While the whole market focuses on the situation in the Middle East, we have quietly seen carnage in the tech names.

The AI story is on the cusp of a meltdown as MSFT enters into a long-term bear market.

The Oracle 5Y CDS is now at its highest level since the GFC, as market participants panic and seek avenues to hedge their tech exposure.

The tech investors will have to endure extreme pain over the next few months (maybe years) as Mr Market resets valuations, as companies' FCF plummets and the Mag7, once known for hoarding cash and buybacks, are now turning net cash negative.

For the first time since the war began, we have also begun writing about the “post-war” analysis, in which we discuss the macro outcome based on probable scenarios.

Some of the outcomes are now certain, given the geopolitical situation and the further escalation over the last 24 hours from both sides (and post the entry of the Houthis).

Paid subscribers can directly jump to the geopolitical section for the analysis.

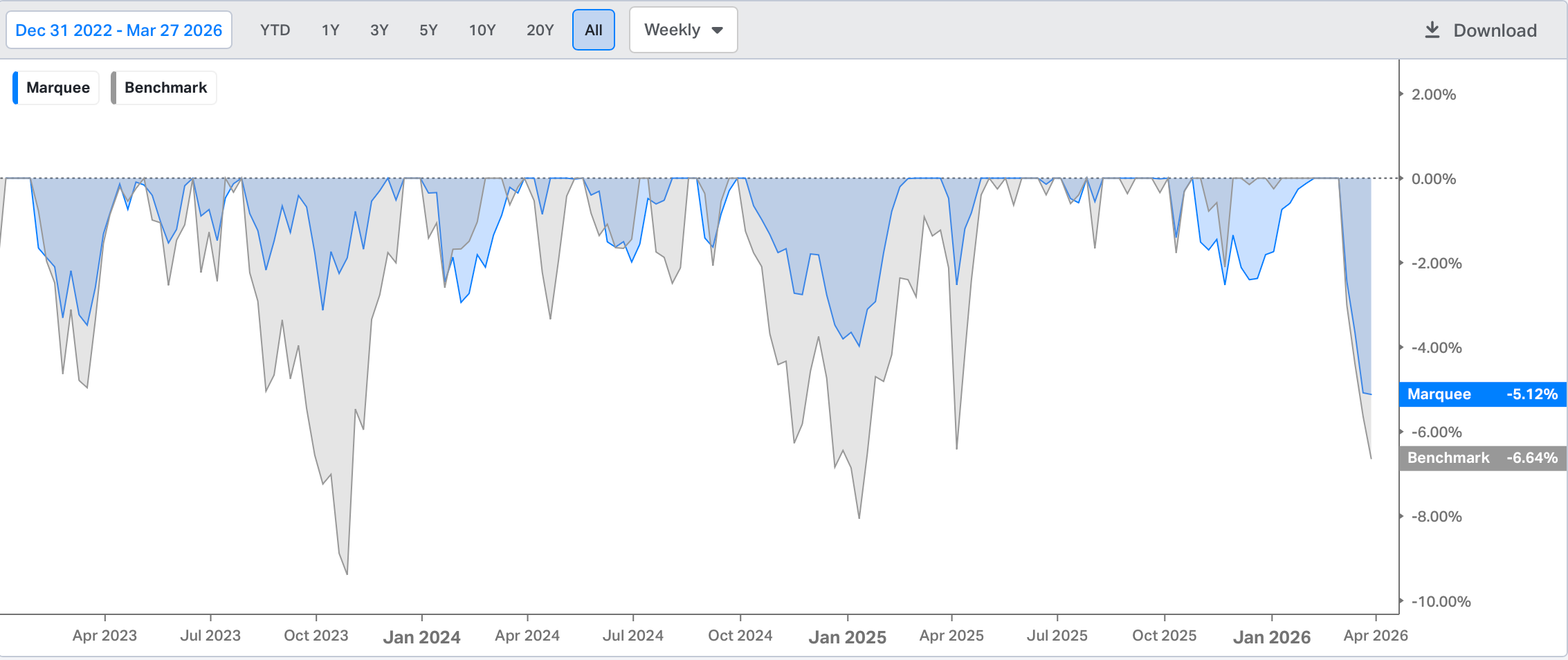

Since the beginning of the year, we have, for the first time, reported a negative YTD return, and the PF is down 7 bps, compared with a 356 bps drawdown for the benchmark.

