Before we start this week’s newsletter, our thoughts and prayers go out to the beautiful people of Venezuela. May God grant them strength to recover from the devastating disaster they experienced this week.

It has been a tumultuous H1. Undoubtedly, the volatility this year, along with the newsflow, has been treacherous and surpassed last year’s liberation day moves.

Note that the liberation day was predictable, and we entered and exited the markets at the right time last year. However, this year was way more challenging.

Nevertheless, we navigated successfully after initial hiccups.

Before we begin, we would like to highlight the multiple risks we see in the financial markets today:

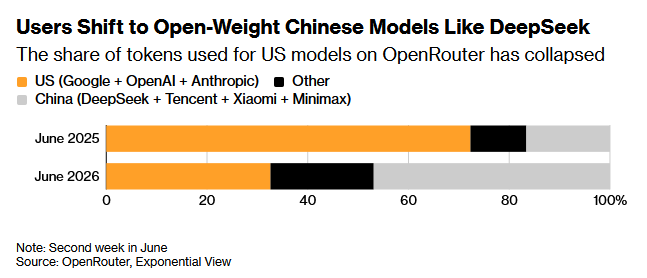

For the last few weeks, we have been raising concerns about the crumbling AI story as the token price index has fallen, and there have been no signs of the promised productivity gains, with companies burning through their annual AI budgets within months. Furthermore, the data demonstrates that the users are now shifting to “cheap” Chinese models. On OpenRouter, the share of Chinese models is now approaching more than 50%. There are also rumours that certain Chinese companies are selling the Claude tokens at a 70-80% discount.

There have been rumours about OpenAI delaying the IPO as US markets crack post the giant liquidity-sucking SpaceX IPO. Furthermore, the US government has taken steps to prevent the release of the most advanced models. The Fable 5 fiasco and the latest news about ChatGPT create an uncertain environment and pose a risk to the AI story.

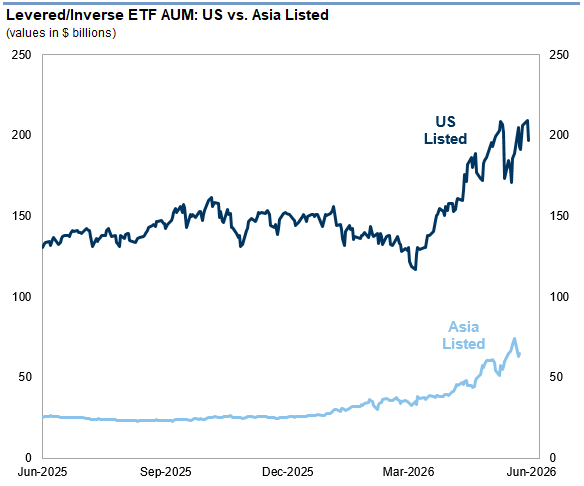

The earlier episodes of euphoria and bubbles were characterised by an explosion in the margin debt. However, this cycle is different, as leveraged ETFs have replaced margin debt. While Levered/Inverse ETF AUM in the US has doubled since the March 26 lows, growth in Asia has been astounding, with the launch of the world’s largest single-stock levered ETF (SK HYNIX). The rebalancing of ETFs amid elevated volatility is one risk we can’t ignore.

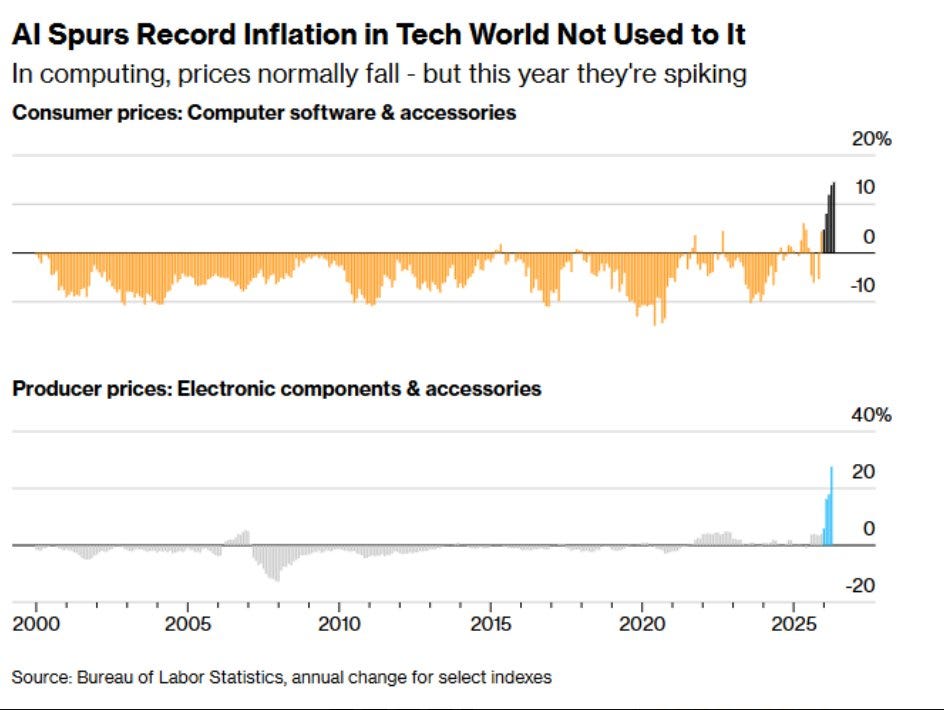

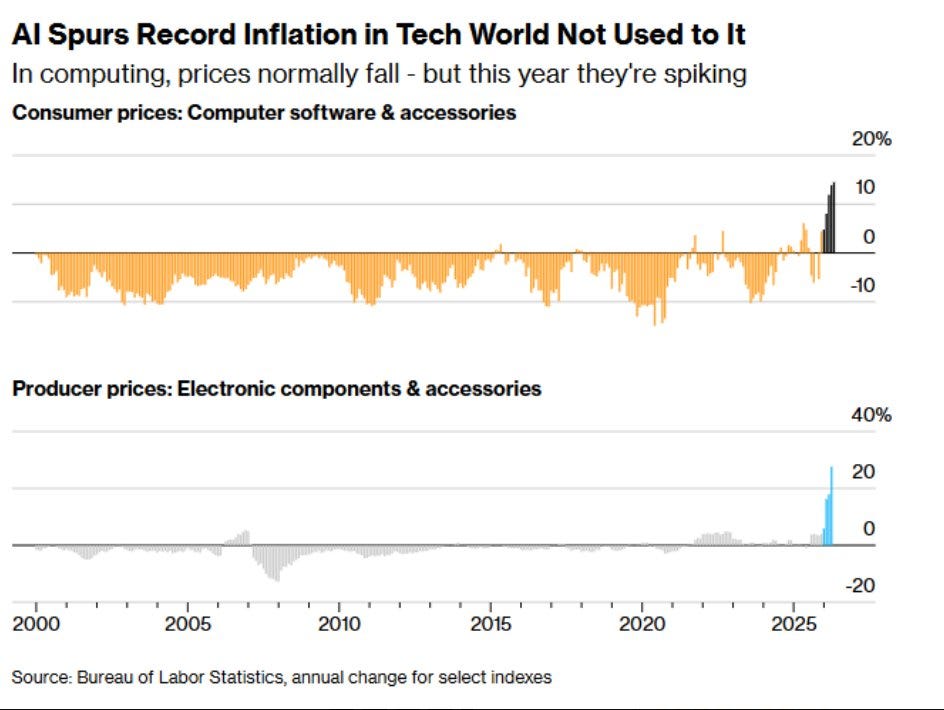

With data centres and trillions of dollars in hyperscaler capex sucking up all the available memory (DRAM/NAND) on the planet, manufacturers of computer accessories are feeling the heat. As memory prices rose by 80% within months, AAPL and MSFT raised their product prices this week. While we were of the view that inflation might peak as oil prices fell more than 40% from their highs, sustained “memory inflation” might keep prices buoyant and thus maintain the Fed's hawkish stance.

