"The Black Swan"!

Taleb, in his masterpiece “Black Swan: The Impact Of Highly Improbable”, mentions "Platonicity".

He refers to it as the concept "which makes us think that we understand more than we actually do".

Many market participants have offered their expert opinions on how the Strait of Hormuz (SOH) situation will end. (There is also an intriguing chapter in the book about the forecasting error rate of so-called “experts”)

We believe that nobody has a clue what will happen (a classic Platonic mindset is at play), and thus we are in the midst of a black swan event as reality slowly seeps in.

The consequences of the conflict will be far-reaching.

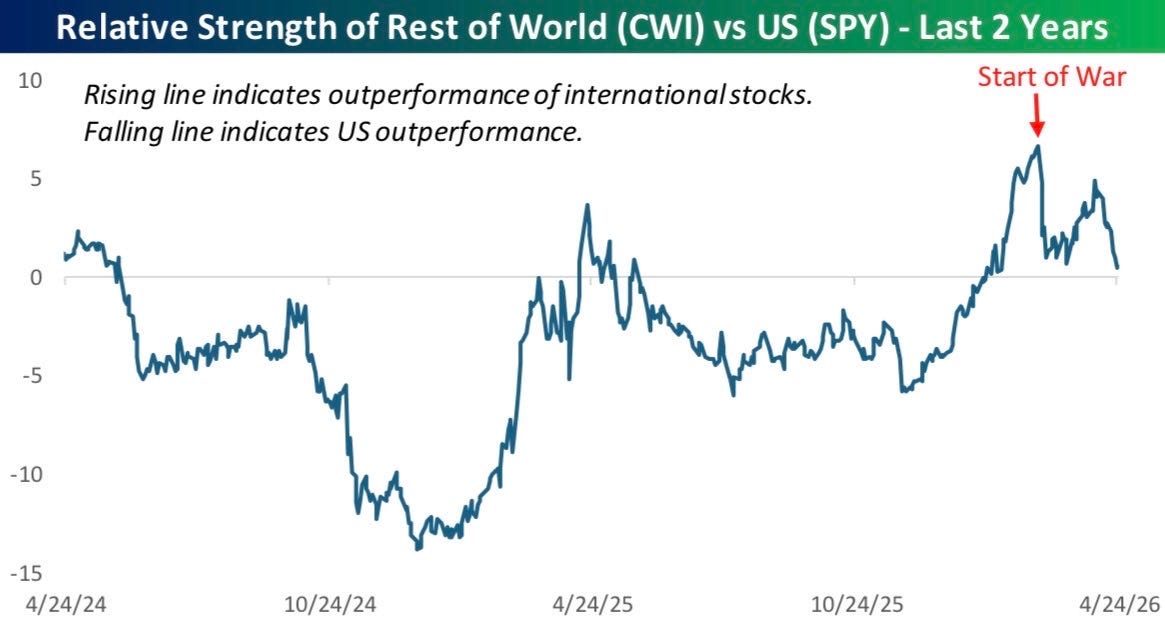

Nevertheless, we have seen unprecedented activity in the equity markets as global liquidity has poured into a handful of semiconductor names, leading to outperformance in the US Tech, South Korean, and Japanese equity markets, while the ROW has underperformed massively.

