July saw a shakeout across assets as the FX moves stunned the global financial system with unwinding in the most crowded trades of the decade: Long Big Tech and Short JPY.

In fact, the sharp reversal can be attributed to extreme positioning across various assets (FX, Mag 7, etc.), which led to enormous unwinding and, thus, rapid moves.

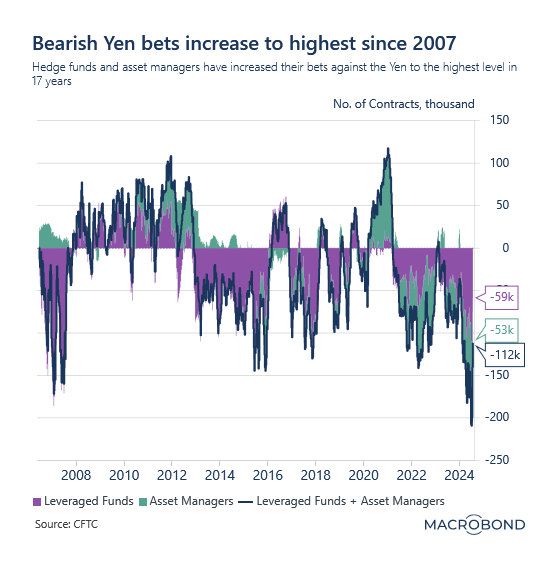

We highlighted this risk in one of our newsletters last month, where we discussed the largest bearish positioning in JPY since 2007.

As one can observe, we raised the risk of unwinding in mid-June, when the positioning was the most bearish since the GFC. However, last week's short-covering rally led to some unwinding.

