Before I begin, I want to thank you all for being a part of the Marquee Finance By Sagar community. This is my 100th newsletter, and the journey that began roughly 18 months ago has been truly incredible and unbelievable.

On this occasion, I am announcing a special undisclosed discount for students who want to upgrade to paid subscription. Interested students can mail me their student ids to avail the special discount at marqueefinancebysagar@protonmail.com !

Furthemore, 2 lucky people who like and share 100th edition of the newsletter will be awarded a 3 months comp paid subscription!!

October was marked by another deadly war that engulfed the heart of the Middle East.

The global financial markets were pounded by not only war but also the rising yields in the sovereign bond markets, which made investors super nervous and led to sell-offs across the equity markets.

Nonetheless, investors found solace in the shiny yellow metal and BTC.

Let us understand via intriguing charts the cross-asset movement and the global macro developments!

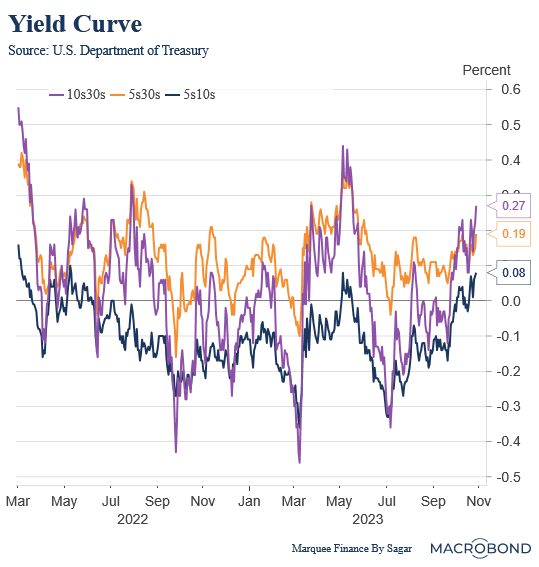

One of the rarest phenomena in the bond markets is the bear steepening, where the long-term yields rise more than the short-term yields. As the US macro data remains resilient, the yield curve witnessed a violent bear steepening in October.

Though bond markets don’t see further rate hikes, the higher for longer mantra was in full force this month.

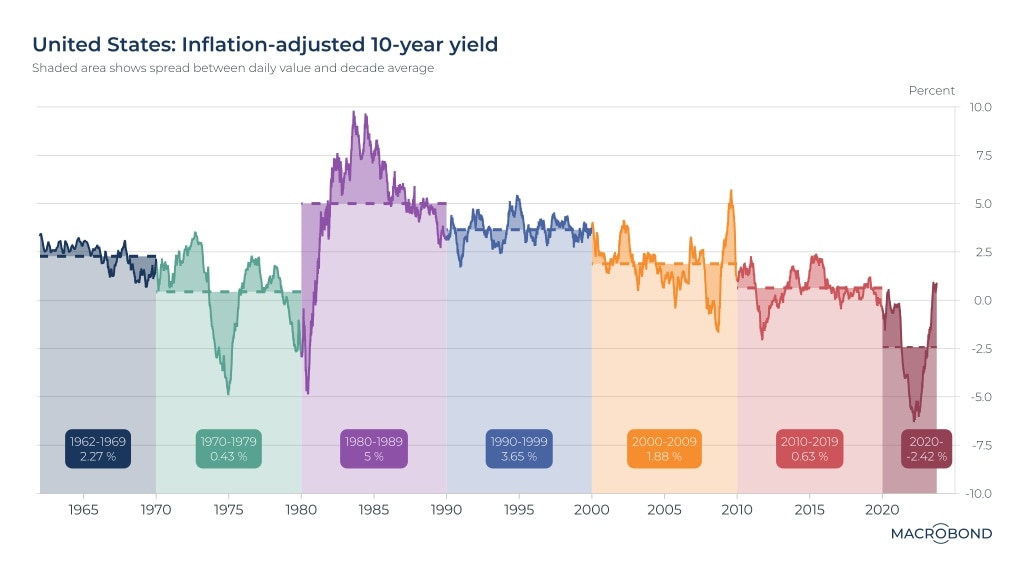

Real yields are calculated as = (nominal yields - inflation expectations). While the US 10Y yield flirted around 5%, the long-term inflation expectations have been well anchored at around 2.5%.