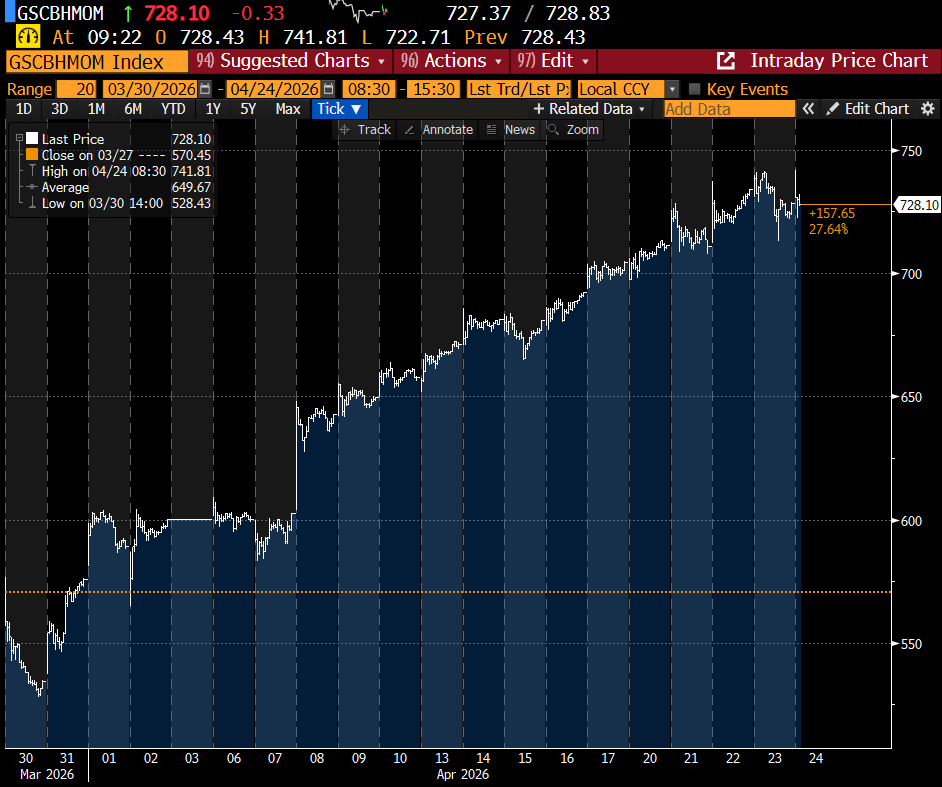

The GS High Beta Momentum Long Index (GSCBHMOM) is recording its second-best 18-day run on record, surpassed only by June ‘00, which followed the initial -60% crash off the March ‘00 peak.

The only other times high-beta momentum achieved a 30%+ gain over 18 days to a 52-week high were Nov. ‘99 (+34%) and Feb. ‘00 (+33%). This is therefore the largest 18-day gain into a new record high.

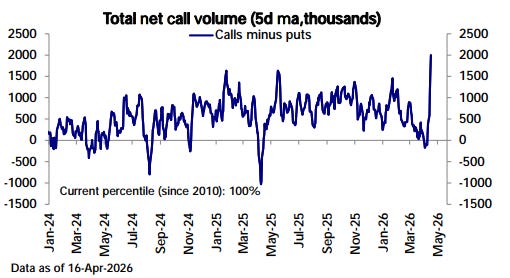

Furthermore, the casino is back as speculative activity hit multi-year highs.

The total net call volume has surged to a fresh 2.5-year high.

Moving on, with the failure of the Islamabad talks and a fragile ceasefire, we might be on the cusp of Round 2.0 of escalation. Note that the tensions are running high as the US utilises all the available tools for the naval blockade, while Iran has blocked all the traffic in the SOH as frequent skirmishes become the norm.

It’s really challenging to predict how this ends, as nobody knows the extent to which both sides will really go to control the Strait.

Macro has taken a back seat as geopolitics takes centre stage, and we are on the cusp of chaos in the energy markets. We are already witnessing the cancellation of tens of thousands of flights worldwide as it becomes unprofitable for airlines to operate amid an explosion in jet fuel prices.

Note that we believe this might be the beginning of a prolonged energy crisis, especially if the situation in the Middle East deteriorates further.

