Welcome to the much-awaited but delayed October Portfolio Update, where we will discuss the recent changes in our PF and examine the intriguing macro data.

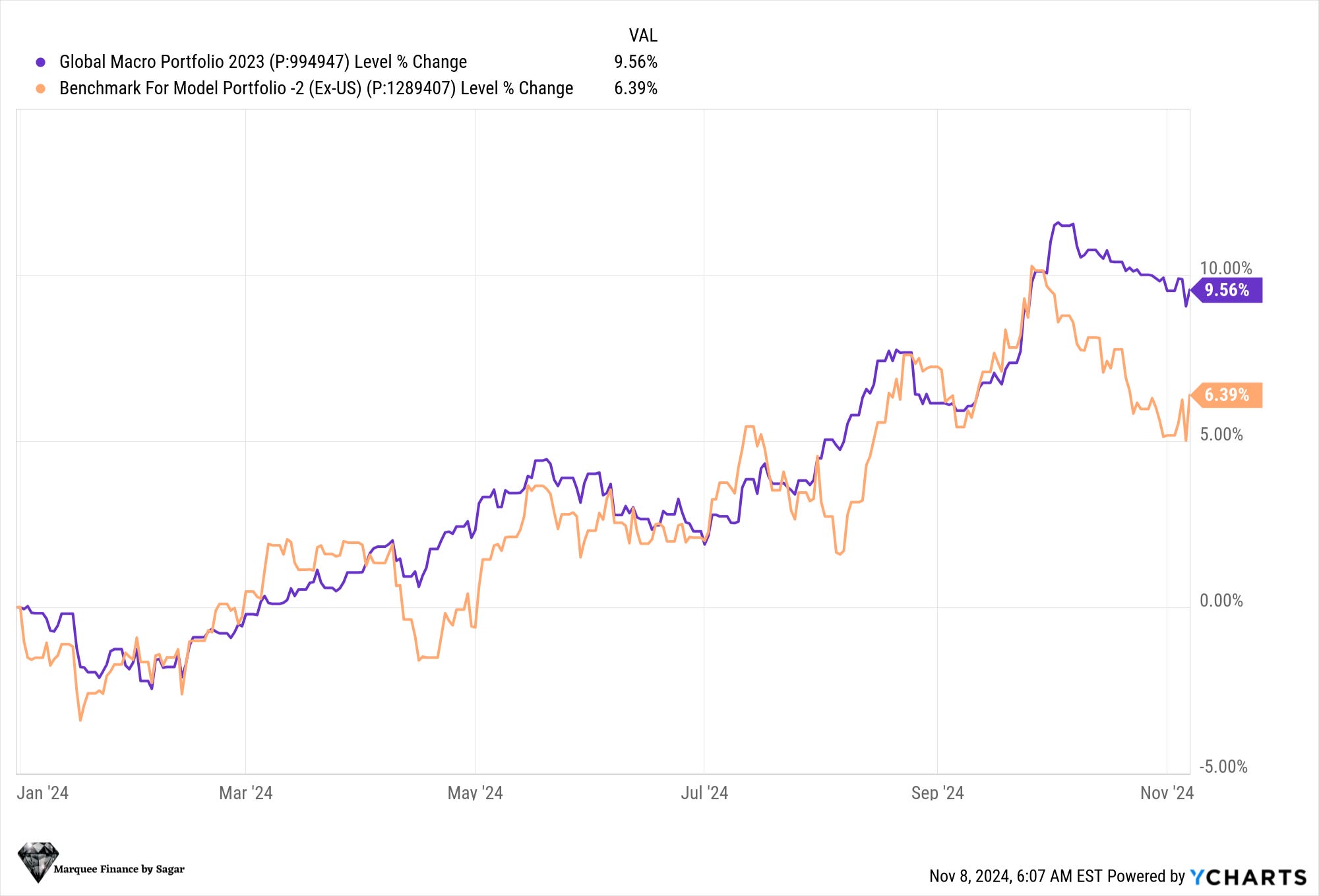

We are glad to announce that we have generated significant alpha this year despite irrational market moves across assets.

As of today, we are outperforming our benchmark (60% IN MSCI ACWI Ex-US and 40% Bloomberg Global Aggregate) by 320 bps.

We also got the crucial results of the US Presidential elections, and Donald Trump is now the 47th President of the USA (results were as per the market’s expectations). Nonetheless, a Republican sweep was a surprise (the House is also most likely going to the GOP).

Furthermore, JayPo announced a 25 bps cut, as the street expected. However, the bond markets are still jittery, as the new President is expected to announce tariffs that will be “inflationary” in the short term.

