A wild and turbulent year marked by dramatic cross-asset moves is “finally” coming to an end.

It was a really challenging 9 months, and we are glad to inform you that we weathered “multiple” storms and emerged unscathed, limiting the drawdowns and outperforming the benchmark for the most part.

We are up 21.5% YTD against a 21.86% benchmark return. The recent (last week’s) underperformance is due to our high cash allocation.

We are happy to protect profits as we close the curtains on 2025, a year that will forever be remembered for a historic reset in global trade.

Today, we will analyse the cross-asset relationship and also some intriguing technical data on precious metals.

Macro Data!

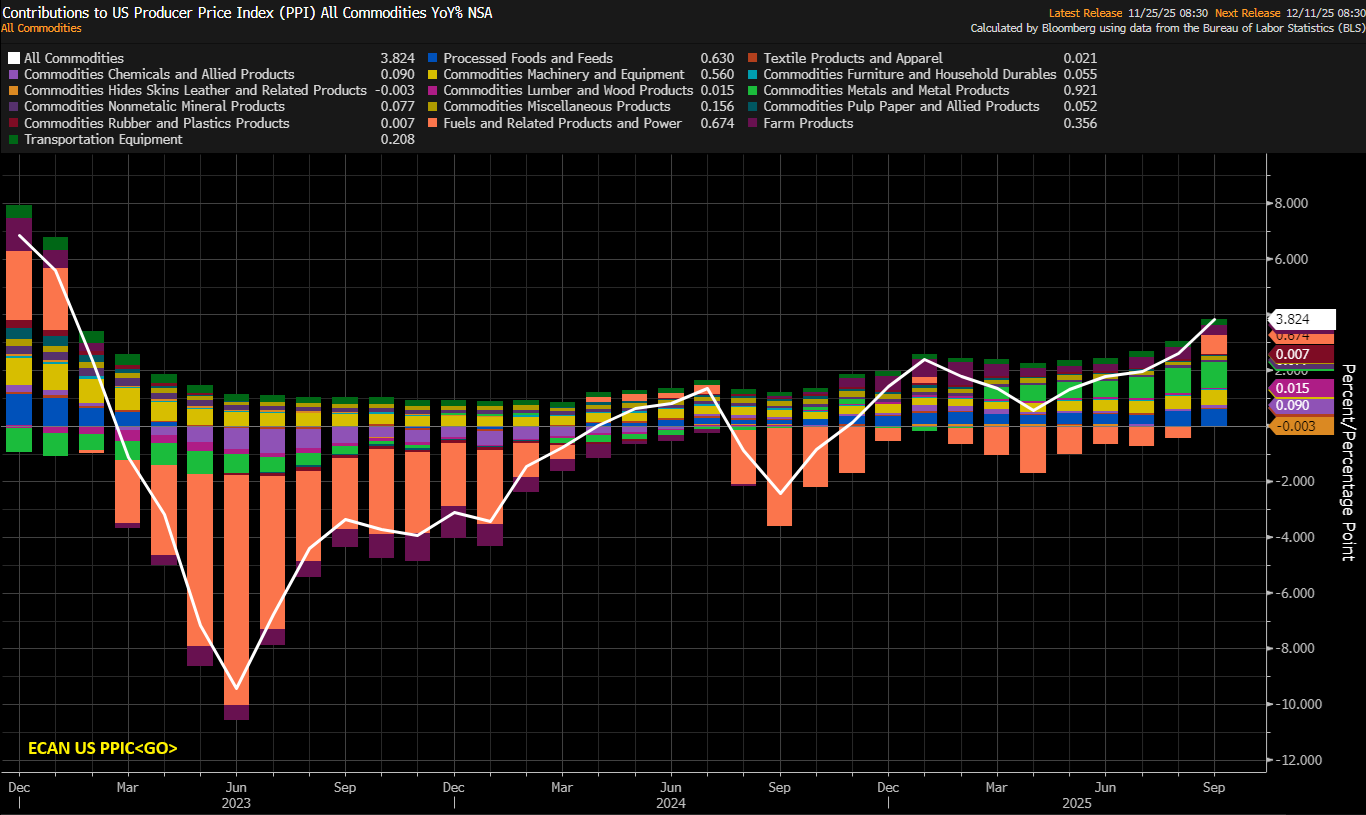

While the headline PPI came in line with estimates at 0.3% MoM, the Core PPI came in a tad softer at 0.1% MoM, against the estimates of 0.2%.

Nevertheless, the internals indicate that pressure is building in commodities, with the YoY change in PPI (All commodities) surging to 3.8%.

