As chaos reigns in the Middle East, with Israel and the US launching an all-out attack on Iran in Operation Fury (US) and Operation Lion’s Roar (Israel), markets were partially prepared for the eventuality.

With oil rallying to $67, Gold to $5200, equity VIX stubborn at 20, and the bond markets sensing a risk-off mode despite a hot PPI, Mr Market, to some extent, priced in a war.

However, there are different scenarios which can play out in the coming days. The response from Iran and the participation of other Gulf countries will dictate the intensity and duration of the war.

We will discuss the probable scenarios later on.

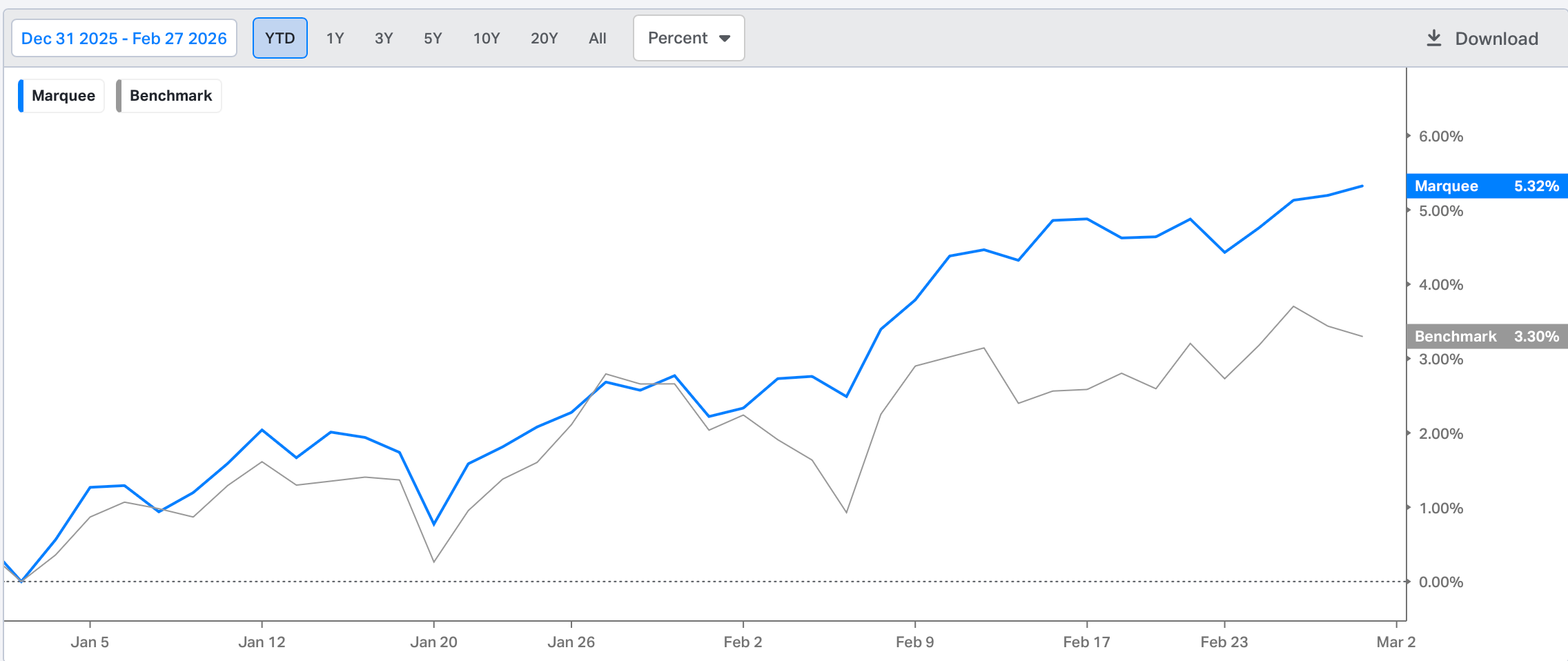

We closed at YTD highs and are up by 5.32%, compared to 3.3% for the benchmark.

The bond rally has been a tailwind for us, along with our positions in the US and RoW.

Let’s take a deep dive into the cross-asset universe!

Equities!

Roughly 18 months ago, we introduced the Thematic Investing Series, in which we discussed themes that are likely to outperform the markets in the coming decade.

We invested in several of the stocks and have delivered 6-7 multibaggers in the Thematic Investing series.

