Risks Of Earthquake Piling Up!

“Frankly, I don’t see markets; I see risk, rewards and money”- Larry Hite.

The financial system, burdened by an astronomical amount of debt, reaching hundreds of trillions of dollars, is teetering on the edge of fragility.

Higher bond yields, which lead to lower bond prices, have created trillions of dollars of “paper” losses for multiple entities globally.

While the Fed used the BTFP to backstop the vulnerable US banks and averted a massive crisis, higher yields still plague the global financial system.

Just a month ago, on 24th May, we wrote to our paid subscribers about the risk emanating from rising Japanese yields.

Unsurprisingly, this week, we learned that Norinchukin Bank in Japan will sell Sovereign Bonds in the US and Europe to cover $63 billion of losses arising from “wrong” bets on interest rates. Notably, Norinchukin holds 20% of all foreign bonds held by Japanese banks.

This “forced” foreign selling phenomenon by Japanese institutions will likely pick up pace (more in the East section later on) and have consequences for the global financial system.

This is one of many risks plaguing the finance world. Beneath the surface, risks have been piling up in the US as the vulnerable sections of the US economy have seen significant deterioration in their health.

As a result, it’s no brainer that Central Banks are “eager” to cease monetary policy.

Today, we will examine the grey areas susceptible to a credit event leading to a chain reaction across the financial system.

US!