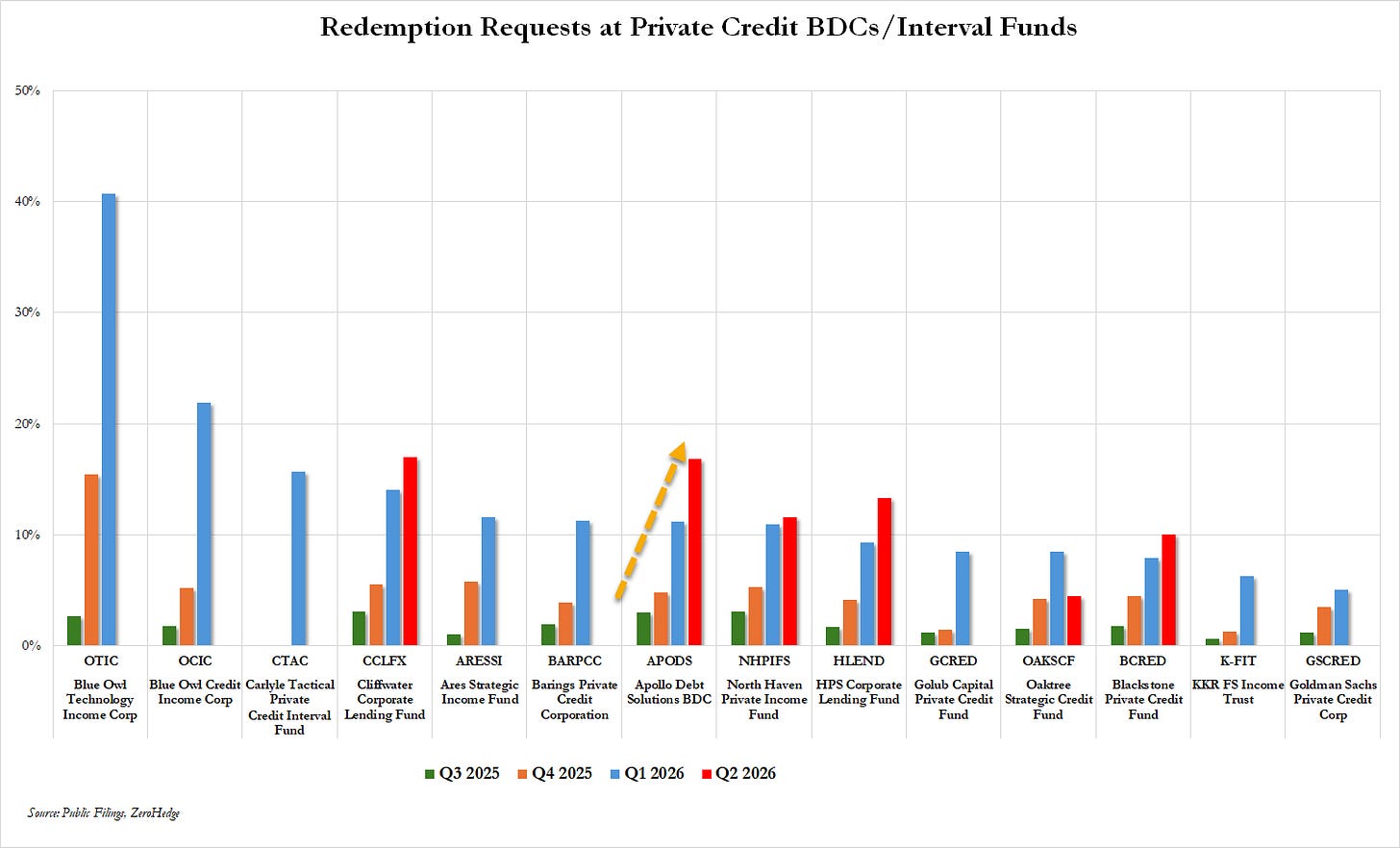

The last one, overshadowed by geopolitical headlines, is the ongoing turmoil in the Private Credit sector. We got another shocker this week as Apollo capped their redemptions. If the problems compound in the illiquid private credit space, it could create ripples across assets. Nonetheless, we don’t believe there will be a systemic crisis similar to the GFC, as banks are well capitalised.

Source: ZH

These were some of the risks that we believe are worth looking at and can lead to dislocation in the financial markets, as the markets (equity and debt) have been riding only on the AI theme, with the most vulnerable sector leading the equity rally in the past few months.

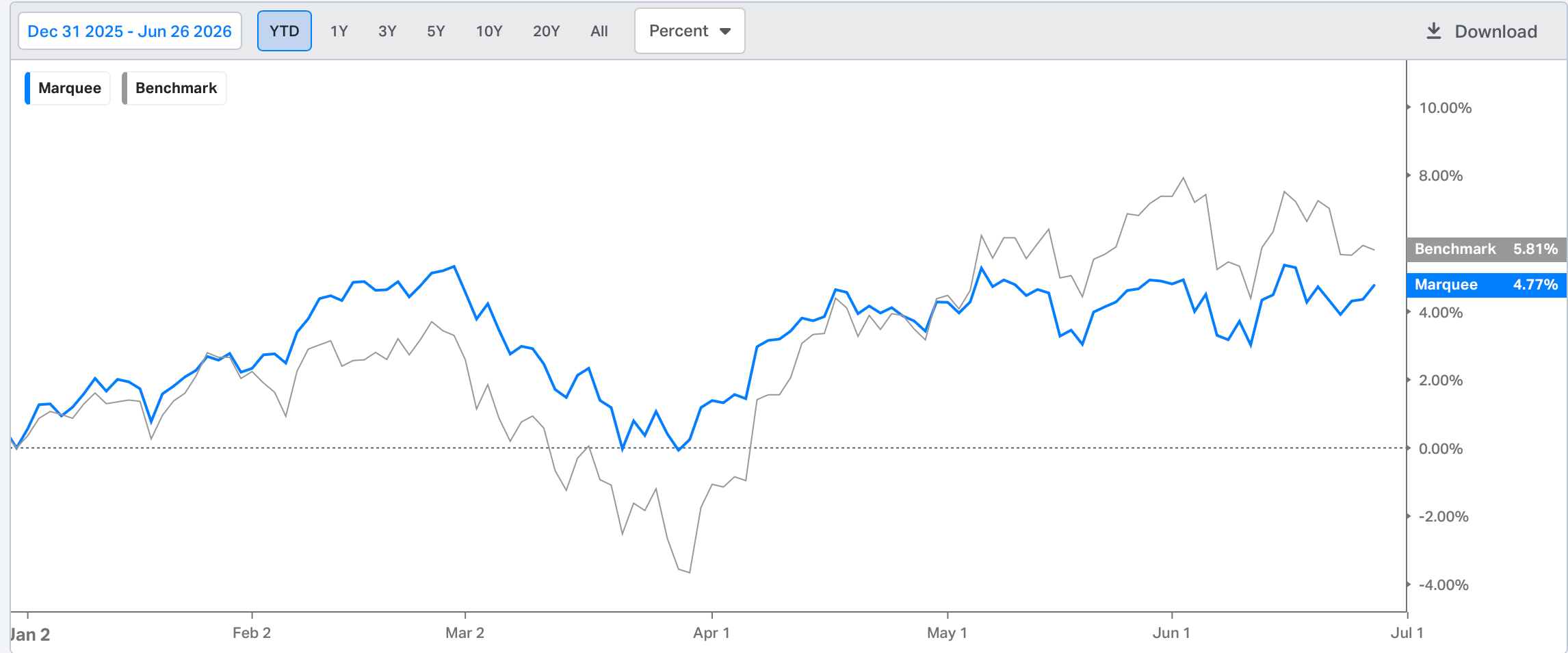

We narrowed the gap with the benchmark and are happy to be at 5% YTD returns, considering the turbulent H1.