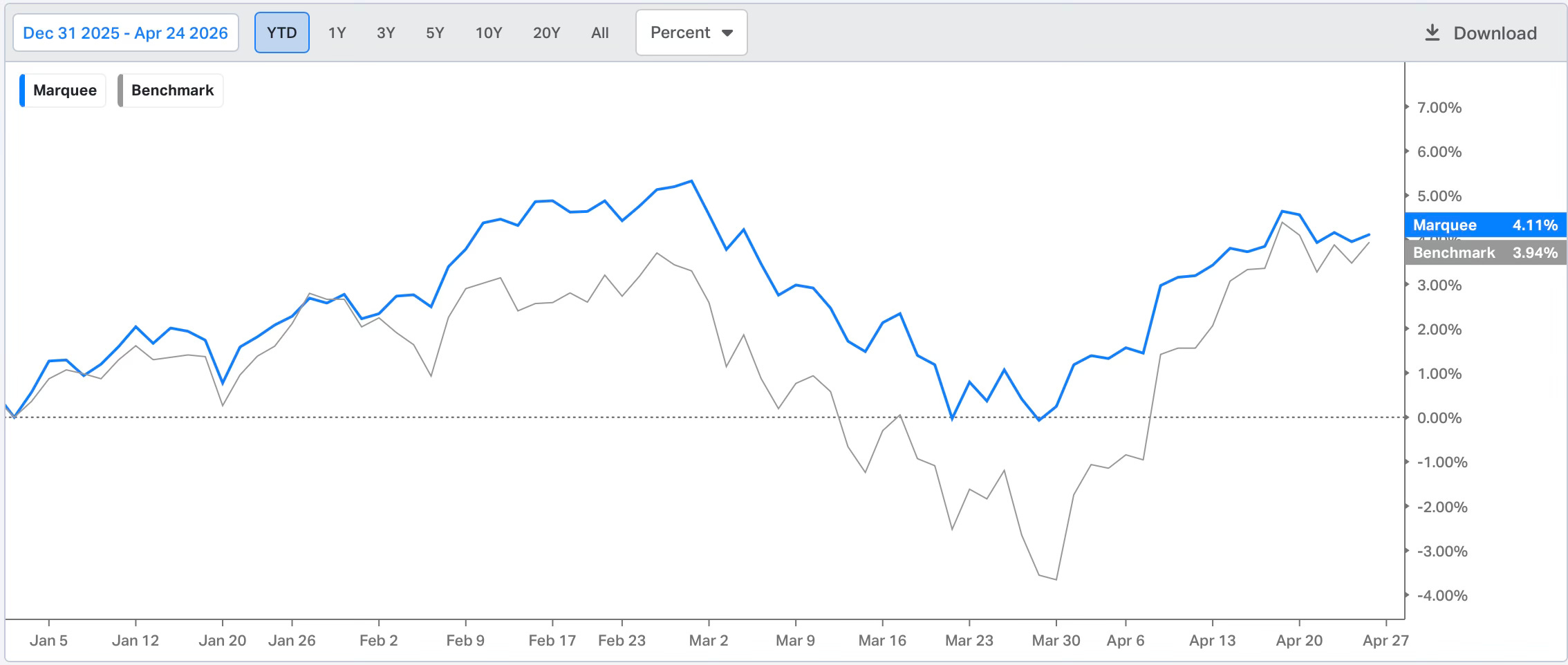

We raised cash two weeks ago, and as a result, the significant alpha we generated has diminished, with the PF now up 4.11% versus 3.94% for the benchmark.

Let us take a deep dive into the macro universe and decipher the cross-asset puzzle.

US/Equities/Bonds/Oil/Dollar/Gold!