Furthermore, the 2000-2009 10Y Real Yield average was 1.88%, and thus, current levels of real yields are really attractive for long-term bond investors.

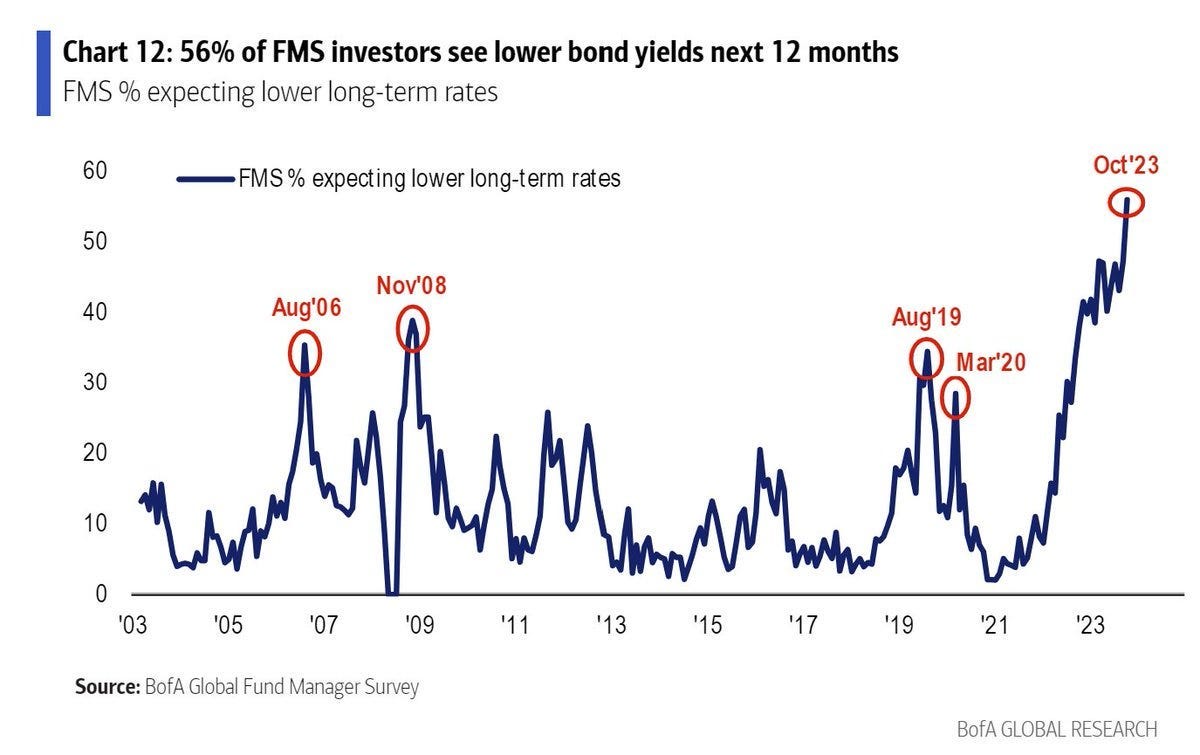

Source: Macrobond As yields became lucrative, there have been massive inflows in ETFs tracking the long-term treasuries. In fact, enormous call option activity has transpired in TLT in the last few days.

The institutional flows have also increased significantly as investors see lower yields in 2024.