The BOE cut rates as expected by 25 bps, but the policy was termed a “hawkish” cut as the budget was termed inflationary by the BOE. Moreover, the BOE mentioned that they don’t see “rapid” cuts.

Let us begin with our analysis and portfolio update!

Equities!

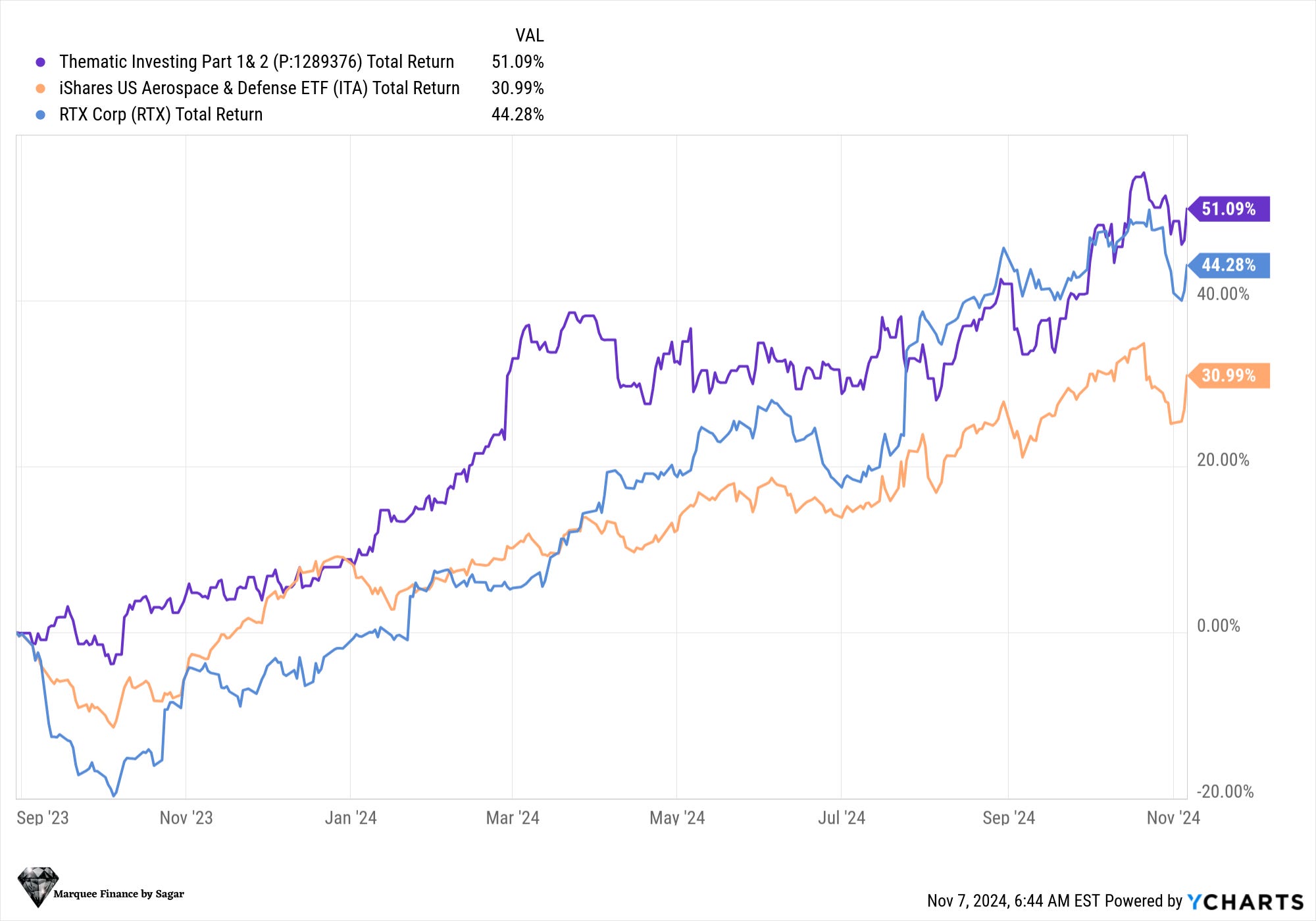

Let us start today with our Thematic Investing bets. In the last 14 months, we have written four pieces on the topic.

In Thematic Investing Part 1&2, we discussed the opportunities in the Aerospace and Defence (A&D) space. Out of the stocks discussed, we bought two stocks in our portfolio and massively outperformed the benchmark ITA.

Note that we exited one of the stocks completely this week after a return of 70%.