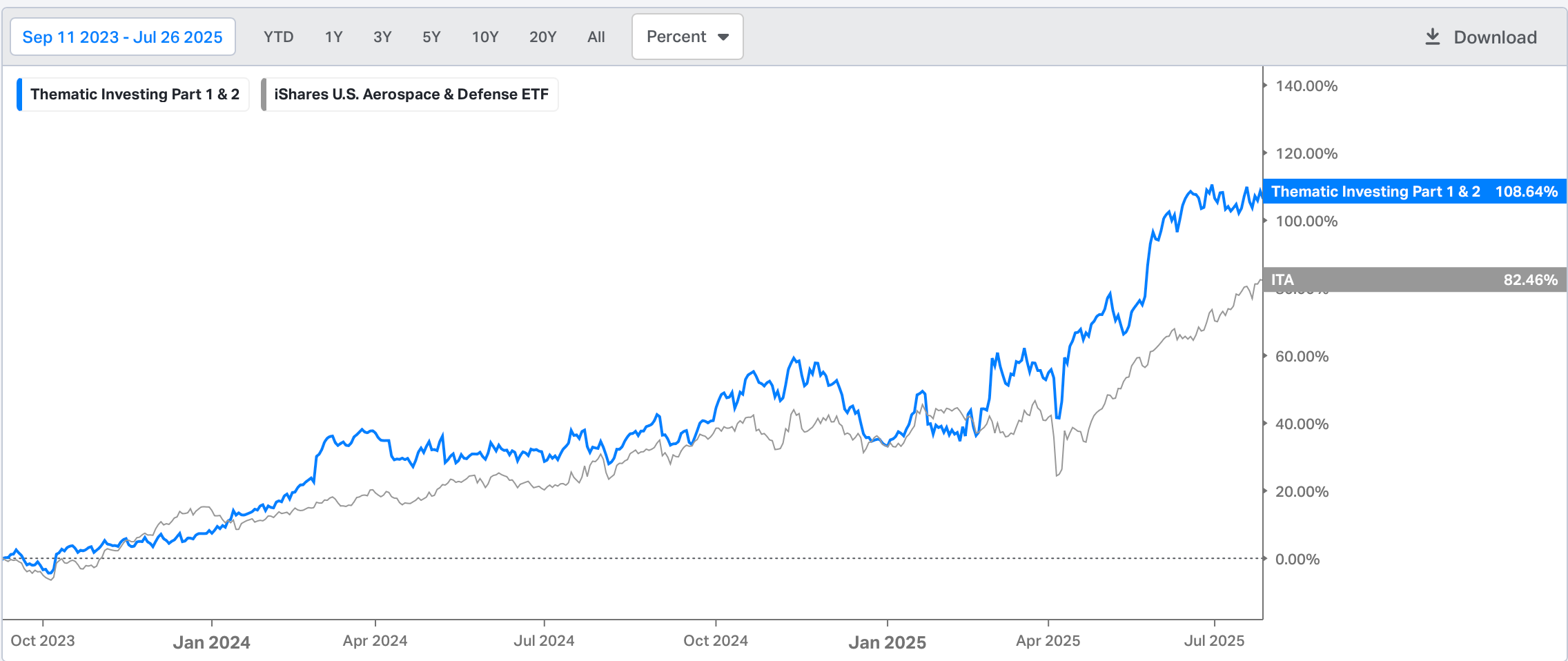

In Thematic Investing Part 1 & 2, we researched and analysed the Aerospace and Defence sector in detail and bought two stocks (it’s an equal-weight portfolio).

The equal-weighted PF outperformed the benchmark ITA ETF for most of the time since inception and has generated significant alpha.

While we didn’t buy the others due to valuation concerns, one of the recommended stocks turned out to be a multi-bagger.

Thematic Investing Part:1

Welcome, folks, to the brand new edition of the Marquee Finance By Sagar. Most of you know me as a macro investor; however, since the advent of my investing journey, one of my passions has been to pick stocks actively.

Thematic Investing Part 2!

Welcome to the second part of the Thematic Investing series that we initiated a few weeks back. In the first part, we did a comprehensive overview of the Aerospace and Defence (A&D) sector (new subscribers can click here to read Part 1).

In October 2023, we wrote about a theme which we believed had long-term potential.

Although there have been several challenges since we wrote the piece, especially the demand for luxury goods in the world’s largest market (China), we have been able to deliver superior returns.