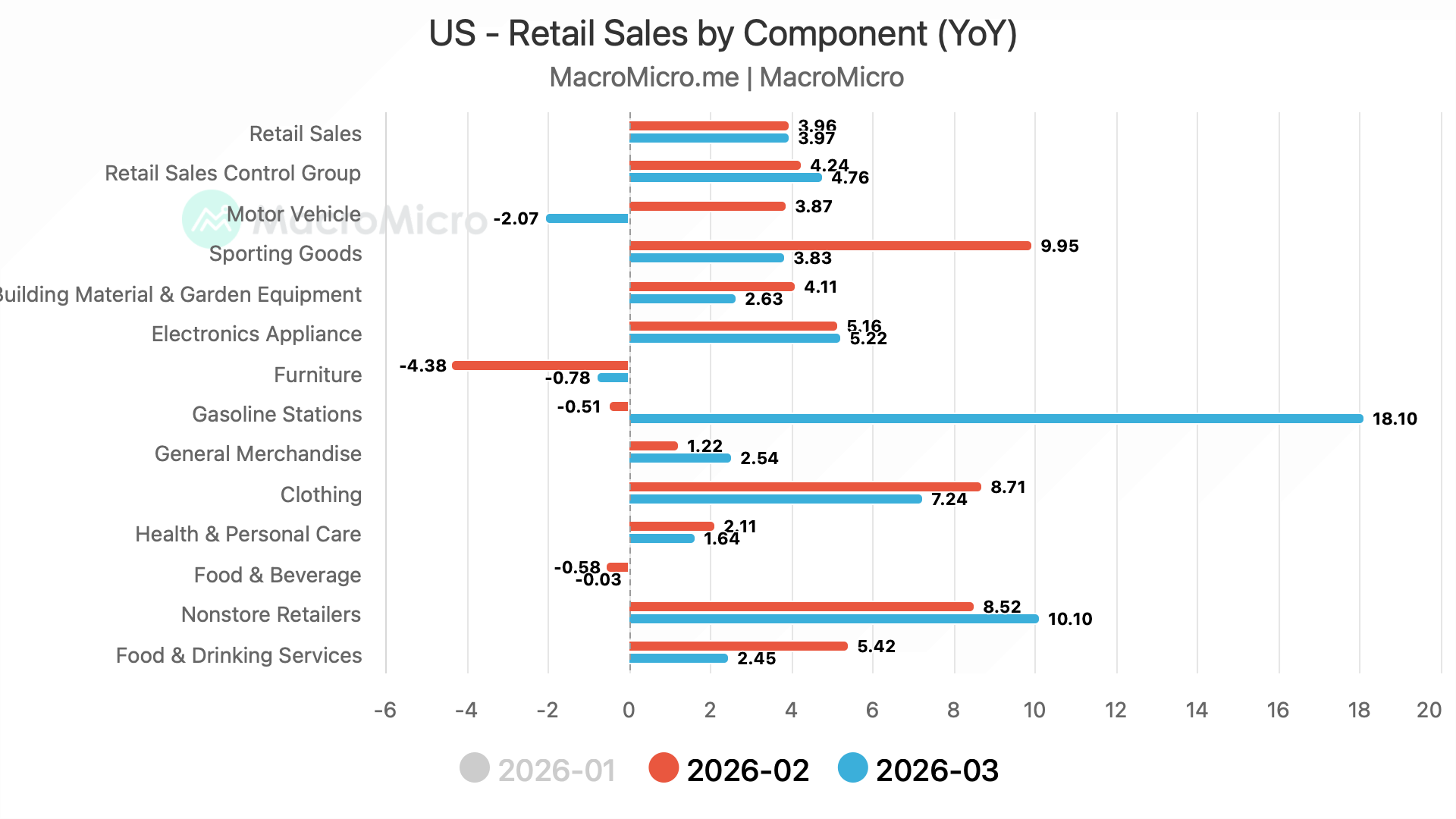

We begin with retail sales data, which is the best measure of consumption in the US (65% of US GDP is consumption).

It was an all-round beat, with headline retail sales growing 1.7% vs exp. 1.4%.

Retail Sales Ex-Auto grew by 1.9% v/s exp.1.5%, and the Control Group grew by 0.7% v/s exp. 0.2%.

While non-store retailers (online sales) have been on a tear, growing in double digits YoY, Furniture (housing slowdown) has been a drag (down -0.78% YoY).