The underperformance has now reduced from 250 bps to 100 bps.

Furthermore, as we have been communicating, our underperformance is due to only two reasons:

The shallow global equity rally led by only a few semi names.

Chinese underperformance.

While nature has been healing with respect to the first, we expect the second to heal as well over time.

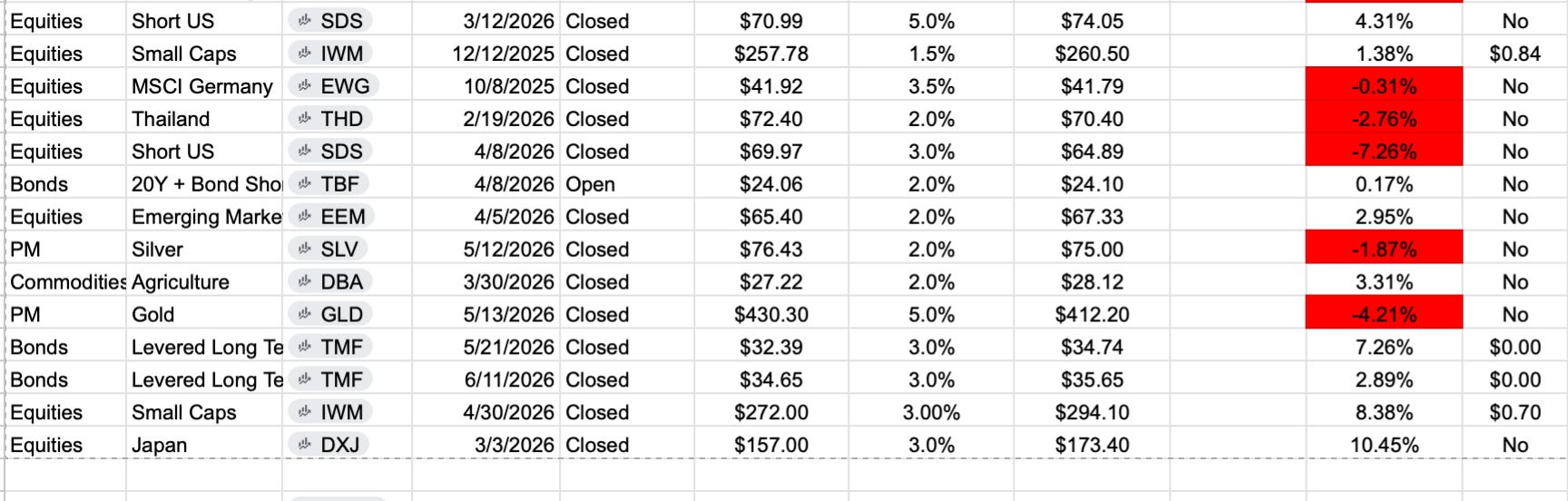

Before we move ahead, as the customary tradition (at the end of H1), we would like to present the trades that we undertook since December and have closed them.

Total trades were considerably less due to elevated volatility. We undertook 14 trades (closed, many are still open), out of which 65% resulted in profits (hit ratio).

We heavily deployed cash in the last week of April and also nailed the bond rally twice (TMF trades).

Let’s do a deep dive into the macro universe and analyse the cross-asset price action.

Macro!

We began with the most important data release of the week.

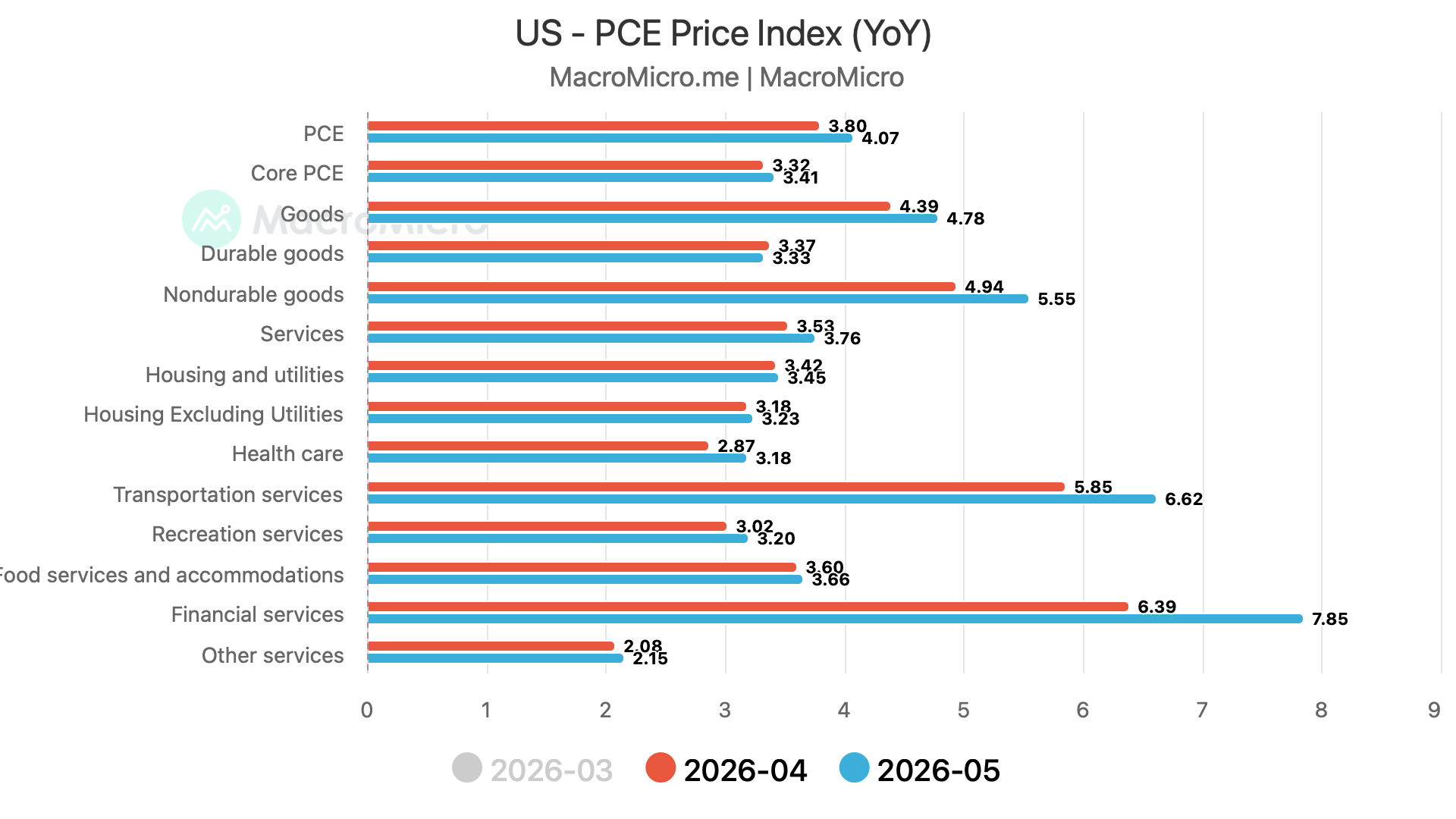

The Fed’s preferred inflation gauge, the PCE, came slightly softer than expectations.

