No Place To Hide!

The largest energy disruption since the 1970s has led to unprecedented cross-asset moves this week as markets prepare for a prolonged war.

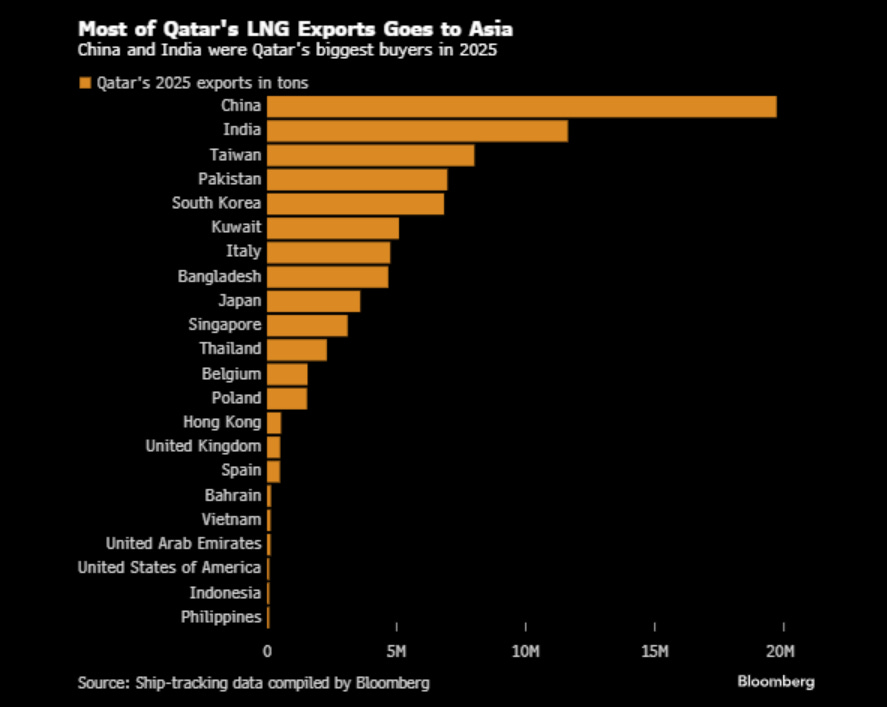

In a stunning development this week, Iran attacked Qatar’s largest gas field in retaliation, and as a result, 17% of Qatar’s LNG capacity was wiped out for the next five years with an estimated $20 billion loss in annual revenues at current gas prices.

While Asia will be the worst hit, Europe is also facing rising pressure, having decided to phase out Russian gas and now facing a dilemma after Qatar announced force majeure on long-term LNG contracts for up to five years for supplies bound for Italy, Belgium, South Korea, and China.