We finalised two stocks and are currently holding one stock in the PF (purchased it late).

We are up 58% on Thematic Investing Part-3, outperforming the benchmark LUX ETF by a huge margin.

Thematic Investing Part-3!

“The single most important decision in evaluating a business is pricing power. If you've got the power to raise prices without losing business to a competitor, you've got a very good business. And if you have to have a prayer session before raising the price by a tenth of a cent

In Thematic Investing-4, we were early to the commodity supercycle, believing that the massive green transition would be a boon for the industry.

Thematic Investing Part-4 is an equalweight PF of 4 stocks.

We are up 81% compared to 87% returns for the benchmark ETF XME.

Thematic Investing Part:4!

“It is important not to view the transition as only onerous; the required economic transformation will not only create immediate economic opportunities but also open up the prospect of a fundamentally transformed global economy with lower energy costs and numerous other benefits.”-

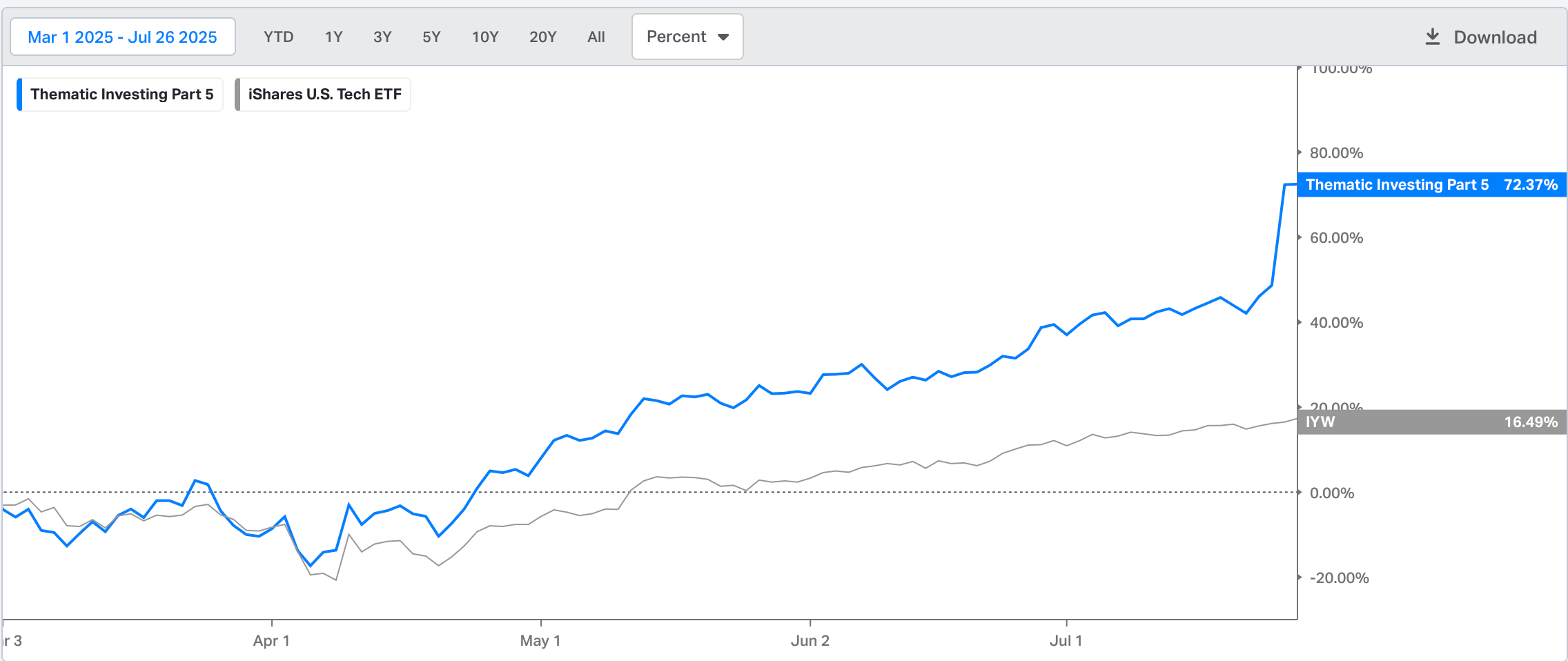

Last year, after a hiatus of more than a year, we wrote Thematic Investing-5, in which we discussed stocks that will benefit from billions of dollars in hyperscaler capex (particularly data centres).

