The Fragile AI Story!

The US capital markets saw a historic milestone with SpaceX's IPO, which raised $75 billion, marking it as the largest IPO in history.

The focus now entirely shifts to the upcoming Anthropic and OpenAI IPOs.

As both companies prepare for their IPOs, growing cracks in the AI narrative may dent their prospects.

Yesterday, the US Government issued an export control directive suspending all access to the latest Anthropic models (Fable 5 and Mythos 5) for any foreign national.

In response, the company disabled the models for “ALL” users.

For the last few weeks, we have been mentioning that cost increases for firms due to rising token prices will lead to a substantial fall in usage.

The LLM Token Expenditure Index is now back to its January level, when the Agentic AI market exploded.

As it becomes super expensive to use AI (no productivity advantage yet), even the big tech firms are pulling back. In yesterday’s news:

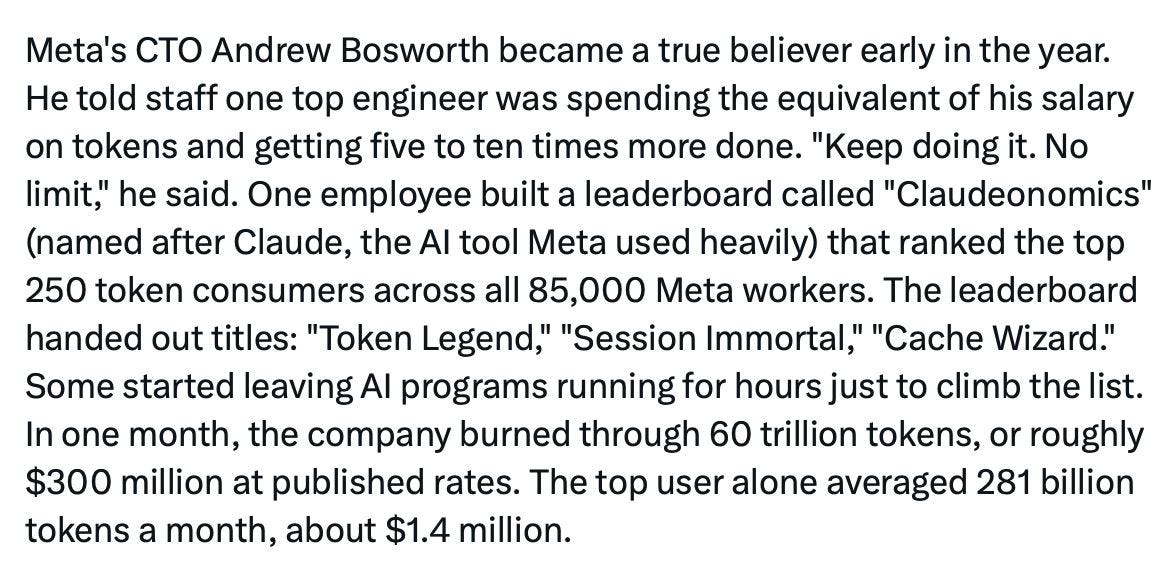

META MOVES TO LIMIT EMPLOYEE AI USAGE AS COSTS REACH BILLIONS.

Note that this comes after a “Max Token” culture was widely promoted across the company.

Furthermore, we now believe that the only way to increase AI adoption is through a price war.

A potential price war between OpenAI and Anthropic will likely compress margins and slow the path to profitability, while also raising questions about the durability of current AI valuations (thus eventually delaying their IPOs).