The headline PCE came in at 0.4% MoM v/s exp 0.5% MoM.

The core PCE came in line with expectations at 0.3% MoM.

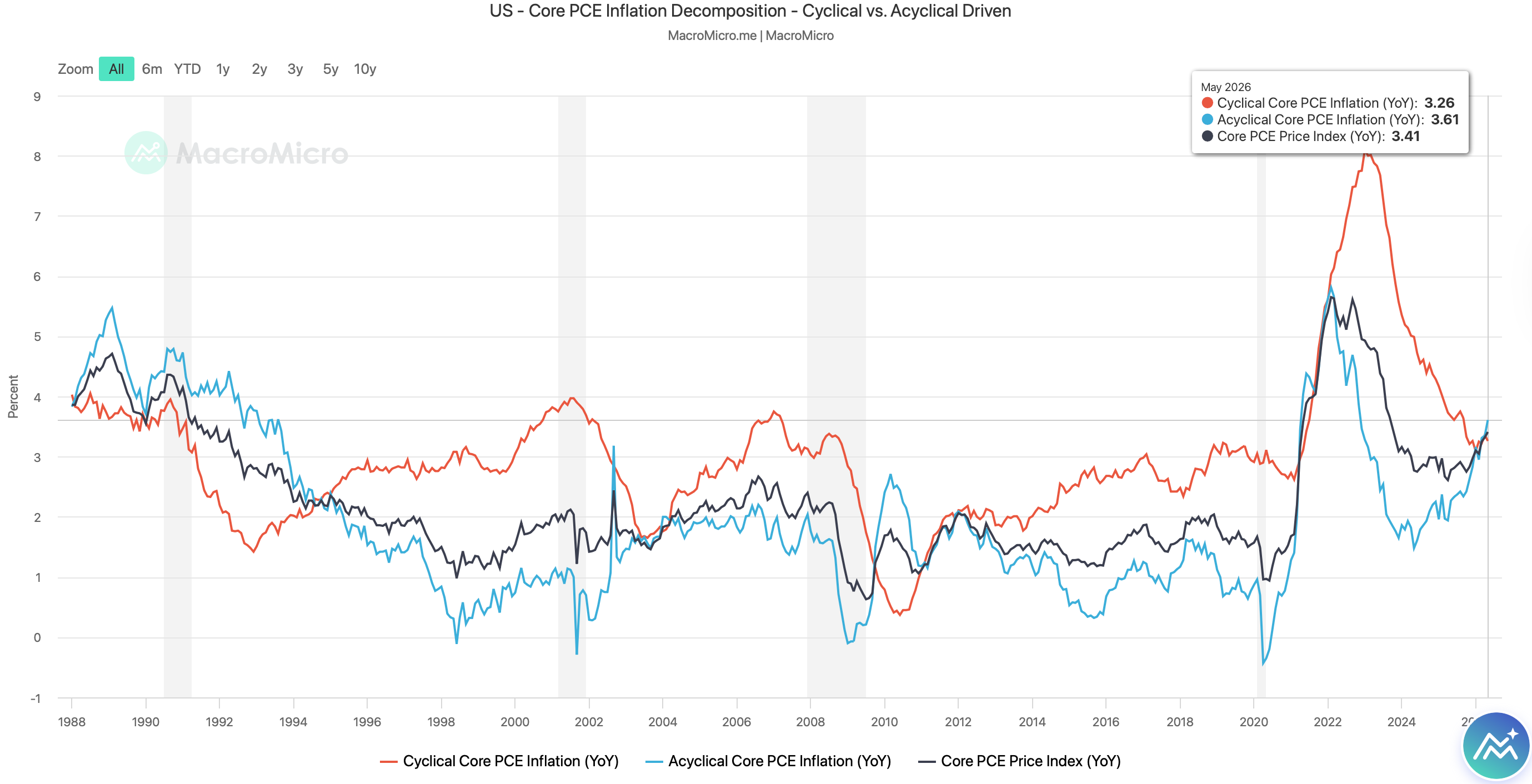

We can decompose the PCE into the Cyclical Core and the Acyclical Core PCE(depending on the item’s sensitivity to the business cycle).

Both the cyclical and acyclical PCE have been trending upward.

In fact, the Acyclical core PCE (financial services, clothing, healthcare, etc.) rose to its highest level since 2022, indicating that “services” inflation is sticky.

When we dig deeper, the financial services (thanks to higher equity markets) for the second month in a row is putting significant upward pressure on the PCE.

Overall, it was a broad-based rise.

