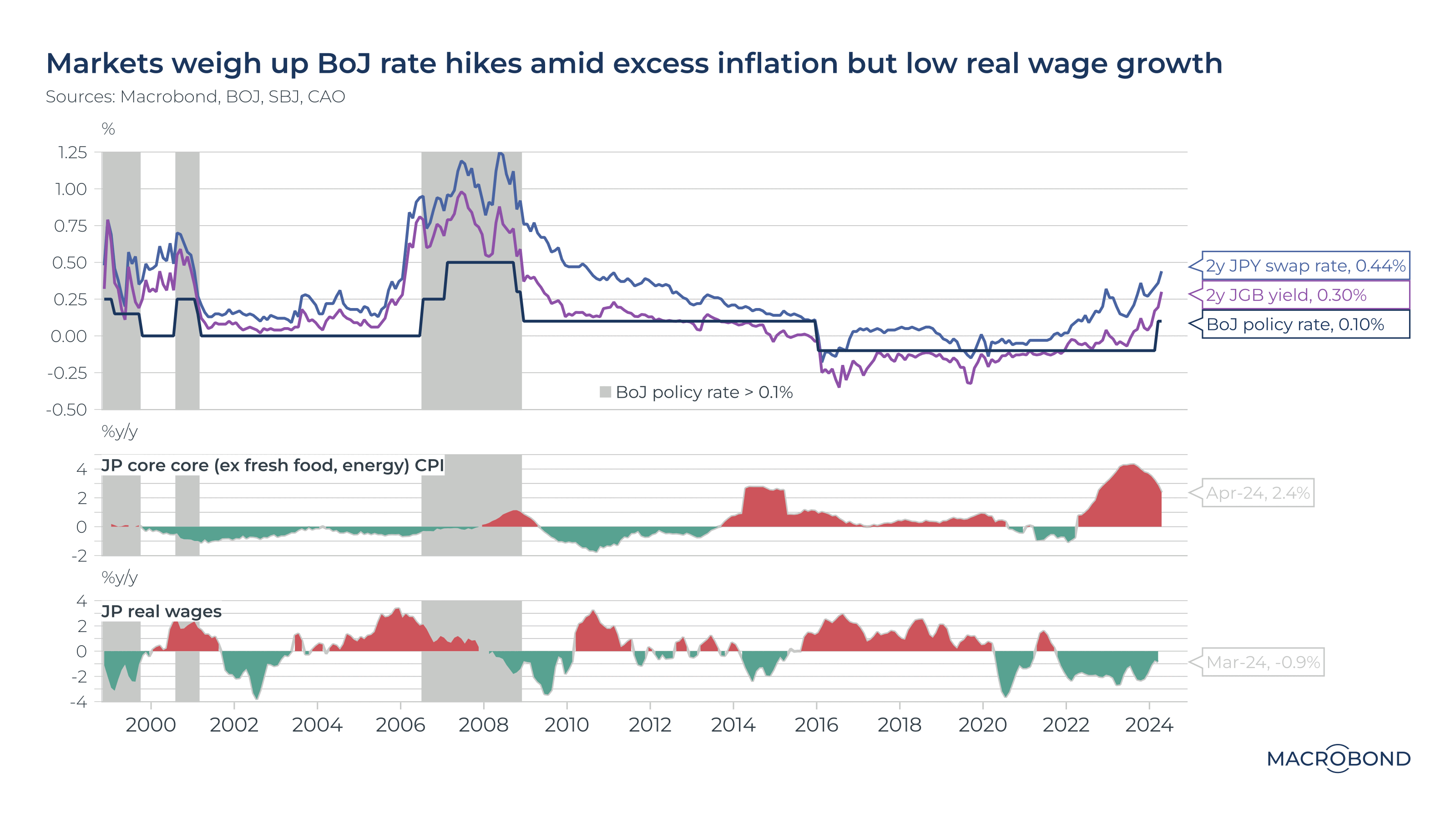

The Japanese 30Y Yield just crossed 2% (the 10Y is comfortably above 1%) and is now at the highest level since 2011.

On the other hand, USDJPY, even after softer CPI, weaker NFP data, and a $62 billion intervention, is still hovering around 156.5.

As a result, the BOJ has no choice but to hike rates aggressively, which will have grave consequences for the global financial system.

Japanese bond markets are already pricing in a July rate hike, with the 2Y swap rate jumping sharply.

The reversal of carry trades will be on everybody’s radar if the other CBs cut rates while the BOJ hikes.

A once-in-a-lifetime event occurred in the commodities market last month as Copper underwent a massive short squeeze.

A massive dislocation between the copper prices traded in New York (Comex) and the London Metal Exchange (LME) rocked the global market for the metal and prompted a frantic dash for supplies to ship to the US.