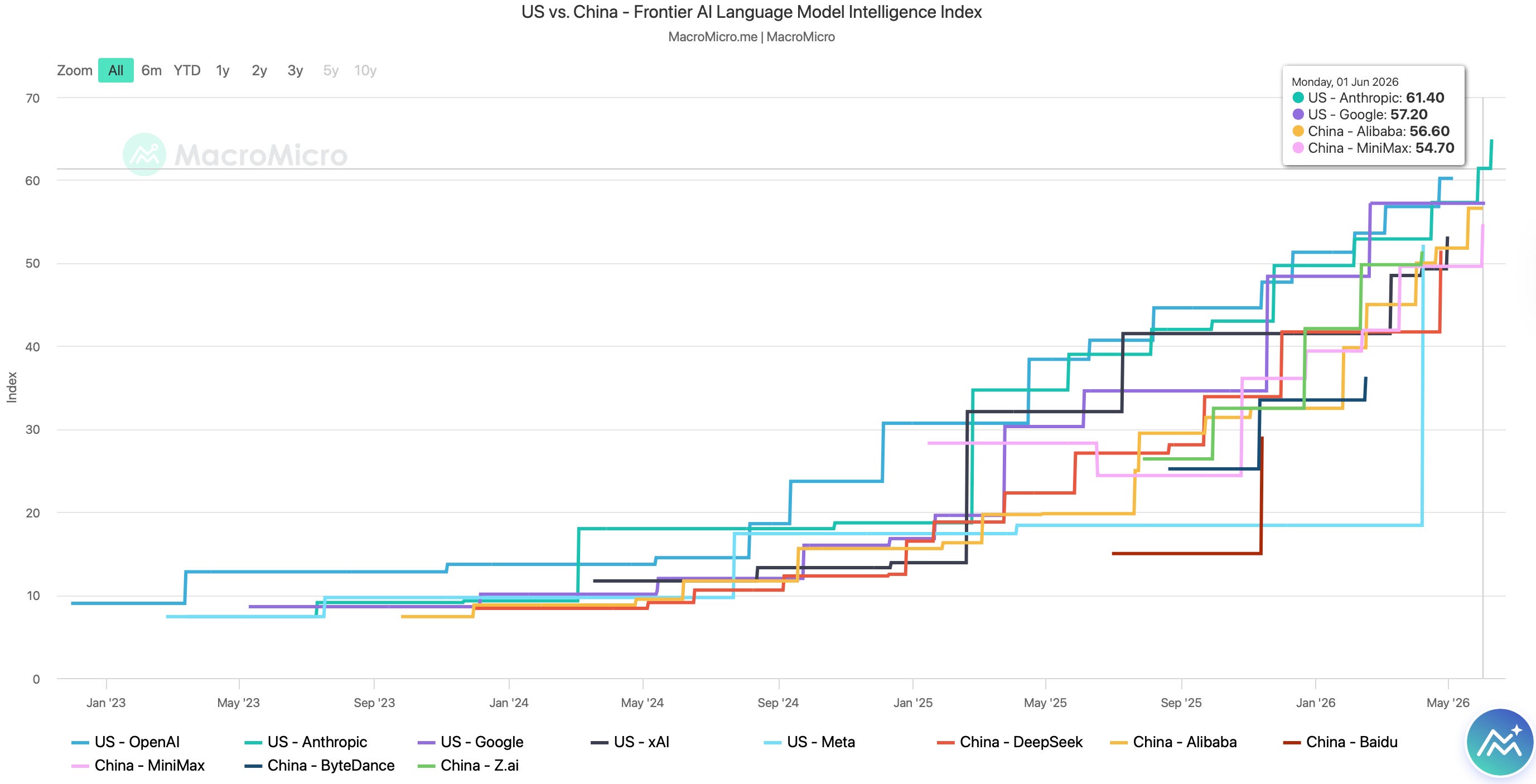

To make matters worse, the Chinese models are now gaining traction in the US as they are significantly cheaper than US models.

For those interested in comparison, you can check this cool website to track token pricing.

While they are significantly cheaper, they are not far behind in terms of intelligence.

