The Epic "Tug Of War"!

You might be wondering about the title “epic tug of war” as there has been no news about a war breaking out.

Folks, we are talking about the all-out war that has been declared by Trump and his administration on bond vigilantes.

In what could be termed a sea change from the first Trump presidency, when he was laser-focused on “stock markets,” the current administration has set its sights on lowering the benchmark yields (USTs) by hook or by crook.

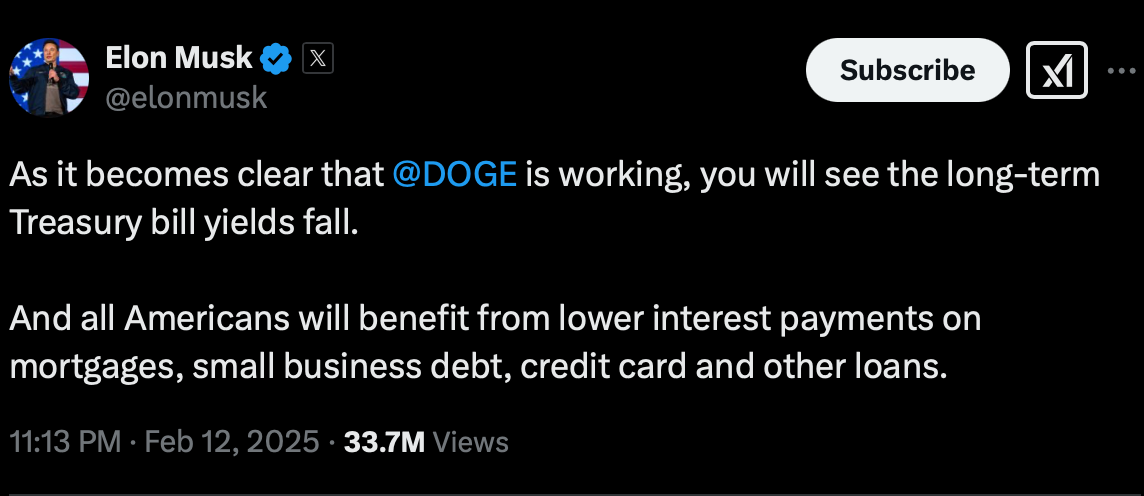

In fact, even the world’s richest man posted on X about lowering the long-term yields (though technically, he got confused between bills/notes).

As a result of the administration’s (Bessent, Trump, Musk) constant chatter about lowering rates, yields erased all the gains this week.

In a stunning move, the 10Y is now below the pre-CPI levels.

Today, we will discuss in detail whether Bessent (Treasury Secretary) would be successful in his mission (and if they are determined, what the path to lower yields would be) and what the repercussions will be on the cross-asset markets of lower yields.

Furthermore, we will also analyse the macro data in detail and discuss our conclusions.

US!

This week was crucial as we got the all-important CPI and PPI data, which led to wild moves in bonds and even in equities.