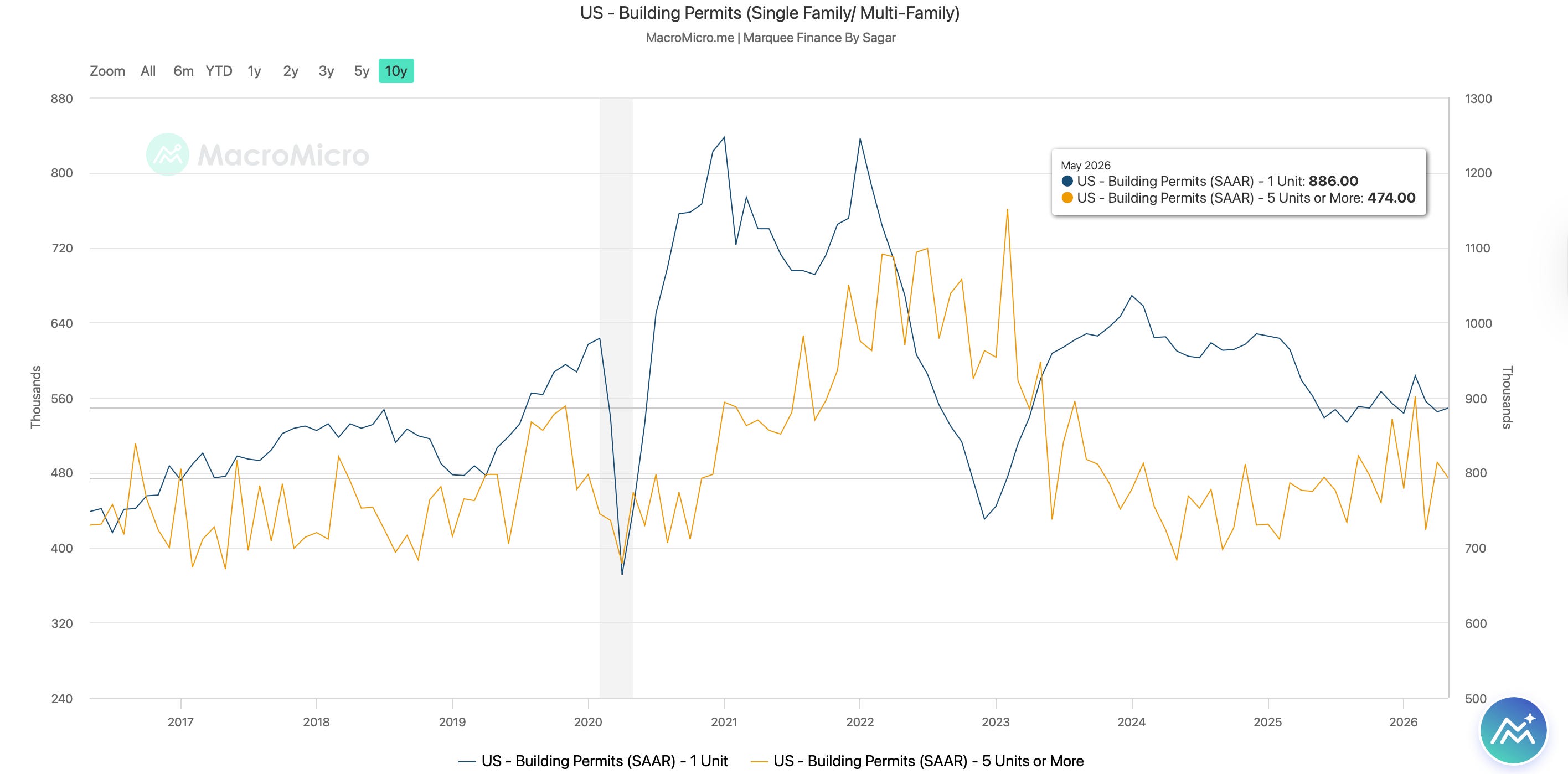

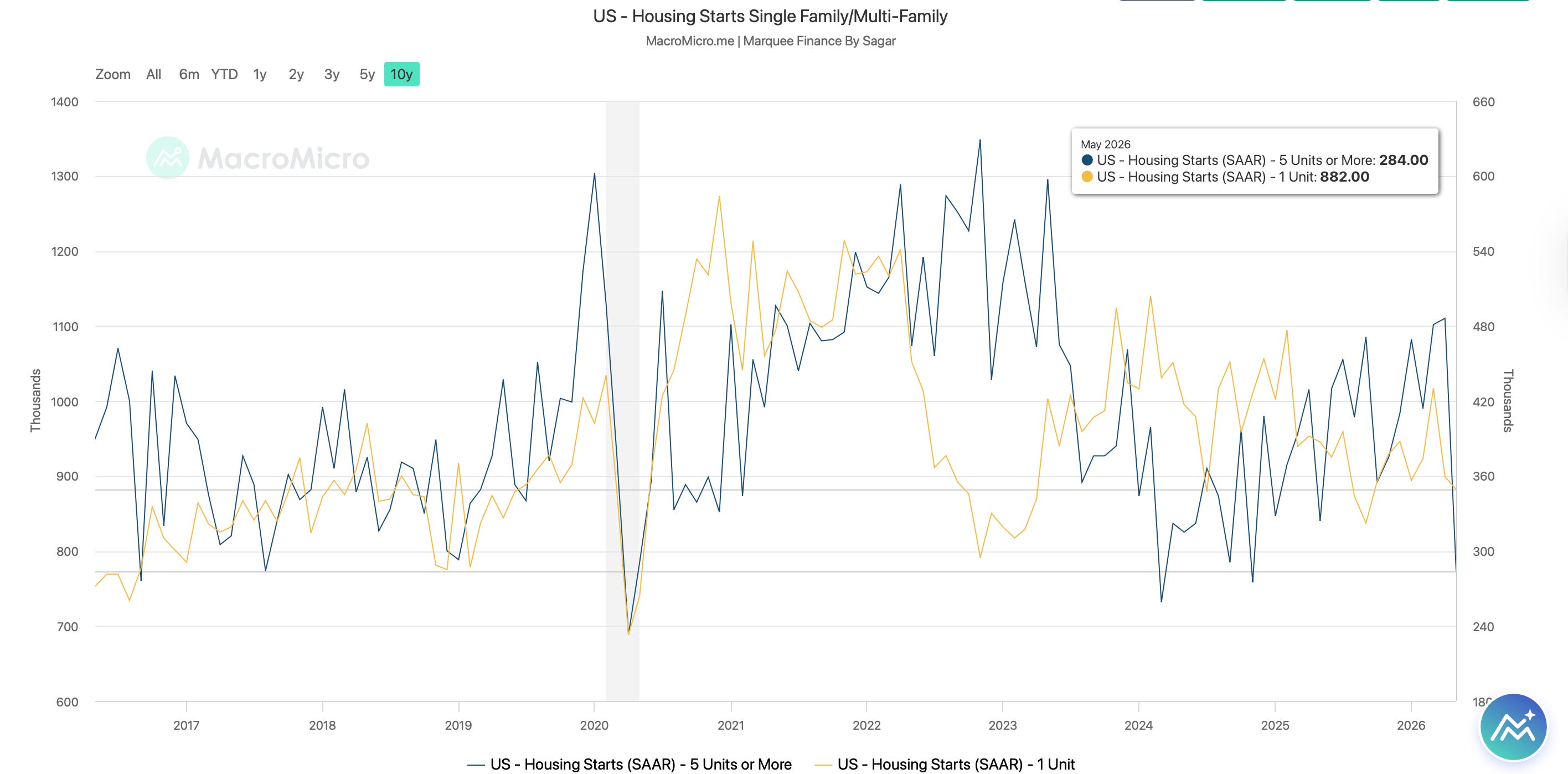

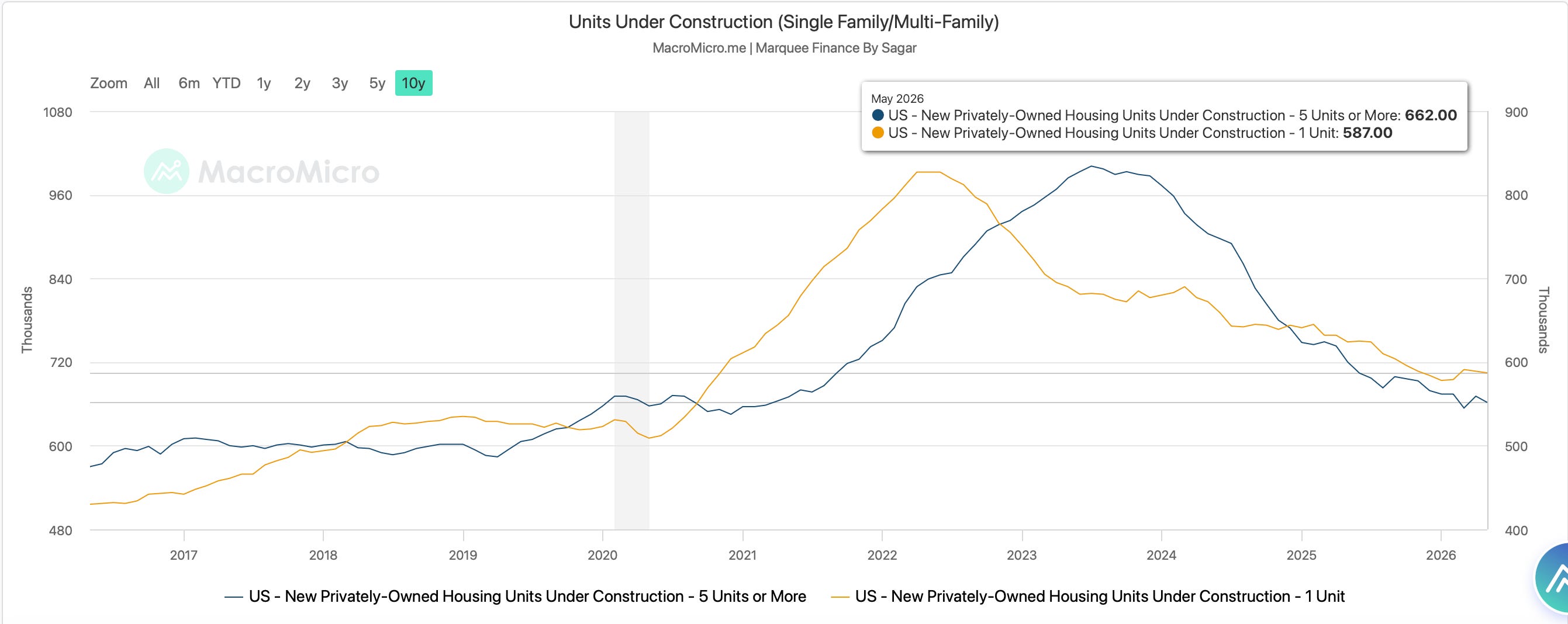

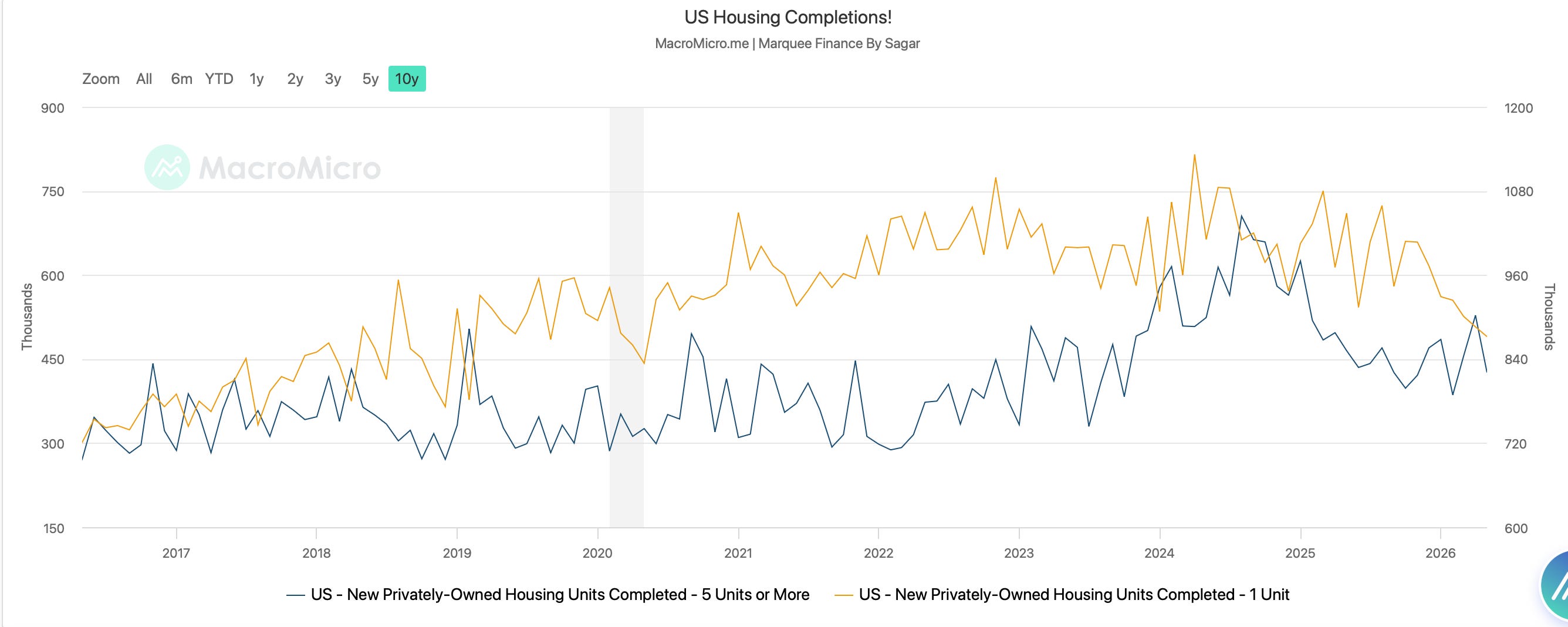

After a long time, we also want to update on the Housing Cycle in the US. As macro watchers, we are big believers in business cycles, and thus, the foundation lies in the housing cycle.

Housing is: Permits→ Starts→ Units Under Construction→ Completions.

This is roughly a 24-36-month cycle, depending on whether it's single-family or multifamily housing.

Post-COVID, we saw institutional capital flooding the multifamily housing sector, which led to an unprecedented boom in housing.

With JayPo's rise in interest rates in 2022, single-family housing was the first to suffer, as it was highly impacted.

As we can see, permits for single-family housing have yet to recover and remain below pre-COVID levels.

On the other hand, multifamily housing seems to have bottomed out, and any recovery will first be visible in higher permit activity.

With the backlog cleared and permits stagnant, Starts for Multifamily plunged to one of the lowest levels (another reason was higher costs due to the war).

The 2023/2024 period was marked by a “housing recession” as activity slowed considerably. As a result, Units under construction have collapsed by 35-40%.

While the activity has stabilised, there are no signs of any pick-up.

The Housing cycle’s most critical component after home sales is employment.

The higher the completions and the more the backlog reduces (as units under construction fall), the more layoffs there are across the housing sector.

Completions have hit a multi-year low in single-family housing, while multifamily saw a bump but remains stagnant at current levels.

The activity in the housing sector, which seemed to have bottomed out pre-war, is still sluggish.

