Entering 2023, a recession was a consensus call among all the market participants. As a result, earnings were expected to fall in 2023, and higher rates were to compress the multiples, thus leading to a fall in equity markets.

Nonetheless, was the consensus wrong, but earnings surprised on the upside as nominal growth was high throughout the year (in fact, in high single to double digits), and the AI-led “Euphoria” led to a sensational rally.

Defying all the odds, a handful of stocks buoyed by regular bouts of enormous liquidity injection led to sensational returns for risk assets in 2023.

In fact, the top performer for the year was none other than BTC, and if you want to dig deeper, it was the fourth largest cryptocurrency, SOL, giving a mind-boggling return of 1100%.

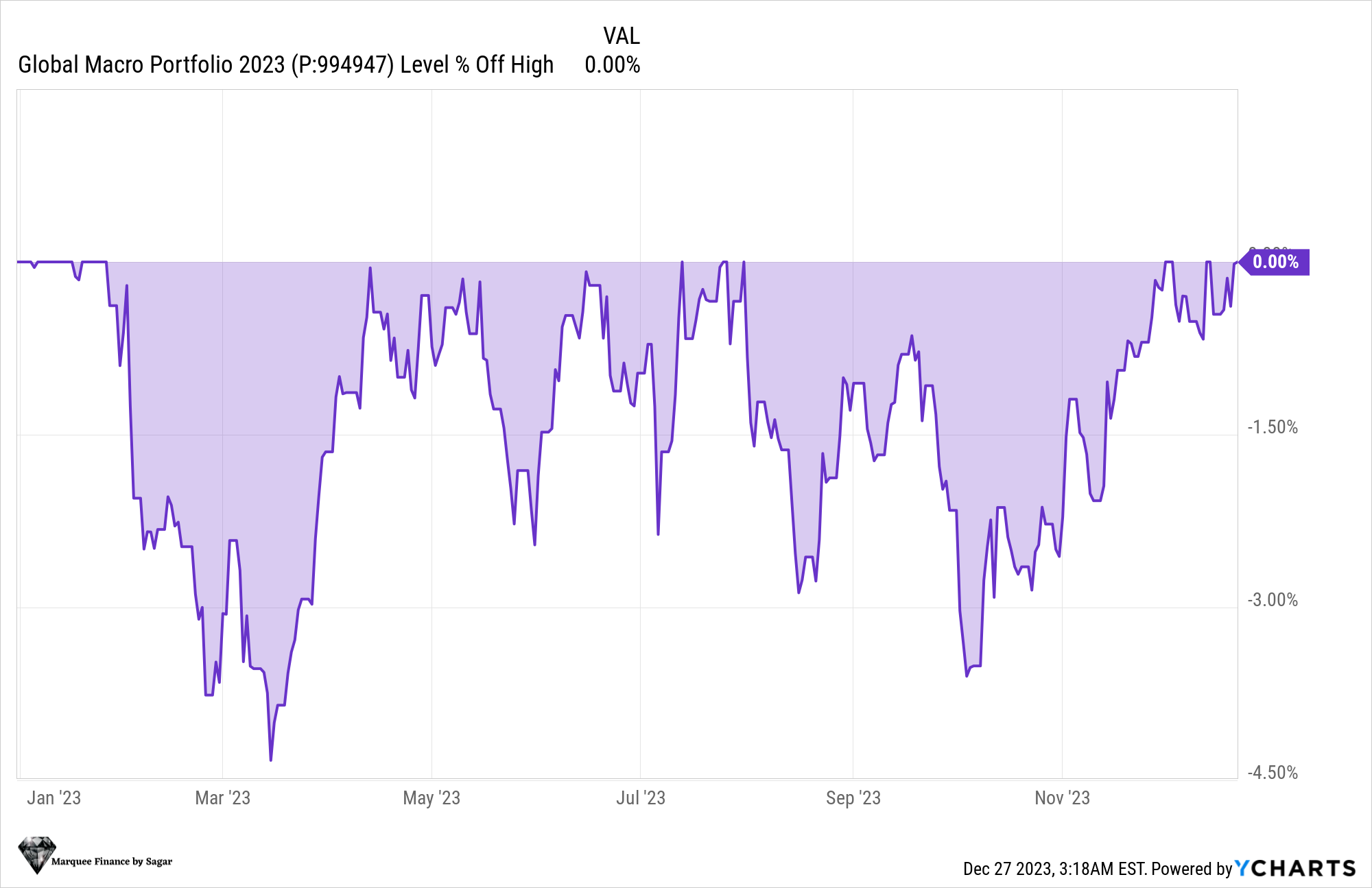

Nevertheless, what matters is the risk-adjusted return and, thus, how one’s PF perform during drawdowns, which we witnessed twice during the year.