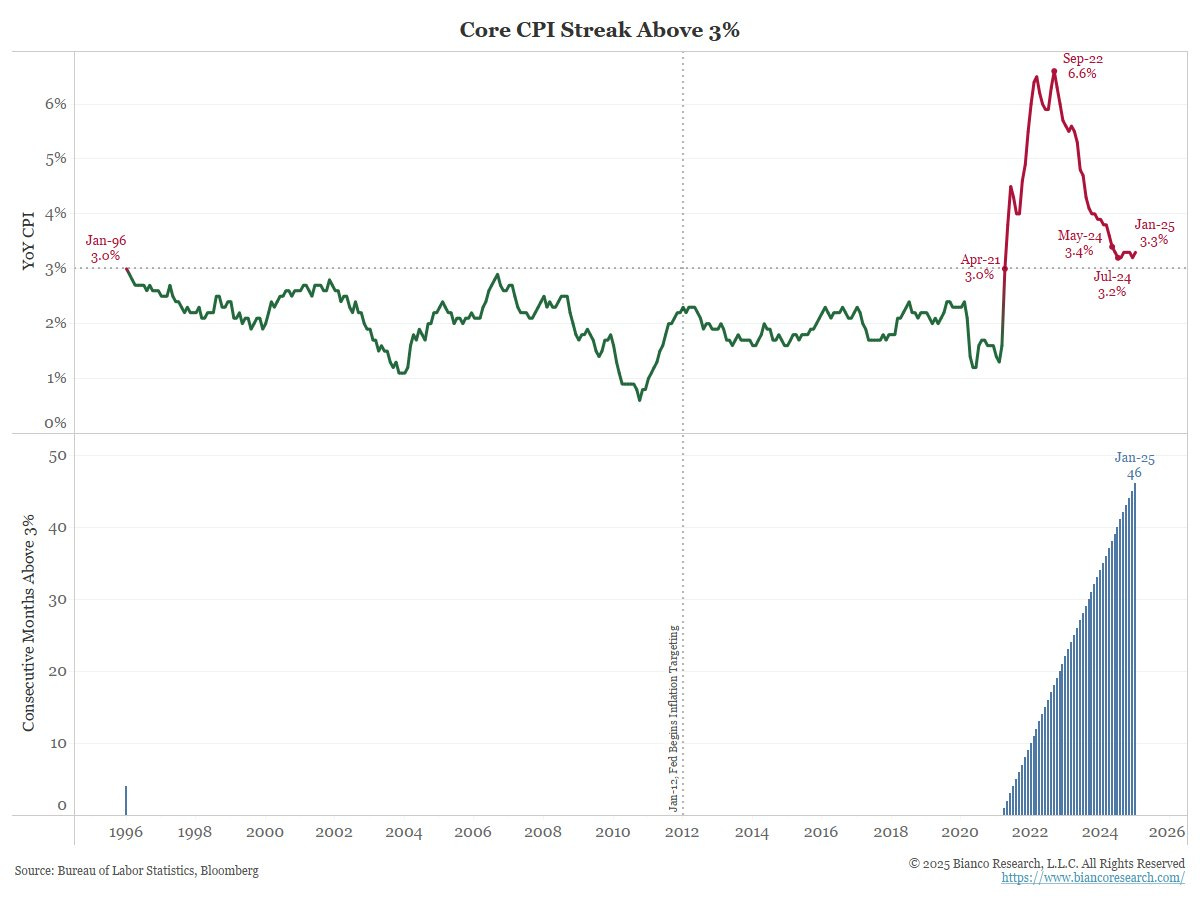

CPI came in hotter than expectations, with MoM Core inflation now above 3% for more than 46 months in a row, a record that was last seen only during the period of draconian inflation/stagflation in the 1970s and 1980s.

Higher food prices have been on a tear since the last few months, especially with rise in egg, orange juice and cocoa prices, all of which have hit the roof, thus hitting the bottom end of the consumers hard.

Note that the US FAO Food Price Index is down from its peak in December and the US CPI Food Index lags the FAO by roughly three months, so we might see some cooling off in the US Food CPI only beginning late Q2.