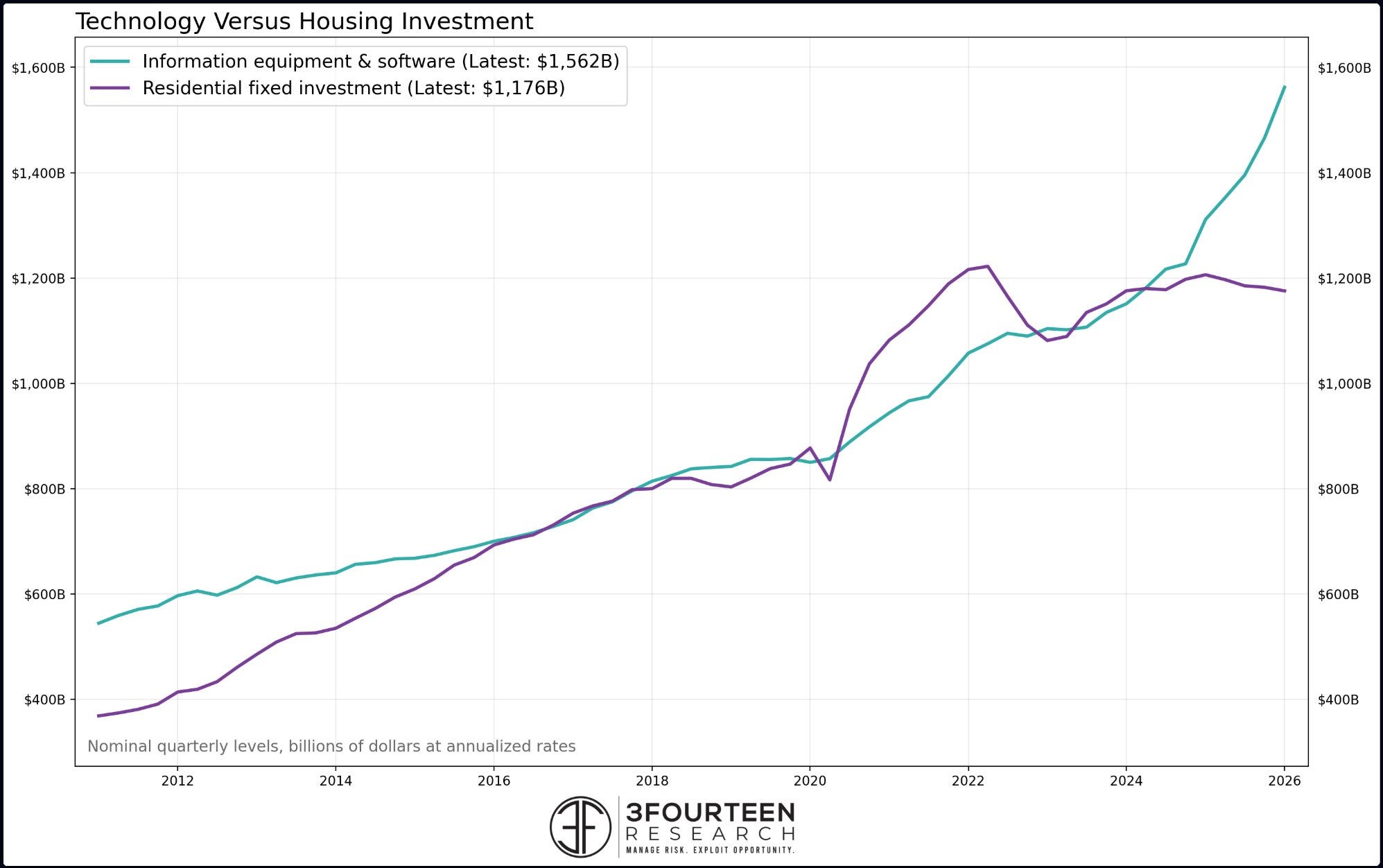

In fact, if we compare the absolute numbers, residential fixed investment is $1.176 billion, below the 2022 peak. The mind-boggling hyperscaler capex has led to information equipment &software investment surpassing the residential fixed investment by an enormous margin.

However, we believe that if the US economy continues to fire, the housing cycle will revive. We remain optimistic about a housing recovery.

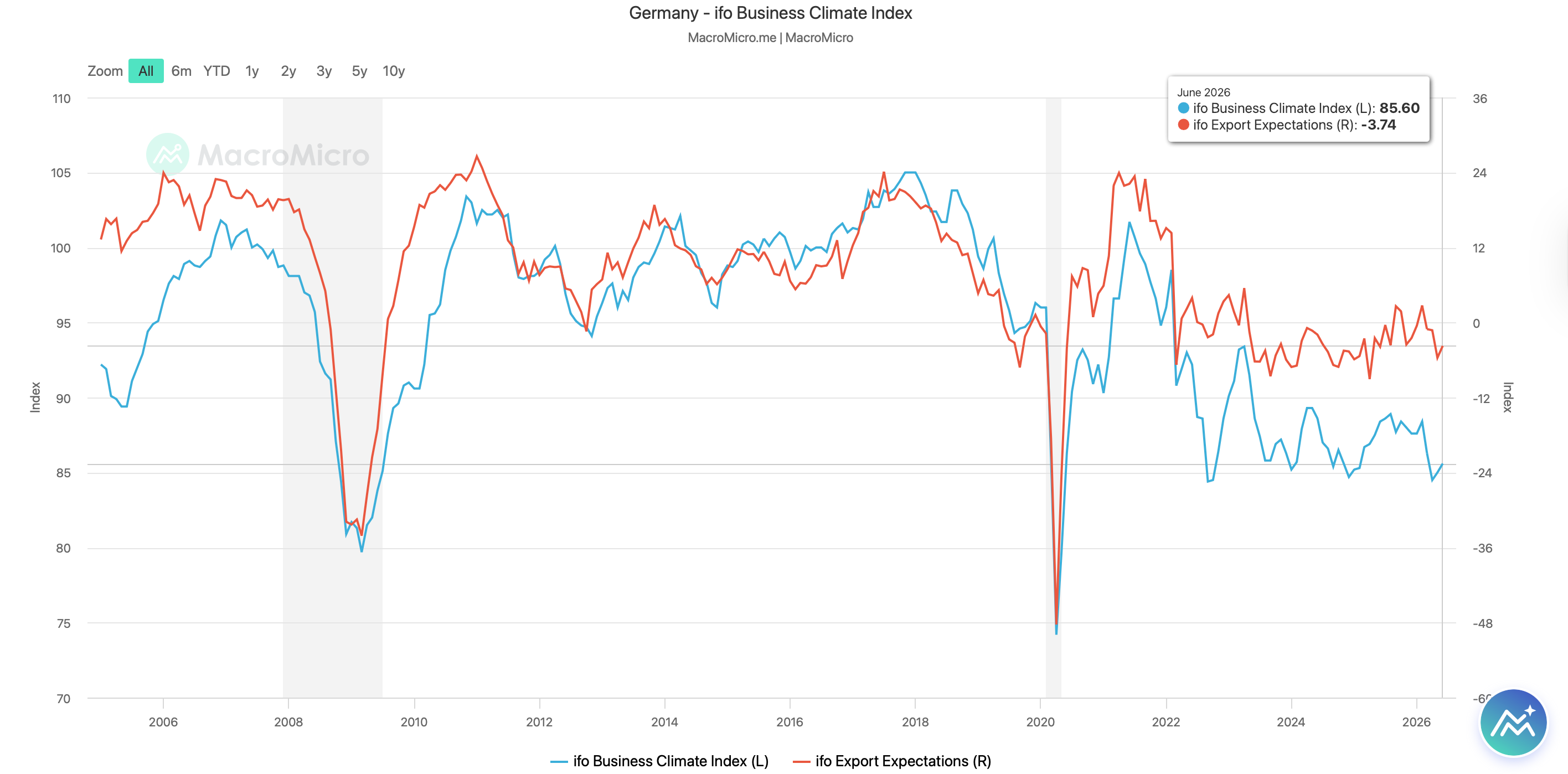

In Germany, the IFO business climate index, which plunged post the geopolitical developments in the Middle East, recovered slightly.

As commodity prices fall sharply, we expect soft data to rebound swiftly, as transpired after the 2022 crisis.