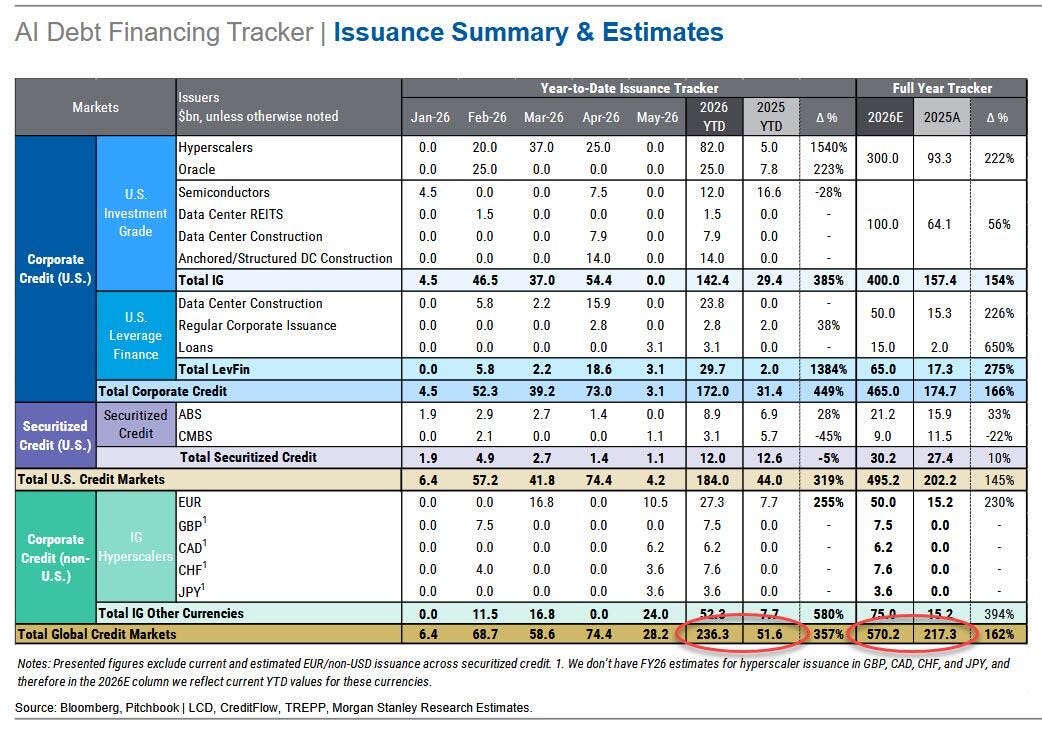

As concerns mount, the first casualty of the “bubble” will likely be the credit markets, with hyperscalers raising billions in debt to fund their capex.

Furthermore, the debt is held in SPVs (off-balance-sheet transactions), which raises concerns about defaults and the subsequent recovery.

According to Morgan Stanley, $236 BN in AI investment-grade debt has been issued YTD, a 357% increase YoY.