In February, we increased the cash to 7% and thus performed well during the March drawdown.

Furthermore, from September till mid-November, we significantly increased the cash in our Portfolio from the lows of 3% to 13%, thus shielding us from the extreme drawdown.

Note that all the asset classes ex-USD were punished hard in these months, thus causing mayhem for the coveted 60:40 portfolio due to the positive correlation at that time.

The max drawdown we witnessed was around 4.5% during the SVB crisis.

More so, we are glad to inform you that we finished the year at a high, with a total return of 8% YTD.

Note that though we have underperformed the 60:40 PF (60% MSCI ACWI World, 40% Bloomberg Global Aggregate), what matters is the process and the long-term returns rather than short-term performance. Furthermore, MSCI ACWI World is largely concentrated to the Mag 7 and the US names which were an outlier this year.

As I have said earlier, we are ready to sacrifice the short-term returns to generate significant alpha in the long term.

We will never ignore the process of chasing the returns as it would distort our thinking and divert us from our path, which involves prudent risk management, regular introspection, position sizing and a data-dependent approach.

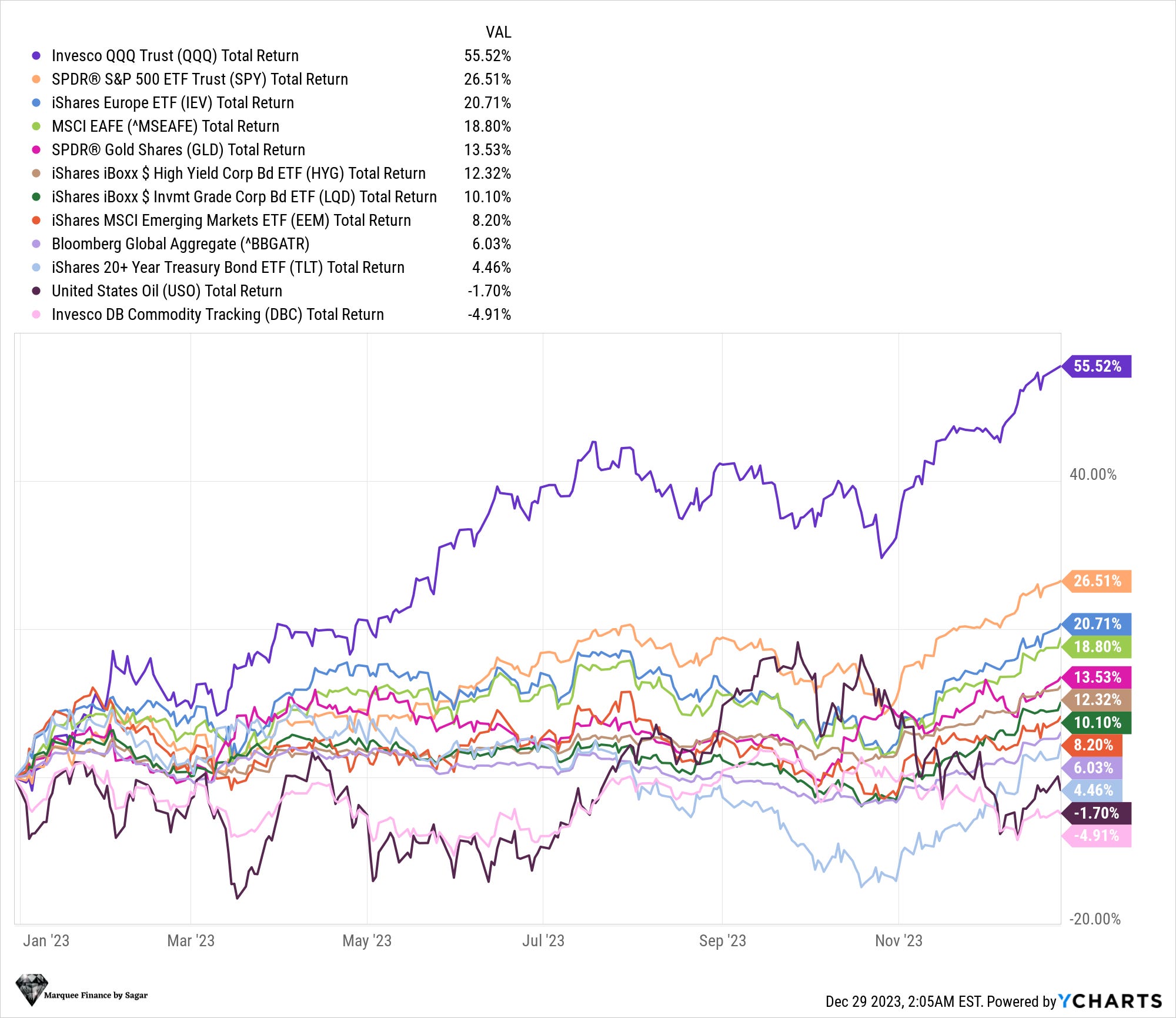

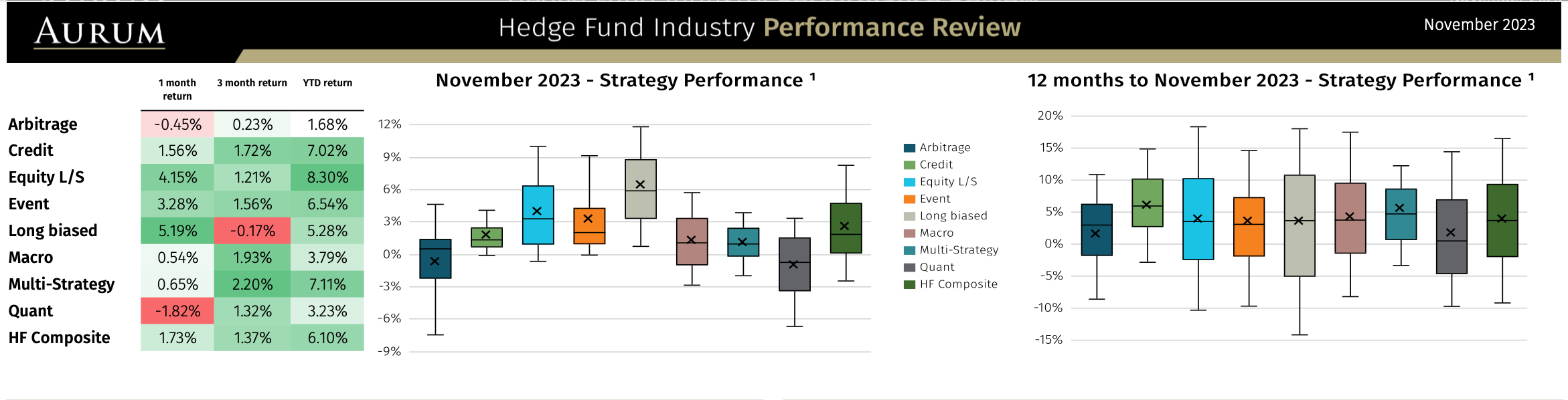

Nevertheless, we still outperformed most of the Hedge Funds, focusing on various strategies (note that macro-based hedge funds returned only 3.79% till 30 November).

Let us look at our performance across various asset classes and also look at our current open positions.

Equities!

Total return from the equity portfolio, which hovered around 38-50% in 2023 (Yes, we were underweight equities compared to a 60: 40 PF), was healthy at around 13.74% (outperforming most of the L/S HFs).

