Point Of No Return?

The largest banks in the world are located in the US and are responsible for moving enormous swaths of money globally.

Since these institutions are aware of the money flow, they are also very well aware of the risks to the global economy.

The world’s most powerful bank is none other than JP Morgan, and when JPM Chairman and CEO Jamie Dimon speaks, we scrutinise every word he says.

He has reiterated his chief concern across public forums in the last year or so.

On 24th September, he was in India to attend the JPM Conference, and this was the statement he made:

“ My caution is all geopolitics, which may determine the state of the economy.”

Furthermore, he mentioned:

“There's a chance for accidents in the energy supply chain. God knows if other countries get involved. You have a lot of war taking place right now.”

And guess what?

He was damn right, as we are on the brink of a significant disruption in the energy supply chain as Middle East tensions explode out of control.

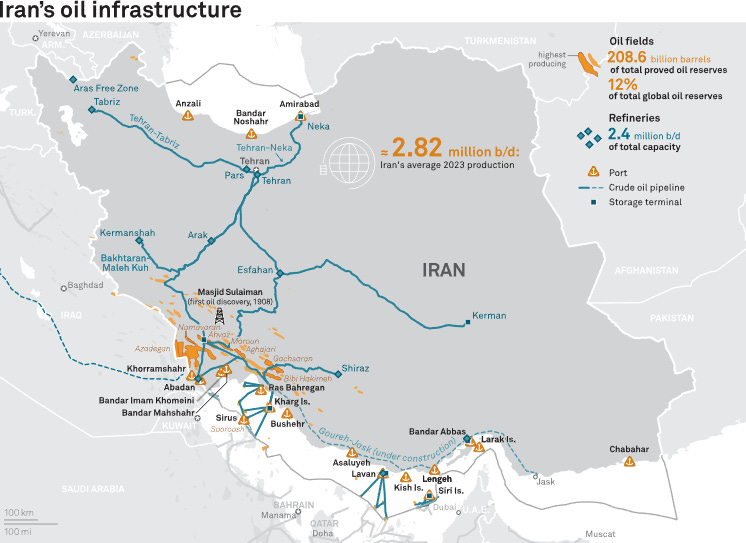

Iran stunned Israel by attacking with 100s of ballistic missiles on the critical Israeli infrastructure (defence and intelligence establishments).

As a result, Israel is now preparing to take revenge by launching an attack on the Iranian oil infrastructure, which will lead to disruptions and can not only lead to higher oil prices but sustained pricing of higher geopolitical risk premium.

Furthermore, Iranian oil infra is highly concentrated, which makes it an easy target of the superior Israeli Air Force.

Nonetheless, since US elections are less than a month away, we can expect some restraint, and Israel can target power plants and IRGC establishments to begin with.

We will discuss more later on.

Let’s begin with an in-depth analysis of the macro data released this week and how the market perceives the geopolitical situation.

US!

We began with one of our most preferred indicators to gauge the cyclical activity in the US.