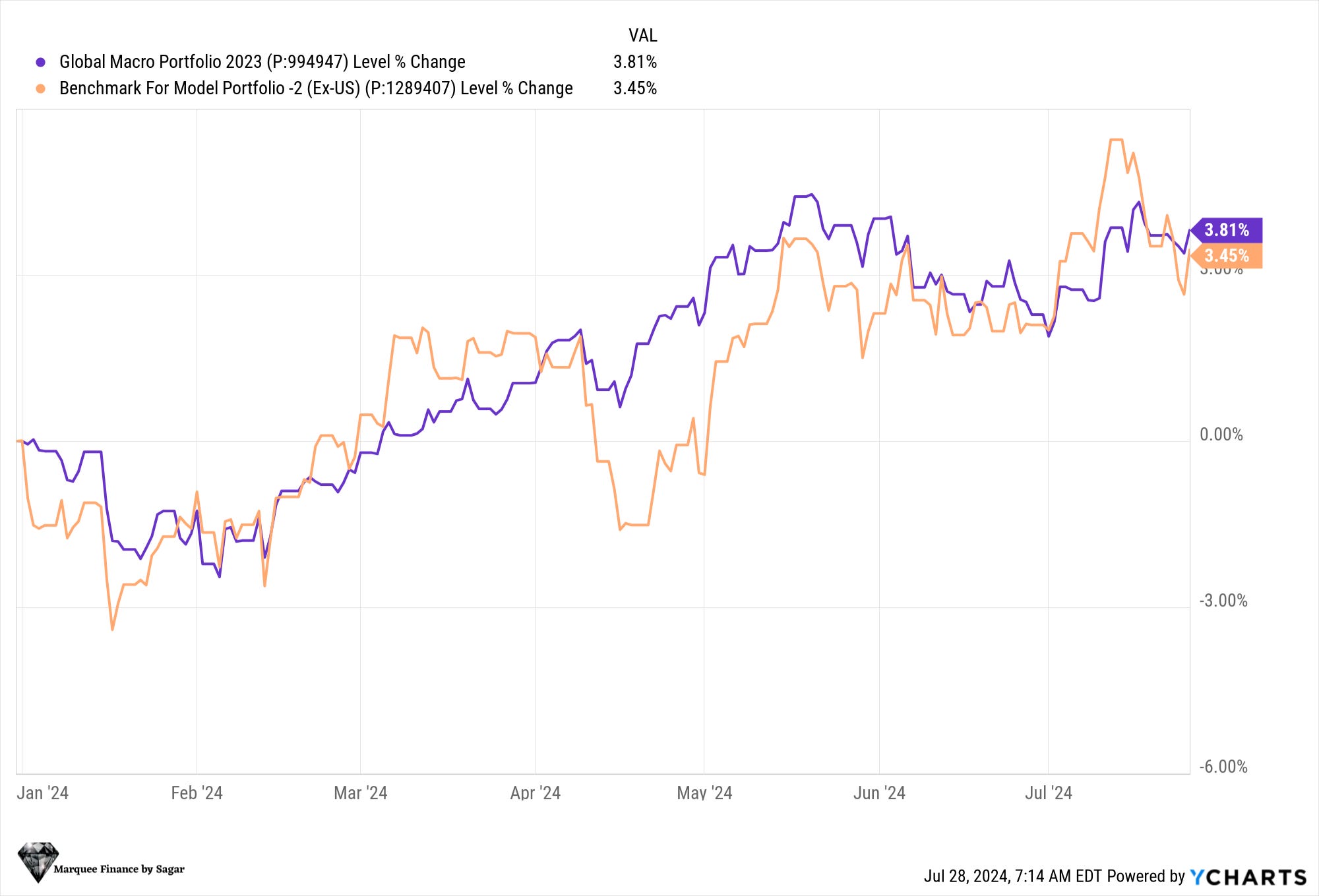

Overall, our cautious approach has led to some alpha generation despite a significant equity bubble.

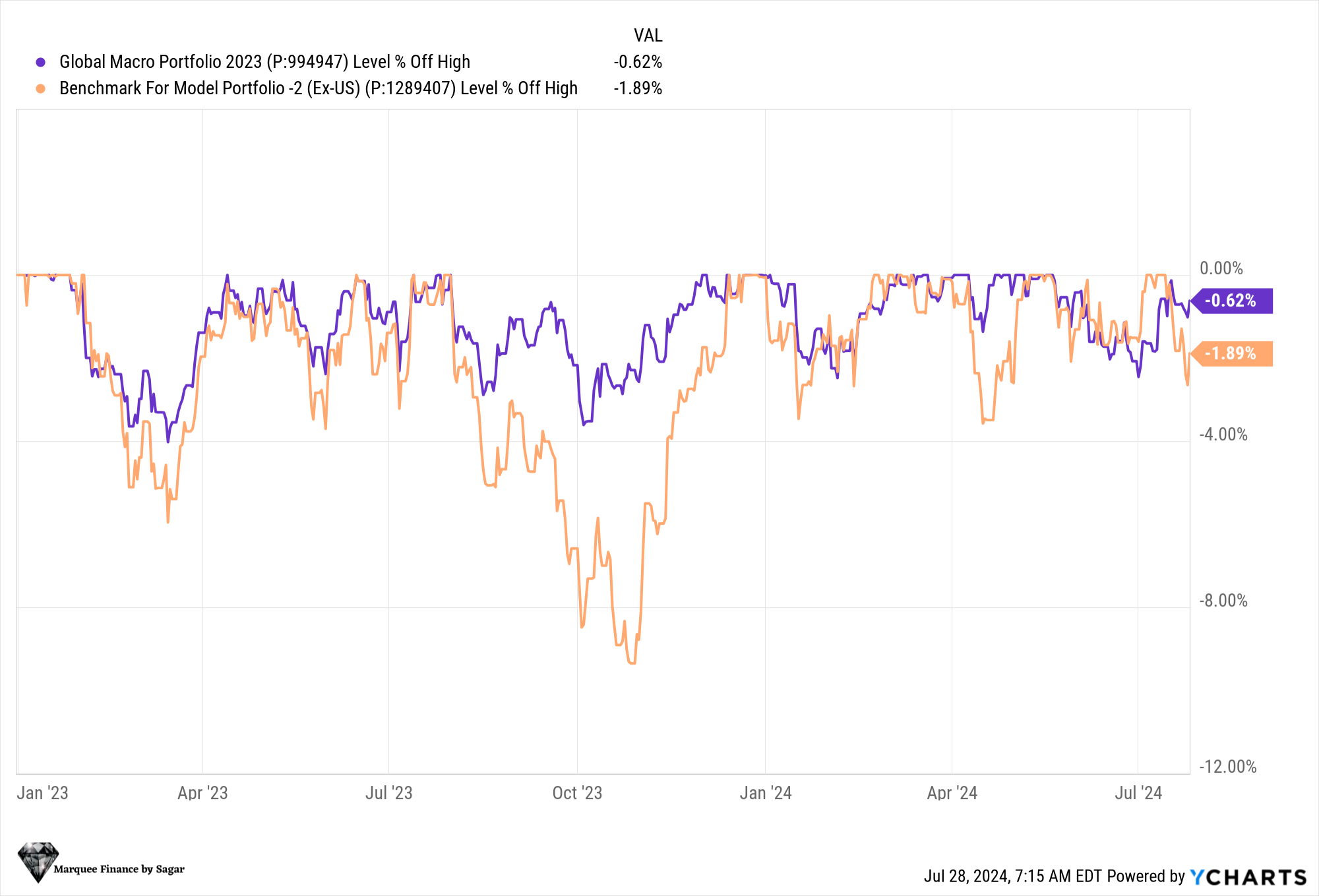

Furthermore, since inception last year, our risk management has kept drawdowns minimal compared to our benchmark, thanks to our high cash levels periodically and conservative approach.