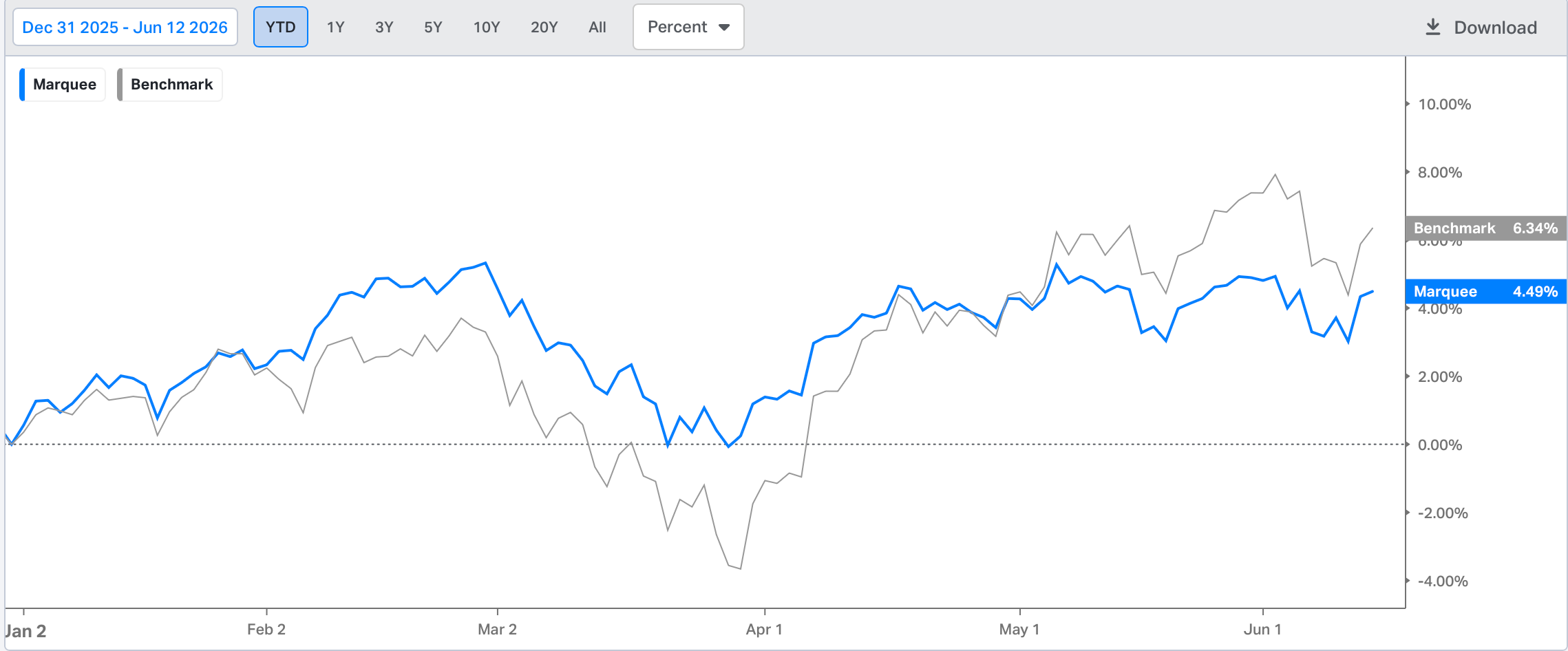

We have erased 100 bps of underperformance (we were underperforming by 250 bps at the peak of Semis mania).

We are up 4.5% YTD and remain confident we will outperform the benchmark in the coming weeks.

US/Equity/Bonds/Oil/Dollar/Gold/Silver!

