The CB "Conundrum"!

When COVID-19 wreaked havoc on our beautiful planet, central banks, along with governments, unleashed trillions of dollars in stimulus to mitigate the impact of draconian lockdowns, which led to a screeching halt in growth.

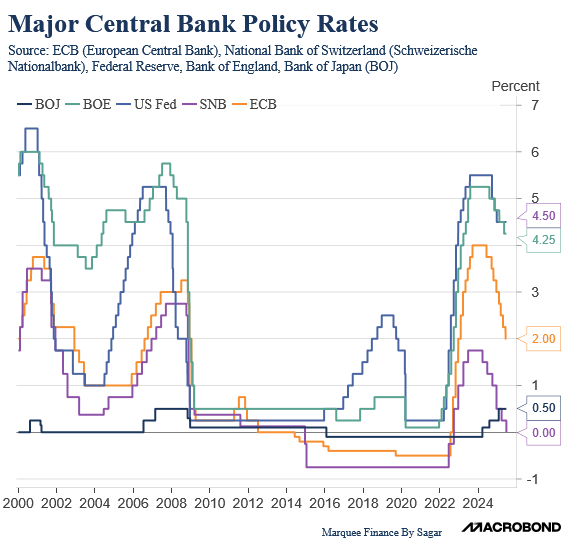

Nonetheless, the gargantuan flood of stimulus led to a resurgence of inflation after more than 15 years. The response to the “transitory inflation” fiasco was one of the most aggressive tightening of monetary policy by central banks (EX, the BOJ and PBOC).

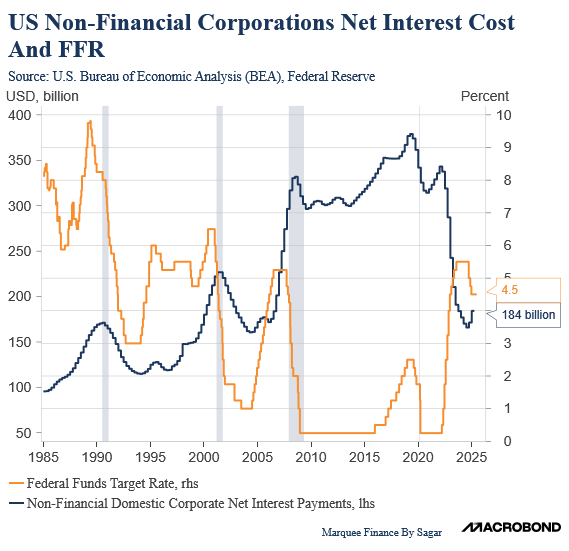

However, despite the recession concerns, the much-anticipated slowdown didn’t arrive as the ultra-loose fiscal policy negated the effect of the tight monetary policy. Furthermore, deleveraged US corporates (private sector) and HHs meant that the higher rates ultimately benefited the cash-rich American corporations.

As the economy experiences a K-shaped recovery, lower-income households are suffering, as indicated by high-frequency data (such as delinquency rates, consumer sentiment, and credit card data), suggesting rising stress.

Nevertheless, the trade policy of the Trump administration has overshadowed the macro concerns, and the world’s most powerful central banker has refused to lower rates unless there is clarity regarding the tariffs and inflation trajectory.

On the contrary, the SNB became the first CB in the post-COVID world to return to zero rates.

Bearing another energy shock, inflation is expected to behave in Europe, and as a result, the ECB and SNB, along with other Central Banks (CBs), have been proactively reducing rates.

Nonetheless, if inflation flares up due to the energy shock, the CBs will be in a conundrum, as growth has been stalling.