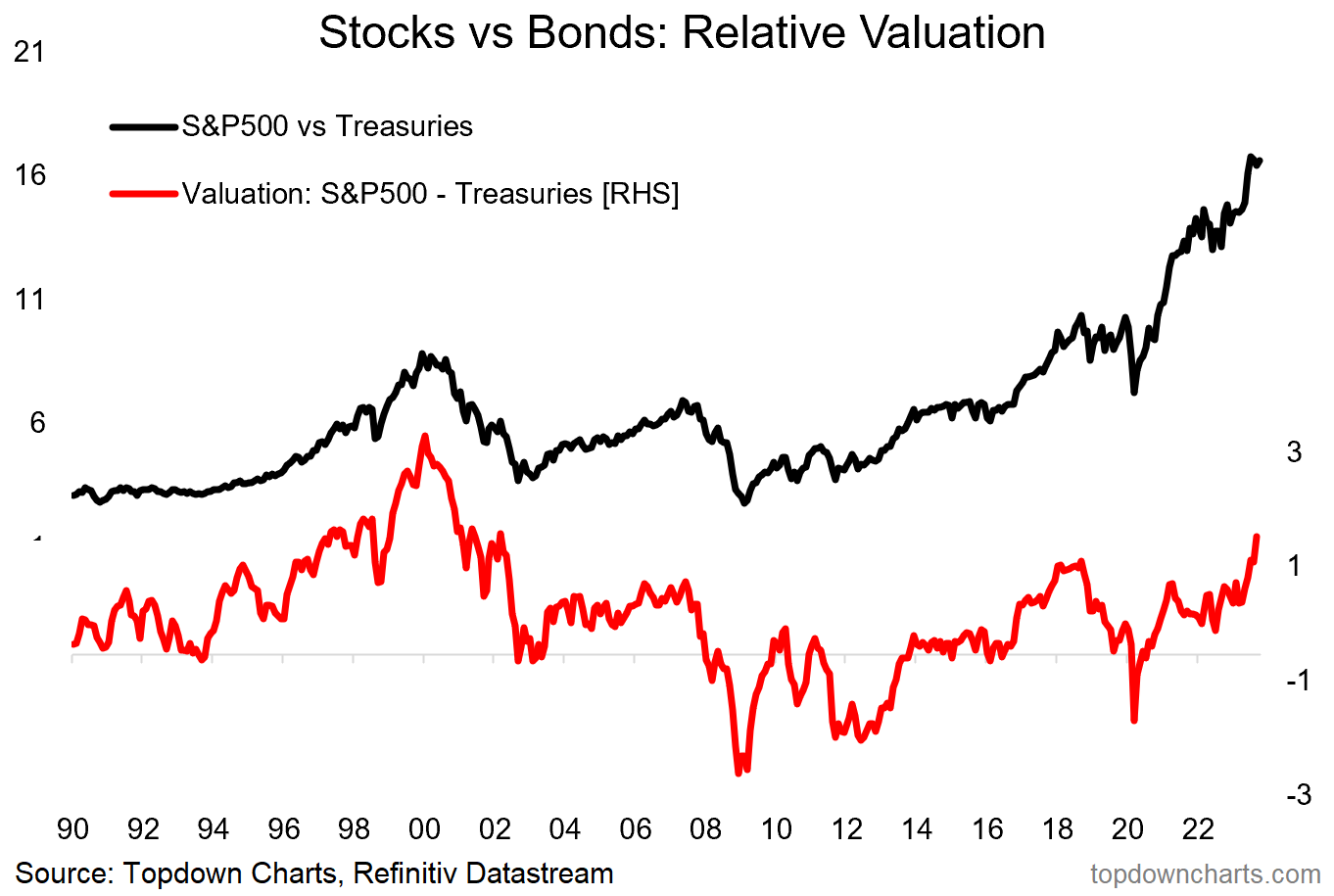

Source: BofA Higher yields have led to a crash in equity risk premium. Undoubtedly, thus, bonds have become much more attractive than stocks.

The relative valuation indicates that holding bonds over stocks will benefit investors at the current juncture.