Those who want to read about Thematic Investing 1 &2 :

Thematic Investing Part:1

Welcome, folks, to the brand new edition of the Marquee Finance By Sagar. Most of you know me as a macro investor; however, since the advent of my investing journey, one of my passions has been to pick stocks actively.

Thematic Investing Part 2!

Welcome to the second part of the Thematic Investing series that we initiated a few weeks back. In the first part, we did a comprehensive overview of the Aerospace and Defence (A&D) sector (new subscribers can click here to read Part 1).

PS: Note that markets are becoming excited about the “nuclear theme” when we have been bullish for the past year and a half. We also made some big money in URA.

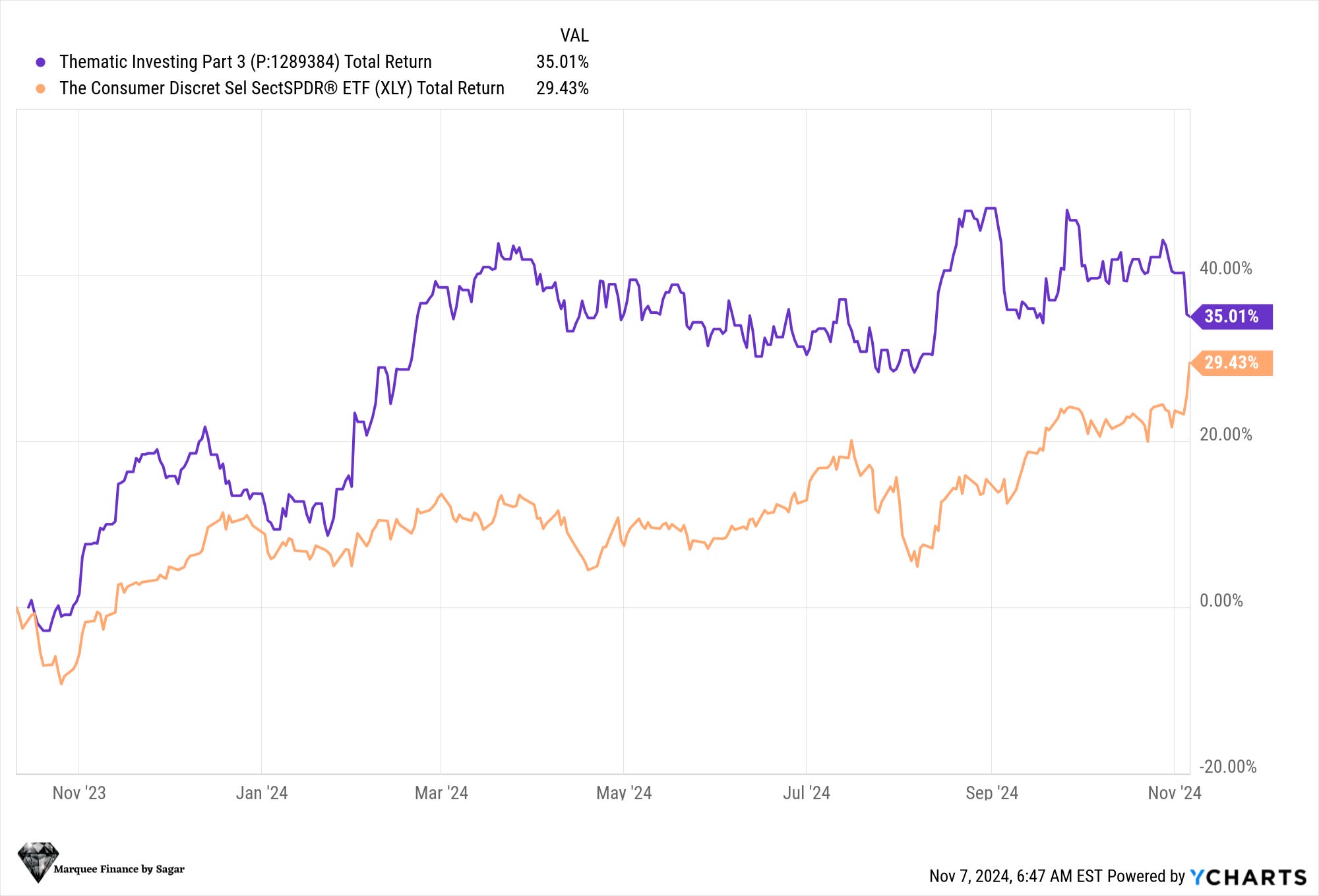

In Thematic Investing Part 3, we selected two stocks (we didn't add them to the PF due to valuation concerns).

Nonetheless, those who would have heeded the advice and bought would have outperformed the benchmark by a wide margin.

Thematic Investing Part-3, those who want to read:

Thematic Investing Part-3!

“The single most important decision in evaluating a business is pricing power. If you've got the power to raise prices without losing business to a competitor, you've got a very good business. And if you have to have a prayer session before raising the price by a tenth of a cent

Note that we had a Part-4 as well, and we only added one stock to our PF from Part-4. Nevertheless, the stock we didn’t add is up 40% thanks to the AI rhetoric (the company is an indirect beneficiary of AI)

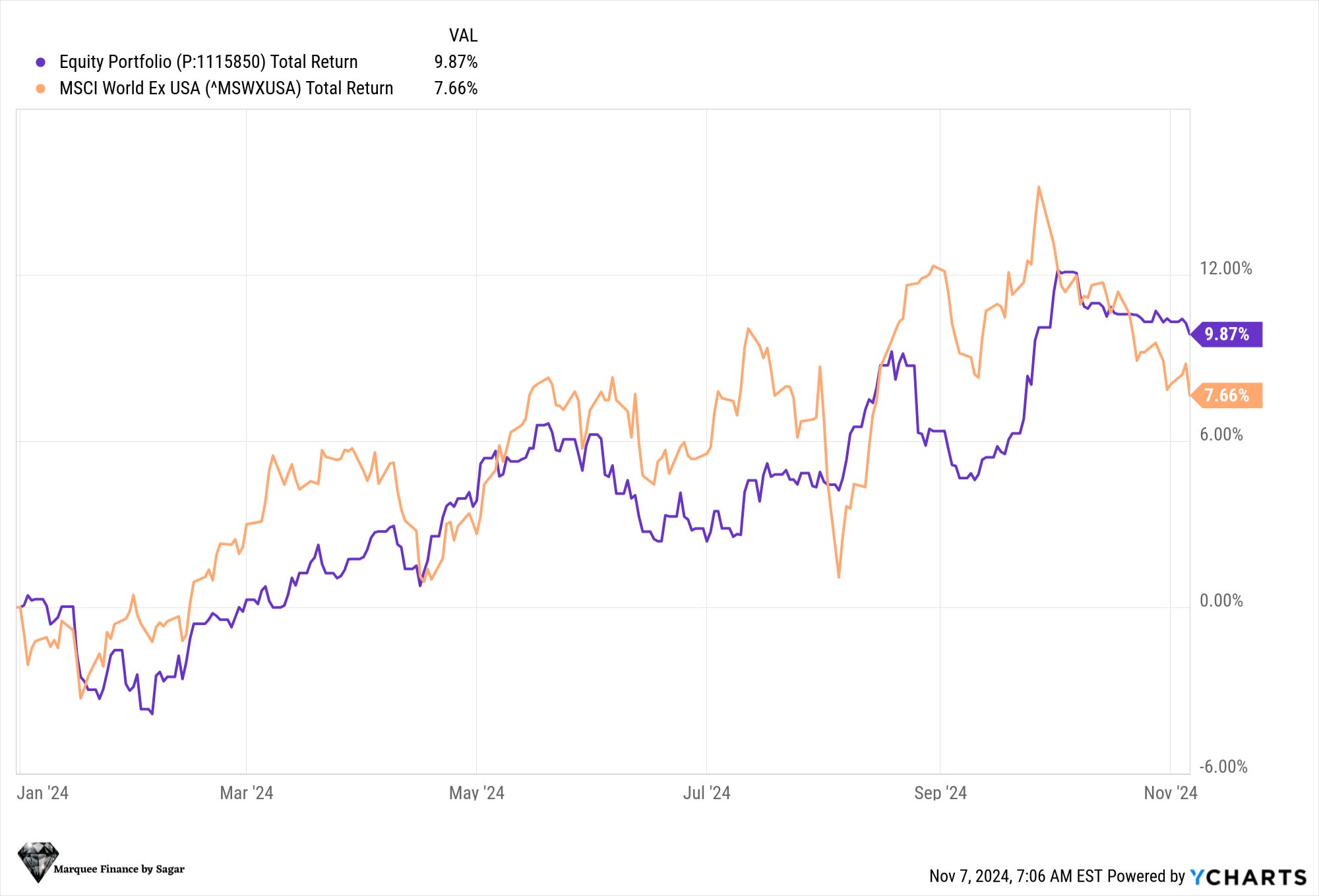

Before we talk about the burning topic of valuations in the US equity markets and jump to some of the earnings of our PF stocks, we look at the performance of our equity portfolio relative to the benchmark.

The underperformance beginning in May was due to the very high cash allocation of our equity PF.

We continue to hold sizeable cash in our PF due to waning opportunities ( valuation concerns).