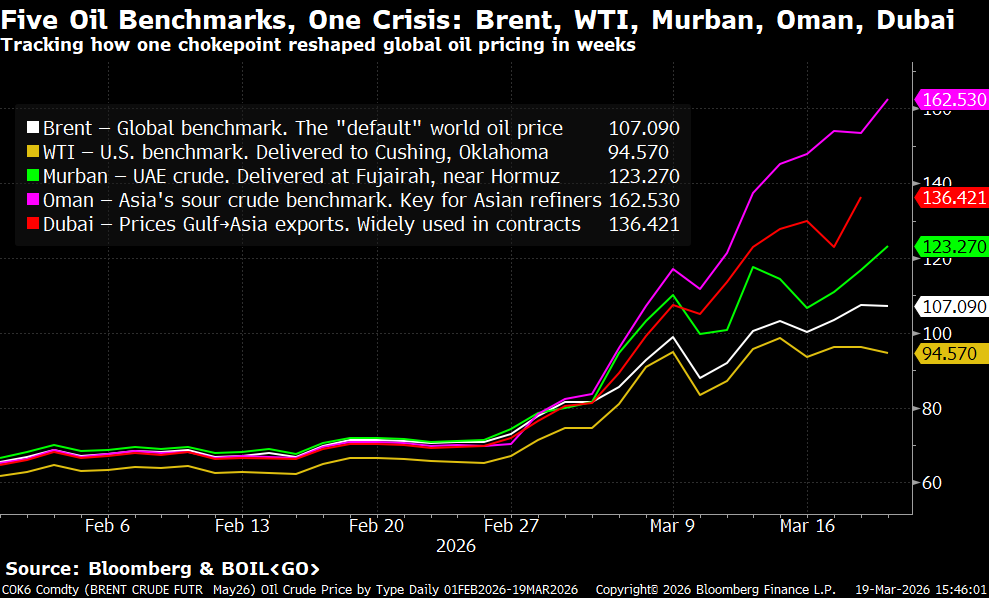

While the 2022 energy shock following the Russia-Ukraine war was driven by “fear” of disruption, we are witnessing actual supply disruptions as the Strait of Hormuz (SOH) remains closed.

Furthermore, production shutdowns (now totalling 7 mbpd+ across the GCC) will ensure that, even when SOH opens, the situation will take months to normalise, ensuring higher-for-longer oil prices.

As physical tightness deepens, this week saw record prices in Oman and Dubai as Asian refiners scrambled for physical barrels.

While the Trump administration was successful in curbing the WTI Prices (can’t remain decoupled for long, though), Brent has consistently traded above $100, with futures trading as high as $119 during the week.

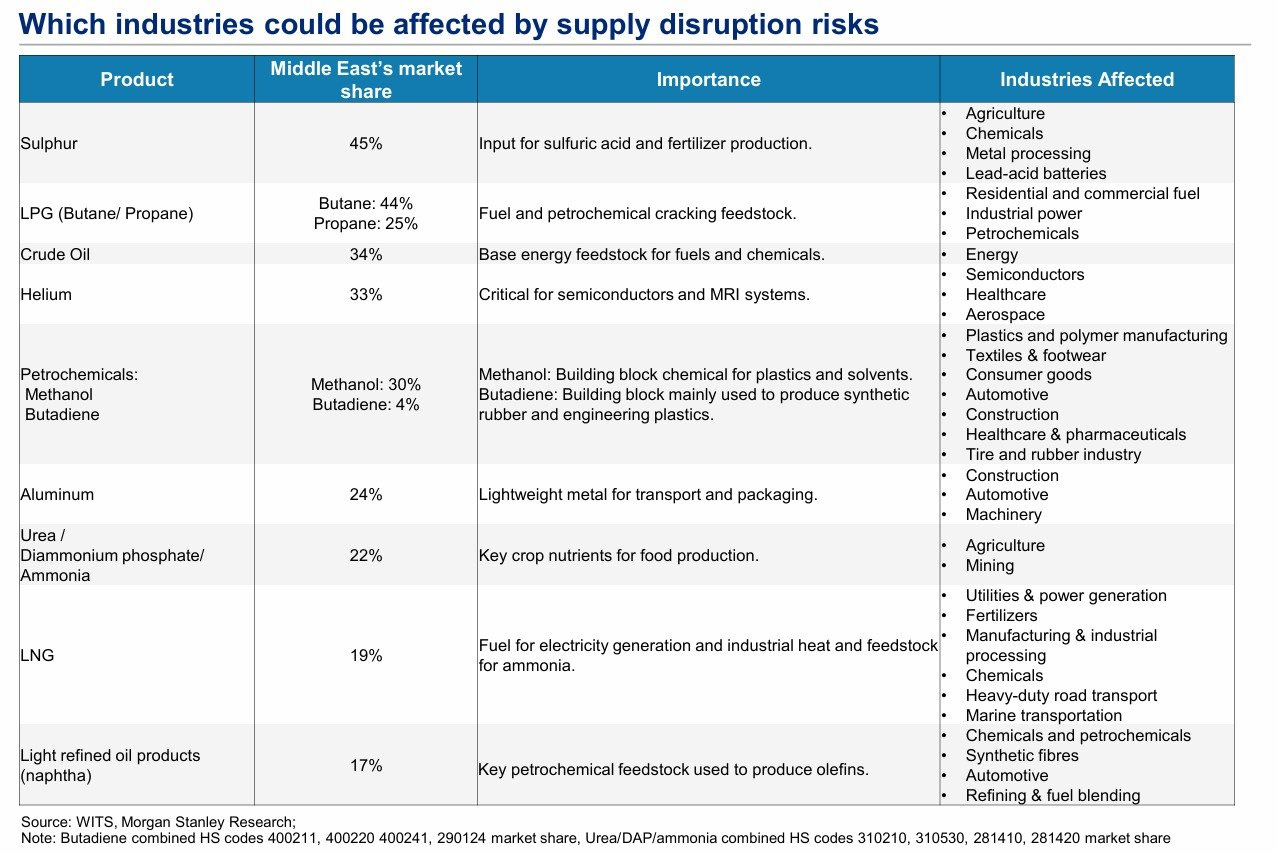

The disruption is now spreading across commodities as the Middle East accounts for a lion’s share in critical petroleum products, helium and fertilisers.

If SOH closure is prolonged, supply chains will be disrupted, triggering an inflationary wave similar to that during COVID. We will discuss in detail later.

Last week, we wrote the 4th edition of Explosive Setup, and these were the targets we mentioned:

Gold: $4200/4300

Silver: $62

Oil: $120

10Y: 4.35/4.5%

DXY: 102

S&P500: 6200/6300

DAX: 22k

CAC40: 7500

FTSE: 9700

Except for the DXY, we saw our targets nearly achieved across assets as the contagion, which began mid-week, spread after markets realised that the war is not getting over anytime soon, with boots on the ground now a high probability event (we discuss later in the geopolitics section).

In fact, there was no safe haven and thus no place to hide. Ironically, the only asset that has weathered the storm has been BTC.

We had multiple central bank meetings this week, and everyone was hawkish amid the recent rise in energy prices.

We reduced duration earlier in the week and, as a result, were able to limit the drawdown with the PF still outperforming the benchmark by about 250 bps.

Let’s begin today’s newsletter and comprehend the extremely elevated cross-asset moves!

US/Equities/Bonds/Oil/Dollar/Gold/Silver!

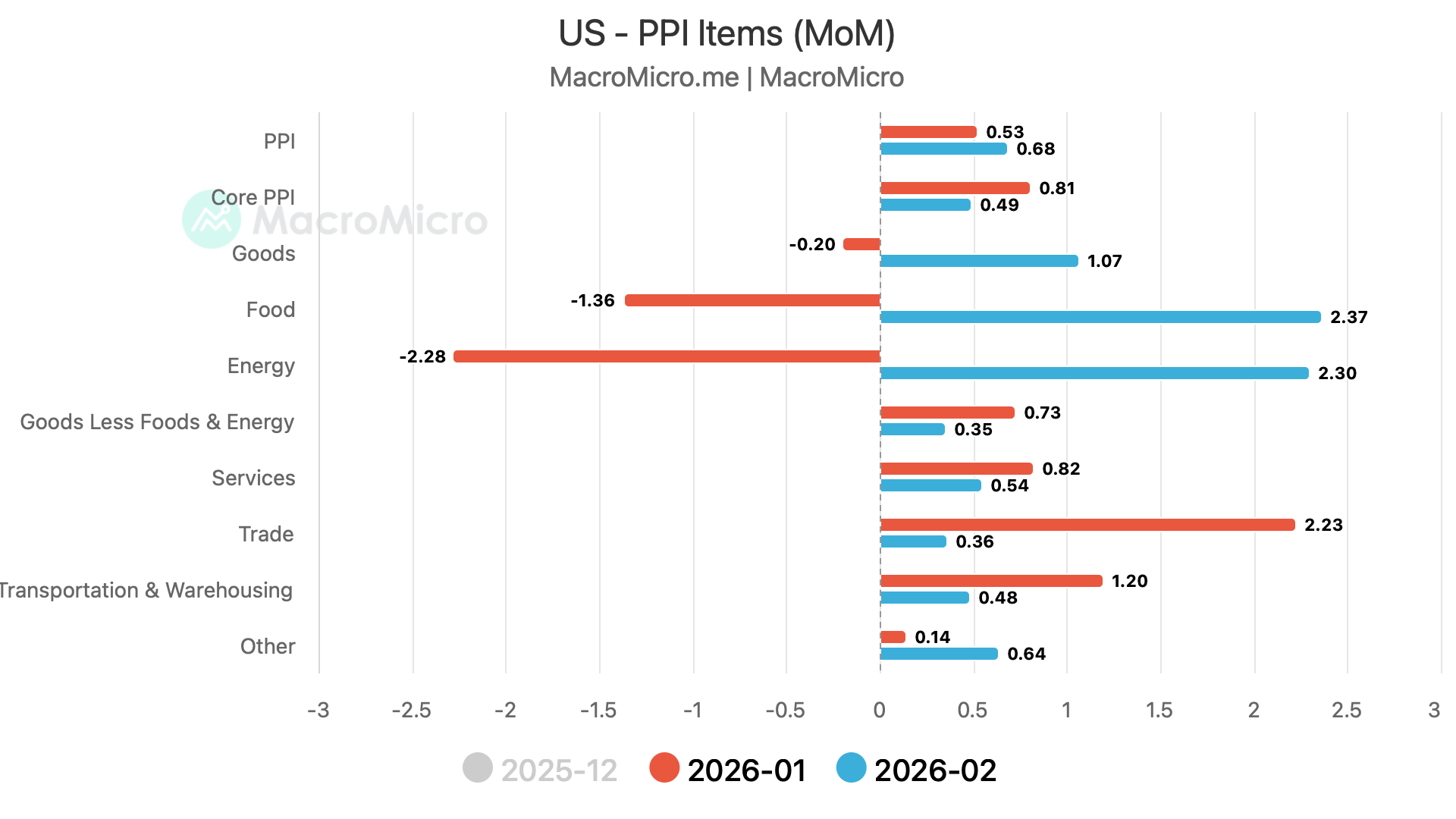

We got a really hot PPI print this week.

Headline PPI: +0.7% MoM vs. +0.3% est.

Core PPI (ex. food & energy): +0.5% MoM vs. +0.3% est.

We saw higher prices across the basket.

The costs of processed goods for intermediate demand rose 1.6%, the largest increase since August 2023.

Whereas farm products were up 0.43% MoM, with fresh & dry vegetables alone up nearly 49%.

Note that Energy was up 2.3% MoM, before the war broke out and gas prices surged by more than 33% MoM.