In just one year, we are up 72% as one of the stocks has turned a multi-bagger (up 5X since liberation day).

Thematic Investing Part-5!

In 2023, we published four thematic investing parts focusing on themes (defence, luxury, and green energy) that we believed held long-term potential.

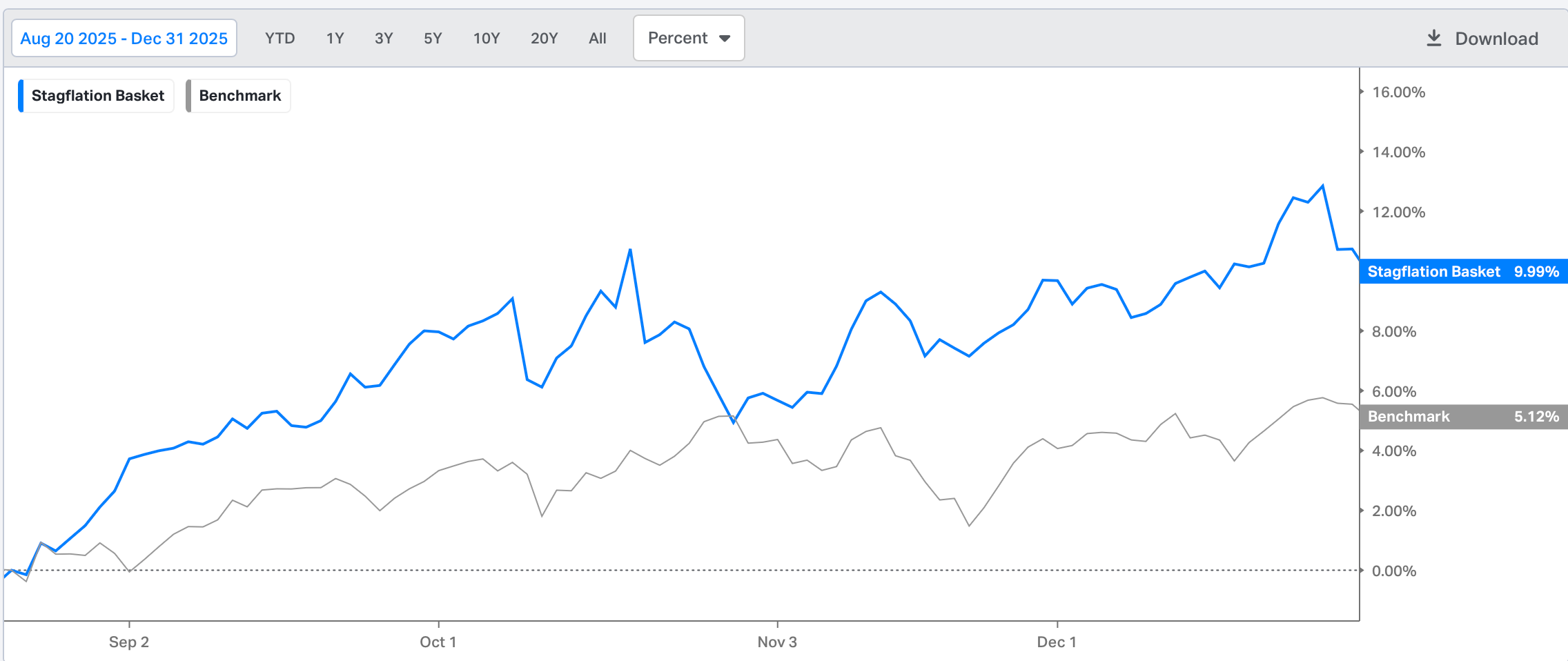

Furthermore, in August last year, as tariffs took hold, there were concerns about stagflation in the US economy.

We formed a stagflation basket at that time, which is up 10% since inception compared to 5% for the benchmark.

PS: Benchmark here is 60% ACWI and 40% GLAG (SPDR Bloomberg Global Aggregate).

Except for these, we were in the process of writing Thematic Investing Part-6, which we never completed, but recommended a stock where we made a cool 30% returns last year. The Thematic Investing Part-6 was about the electrification theme.

Note that we still hold 1 position (an ETF) in the Portfolio dedicated to the electrification theme, which we believe will outperform the broader markets due to the gigantic AI rollout.