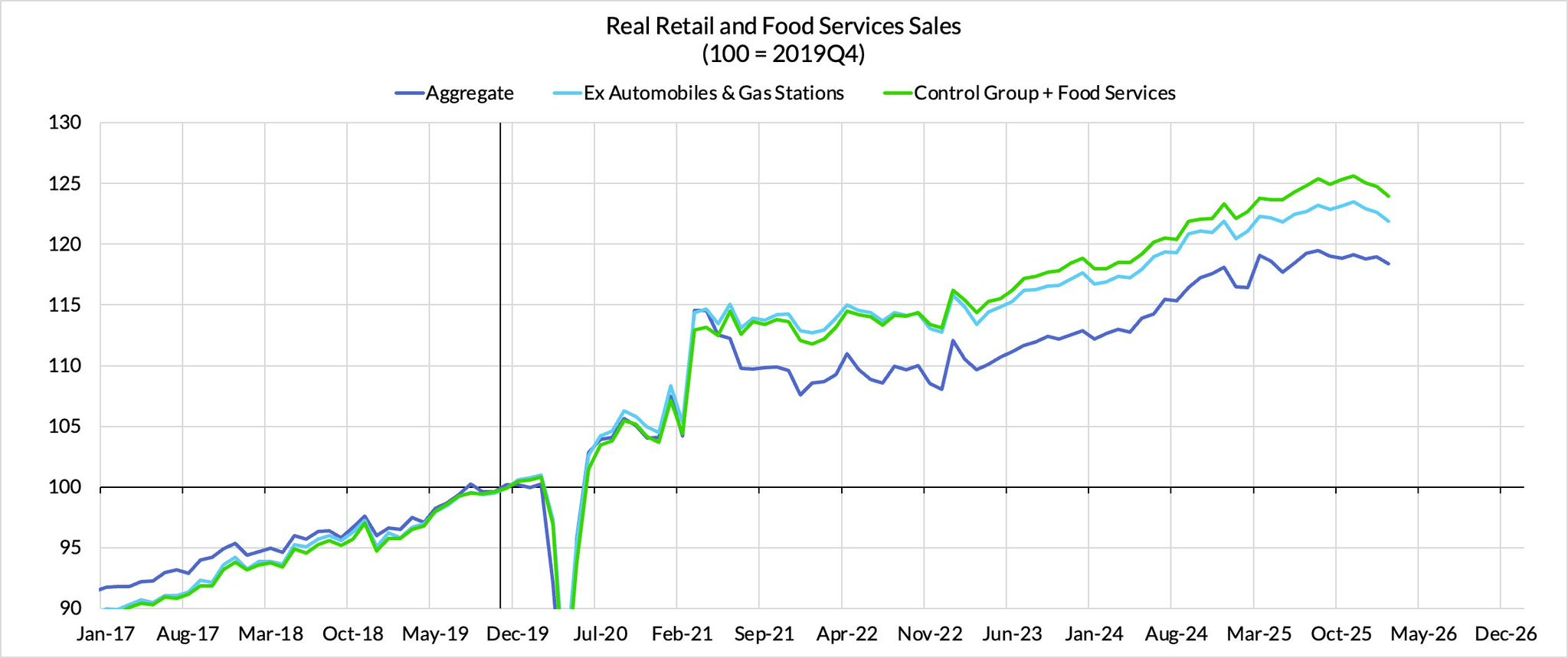

Nevertheless, real retail sales (adjusted for inflation) have disappointed and are below their peak, indicating that nominal retail sales growth has been driven by value rather than volume.