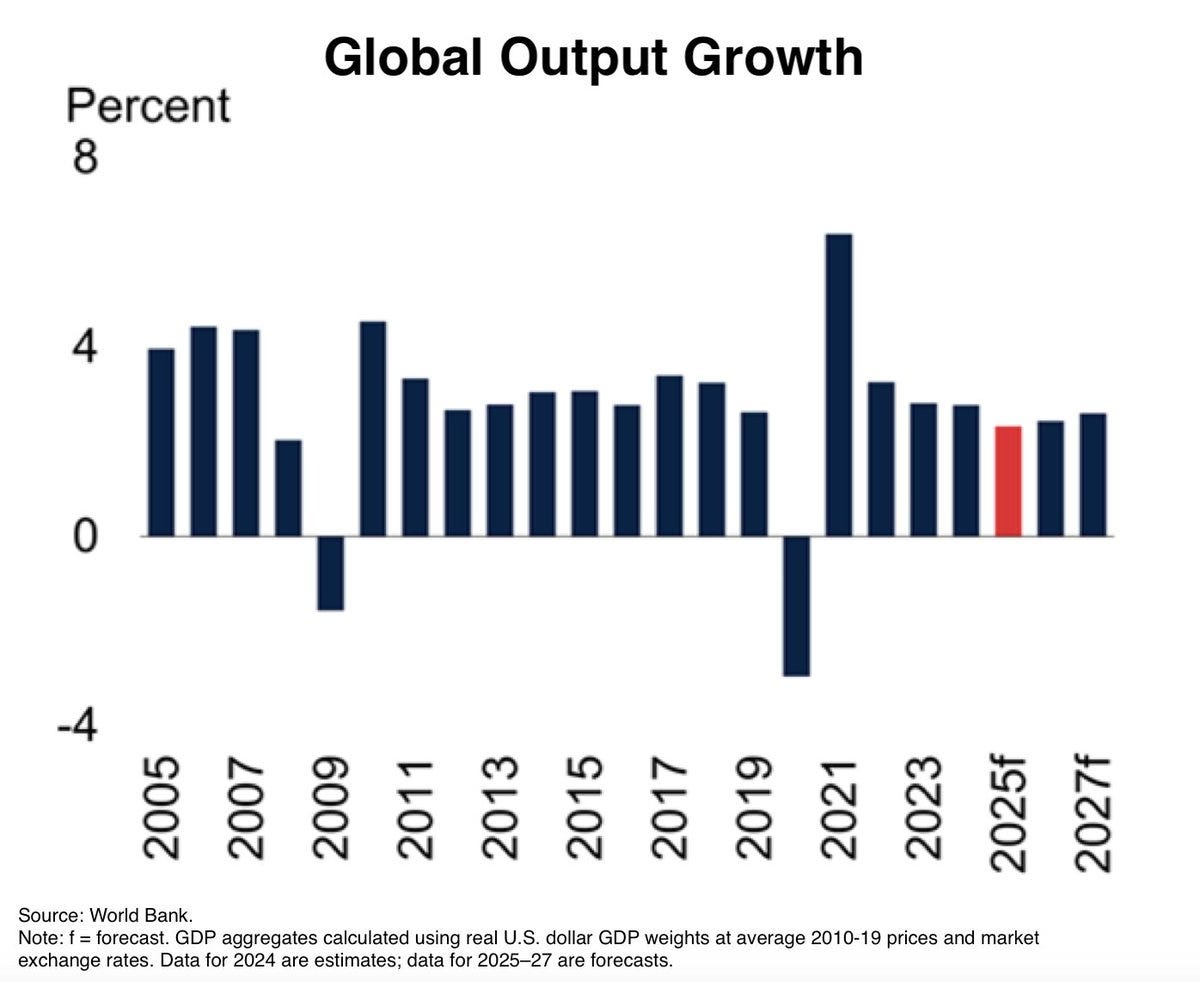

According to the World Bank, global growth this year will be the lowest since the 1960s (except for the crisis years of 2009 and 2020).

As the war rages in the Middle East and the US is on the verge of joining the war to bomb the Fordow Nuclear Facility, we are on the cusp of a major escalation which can lead the world to World War 3.

The role of monetary and fiscal policy, and thus macro, becomes increasingly important as the world heads towards chaos with no leader advocating peace and none adhering to it.

Let’s dig deeper into the macro world and

US/Bonds/Dollar/Gold/Oil!