Before we proceed further, paid subscribers can find the list of all the stocks covered in Thematic Investing Series in the spreadsheet.

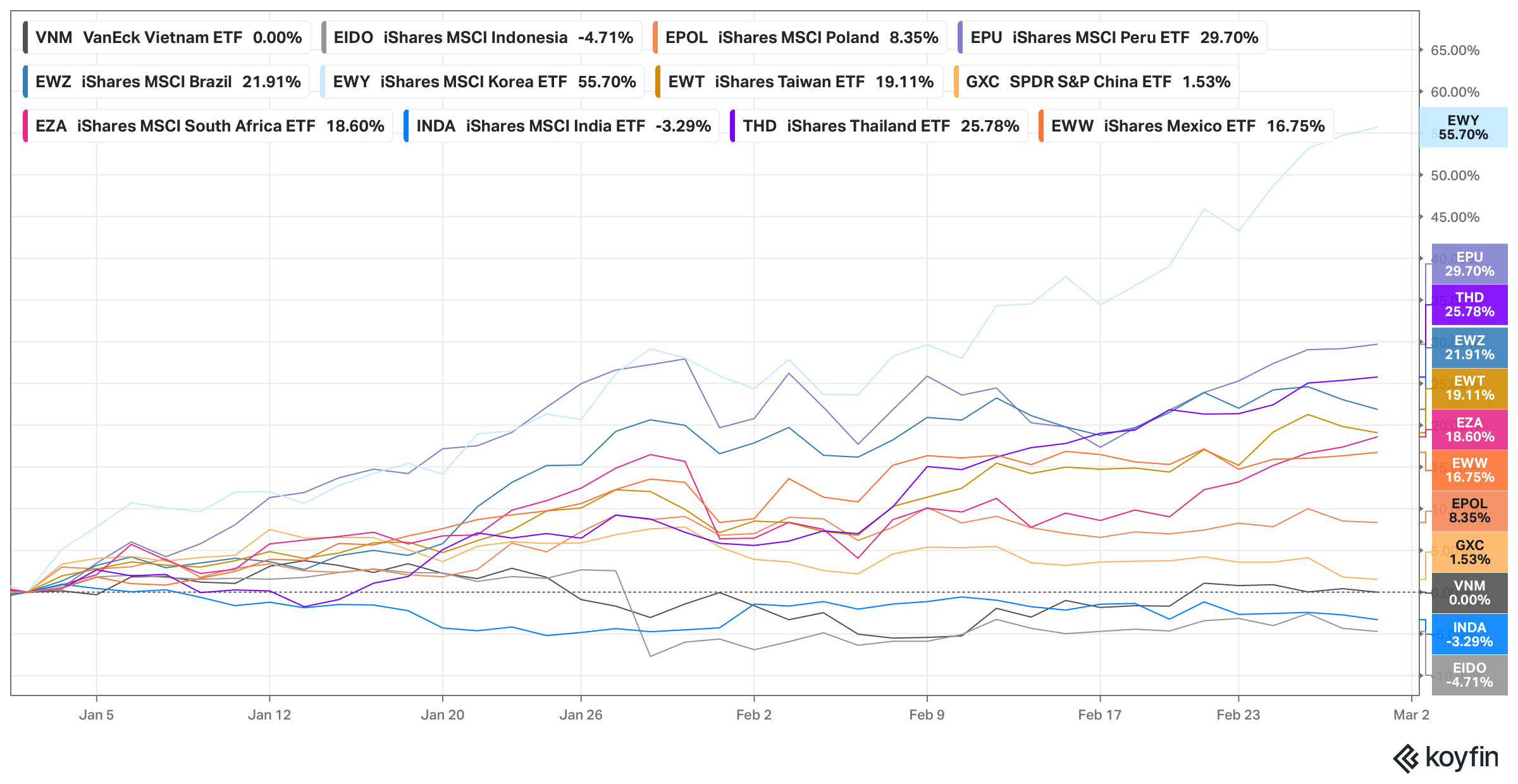

Since the last 15-18 months, we have been of the view that the Rest of the World (RoW) would outperform the US equity markets in the coming years, as the weight of the US in the ACWI Index has reached unprecedented levels, and the ROW has underperformed the US since the 2008 GFC.

Since Liberation Day, we have seen peaks in the SPY/EEM and SPY/VGK ratios, indicating that Emerging Markets and Europe have outperformed the US.