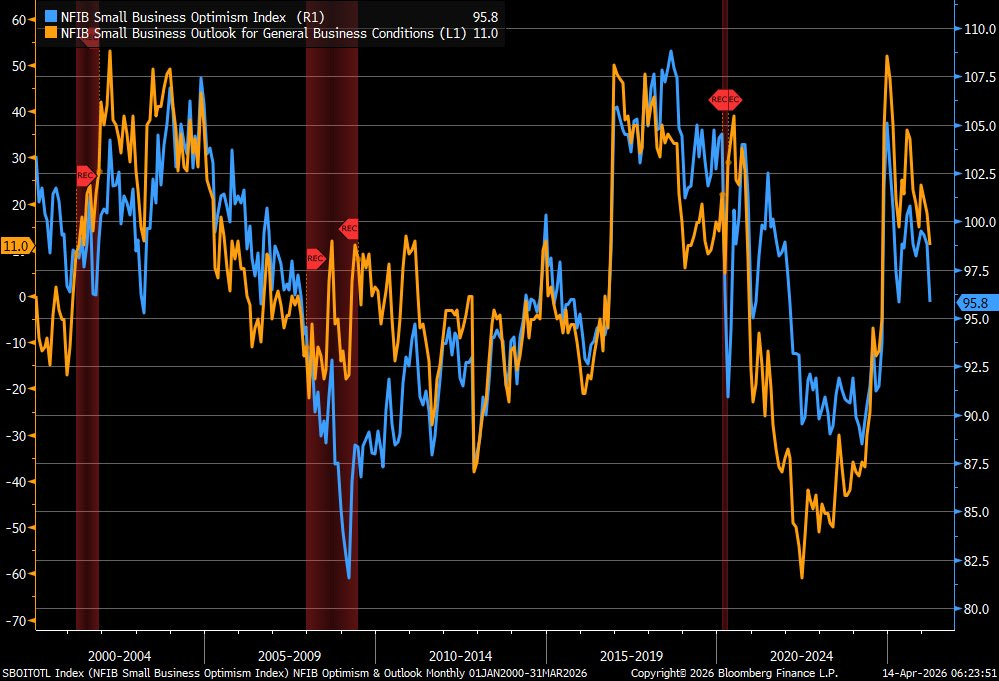

Last week, we received the NFIB Small Business Survey, which we monitor to understand small businesses’ sentiment.

The headline index plunged to 95.8 v/s exp. 97.9, indicating waning sentiment due to war-related uncertainty.