Source: BBG

Not only Copper but commodity prices all across the board have given double-digit returns this year as geopolitical concerns, sanctions, trade war, Chinese mysterious buying, and AI Capex have been fueling speculation about shortages.

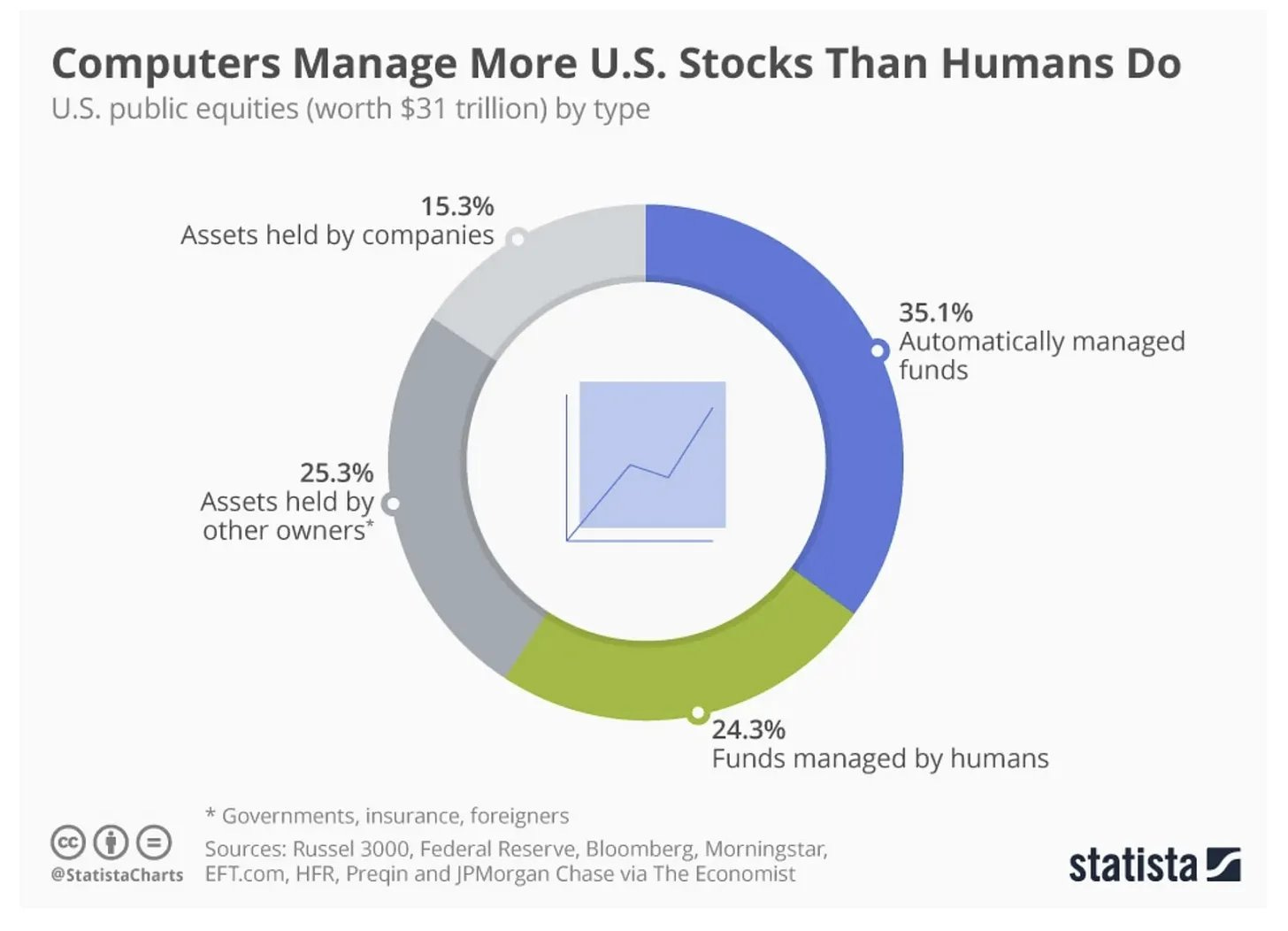

BONUS CHART: One should not be surprised that computers manage more US Stocks than humans do!

Disclaimer

This publication and its author is not a licensed investment professional. The author & any other individuals associated with this newsletter are NOT registered as Securities broker-dealers or financial investment advisors either with the U.S. Securities and Exchange Commission, Commodity Futures Trading Commission, or any other securities/regulatory authority. Nothing produced under Marquee Finance by Sagar should be construed as investment advice. Do your own research and contact your certified financial planner or other dedicated professional before making investment decisions. Investments carry risk and may lose value; Marquee Finance By Sagar LLC, Marqueefinancebysagar.substack.com or Sagar Singh Setia is not responsible for loss of value; all investment decisions you make are yours alone.