When we dig deeper, the outperformance was led by only 3 stocks as the flagship EEM ETF saw massive gains due to South Korea (Samsung and SK Hynix) and Taiwan (TSMC).

Furthermore, Latin America, led by Brazil and Peru, has been the outperformers due to the commodity gains we have witnessed in the last few months.

We believe that while the EMs will continue to outperform, the rally will broaden in the coming months, and we are very well prepared for it.

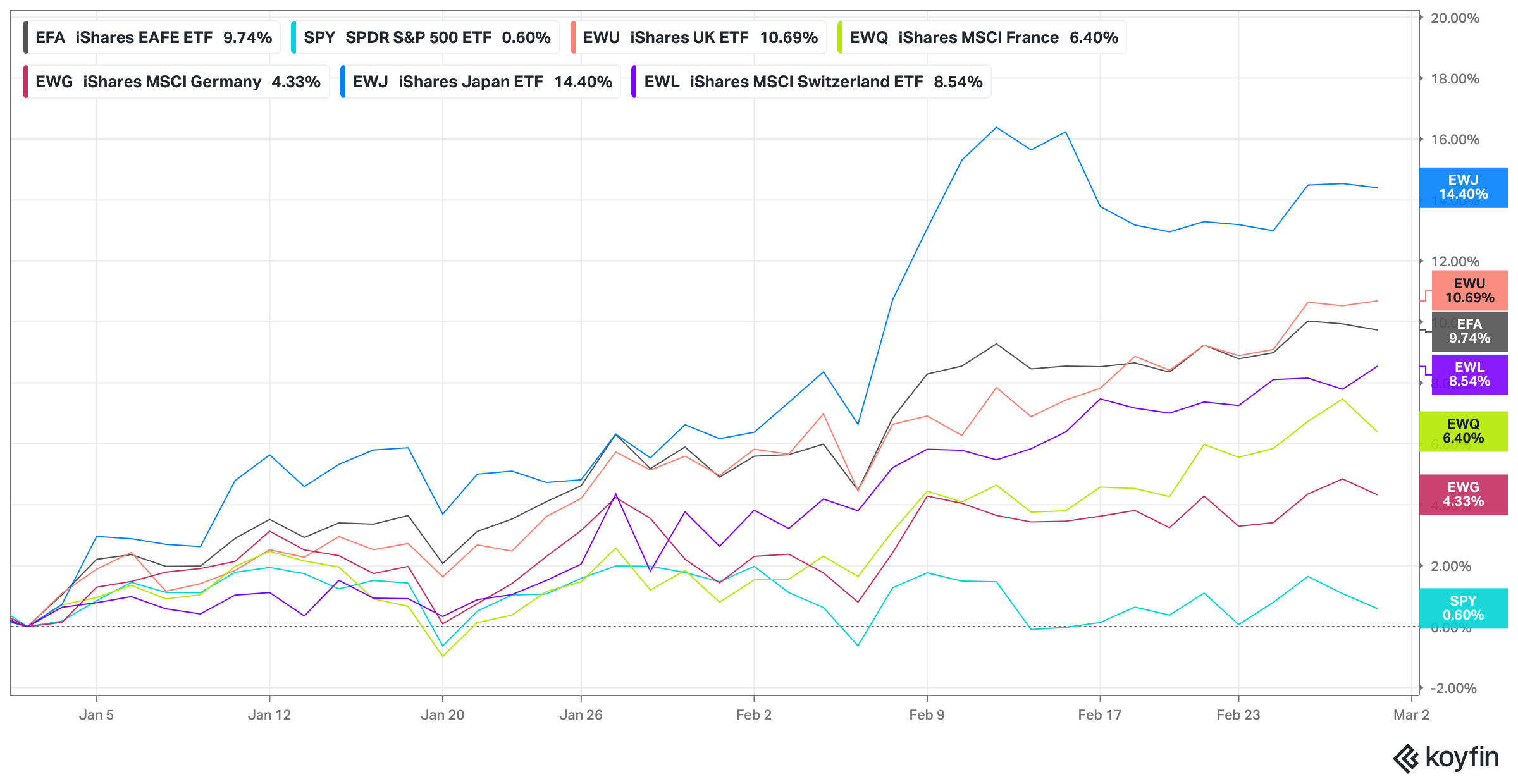

In developed markets, Japan and the UK have been the biggest outperformers YTD (the two markets outperforming the benchmark EFA ETF), and ironically, Japanese markets have witnessed a sea-change with valuations now approaching levels last seen decades ago.