Furthermore, we were long throughout the year, with some short positions beginning in early H2.

Total Long/Short Ratio (ex-Cash) remained healthy at around 80-90%, thus benefitting from the enormous return in the equities.

Let us first look at the gains we made across all our equity positions in 2023.

DXJ (Hedged Japan): 32% (7 months)

EWW (Mexico): 30% (8 months)

URA (Uranium): 29% (4 months)

HDB (HDFC Bank, India): 8.1% (5 months)

DBEU (Hedged Europe): 4.2% (partial profits: 5 months)

CHIX (Chinese Banks): 6.2% (8 months)

RIO (Commodities): 4.5% (2 months)

EIDO (Indonesia): 3% (11.5 months)

Note that these were our successful exits.

Japan had been one of our biggest winners (note that the hedged ETF outperformed the unhedged EWJ). Furthermore, EWW benefitted greatly from the sharp appreciation of MXN in the first half.

We also entered Uranium in late H1 and juiced most of the rally. Although exited a bit early, but again had to follow the process, and the valuation of Cameco Corp was a bit uneasy for us.

The only disappointment was Indonesia, which we expected to outperform the Asian peers considering the macro fundamentals and valuation comfort, but it didn’t transpire.

Now let us look at some of the misses:

GNR (Commodities): -2% (8 months)

INDA (India): -3% (45 days)

VIXY: -3% (15 days)

THD (Thailand): -14% (8 months)

As one can observe, Thailand was a disappointment as Chinese tourists remained absent in 2023. Thus, our macro strategy of Thailand benefitting from the influx of Chinese residents after the reopening failed.

Furthermore, commodities performed poorly throughout the year and thus, GNR was a drag on the PF.

VIXY was a very short-term trade with a tight SL to benefit from the elevated volatility. In fact, we were up by 7-8% at one time but a sudden VOL crush post the QRA announcement in late October led to our SL getting hit.

Now let us look at our open positions: