Pandora's Box!

“Women, Life, Freedom, that is the future of peace. And I have no doubt that we will realise that future together – a lot sooner than people think. I know and I believe we will transform the Middle East into a beacon of prosperity, progress and peace.”- Benjamin Netanyahu, 12th December 2024.

After crippling the terror infrastructure of Iranian proxies across Lebanon and Syria, six months ago Bibi (Netanyahu) appealed to Iranian citizens that one day Iran will be free.

Since that day, we have consistently written and warned our paid subscribers that Bibi was determined to achieve his objective of regime change (also an angle of domestic politics here).

Thus, we can’t ignore a single word that comes out of Bibi’s mouth (he is not TACO!).

As Israel opens the Pandora’s box, the move will have dire consequences for the asset classes, as Khamenei won’t give in easily despite significant blows to the top military leadership in the last 48 hours.

Today, we will discuss the strategy Israel is using and use scenario analysis to determine the probabilities and predict the performance of the asset classes. (scroll down to Section 2)

Ex-Oil and Gold, markets had a muted response to the conflict; we expect significant moves in the coming days.

On the other hand, macro data continues to deteriorate/soften across the developed world.

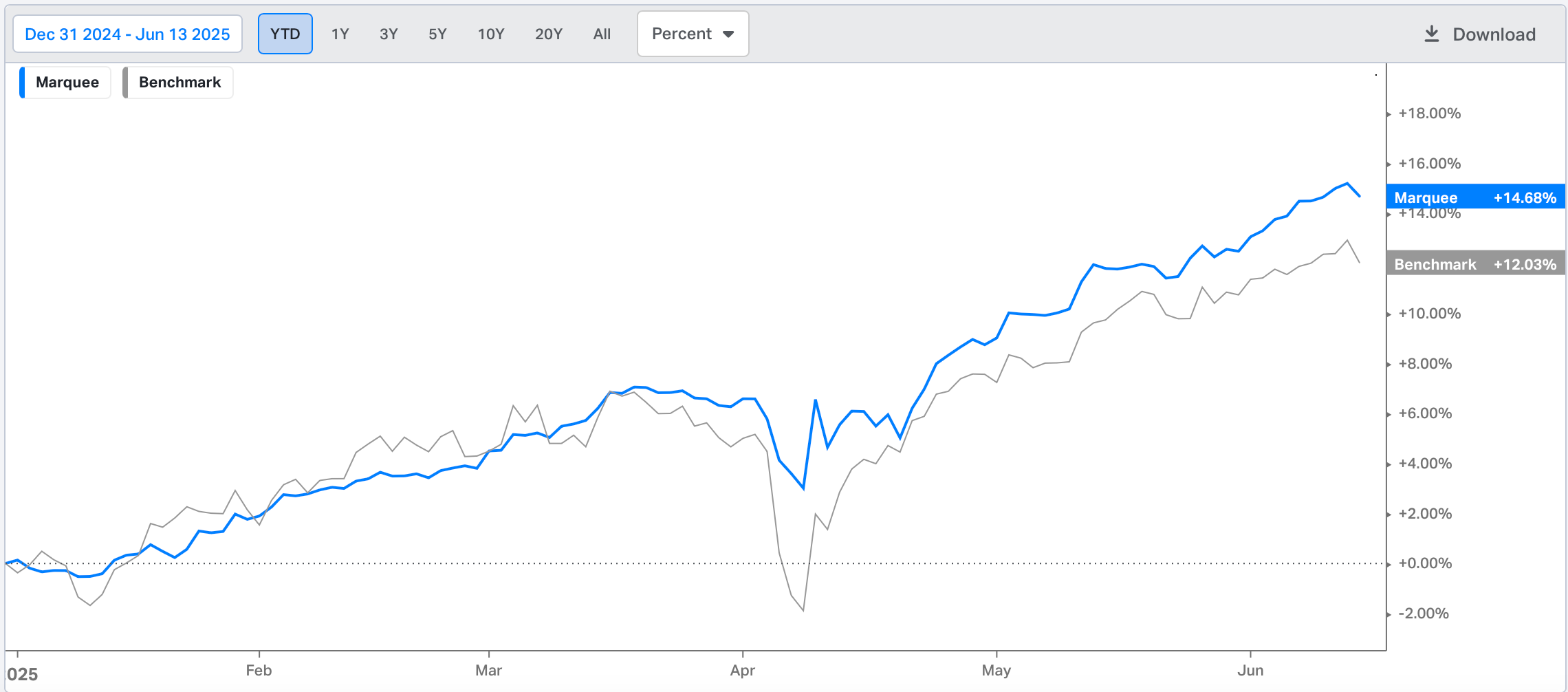

We continue to outperform the benchmark with a 14.68% YTD gain, outpacing its 12.03% performance by 250 bps.

Let us begin today’s newsletter and explore the geopolitical developments, along with some intriguing macroeconomic data.

US/FX/Gold/Oil!

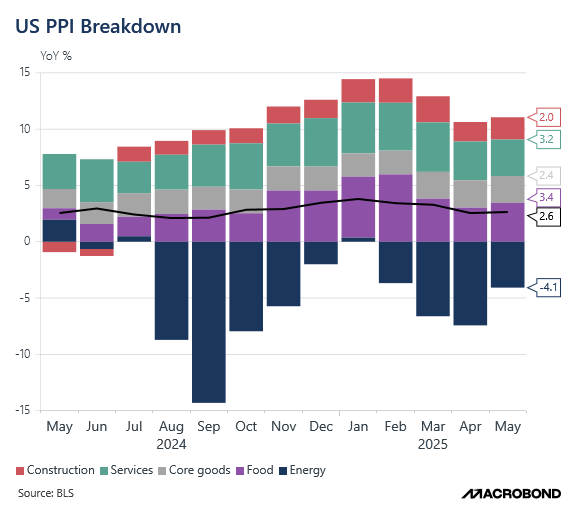

Let’s begin with the Producer Price Index (PPI), which came in softer than expected at 0.1% MoM versus the expected 0.2%.

The biggest drag was the energy component, which declined by 4.1% YoY. Interestingly, due to lower crude prices, energy deflation has been a significant contributor, pushing both the CPI and the PPI down.

Nonetheless, the revisions were stark, as the March and April PPI were revised upwards by 40 bps and 30 bps, respectively.

So, we will not be surprised if the May number is revised upwards and the “soft” number isn’t so soft after all.

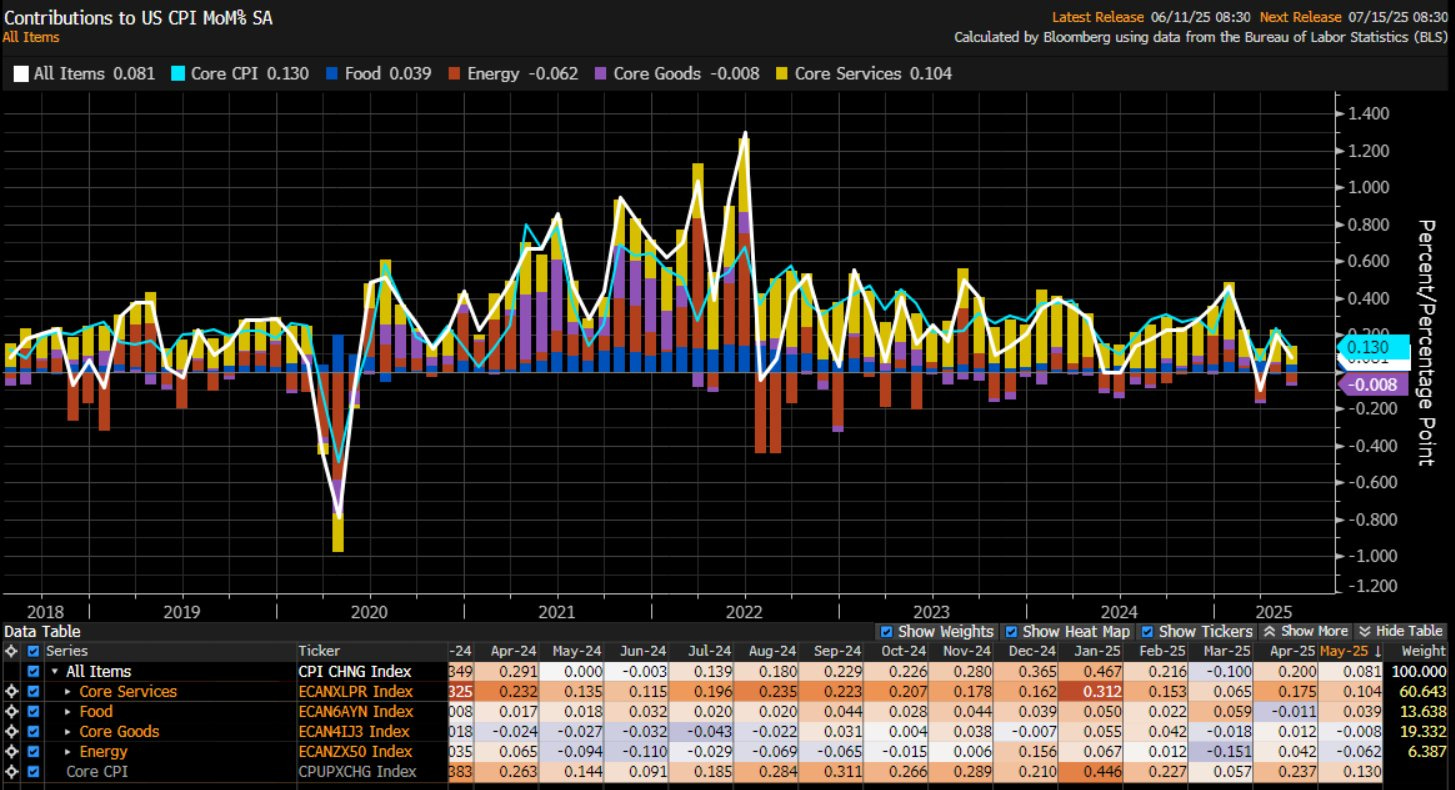

Moving on, the CPI also came in softer than expectations at 0.1% MoM v/s 0.2% expected. Core CPI came in significantly below expectations (0.3%) at 0.1% MoM.

The culprit was the core goods, which sprung into deflation with a -0.008% MoM print, surprising most market participants as everybody expected a higher number due to the tariffs pass through.

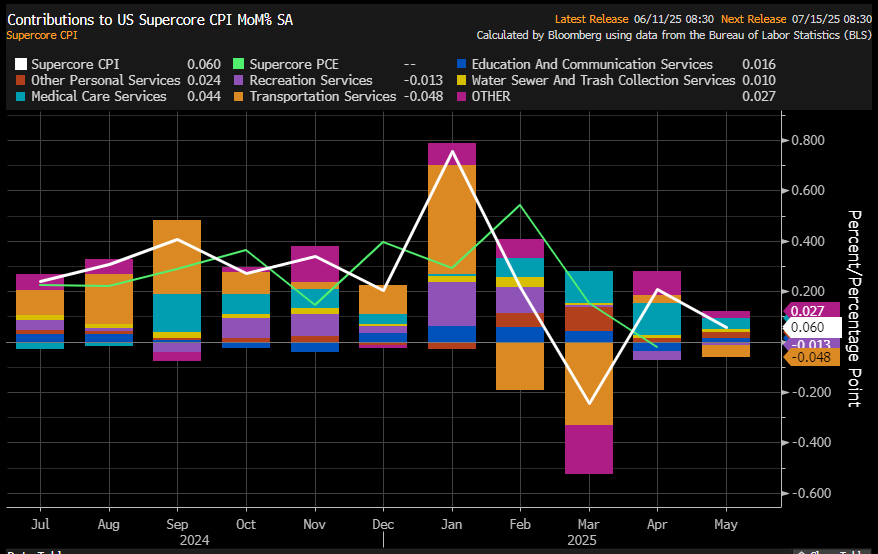

The sticky Supercore CPI (Services Ex-Housing) also cooled down significantly, with transportation services dragging the index lower.

Interestingly, the trend appears to have been down since February, and no tariff impact is visible here either.

Nevertheless, the next few months are super crucial for the CPI data, as the data predicts that