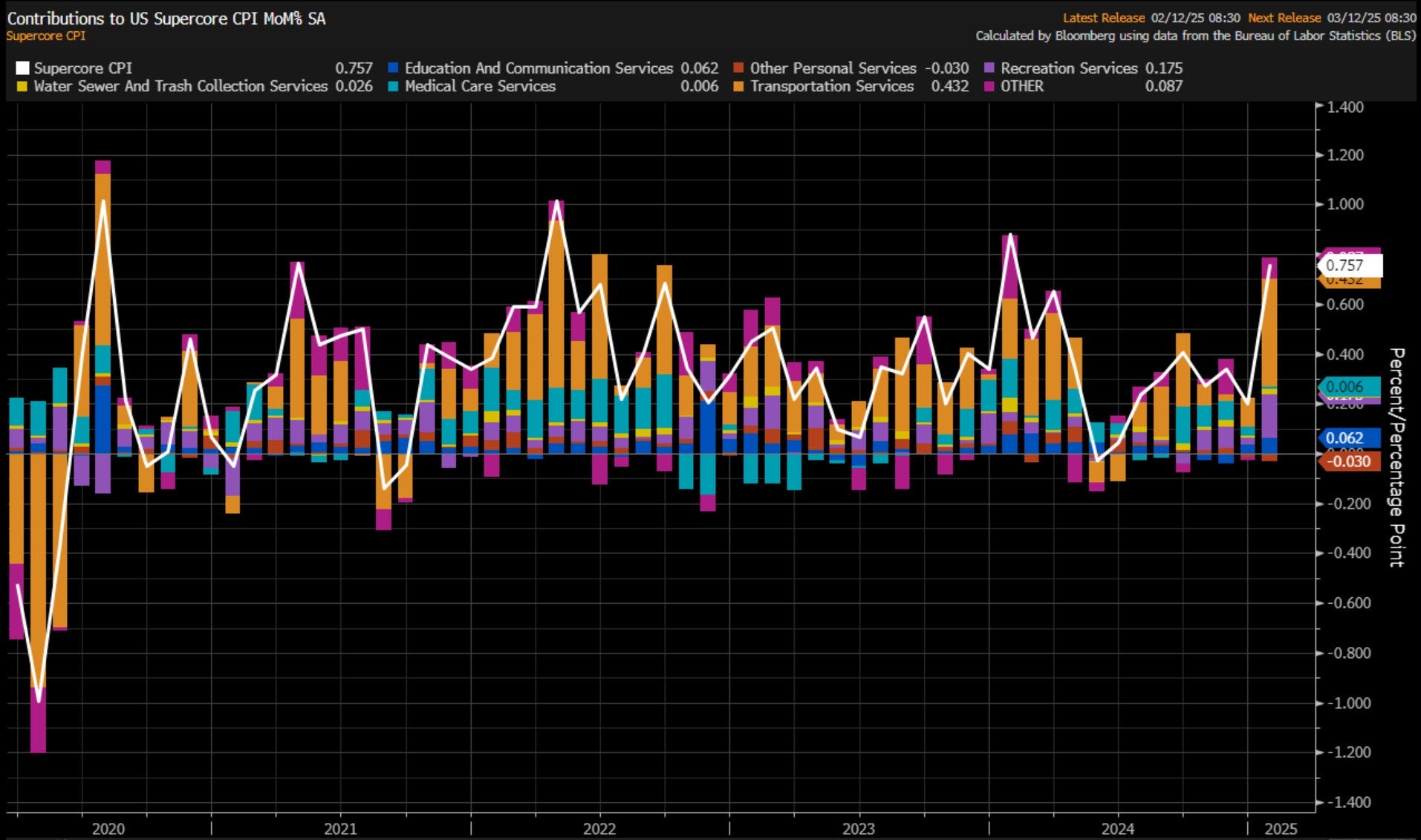

Furthermore, the US Supercore (Services Ex-Housing) popularised by JayPo rose sharply in January (0.75% MoM), with transportation services as the most significant contributor.

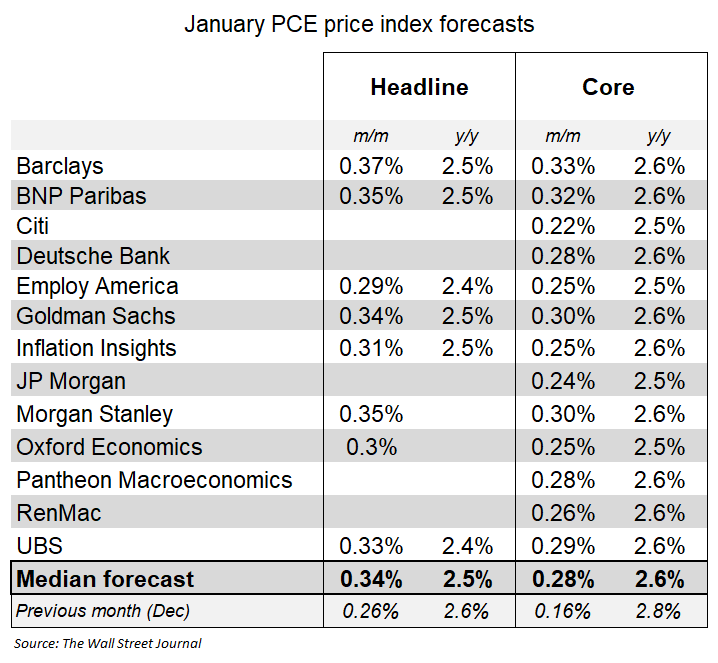

Nonetheless, the markets shrugged off the higher CPI print as “some components” of Producer Price Inflation (PPI), which is fed into the PCE, came in softer than expectations. As a result, the January core PCE is expected to come in lower than December.

So, let’s now move to our guidance on the CPI, which we have been providing every month for the last few months.