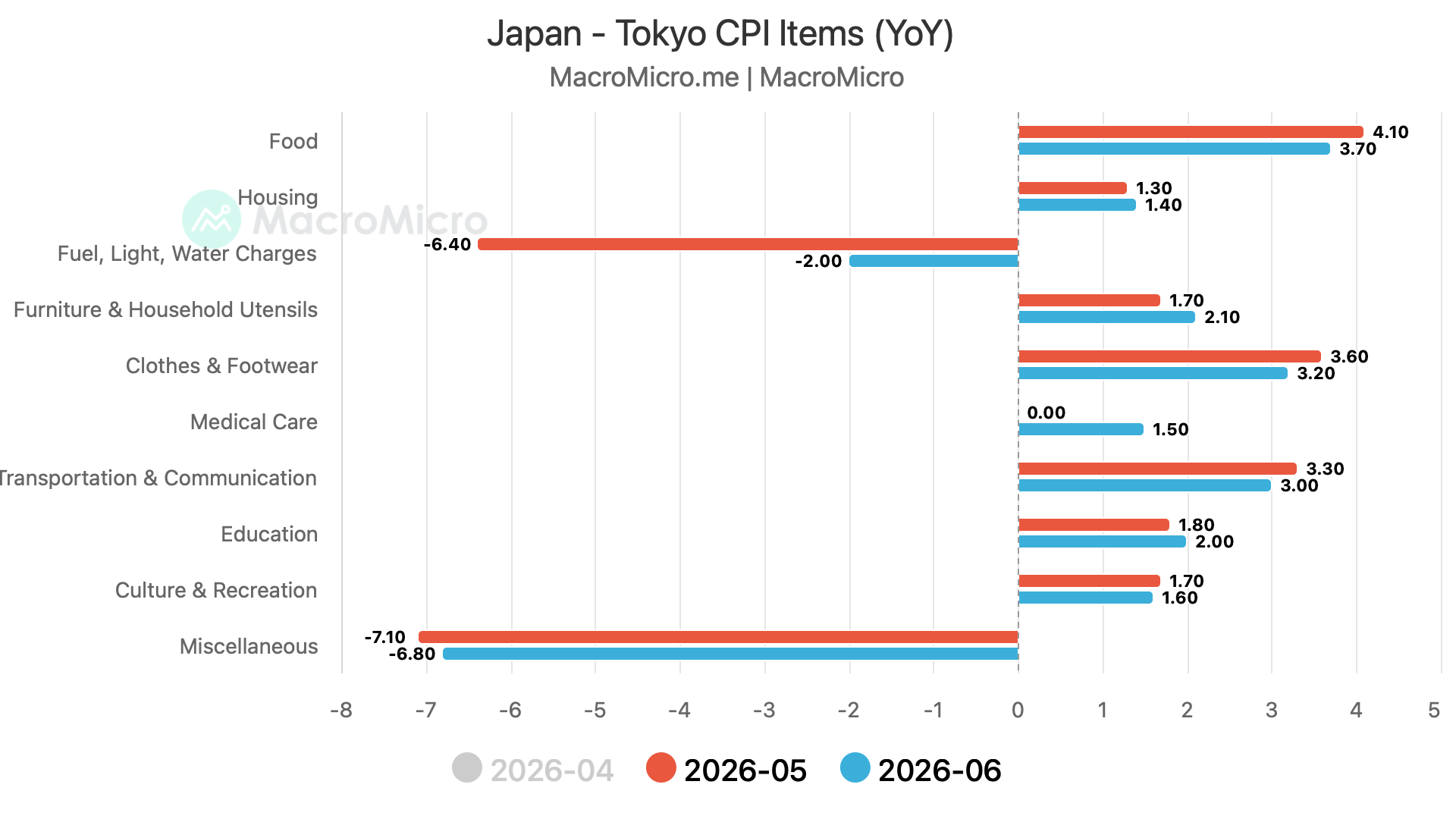

In the land of the rising sun, the Tokyo CPI accelerated to 1.7% in June.

The core CPI, which excludes volatile fresh food prices, grew 1.6% YoY, up 30 bps from the prior month. Furthermore, Core Core CPI (which excludes both food and energy) rose 1.9%, indicating that the inflationary pressures are rising.

When we dig deeper, the disinflationary impact of Fuel, Light and Water charges has reduced significantly. Note that the disinflation was due to government subsidies.

Equities!

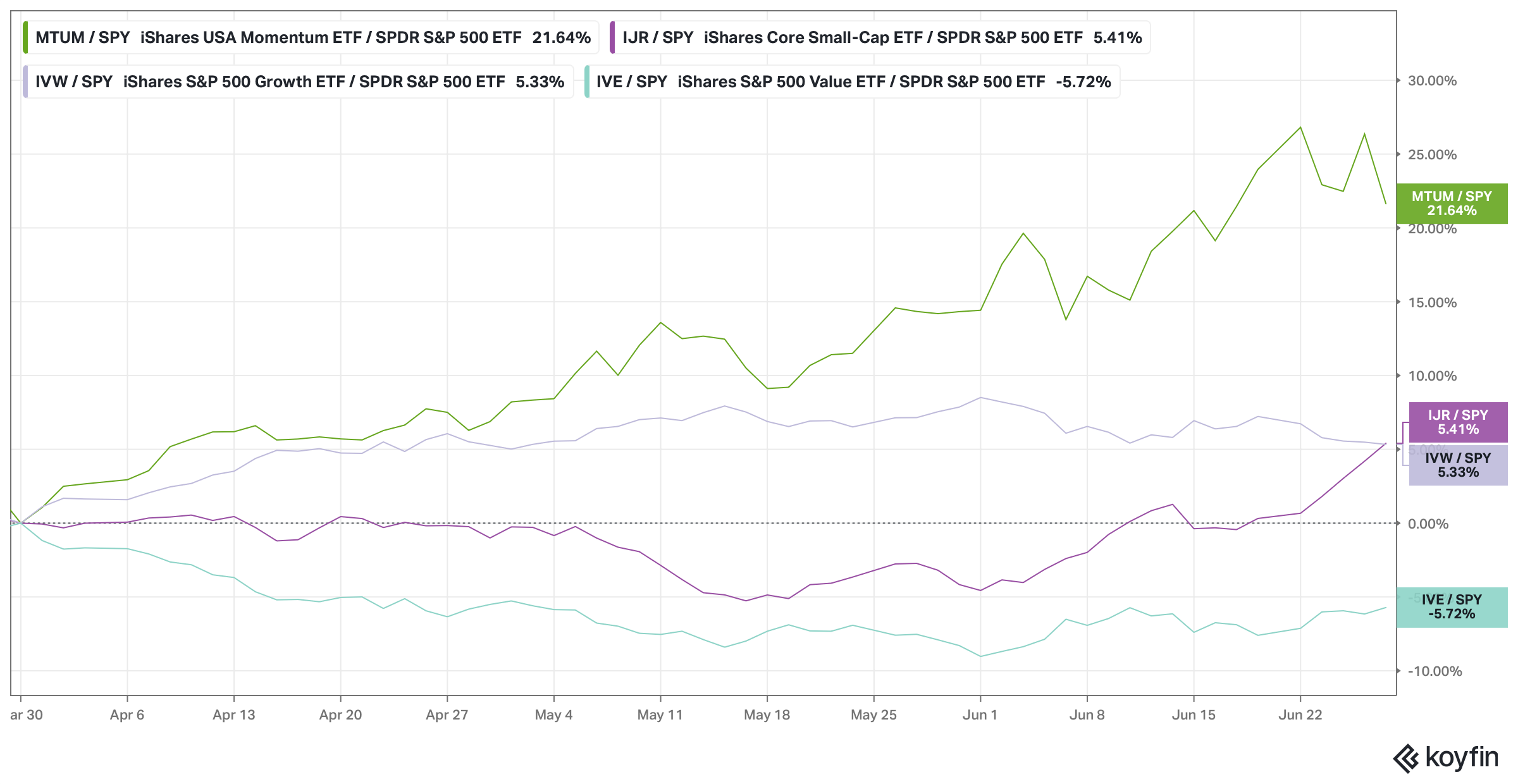

Since the market bottomed out on 30th March, it has been a one-way ride up led by momentum and growth stocks.

MTUM and IJR relative to SPY have seen huge outperformance, while value and small caps have been crushed.

However, since 15th June, we have seen small caps outperform the SPY. As a result, IJR outperformance relative to SPY has now reached 4.5%+.

On the contrary, Momentum has faltered after a stupendous run.