It is also our largest drawdown from the highs since inception, as we were of the view that the war would be short.

However, as we became certain of weak technicals and a protracted war, we reduced duration and initiated short positions, which have helped us limit our drawdowns.

Let’s dig deeper into the world of macro, geopolitics and cross-asset relationships.

Macro!

The first signs of the Middle East conflict taking a toll on consumers were visible in Germany’s GfK Consumer Confidence.

Note that last week we saw the first signs of worsening business sentiment as Germany faces significant headwinds from higher energy prices.

The GfK consumer sentiment index dropped by 3.2 points to -28.0, the weakest reading since 2024.

Furthermore, Income expectations have fallen back into negative territory, while economic expectations have declined to their lowest level since Dec 2022.

If there is no respite in energy prices in the coming weeks, expect a “recessionary” reading across both soft and hard data.

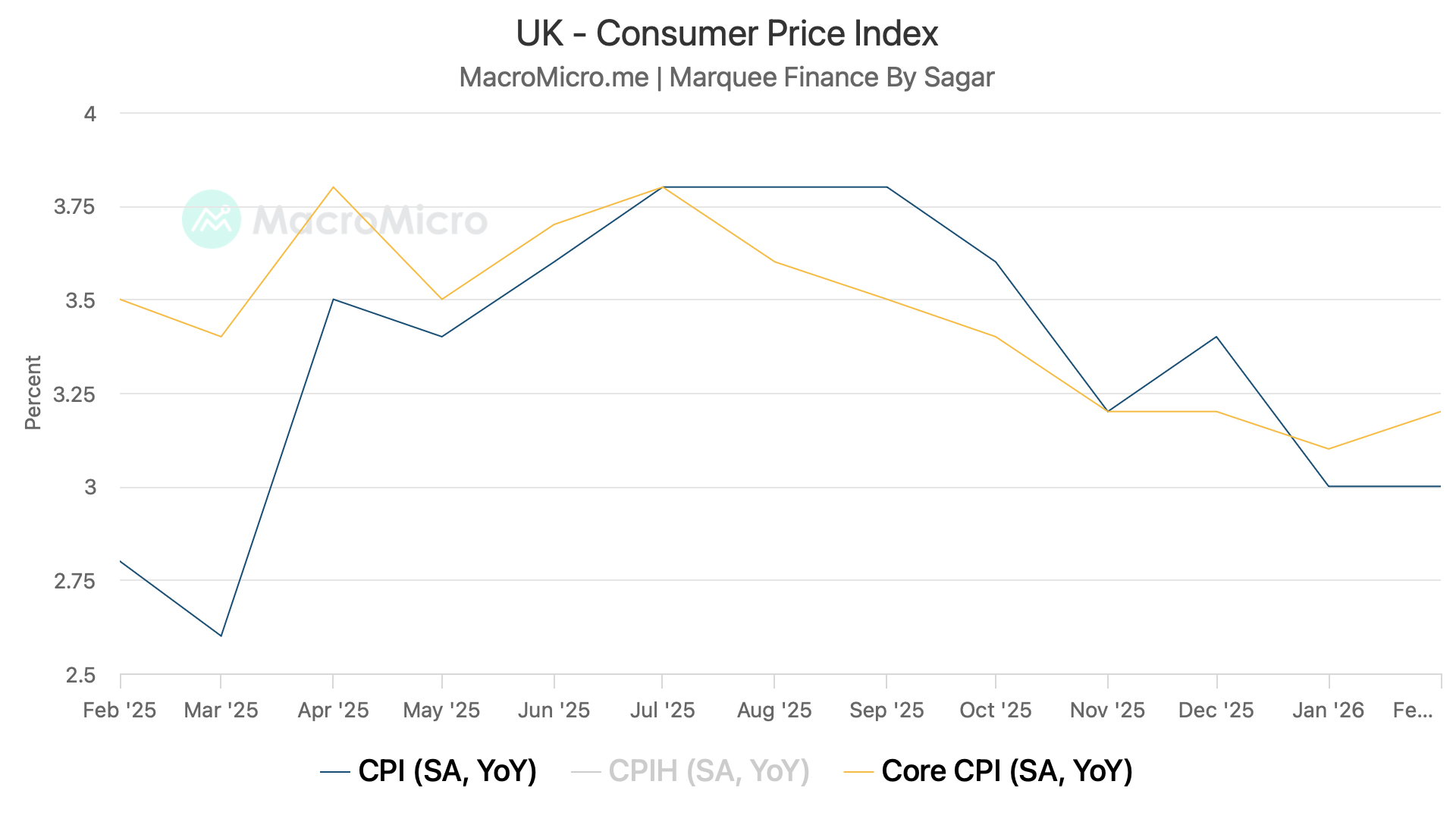

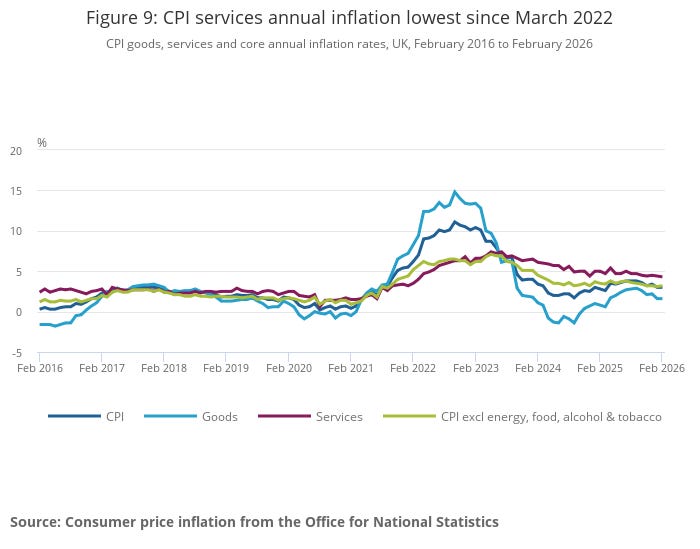

In the UK, headline CPI came in line with expectations.

The February Consumer Prices Index, including owner-occupiers’ housing costs (CPIH), rose by 3.2%.

Service price inflation was hotter than expected, and core prices rose to 3.2%, up from 3.1%.

However, the good news was that the CPI all-services index rose by 4.3% YoY, down from 4.4% in January.

The rate is the lowest since March 2022, when it was 4.0%.

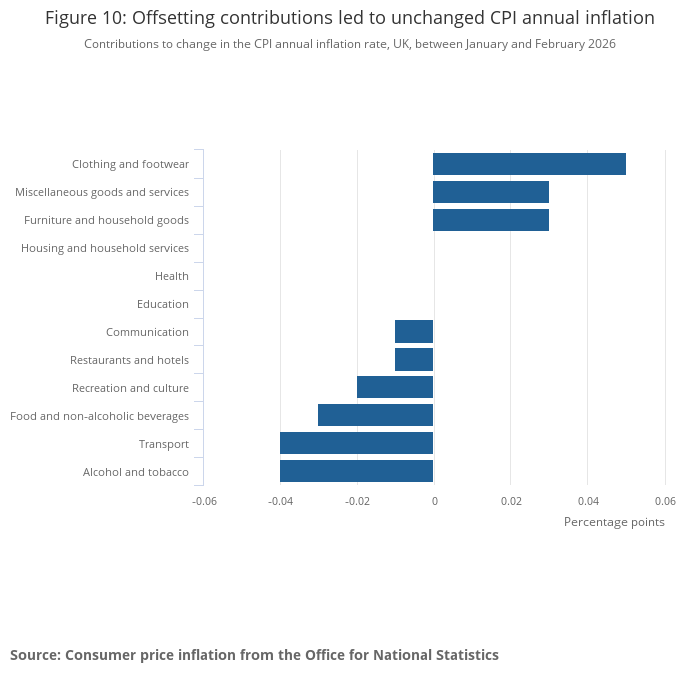

Clothing made the largest upward contribution, while Alcohol and tobacco put downward pressure on the CPI.

Note that these readings were before oil prices surged. BOE has already raised the CPI target.

Furthermore, there are unintended second-order effects of a spike in energy prices, and we expect CPI to surprise higher if the war is prolonged.