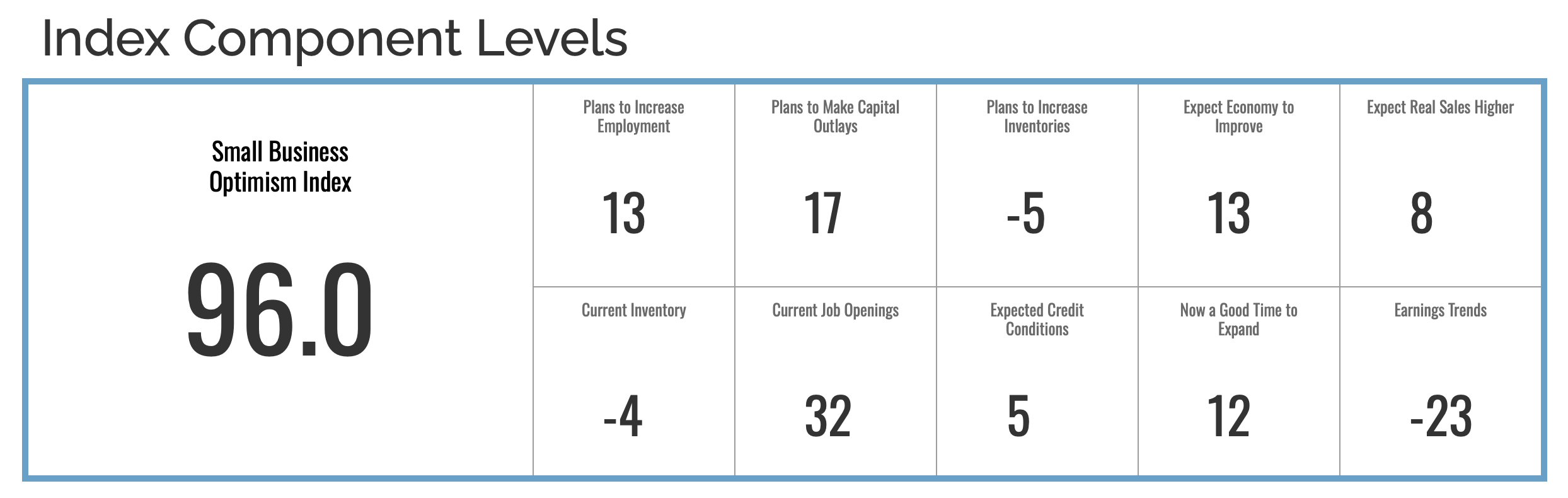

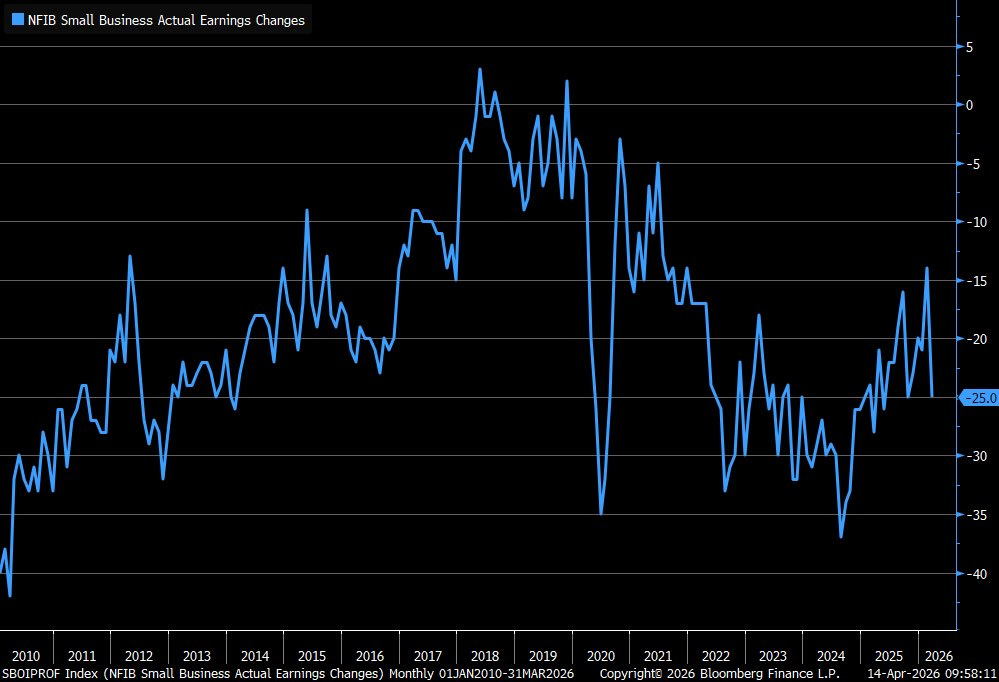

When we dig deeper, the shocker came from the earnings trends, as it was the single biggest sub-component to drag the headline index lower.

The net % of small businesses reporting positive fell 11 points to -25%.

The NFIB job report was a mixed picture.

A seasonally adjusted net 12% of owners plan to create new jobs in the next three months, unchanged from February.

PS: Note that this is at one of the lowest levels since 2018 and the measure has failed to move up.

