The recipe for success that seasoned finance professionals and portfolio managers, with their years of experience, advise is that markets are a game of permutation and combination.

There is a very famous quote: “Nobody knows anything beyond a certain point”!

Thus, as we manage money, we need to account for all the probabilities of the macro outcomes. If we position our portfolio with only one outcome, then there is a serious risk of underperformance as the tail risks arrive, or the macro outcome is contrary to which one expects.

Nonetheless, there can be periods of extreme cross-asset price movements when markets price in only a single outcome with a cent-per-cent certainty.

In the past few weeks, Mr. Market has oscillated between a “soft landing,” a late-stage euphoria known as the “Last Hurrah” (we wrote about this month), and a potential “stagflationary” scenario. Thus, one needs to be aware of the social media narratives floating around and position/churn their portfolio by making informed decisions based on the incoming data.

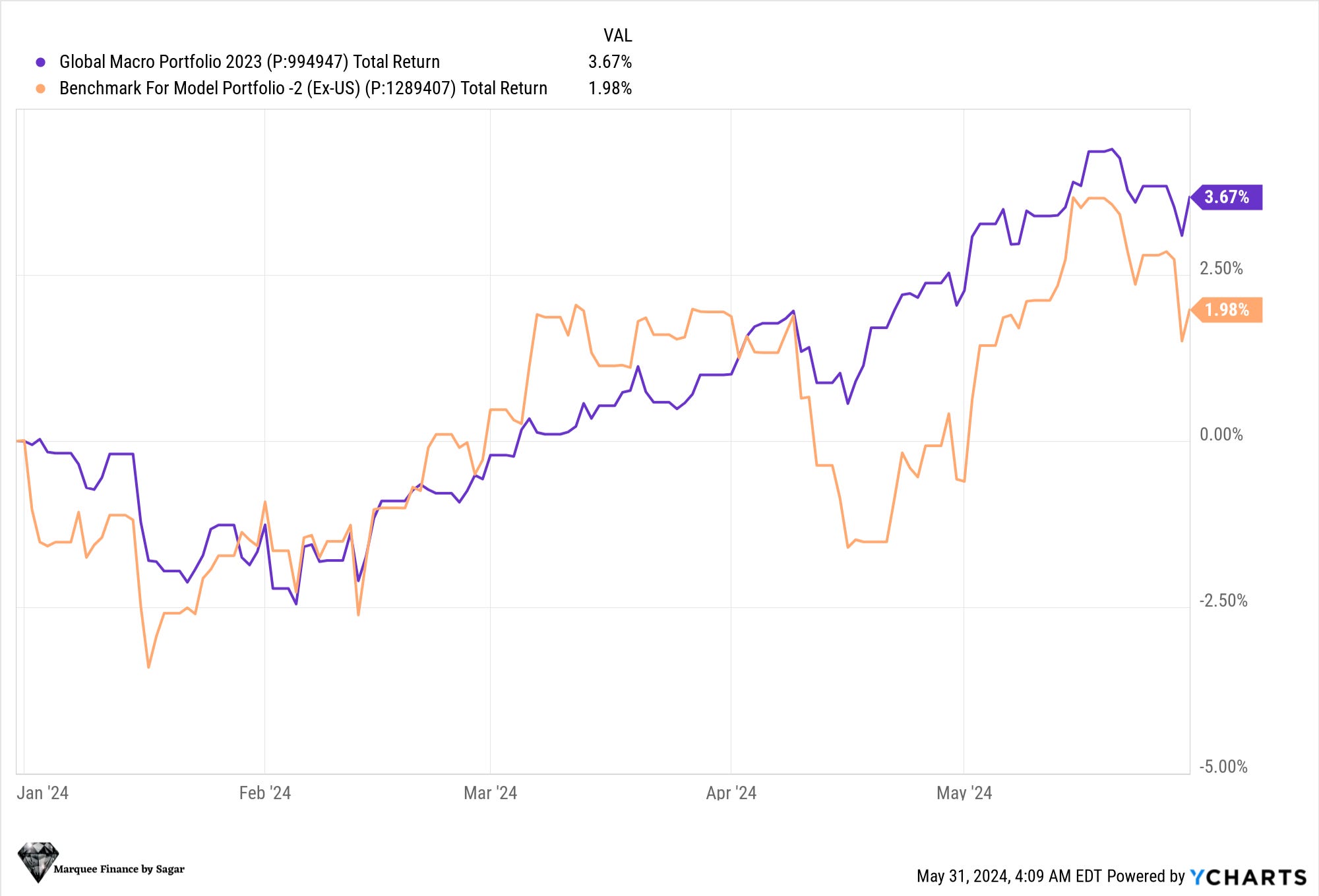

Due to our sound approach and focus on the macro framework, we have been able to generate alpha this year and beat our benchmark.

However, we believe that superior returns are still far away. The market pricing of a soft landing will eventually fade, and the frenzy in the equity markets will soon end as reality about the macro fundamentals sets in.

Equities!