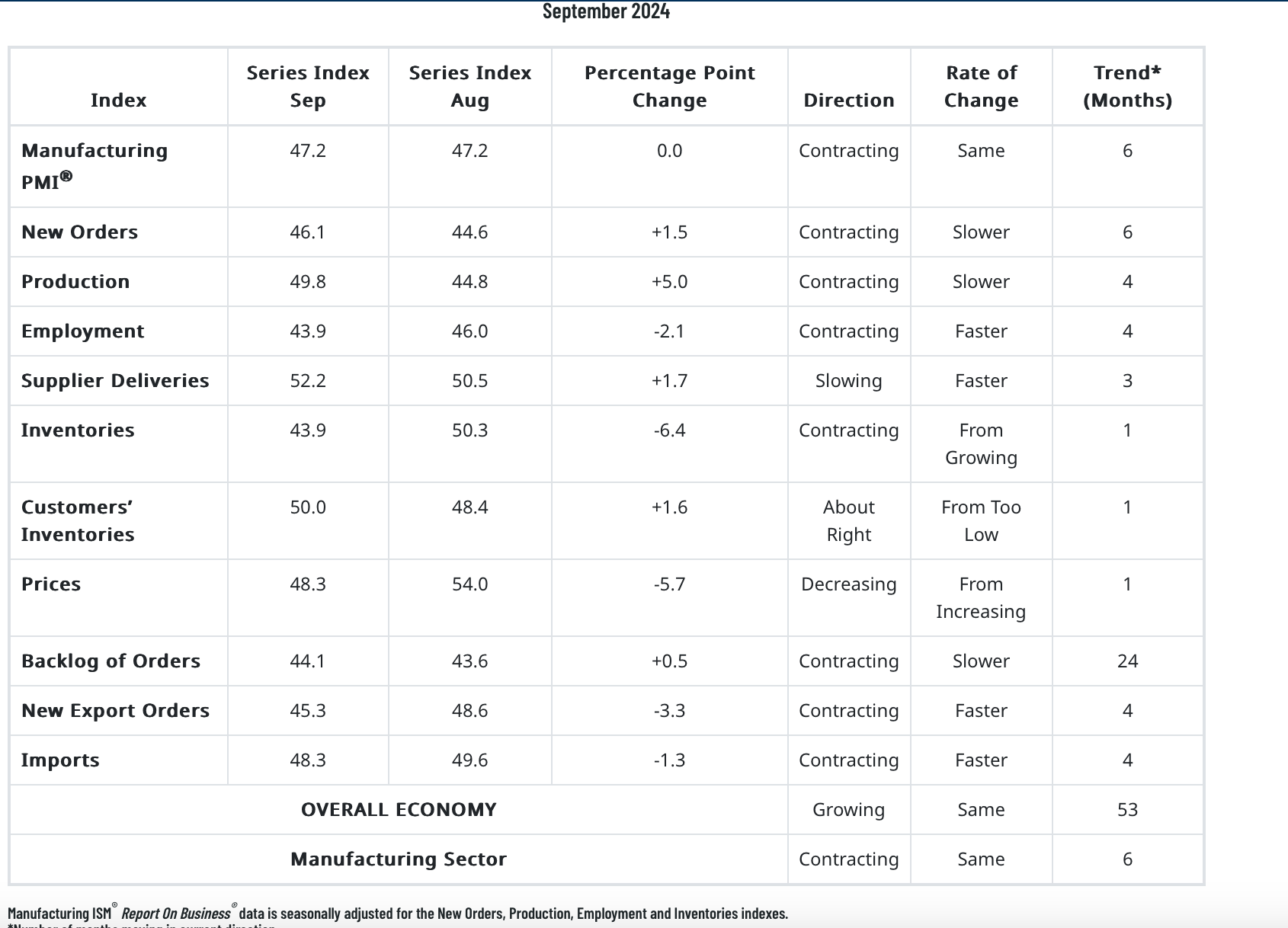

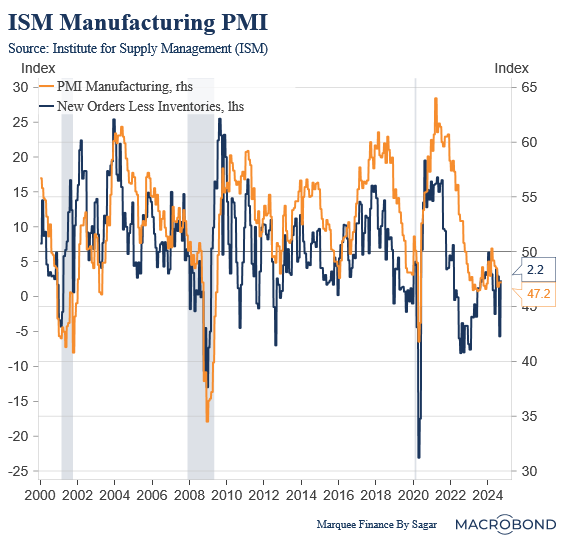

The ISM Manufacturing PMI came in line with the estimates and is still in contractionary territory.

As we can observe, New Orders recovered slightly, whereas inventories fell sharply (indicating liquidation ahead of a busy festive season).

As a result, Orders Less Inventories (which leads the PMI) recovered sharply contrary to our expectations of further fall.

It has been very volatile lately, and thus, it’s challenging to predict the trend.

We will wait for further readings to gauge the trend here, though we expect the headline index to crash to 40 eventually.

Nonetheless, the notable point remains that the Employment and Prices component has fallen to nearly 40.

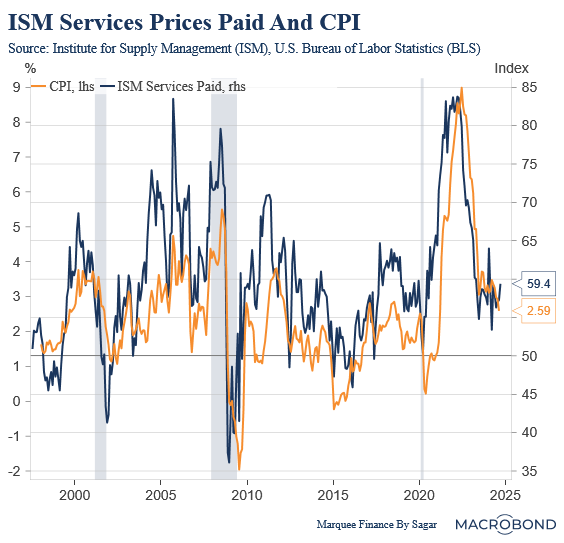

The macro surprise of the week was the ISM Services, which had a mind-boggling beat yesterday, leading to market participants calling out for a resilient economy.

Digging deeper, ISM Services Paid has a tight correlation with the CPI, and if the trend remains higher, we may see a rise in inflation in Q4 (which we predicted last month).

However, the one worrying sign in the Services PMI takes us to the..