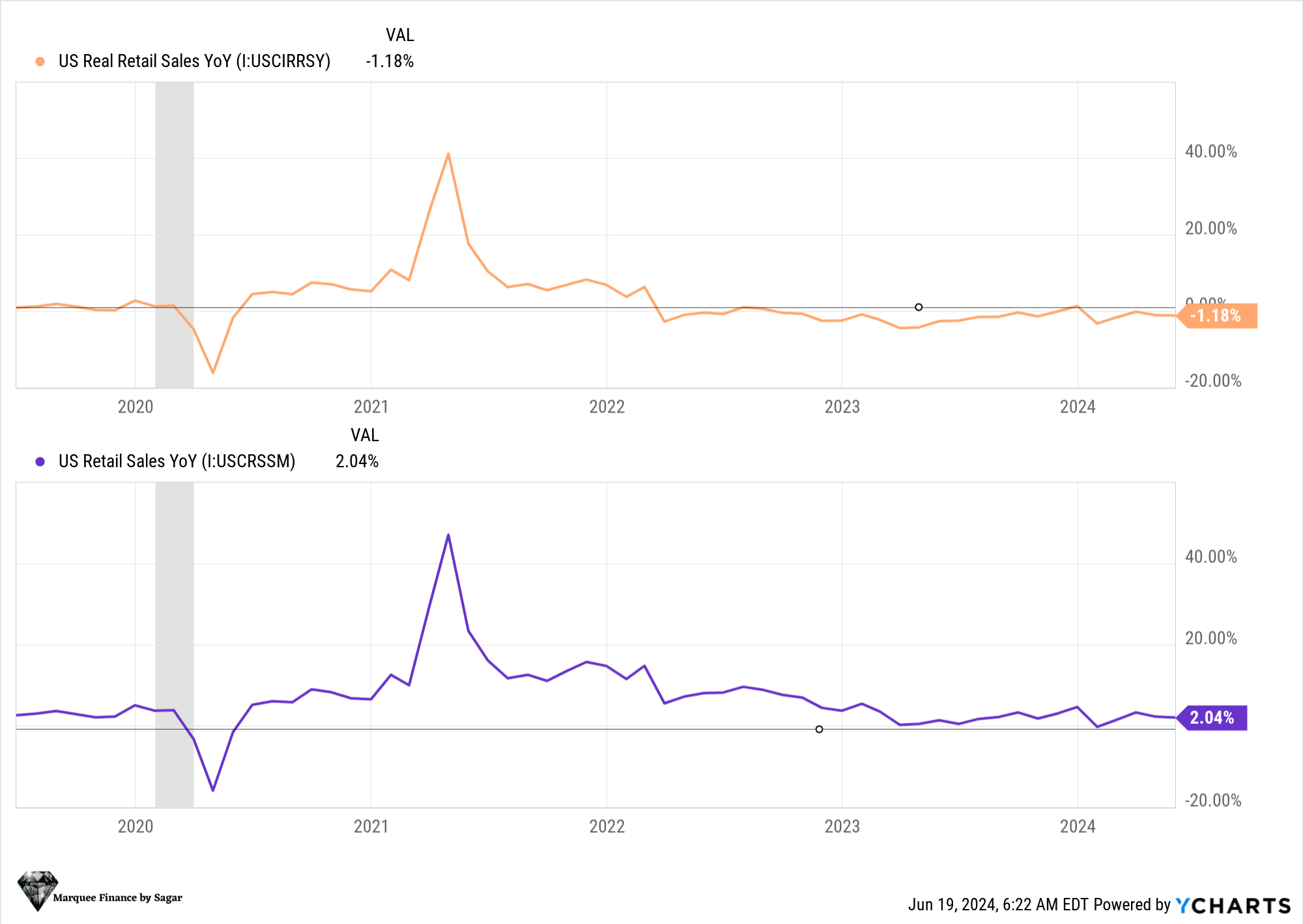

First, let us briefly discuss the macro data released this week. One of the highlights was retail sales, which have been disappointing for the last few months.

This month was no exception, as the numbers missed the street expectations. The May retail sales ex-autos and gas rose by 0.1% MoM against the estimates of 0.4% MoM.

While nominal retail sales have been subdued, real retail sales (adjusted for inflation) remain in negative territory, indicating that the bottom pyramid of consumers is struggling.

Due to the inherent weakness in real retail sales, they have now normalised back to the pre-COVID trendline.

In fact, this is one of our first risks for today:

RISK 1:

As we can observe, the plunge in real retail sales below the trendline has led to a Fed pivot on previous occasions. Just before COVID hit, the US economy was “headed” for the first post-GFC recession as real retail sales fell below the trendline.

In fact, if we connect the dots, we can comprehend that in late 2019, anticipating the weakness in the labour market/economic data, the yield curve inverted, and a recession was predicted for 2020.

Thus, we can’t ignore the macro data, which has suddenly turned sour in the past few weeks/months.

It’s a known fact that the effect of tight monetary policy takes more than 18-24 months to affect the labour market, which is the economy's most lagging indicator. This is one of the most significant risks we need to watch closely.

RISK 2:

In our one of the most viral pieces (paywalled removed):

The Big Short 2.0?

“How did you go bankrupt?” “Two ways. Gradually, then suddenly.”- Ernest Hemingway.Thanks for reading Marquee Finance by Sagar! Subscribe for free to receive new posts and support my work. The recent events that have unfolded in the last month have everyone left wondering about

we wrote that a credit event if it transpires, will likely emerge from the unregulated parts of the financial system. We wrote that the unprecedented growth in private credit post covid, especially post the SVB crisis, is a grey area and susceptible to significant liquidity shocks.

We saw that a fortnight ago, Ninepoint halted cash payouts in its three private credit funds worth $1.5 billion. Though it’s a minuscule amount, it demonstrates that at a time of a slowing economy and reducing liquidity, issues will emerge in the “opaque” private credit markets, similar to what happened in the CDO markets in 2008.

Note that several banks have also recently increased their exposure to private credit firms. Thus, the ripple effect can be far-reaching for the banking industry.

This is what Jamie Dimon said about the private credit markets 20 days ago:

“There could be 'hell to pay' if the swelling private credit market starts showing cracks.”

RISK 3:

We also discussed this earlier, but today, we will discuss the numbers and consequences, as this is one of the risks that markets have yet to consider.