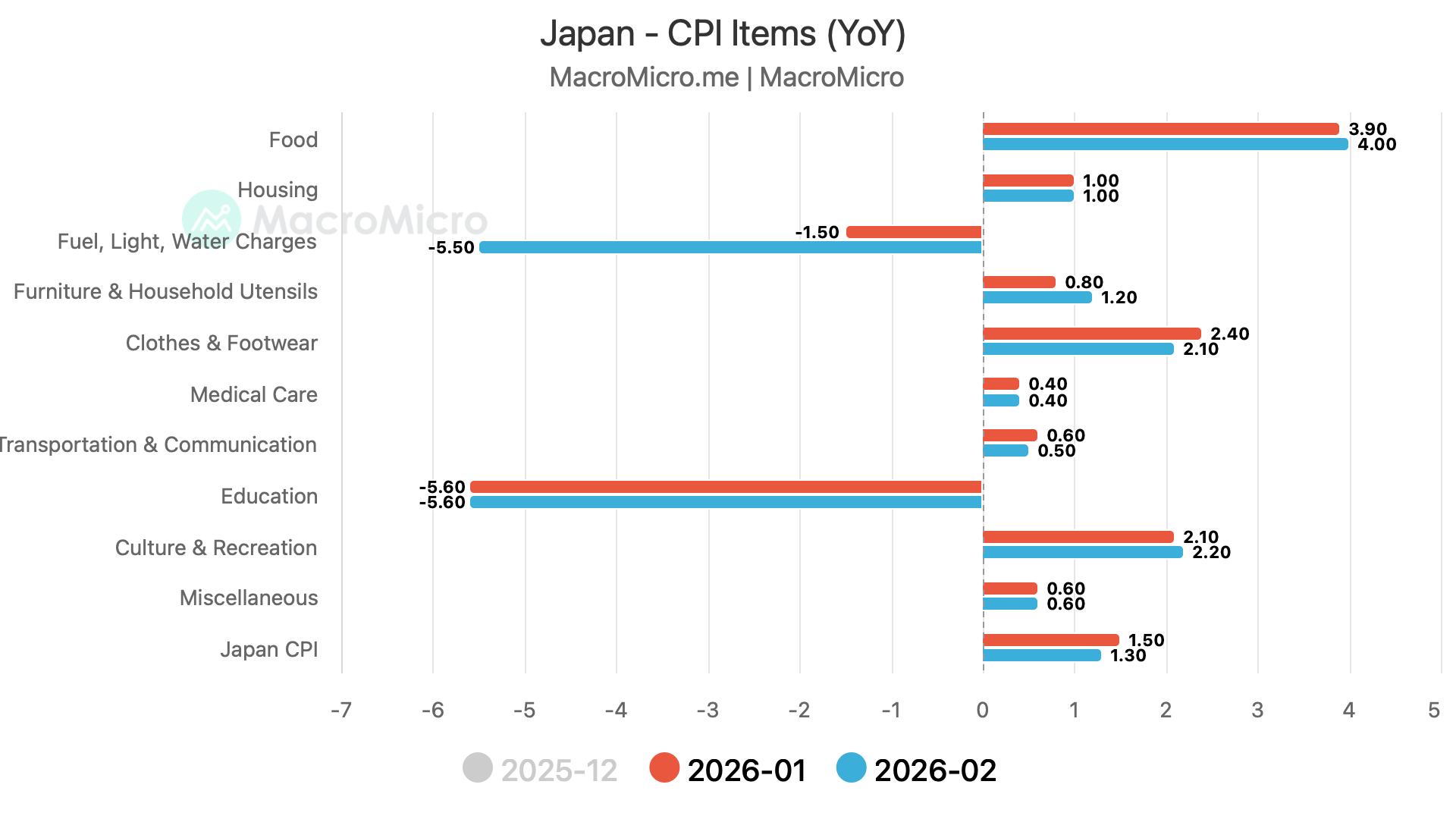

In the land of the rising sun, the headline CPI fell to 1.3% YoY, its lowest level since March 2022.

The disinflationary impulse stemmed from government fuel subsidies and the fall in rice prices (base effect).

The Core CPI, which includes oil products but excludes fresh food prices, rose by 1.6% YoY, missing economists’ median estimate for a 1.7% annual gain.

Core-Core inflation, which excludes food and energy, came in at 2.5%.

Since the Japanese government has vowed to keep fuel prices low (subsidies), we can expect the CPI to remain below 3% despite higher gas/oil prices.

However, a prolonged disruption could lead to higher prices across the board.

Equities!

In equities, we will stick with our allocation and thesis that