In fact, as you can observe, our PF has never witnessed more than a 4% drawdown, even during the worst-case scenarios (SVB, last year's equity correction).

Let’s dig deeper and understand how we are positioned for a cracker H2.

Equities!

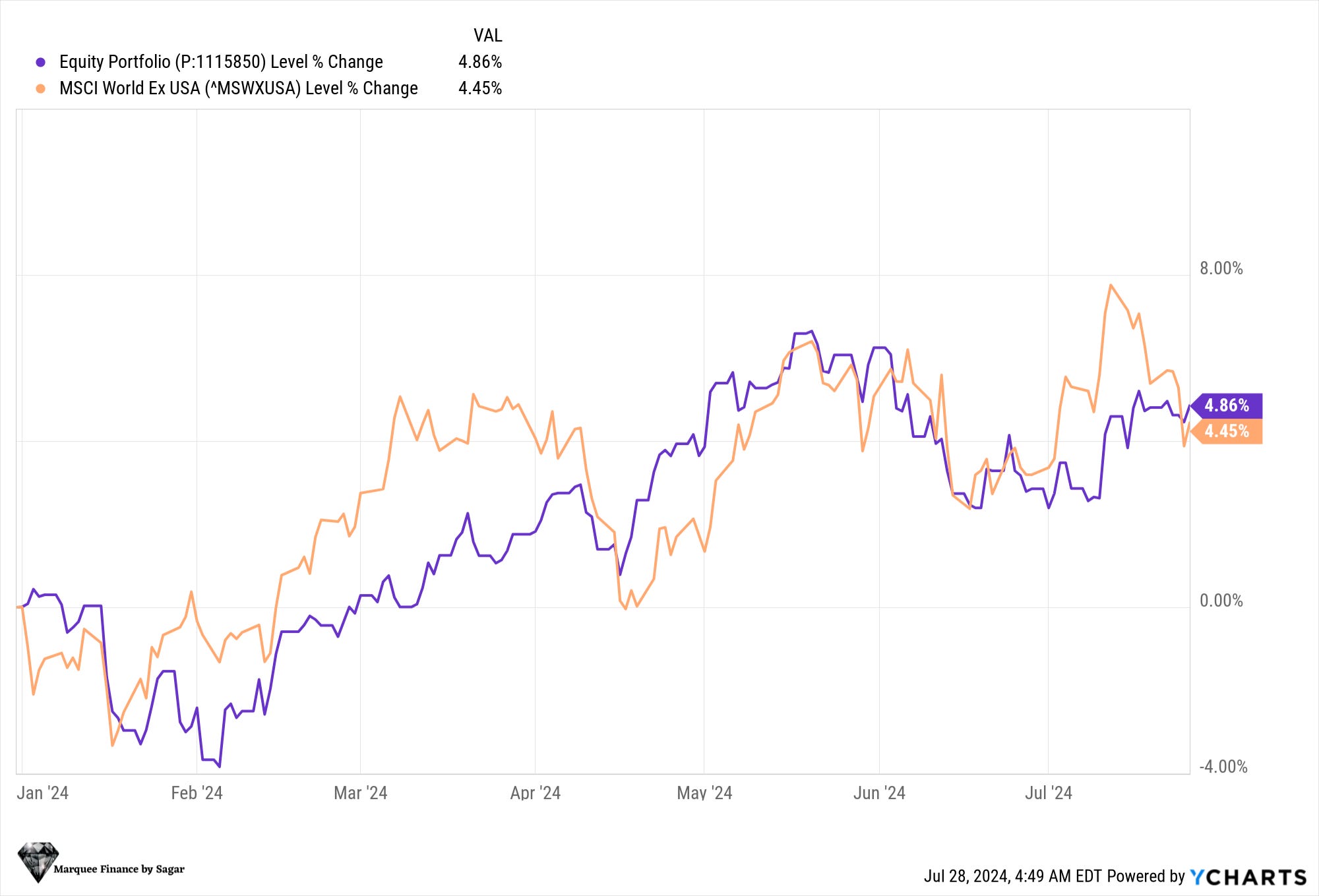

Equity performance has been in line with the benchmark performance despite our underweight stance and high cash position.

We wrote about the valuation in detail a few months ago, and we mentioned that