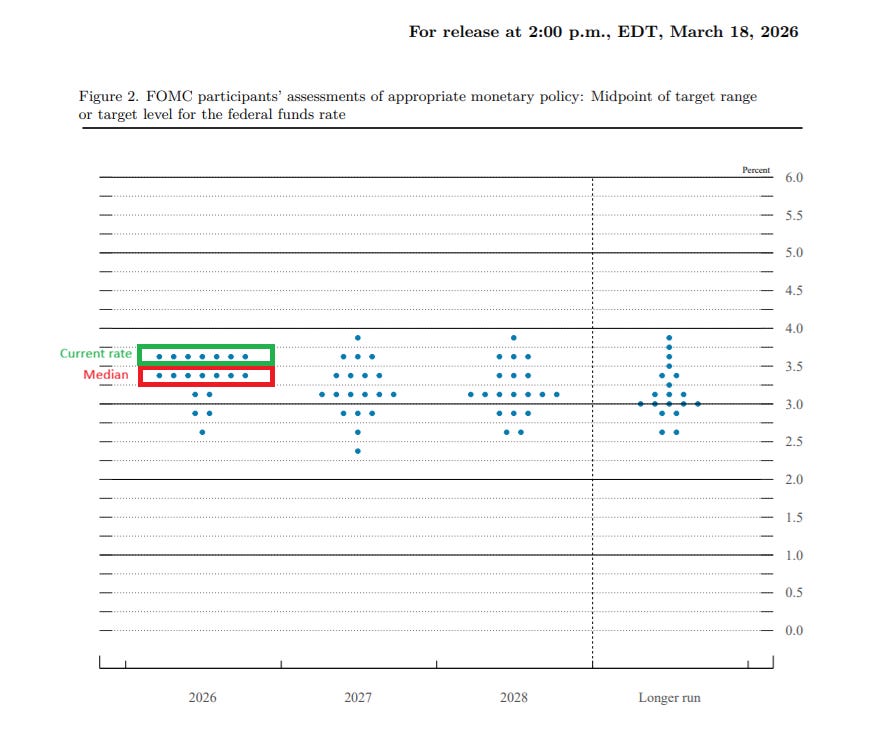

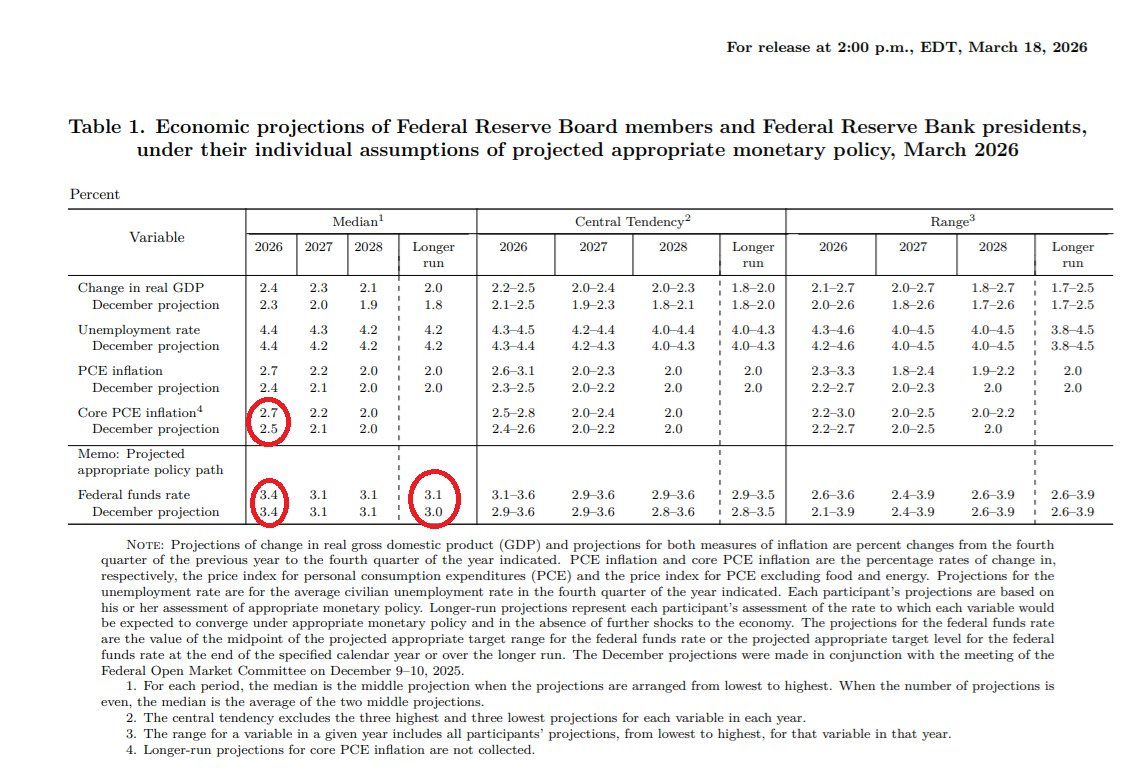

When we got the FOMC decision, markets were still pricing in a rate cut for 2026.