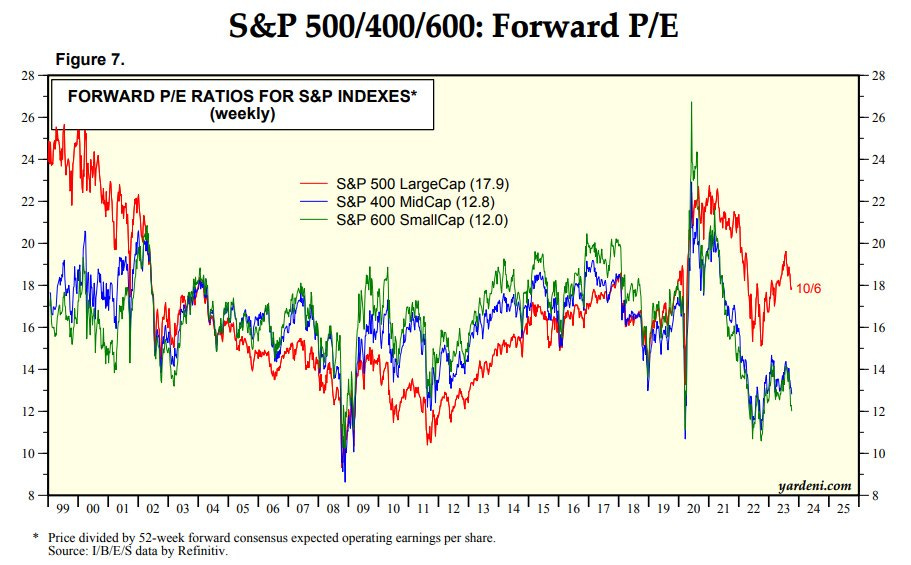

Source: Topdown Charts As the real yields skyrocket, the equity markets are now witnessing a contraction in multiples, which expanded due to the illusion of a soft landing.

While the forward PE multiple for the S&P 500 is still higher than 15X (long-term average), small caps are signalling more pain ahead as multiples contract to extremely low levels.

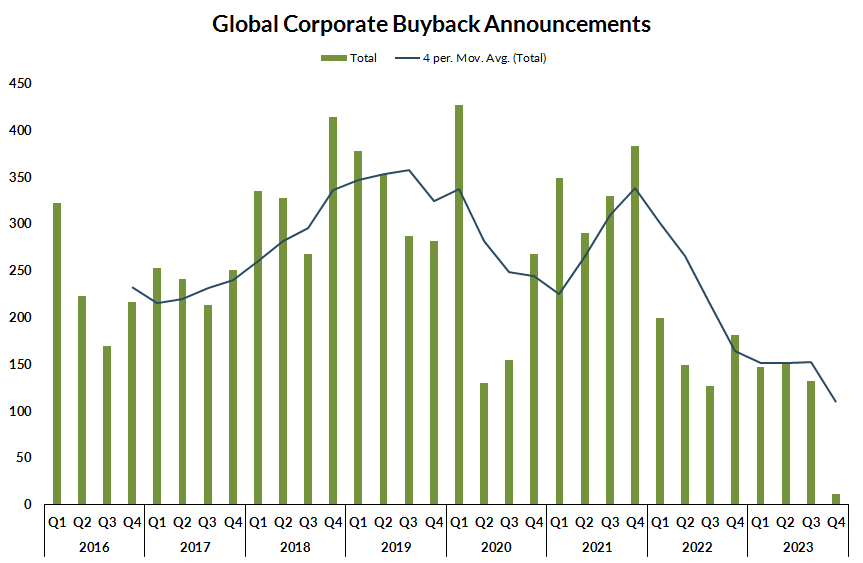

Source: Ed Yardeni One of the factors for the mega bull rally post-GFC was the golden era of low interest rates. Lower interest rates fuelled the buyback regime, where corporations borrowed heavily and repurchased their stocks.

As we enter a high-interest rate regime, the corporate buybacks plunge lower as the luxury of borrowing and buying back evaporates.

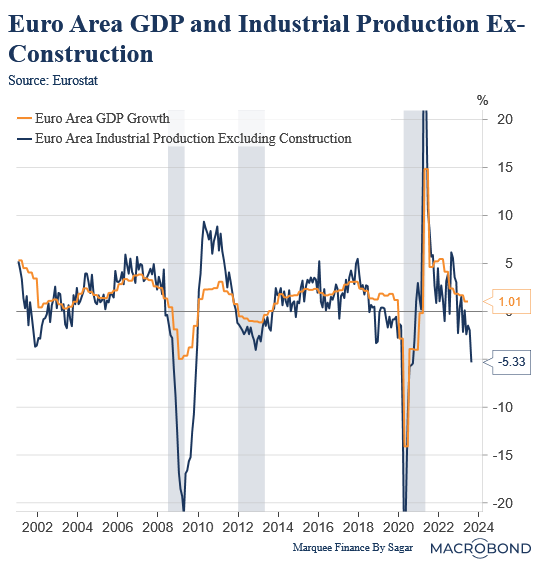

Source: Mike Zaccardi Europe has seen faster transmission of interest rates than the US. The result has been a sharp downturn in cyclical activity, with industrial production crashing.