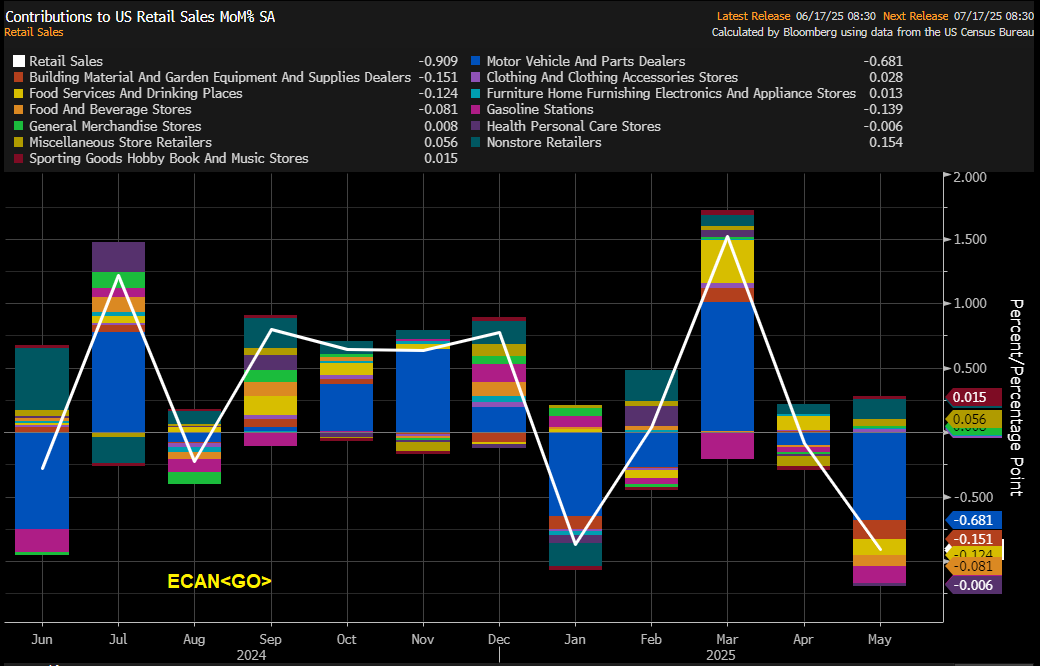

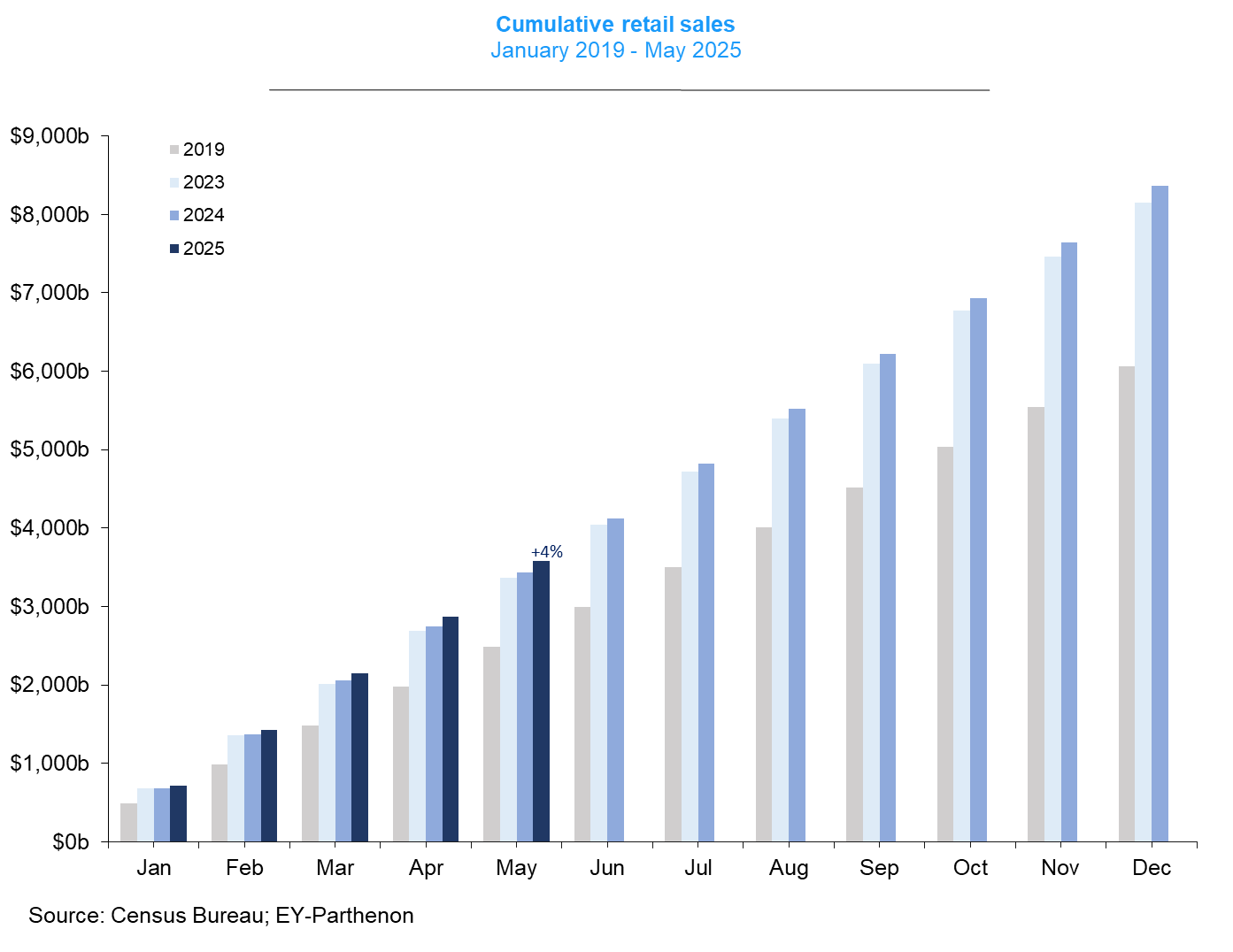

Although this was a data-light week (excluding housing data), the highlight was the retail sales, which is one of the most crucial macroeconomic data points outside the labour market and the CPI/PPI data.