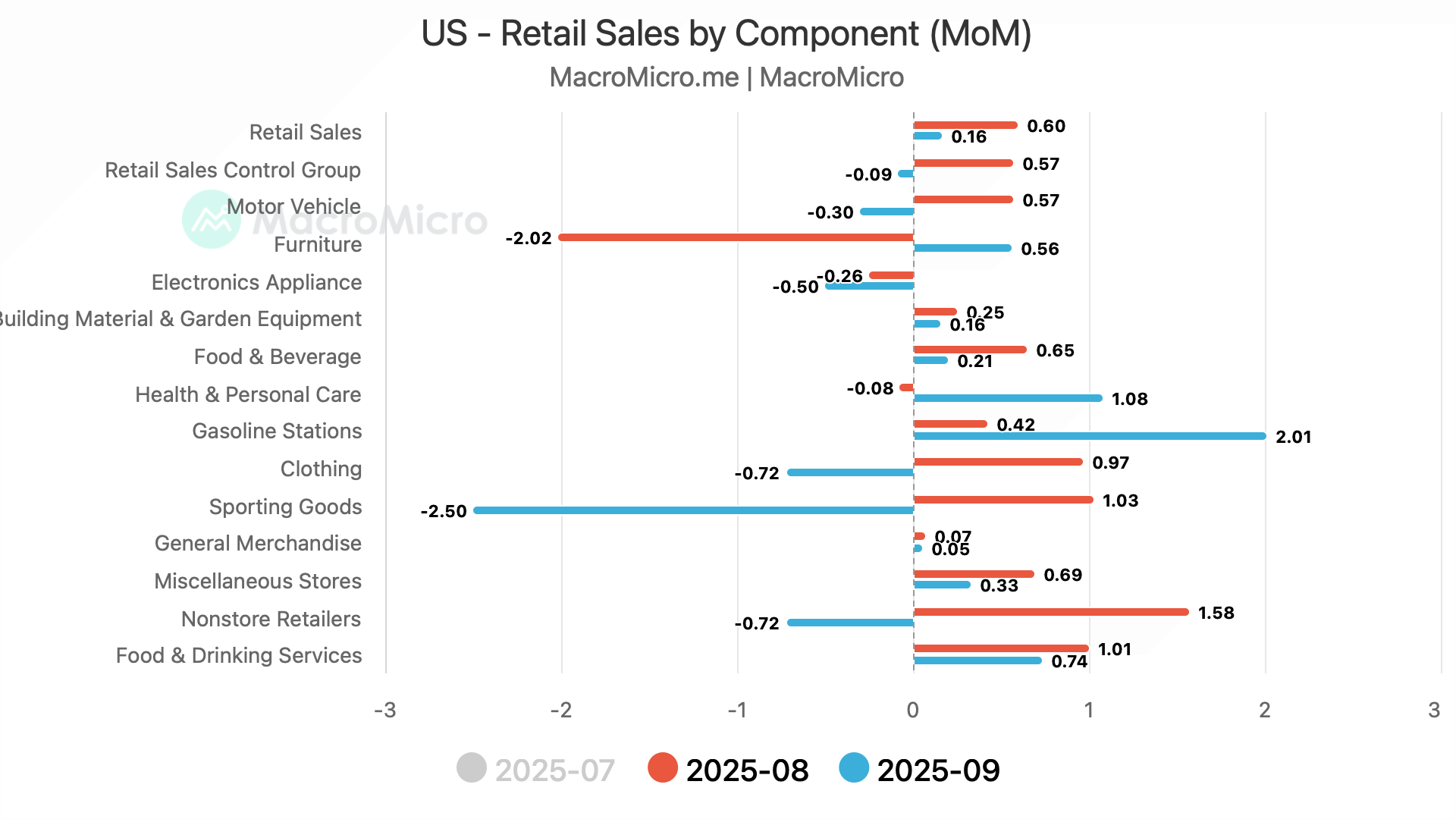

The next macro data point markets eagerly awaited was Retail Sales, which came in significantly softer than expected.

Retail Sales Control Group came in at 0.1% v/s 0.3% Exp, and Retail Sales Ex-Auto came in at 0.3% MoM v/s 0.3% Exp.

Unsurprisingly, the weakness was led by items related to housing, which is in a “recession” as the housing market becomes increasingly unaffordable for the average American.

When we zoom out and look at the broader picture, real retail sales (inflation-adjusted) have grown by just 1% over the last few years, while nominal retail sales are up by 16%.