No doubt, European countries are the first to enter a much anticipated “recession” in the West.

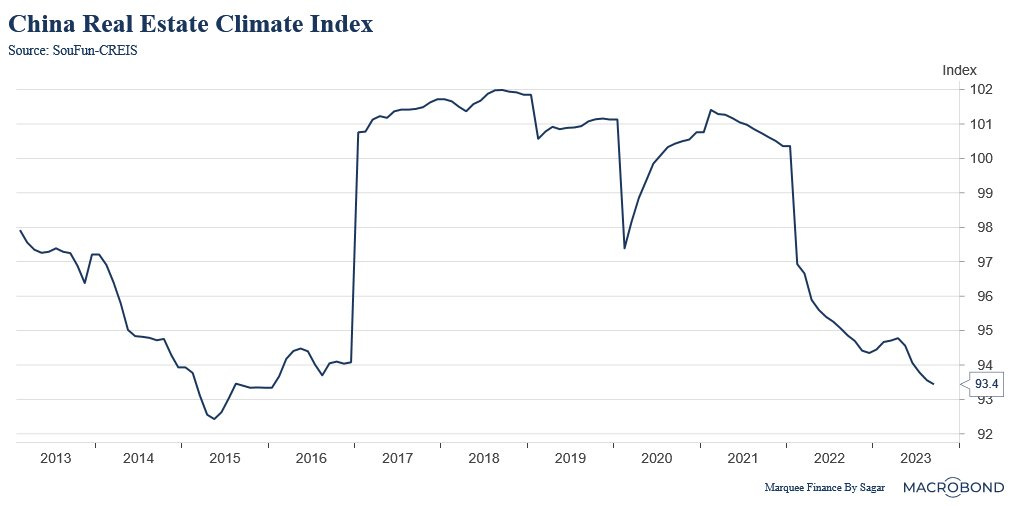

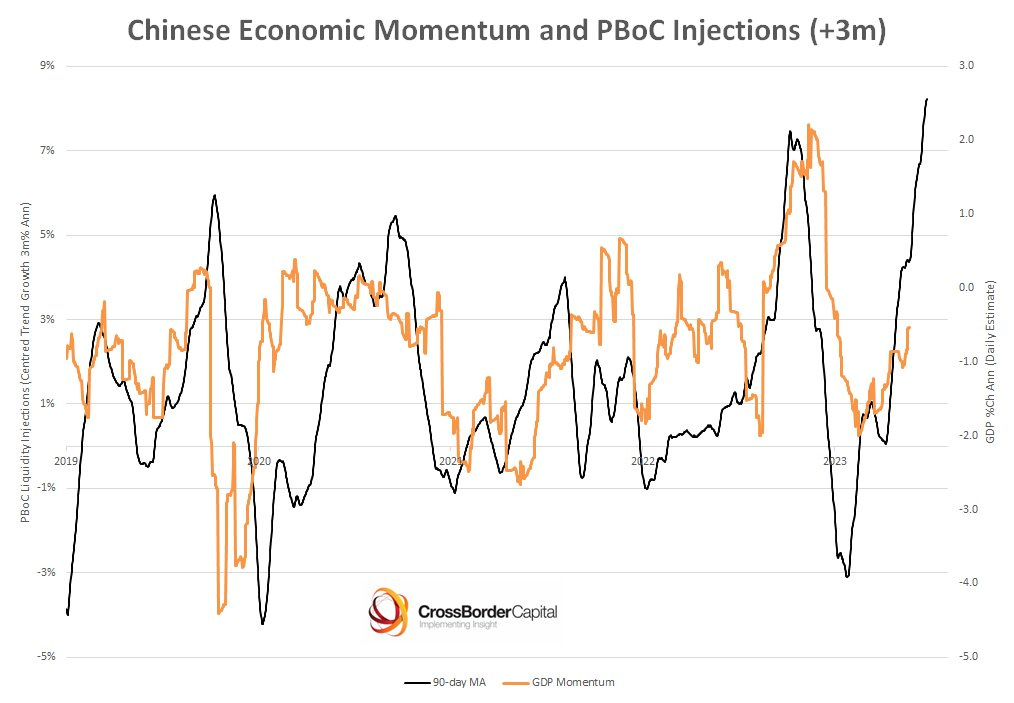

China’s epic property meltdown continues as the sentiment has worsened considerably.

As the spillover effects from the property meltdown haunt the consumers and, thus, the economy, Xi Jinping visited PBoC and announced additional fiscal measures to spur the economy.

As a result of enormous monetary and fiscal stimulus in China, it is expected that the Chinese economic momentum will finally revive, leading to a “Santa rally” in Chinese stocks.

Nonetheless, some people speculate that the Chinese money is moving to hard assets like Gold and BTC instead of stocks.

In the East, Japan has finally won its long-drawn battle against deflation.

