The "EPIC" Reversal!

“Every great narrative is at least two narratives if not more- the thing that is on the surface and when the things that are invisible.”- Ali Smith.

Once again, we have defeated the most powerful narratives floating around social media.

At the beginning of the year, there was a consensus about the long duration trade as markets expected 7 rate cuts in 2024 beginning from March. We booked profits in December in our long TLT trade and stayed away in most of the H1 from going long duration.

The second narrative that gave us an excellent opportunity to go long on the shiny yellow metal (Gold) was the sudden halt in purchases by the Chinese Central Bank. Social media was inundated with Chinese news and predicted that the bull market was over.

However, our paid subscribers will appreciate that we increased our long GLD position at the most appropriate time (we may have been lucky this time).

Nonetheless, there are always hits and misses. The macro data and the valuation scenario kept us from going overweight stocks (though we had some great returns in our value picks).

Furthermore, a confluence of factors (geopolitical, domestic US political circus, and macro) will determine the future outlook of cross-asset movements, which we will discuss today.

PS: Since I am travelling this week (on a vacation to beautiful Turkey), next week's month-end newsletter will be delayed by 2-4 days. Furthermore, paid subscribers can get live macro updates on the chat section as we will be active on chat this time.

US!

Let us begin today with the political developments in the US, which shocked the entire world.

Across the global financial system, there was a knee-jerk reaction on Monday, with long-term yields rising, BTC crashing up and a general move higher in risk assets as the odds of a Trump win increased significantly.

However, as we wrote to our paid subscribers, the move faded by the market closing, as politics can be unpredictable.

The one thing that can be said with a 100% probability is the rise in volatility as uncertainty looms regarding the path of US government policies.

The beauty of macro data is that you can shape or portray it in any way you like and create a narrative.

We have long mentioned that the data quality has significantly deteriorated in the US, increasing the probability of a hard landing.

This was visible this week as well.

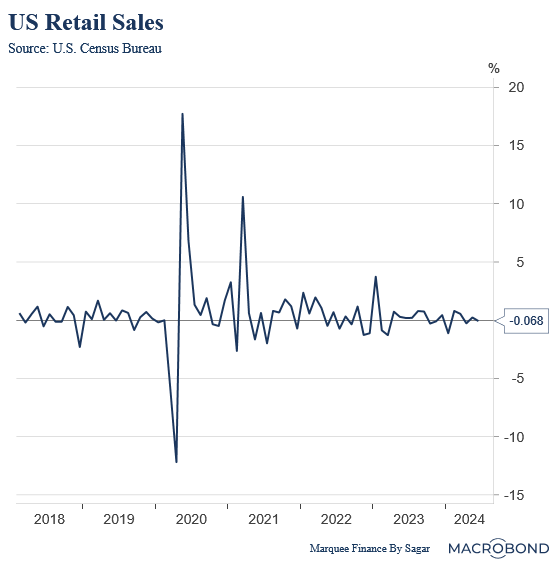

On the face of it, the retail sales data, the most significant data release of the week, came in much ahead of expectations.

But (and there is always a but) the devil lies in details.