This further signals what we have been advocating for the past few months (K-shaped recovery).

One data point that JayPo monitors closely, which was absent from the social media, was the Beige Book.

Note that the following statements from the Beige Book are self-explanatory:

Beige Book:

“Employment declined slightly over the current period with around half of Districts noting weaker labor demand. Despite an uptick in layoff announcements, more Districts reported contacts limiting headcounts using hiring freezes, replacement-only hiring, and attrition than through layoffs”

“There were multiple reports of margin compression or firms facing financial strain stemming from tariffs. Prices declined for certain materials, which firms attributed to sluggish demand, deferred tariff implementation, or reduced tariff rates.”

The Beige Book was also a factor that increased the probability of a Fed rate cut at the upcoming December FOMC.

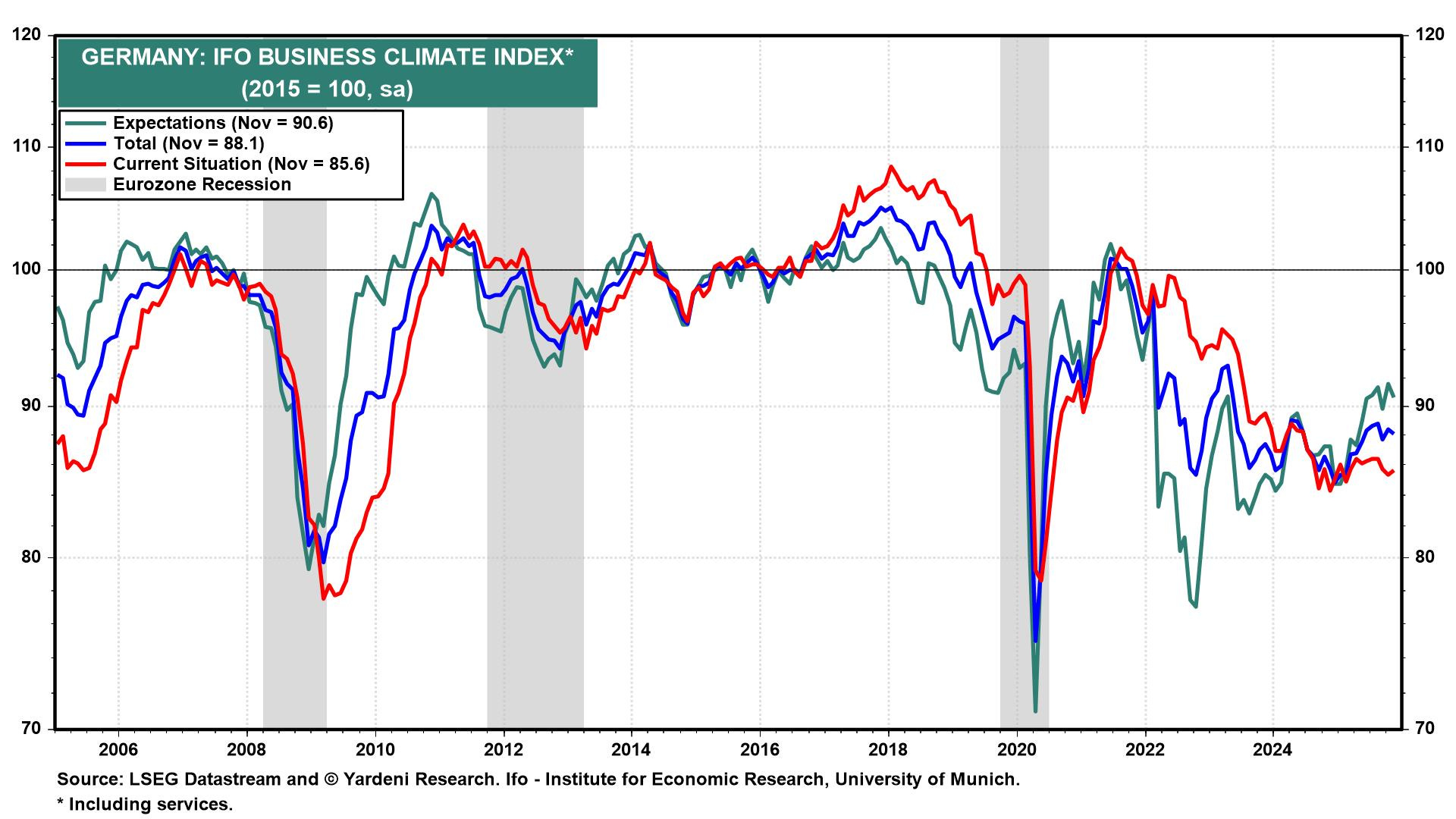

Moving on to Europe, we got Germany’s IFO Business Climate Index.