The inflation projections have been significantly revised upwards by the BoJ in its policy today, and the breakeven rates are flying.

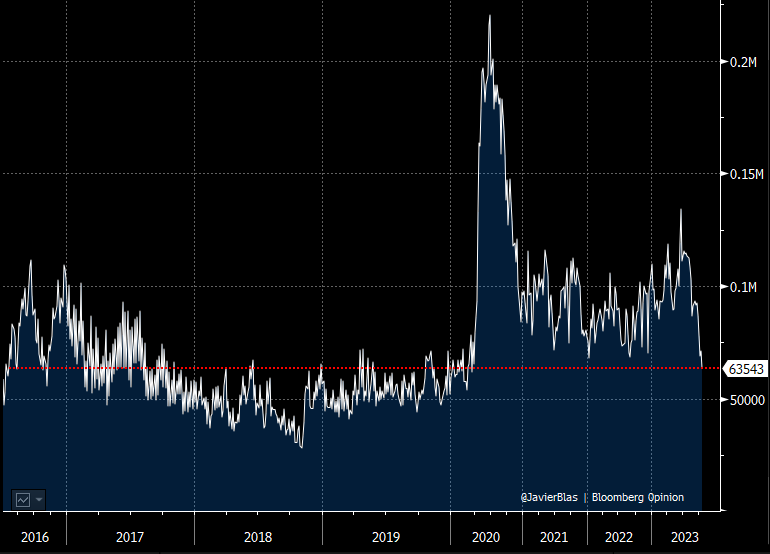

Source: AlessioUrban, BBG There was a considerable debate about Iran’s involvement in the October 7th attack. Nevertheless, Iran has seen an enormous increase in oil production and has liquidated massive amounts of floating storage. Maybe the sanctions are now ineffective against Iran and Russia.

As a result, global crude oil in floating storage has declined to a near 4-year low of around 63.5 million—one more sign of a tight physical market.

Source: Javier Blas While everyone is not a fan of orange juice, most of the people I know, including yours, truly are big lovers of chocolates.

Unfortunately, we all will have to shell out a lot more to buy our favourite chocolates as cocoa prices are off the roof. Isn’t that inflationary?