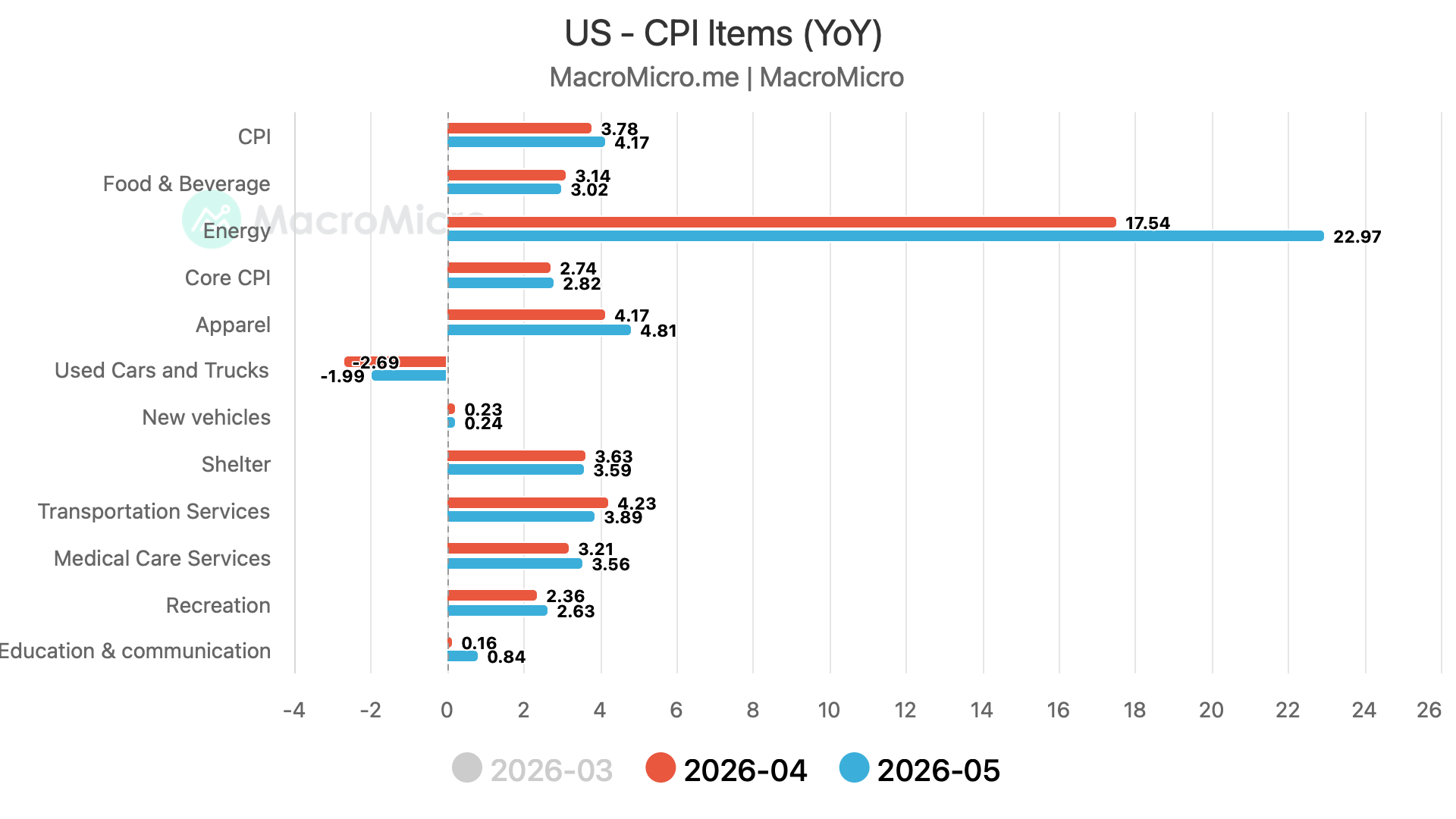

The much-awaited inflation data was released this week in the US.

The headline CPI came in at 4.2% YoY v/s Exp. 4.2%, while the Core CPI (ex-food and energy) came in at 2.9% YoY vs exp. 2.9%.

The headline was significantly higher, driven by a 23% YoY rise in energy prices.

While the core CPI remains below 3%, we expect it to rise gradually in the coming months as higher energy prices filter through the economy.

Note that the CPI is a lagging indicator.

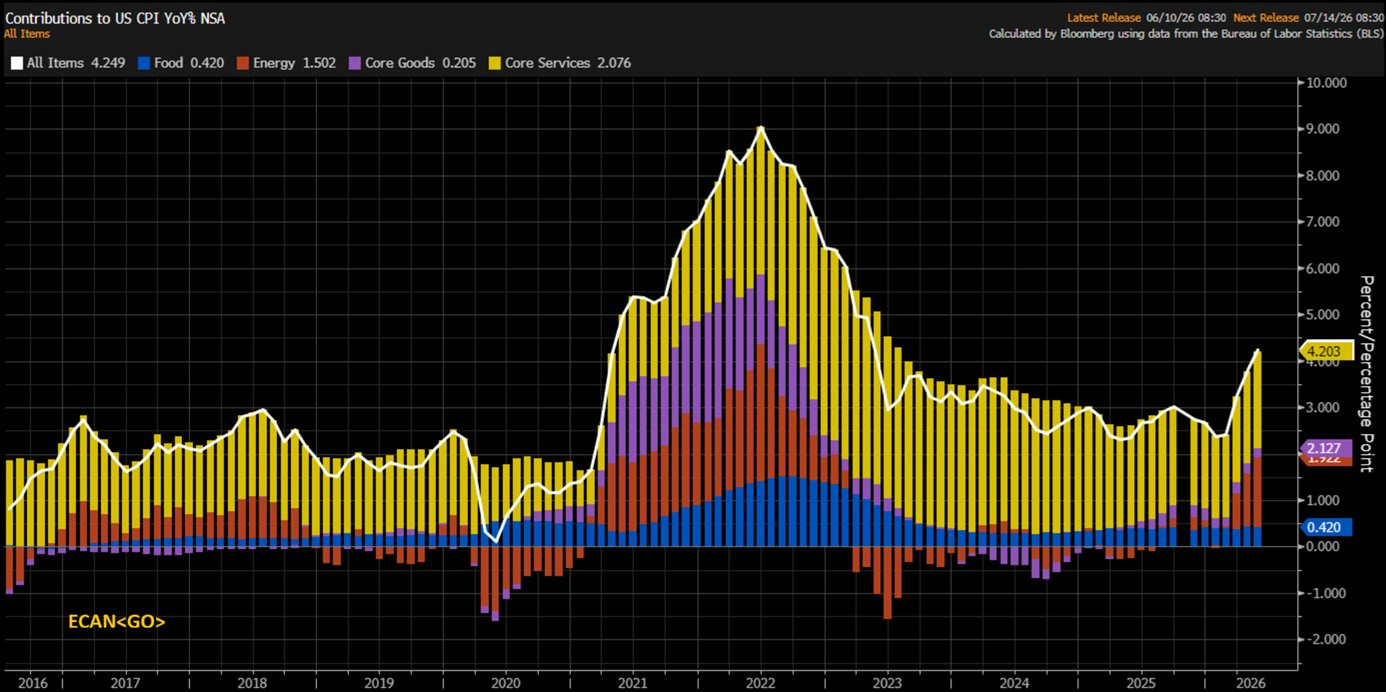

Core Services also saw a sharp jump with a 2.08% YoY rise, while Core Goods saw a small uptick.

