As we close the third quarter of an unimaginable year loaded with numerous reckless narratives spanning from an imminent recession early in the year to a soft landing narrative, we are satisfied with our performance and the trades (80% profitable) we undertook this year.

Nonetheless, the slight underperformance of 50 bps relative to our benchmark is due to the very high cash levels (around 30%) we have maintained for the last few weeks.

We have been right in most trades this year (and profitable), while some have been disappointing.

Nonetheless, the total return and the alpha generation ultimately matter when investing.

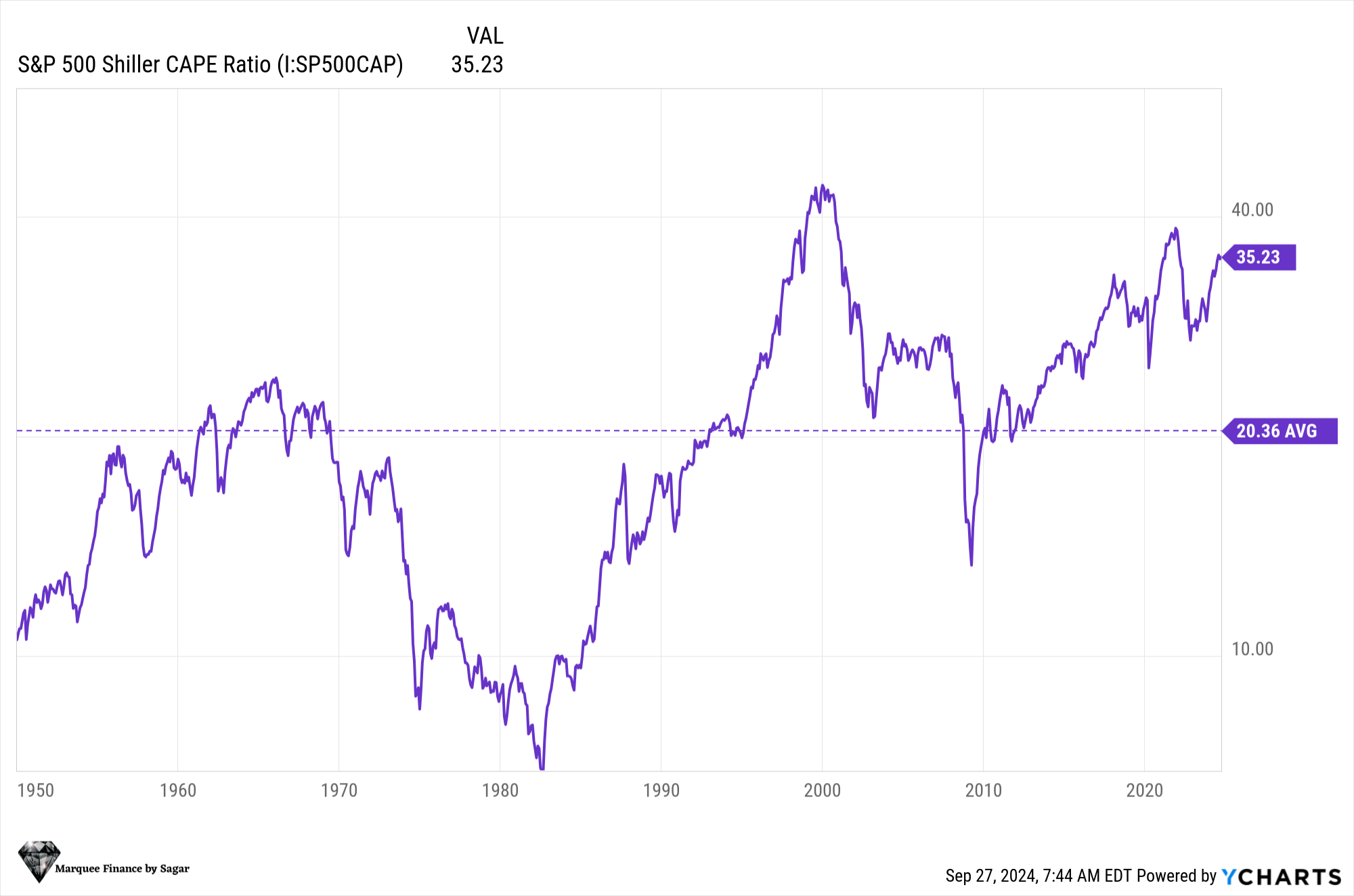

We strive to do our best even though some parts of the equity markets are “irrational” and have reached insane valuations.