Furthermore, the Fed's dot plots also predicted one more rate cut this year.

However, by the end of the week, the rate cut was reversed into a rate hike as yields surged and markets feared prolonged disruption.

Digging deeper, once again, the surprise was further moved up in the longer run rate, aka the neutral rate, to 3.1% from 3%.

We have been demonstrating how the Fed has been quietly moving up the long-run rate since the last two years suggesting that we are never returning to the 2% inflation again (structural rise in inflation).

The Core PCE projections were raised by 20 bps to 2.7%, likely factoring in higher energy prices.

Last week, we mentioned that JayPo will be concerned by the inflation expectations. He commented:

“Near-term measures of inflation expectations have risen in recent weeks, likely reflecting the substantial rise in oil prices caused by supply disruptions in the Middle East.”

Unsurprisingly, JayPo has been watching Mr Market, which has been ruthless in raising the 1Y Inflation expectations to more than 5%.

Interestingly, he also mentioned that the rollout of AI is “inflationary”, leading to a higher neutral rate (came as a surprise to us, given the narrative that AI will lead to productivity gains that are deflationary).

“So, remember, in the short-term what’s happening is we’re building data centers everywhere.

And that’s actually putting pressure on all kinds of goods and services that go into building these things.

So that’s actually probably pushing inflation up at the margin. In addition, it probably raises the neutral rate.”

The rationale behind one rate cut in the projections was explained:

“We also think it’s important though to keep policy either mildly restrictive, or close to that. But not too restrictive because of the weakness in -- the downside risk in the labor market.”

In the last few months, JayPo has been discussing a new inflation measure, “Core PCE Ex-Tariffs,” as the Fed believes tariff-led goods inflation is “transitory”.

Note that last week we highlighted the segments (recreational goods, apparel, etc.) affected by tariffs, leading to a surge in prices.

This week, we further got insights from JayPo:

“Total core inflation, it’s about 3 %, and some big chunk of that, between a half and three-quarters is actually tariffs, so we’re looking for progress on that.”

While we believe most of the pass-through is complete, skyrocketing oil prices will further stoke inflation, albeit with a 2-3 quarter lag.

Last week, we also mentioned that we can’t comment on the macro outlook until we are sure about how long the war will last and how much supply disruption we will face across sectors.

We had JayPo mentioning the same this week.

“If we have a long period of much higher gas prices, that’s going to weigh on consumption, that will weigh on disposable personal income, and it’ll weigh on consumption. But we don’t know if that’s going to happen, it -- something quite different from that, we might have much lower than expected pass-through”.

It’s just, we don’t know what the effects of this will be, and really, no one does.

It’ll come down to how long the current situation lasts, and then what are the effects on prices and then how do consumers react and that kind of thing.

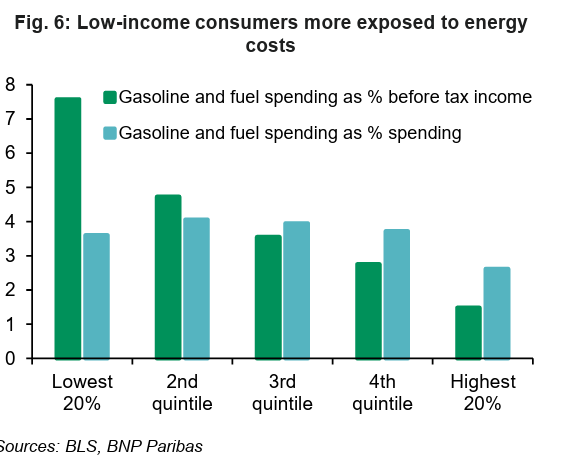

Note that gasoline and diesel prices have skyrocketed by more than 35%, which will squeeze households, especially lower-income households.

Nevertheless, if the disruption is short-lived, we might see a few months of lower consumption (also keep in mind that higher tax refunds might cushion some of the hit).