Note that all the returns mentioned above are in dollars.

Since most currencies have significantly appreciated against the dollar, the returns have amplified.

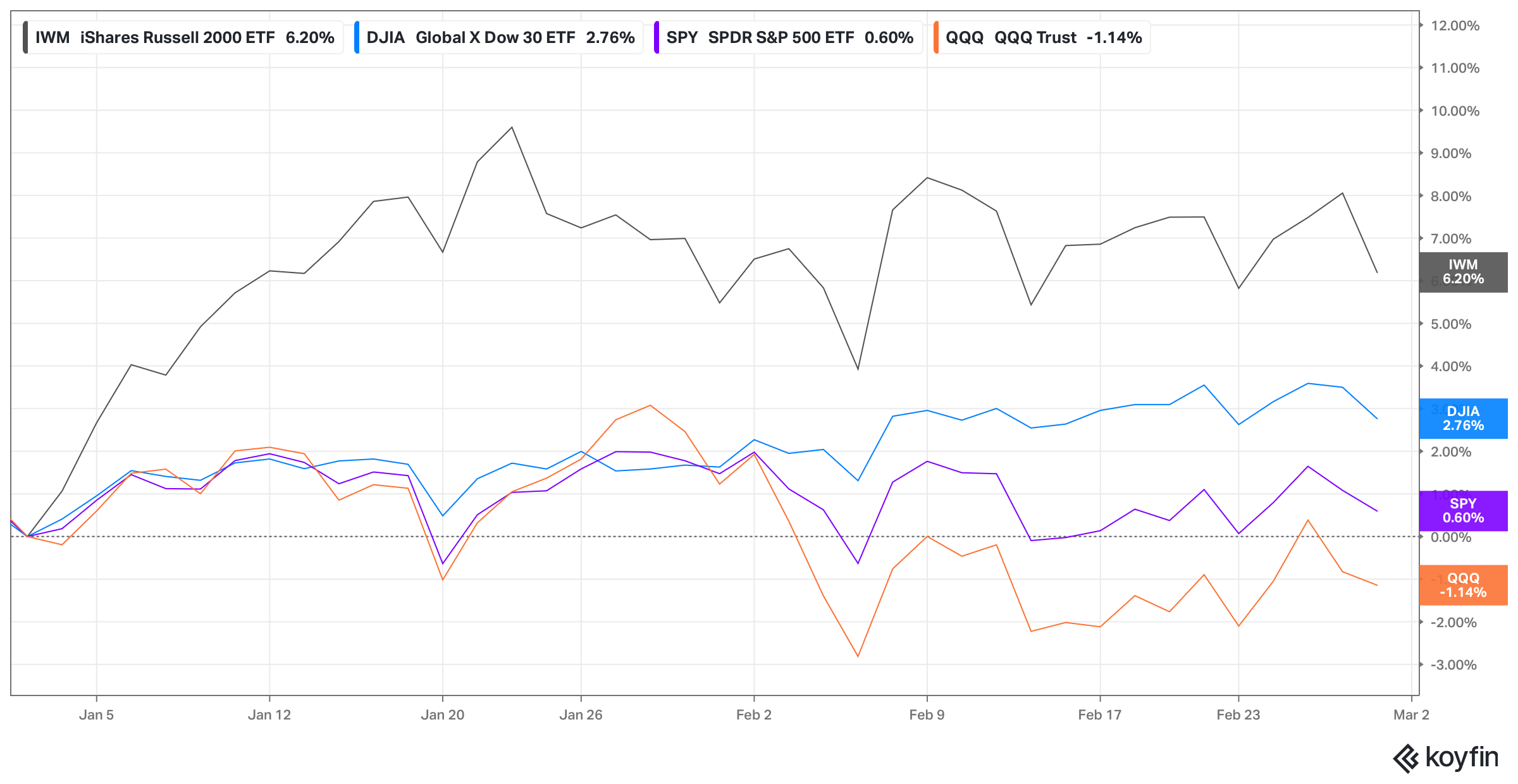

While the benchmark indices (S&P 500, NDX) are subdued, small caps and Dow Jones have been relative outperformers.

In fact, when we dig deeper, some of the constituents have been massive outperformers.