Let us look at the performance and review the trades for September!

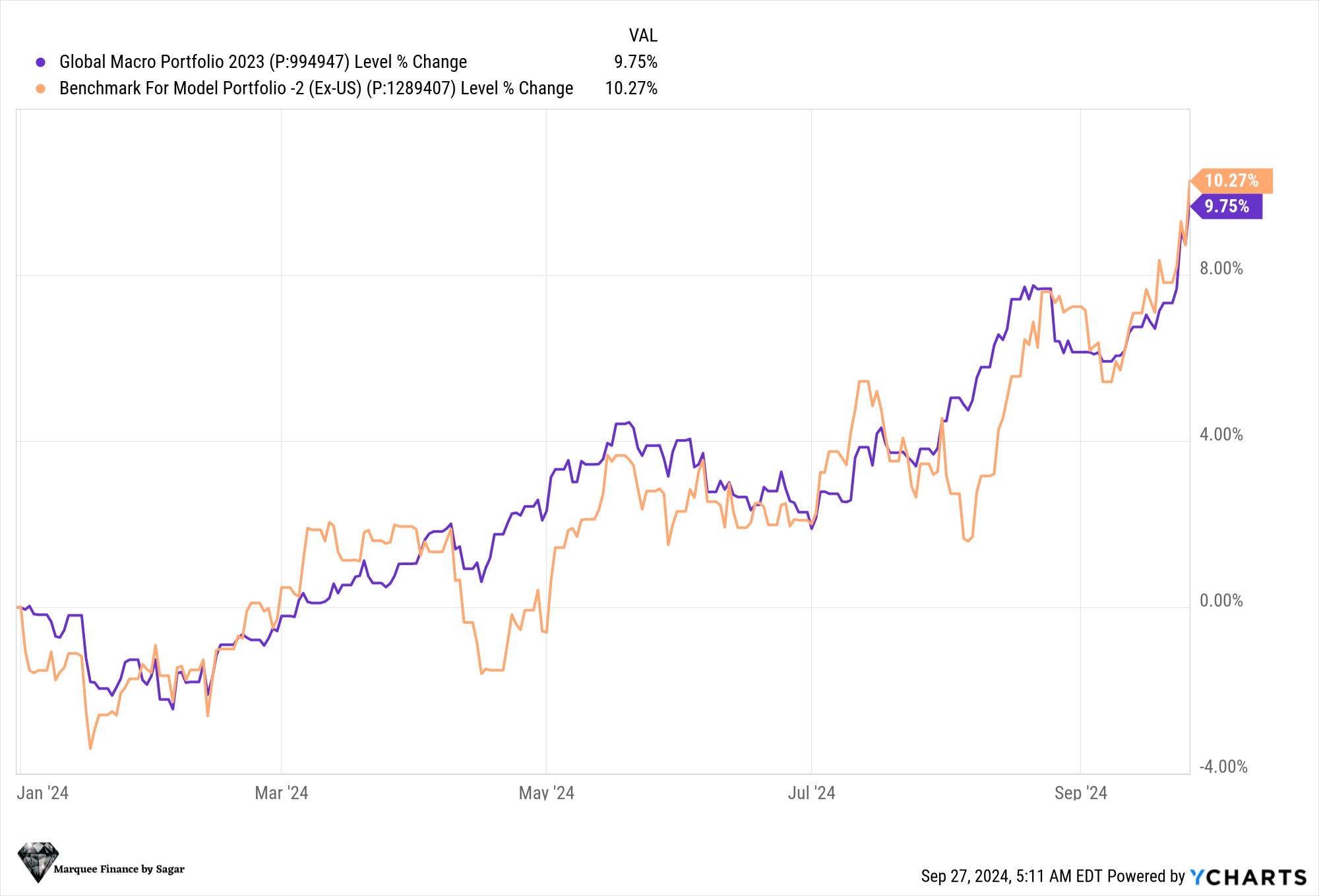

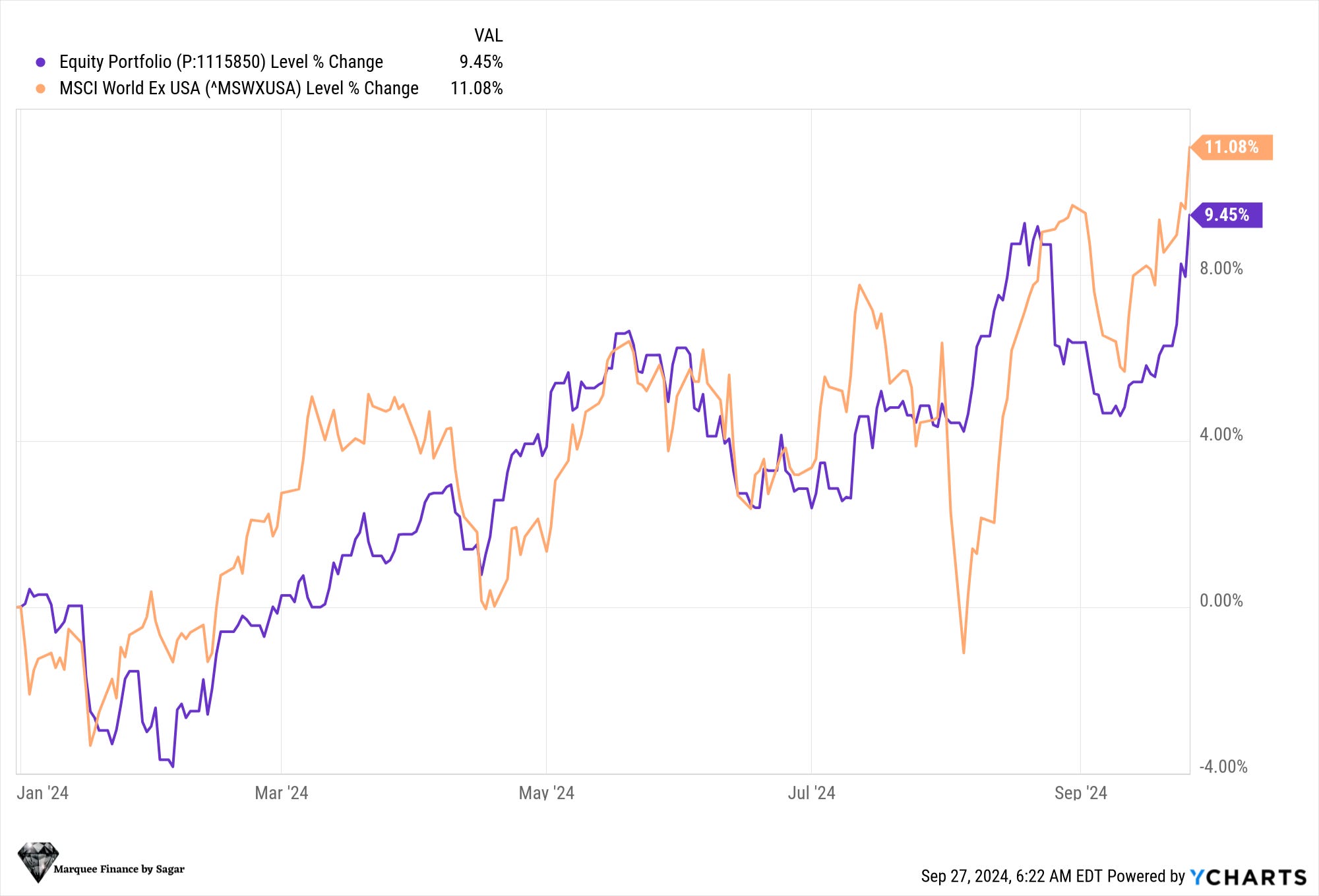

Equities!

Last month, we wrote that the portfolio suffered severe underperformance due to a significant drawdown in one of our equity holdings.

However, we recovered from the drawdown, and now the equity PF is at YTD highs.

Furthermore, the PF's underperformance is due to our high cash levels, which we have maintained due to political uncertainty and our negative view of US equities (valuation concerns).

