The "Fairytale" Landing!

“Once in a while, right in the middle of an ordinary life, God gives you a fairytale.”- Unknown.

The human mind is designed to concentrate exclusively on a few things at a particular time. If you inundate it with a flood of narratives: the result is confusion which leads to an erroneous decision, thus benefiting those who spread those narratives.

The current narrative being promoted by the who’s who of the finance world is the imminent “soft landing” (inflation will be brought under control without sacrificing growth and keeping a lid on the unemployment rate) that the US economy will undergo. The social media biggies have forgotten the words JayPo echoed last year during the Jackson Hole.

Friends, I would like to remind you about JayPo’s statement:

“While higher interest rates, slower growth, and softer labour market conditions will bring down inflation, they will also bring some pain to households and businesses.”

Risk assets are partying like never before, thanks to the buoyant liquidity still sloshing around the system.

Nevertheless, it’s time to be cautious as Fed has some unfinished business left, and the variable lags have distorted the true macro picture and led us to believe that we have got a “fairytale” landing in sight.

Let us understand the economic data and the lags in the housing market to understand the economy's direction!

US Economic Data And Housing Deep Dive!

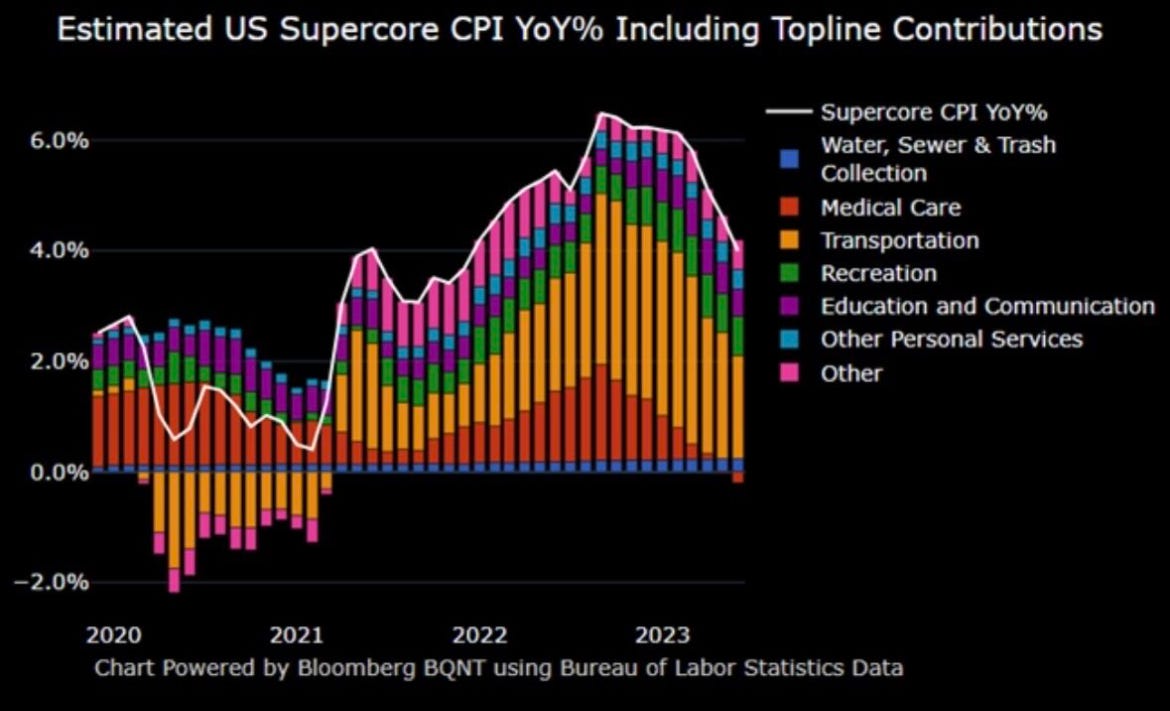

Since we had the portfolio update last week, we didn’t get the time to discuss the uber-important CPI data, which triggered an enormous rally in risk assets on the false hopes of a “soft landing”.

While the headline print came in at 3%, the supercore inflation, which the Fed tracks closely, also demonstrated initial signs of plateauing.

One of the surprises was the negative contribution of Medical Care which will get reversed in October due to some methodological changes (market participants expect an increase of up to 2-3%), which will act as a tailwind for higher inflation.

Furthermore, the base effect, as we predicted, will wane off from July onwards. There is a high probability that the second bout of inflation will transpire before the end of the year as the positive wealth effect leads to higher spending and supports the economy in an election year.

On the contrary, certain headwinds remain for consumption to move higher from here on.