This is because roughly 60% of the US economy is driven by consumption, and faults in consumption are first visible in retail sales.

Retail sales data has been noisy due to the front-loading of the tariffs, with a massive jump in March.

As a result, we are now witnessing some cooling off, with the MoM number at -0.9% v/s expected -0.6%.

A significant weakness was observed in Retail Sales Ex-Auto, which came in at -0.3% MoM compared to the expected +0.2%.

Nonetheless, when you zoom out and look at the broader picture, one will be disappointed that the cumulative “NOMINAL” retail sales are up by only 4% (and this includes the massive front-loading due to tariffs).

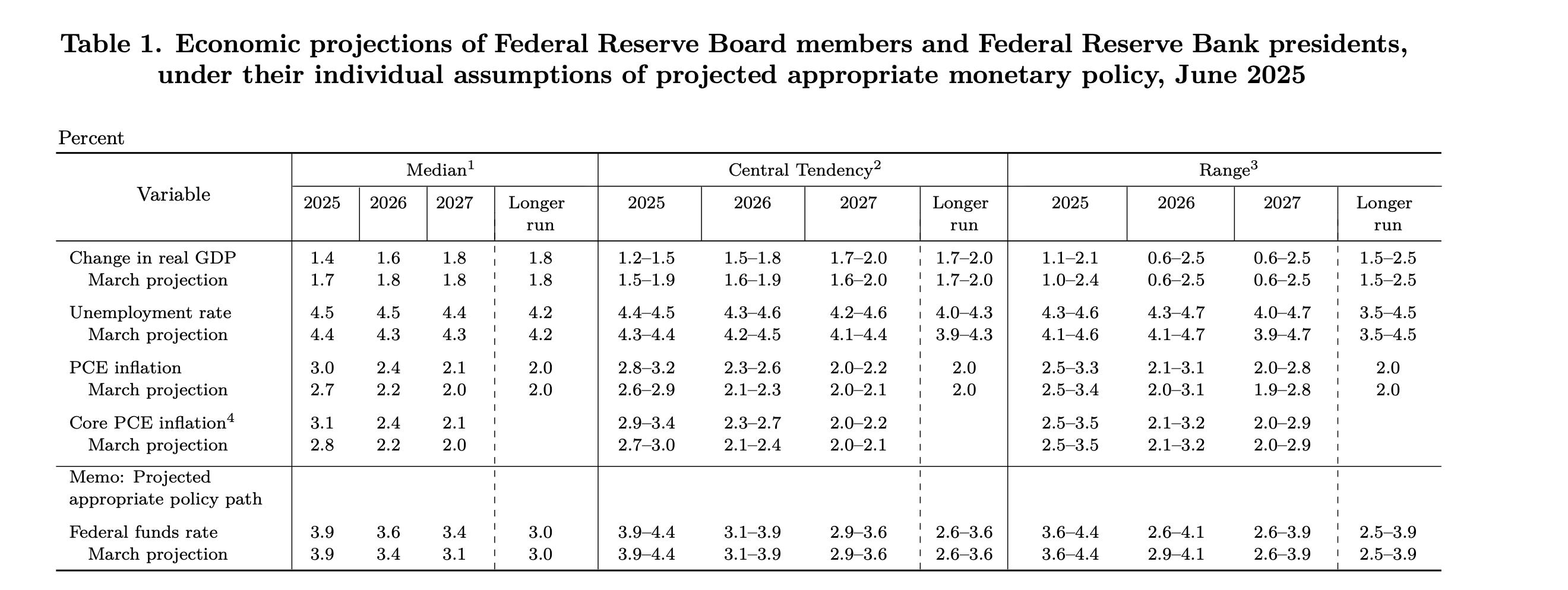

Let’s jump to the most significant event of the week, which was the Fed policy.

It was time for the dot plots, and the summary is as follows:

Growth projection for 2025/2026 was revised lower from the March projection. The Fed now expects the US economy to grow at a rate of just 1.4%.

The Unemployment Rate (UR) was raised higher by 10 bps to 4.5%.

The PCE inflation and Core PCE was raised significantly higher by 30 bps and 20 bps to 3% and 3.1% respectively.

There was no change in the long-run FFR.

However, the biggest surprise was…