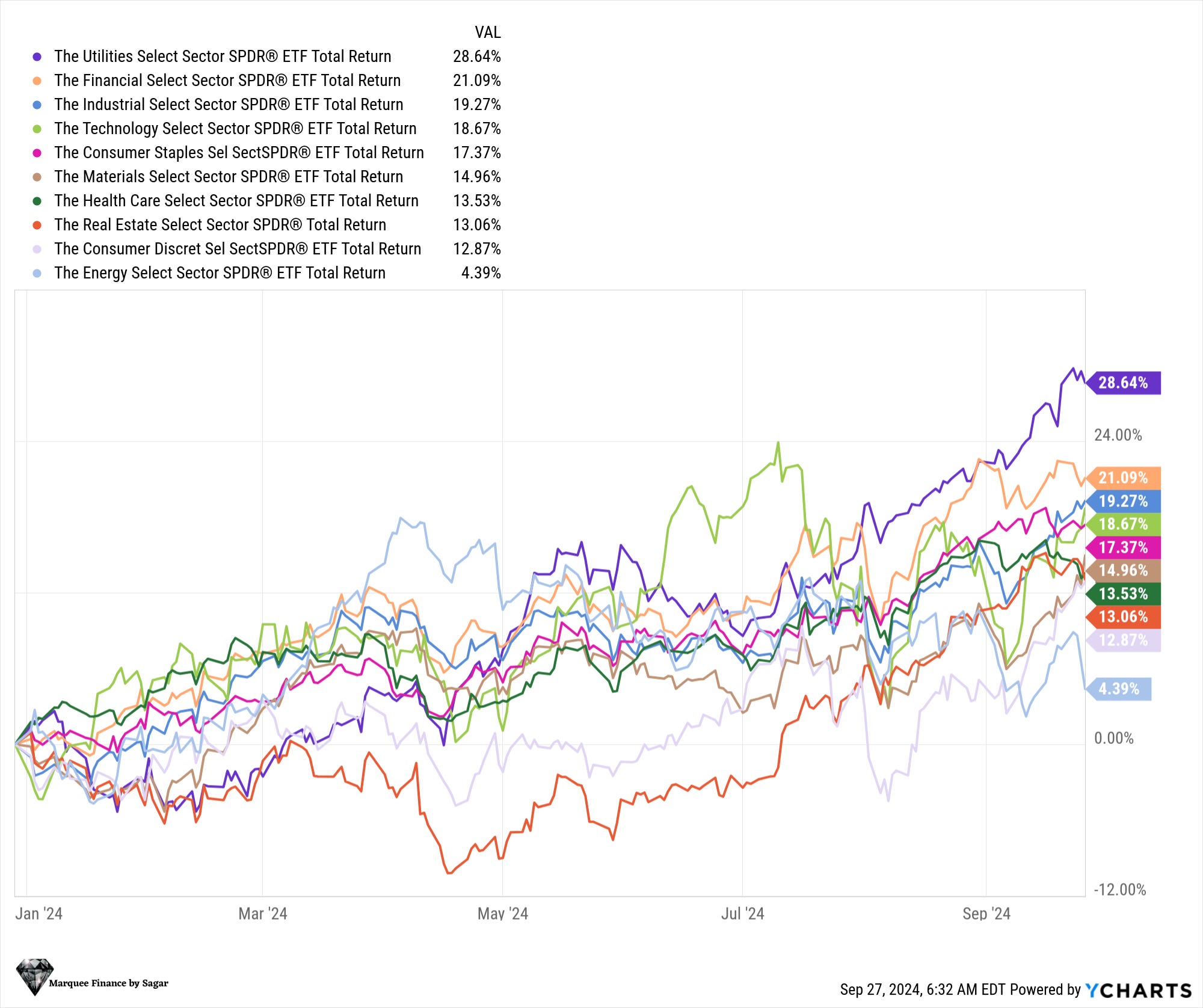

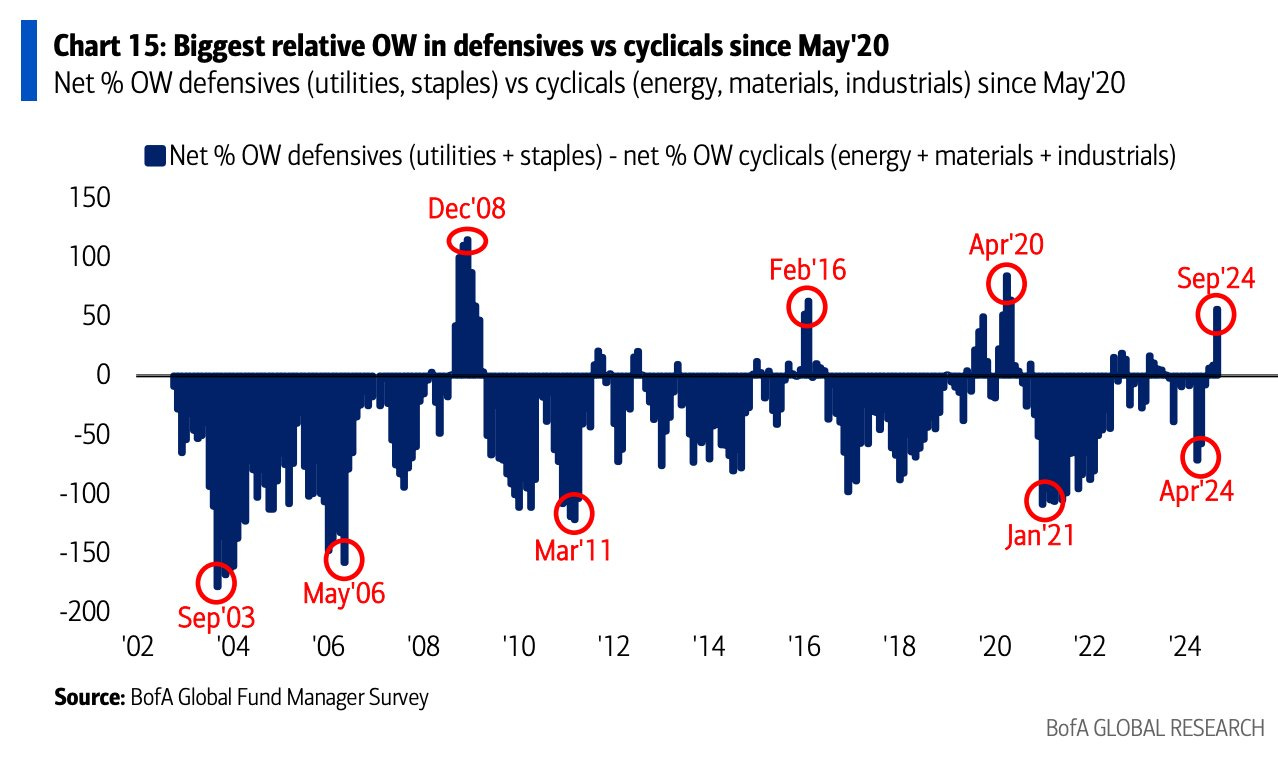

One of the trades that worked favourably for us (which we completely exited this week) was the long XLU (utilities) trade.

We were early in the trade and entered last year as we expected utilities to outperform other sectors due to recession concerns (defensive play) and a potential fall in long-term yields (100 bps fall in 10Y since we bought).

Unsurprisingly, XLU is the best-performing ETF YTD as market participants dumped the expensive tech names and went all in on defences.

Nonetheless, utilities had now become an overcrowded and consensus trade. Furthermore, the recent AI pump indicated that the risk reward was unfavourable.

Overall, we expect US equities to remain rangebound as we enter the earnings period and a blackout period for buybacks (note that the most significant demand for stocks YTD has been by buybacks).