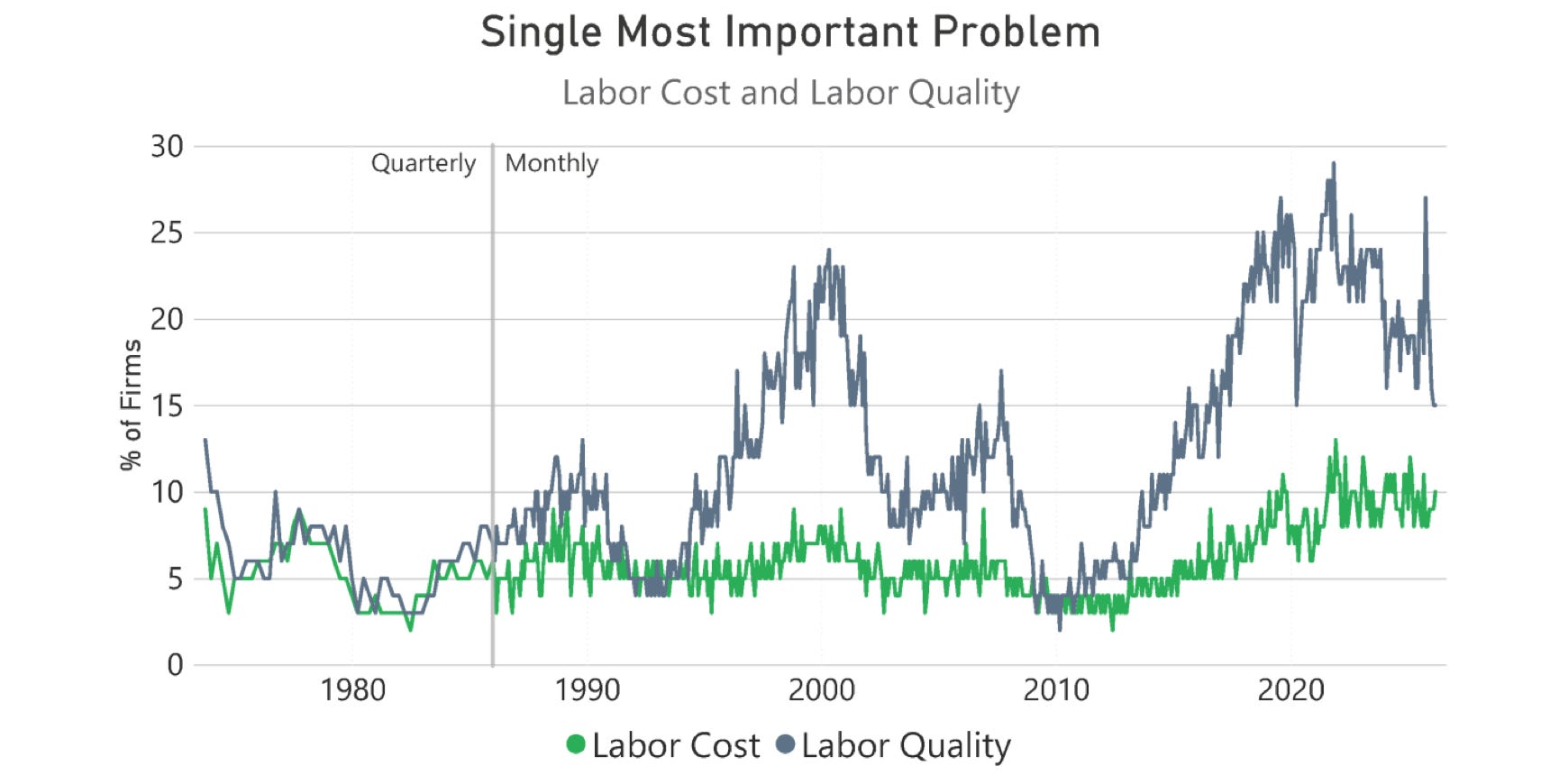

While labour quality has declined over the past few months, reports of labour costs as the single most important problem have gradually increased.

10% of business owners reported labour costs as their single most important problem, up 1% from February.

The last time labour quality, reported as the single most important problem, was below 15% was in December 2016.