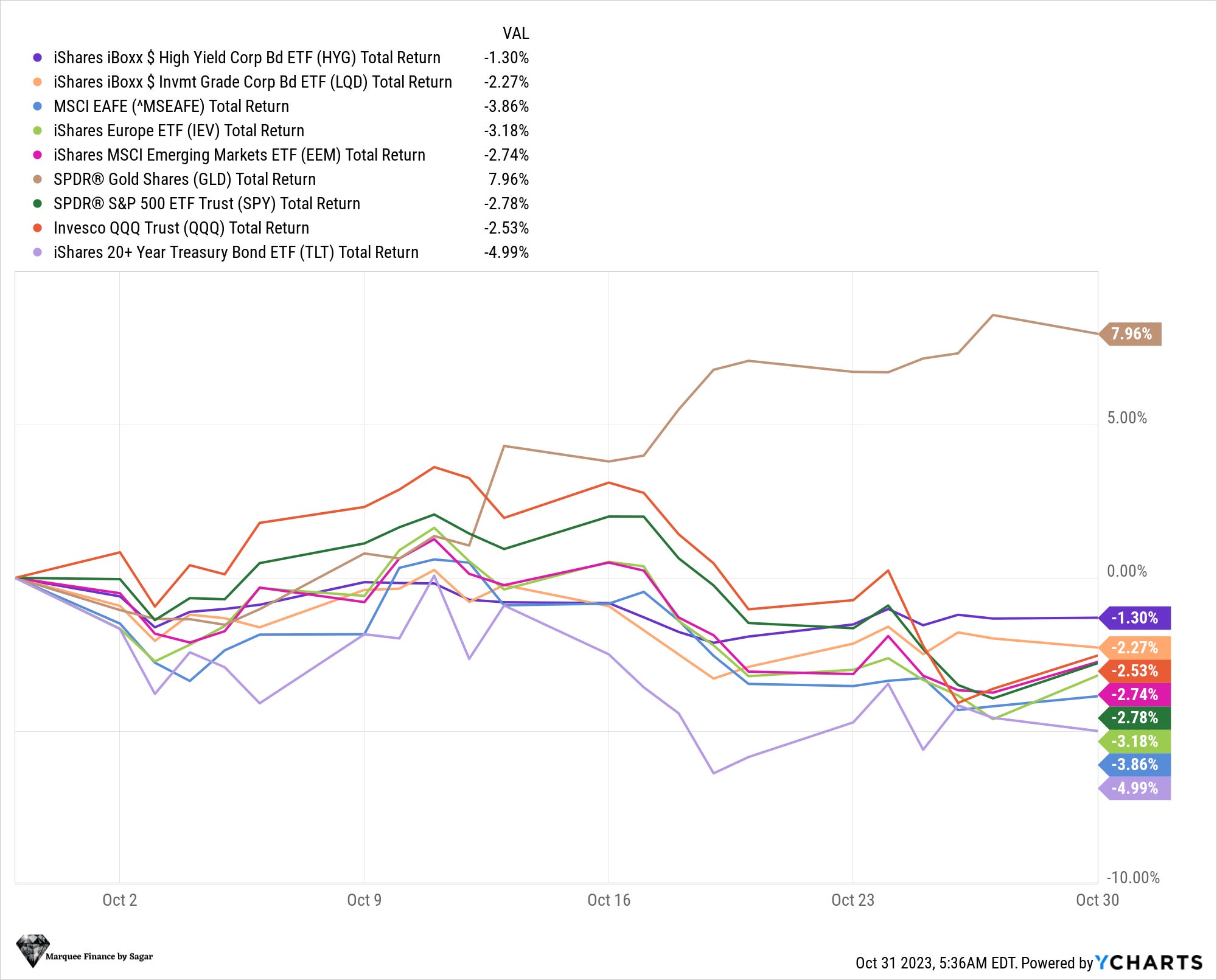

Source: BBG No doubt that considering geopolitical conflict and the mounting debt concerns in the US, the best performers in October were Gold and BTC.

SUPER IMPORTANT ADDITIONAL CHART:

Touted as the next big bull market leader with trillions of dollars of potential, the clean energy sector has burnt investors' fingers. The bubble in clean energy has burst, and the stocks/ETFs are below the pre-COVID levels with the drawdown of more than 60%.

Source: Bespoke

Disclaimer

This publication and its author is not a licensed investment professional. The author & any other individuals associated with this newsletter are NOT registered as Securities broker-dealers or financial investment advisors either with the U.S. Securities and Exchange Commission, Commodity Futures Trading Commission, or any other securities/regulatory authority. Nothing produced under Marquee Finance by Sagar should be construed as investment advice. Do your own research and contact your certified financial planner or other dedicated professional before making investment decisions. Investments carry risk and may lose value; Marquee Finance By Sagar LLC, Marqueefinancebysagar.substack.com or Sagar Singh Setia is not responsible for loss of value; all investment decisions you make are yours alone.