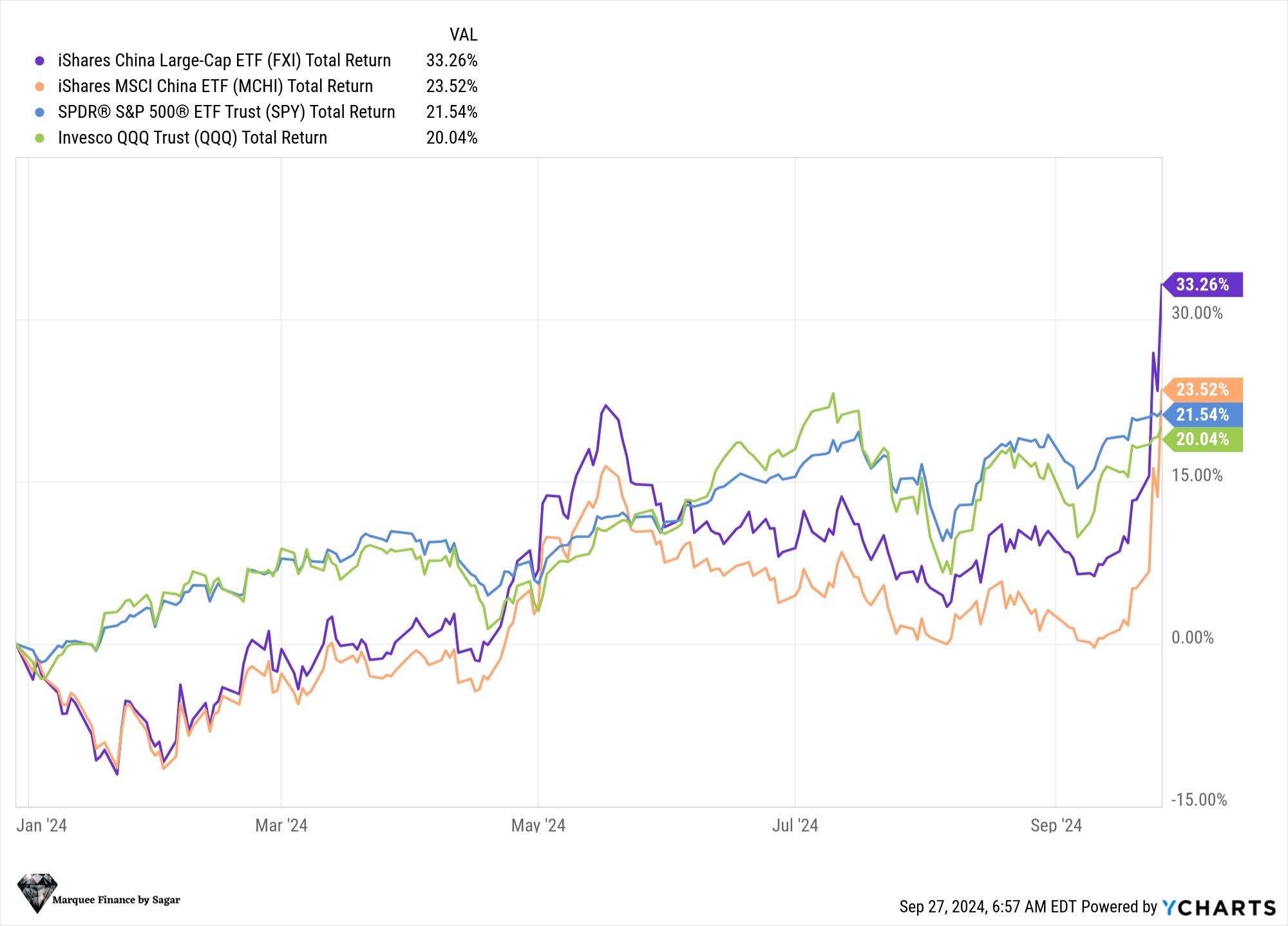

Moving on, many market participants have been surprised by the Chinese rally.

We have been bullish on China because of extreme pessimism (though macros are horrendous), and the valuations for the large-cap Chinese names have been dirt cheap.

As a result, the lightning rally in Chinese names has led the Chinese ETFs to outperform the US markets by an enormous margin.

PBOC launched a stimulus package early this week, the largest since the COVID-19 pandemic. The package also included a surprise fiscal stimulus, which involved doling out cash payouts, aka the “helicopter money,” to the poorest residents.

To summarise:

50bps RRR cut providing RMB 1 trillion long-term liquidity (guidance of another 25bps to 50bps cut before year-end).

20bps rate cut of the 7-day reverse repo.

30 bps rate cut of the 1-year China Medium-term Lending Facility (MLF).

Lowering existing mortgage rate.

Announced RMB 500 billion in liquidity from the PBoC to buy equities!

Lowering the deposit rate to mitigate the impact on bank margins.

Injecting up to 1 trillion yuan ($142 billion) into its biggest state banks.

Nonetheless, we are not optimistic about the prospects of the recovery in the Chinese property market.

The first step is the “bottoming out,” as the prices have been in a free fall.

Secondly, we have mentioned multiple times this year that the Chinese