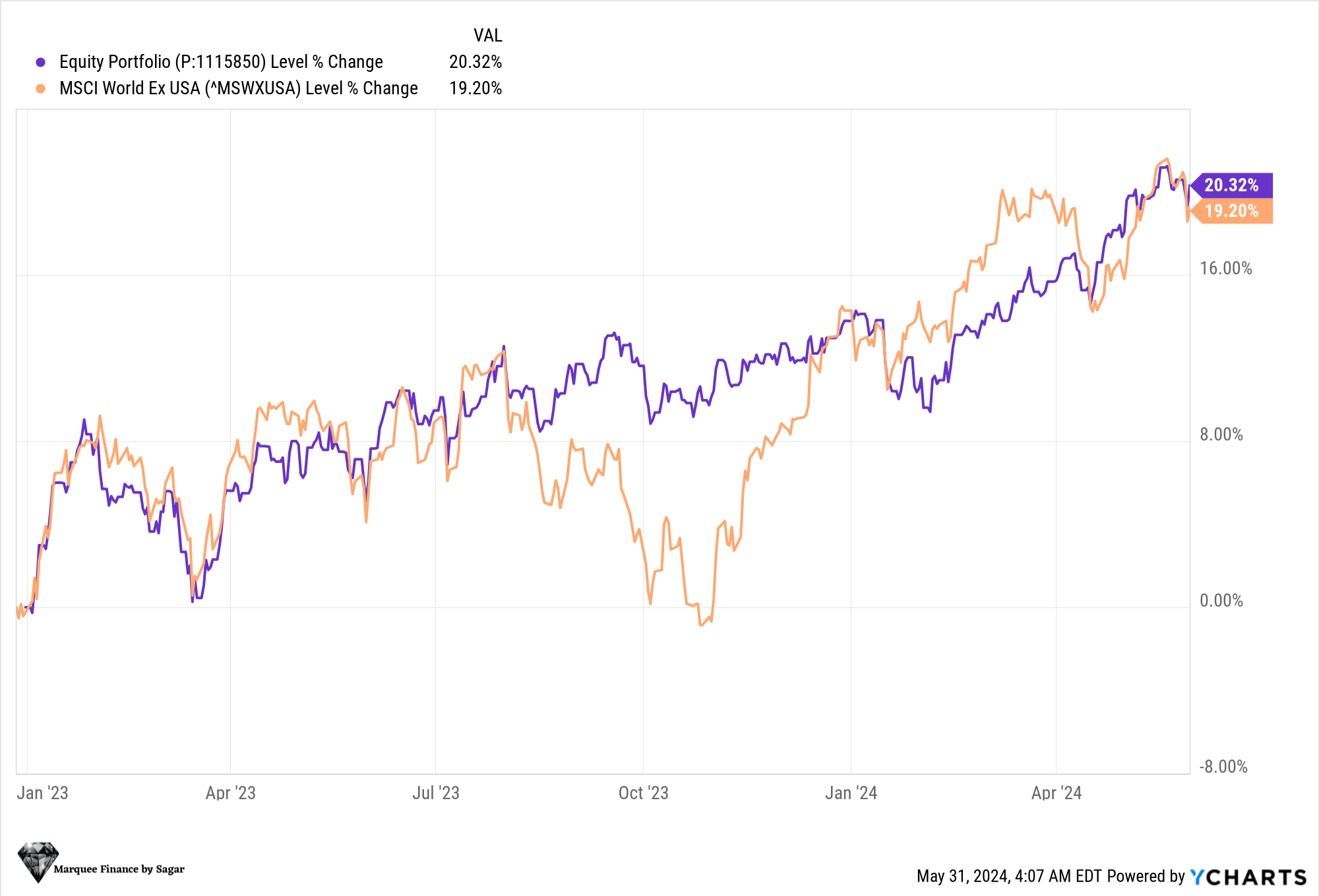

Equity performance has been in line with our benchmark despite high cash levels, as we are unable to discover opportunities to invest in at the current juncture and valuations.

Furthermore, as macro signs of a slowdown in the world’s largest economy become apparent, there are considerable doubts about future earnings growth.

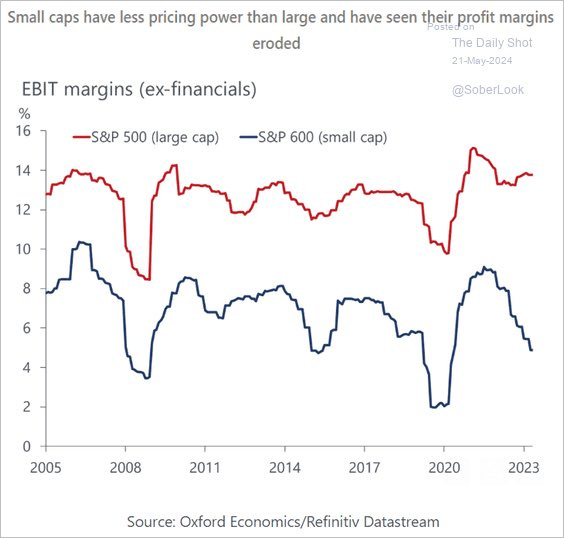

The prominent reason is the operating margins.

Nothing excites or disappoints markets as the margin expansion or margin contraction respectively. Interestingly, the largest companies in the S&P500 (Mag 7) have collectively witnessed margin expansion.

When we dig deeper, we can conclude that the margin expansion is due to the following reasons:

Accelerated layoffs after they overhired post-pandemic, thus resulting in lower employee costs over the past year.

The subscription model aids margins as it’s a high-margin business (rise of subscription business in overall revenue mix).

Pricing power due to changes in long-term structural trends (example-Netflix)

Nonetheless, we have seen some margin erosions from the post-pandemic highs as inflation cools down.

One needs to appreciate that inflation is a double-edged sword. When the economy is buoyant, and consumers are strong, an inflationary environment results in margin expansion across the board.

However, as demand normalised and excess savings vanished, margins fell for small-cap companies. This resulted in a double whammy of higher interest rates and falling EBIT margins, leading to an enormous earnings contraction and underperformance.

Furthermore, market participants believe that AI