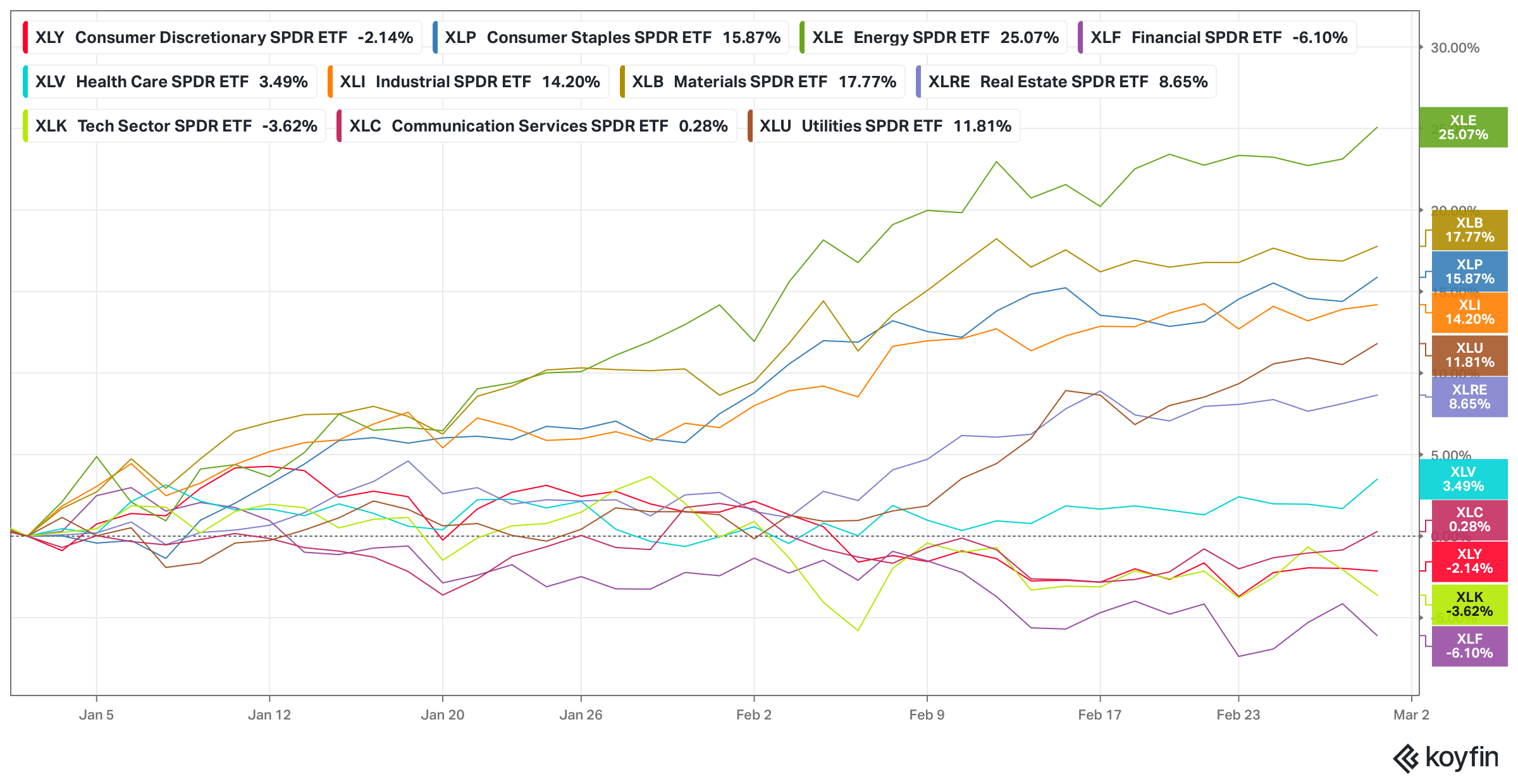

The energy sector has witnessed massive short covering and is the biggest gainer YTD (XLE is up 25%).

Other cyclical sectors, such as XLB, XLI and XLRE, have also given double-digit returns, while consumer staples, led by Walmart, is up a whopping 16%!

As private credit concerns rise, especially after the default of the UK-based MFS, banks took a massive hit yesterday (also post Dimon warning about structured products in the market, similar to what transpired before the 2008 GFC).

As a result, XLF is now the worst performer YTD.

XLK and XLY (due to AMZN) also posted negative returns amid concerns about hyperscaler capex.