Since the ECB began the rate-cut cycle, the IFO Business Climate Index has shown a steady recovery; however, as the Trump administration implemented tariffs, the recovery stalled.

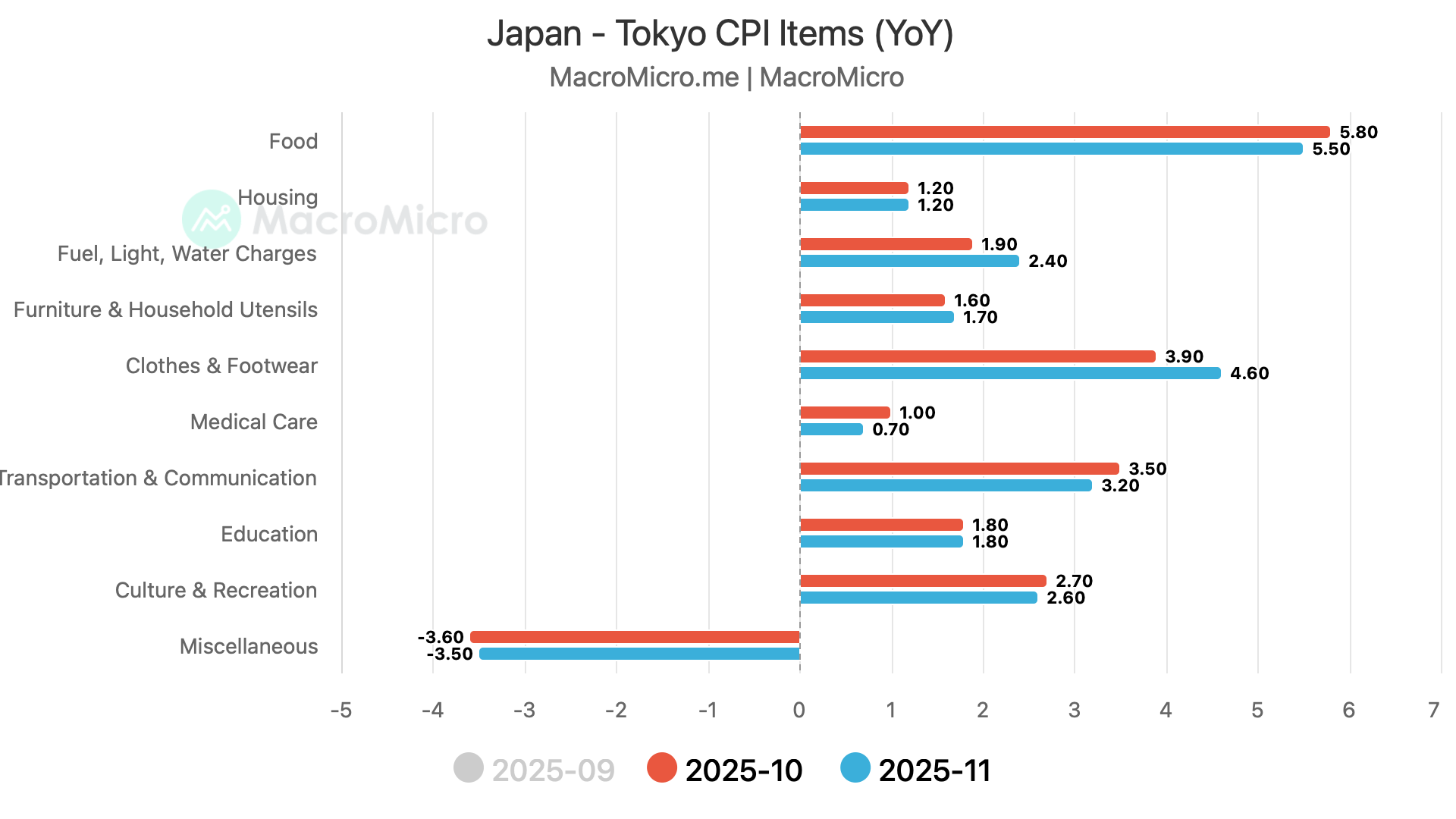

In the land of the rising sun, we received the Tokyo CPI.

The core CPI came in at 2.8%, higher than the 2.7% YoY estimate.

As we can observe, while food inflation has cooled off (as rice prices have eased), there are clear signs of inflation stickiness across categories.