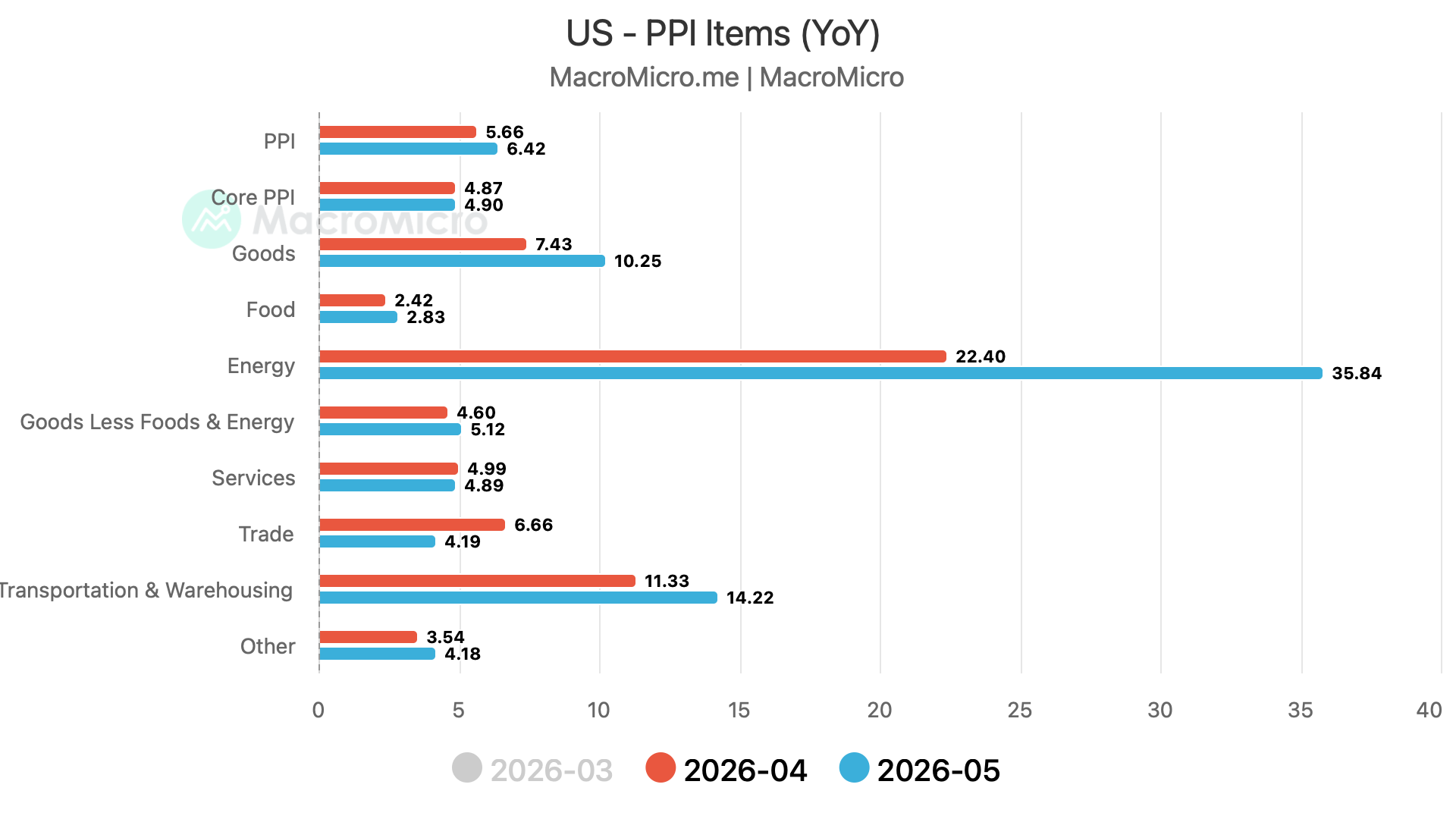

The headline PPI soared to 6.5% YoY in May v/s exp. 6.4%, while the core PPI came in at 4.9% YoY v/s exp. 5.4%.

Again, as expected, energy was the culprit, with a mind-boggling 36% rise YoY.

Goods and Transportation also saw a double-digit rise.

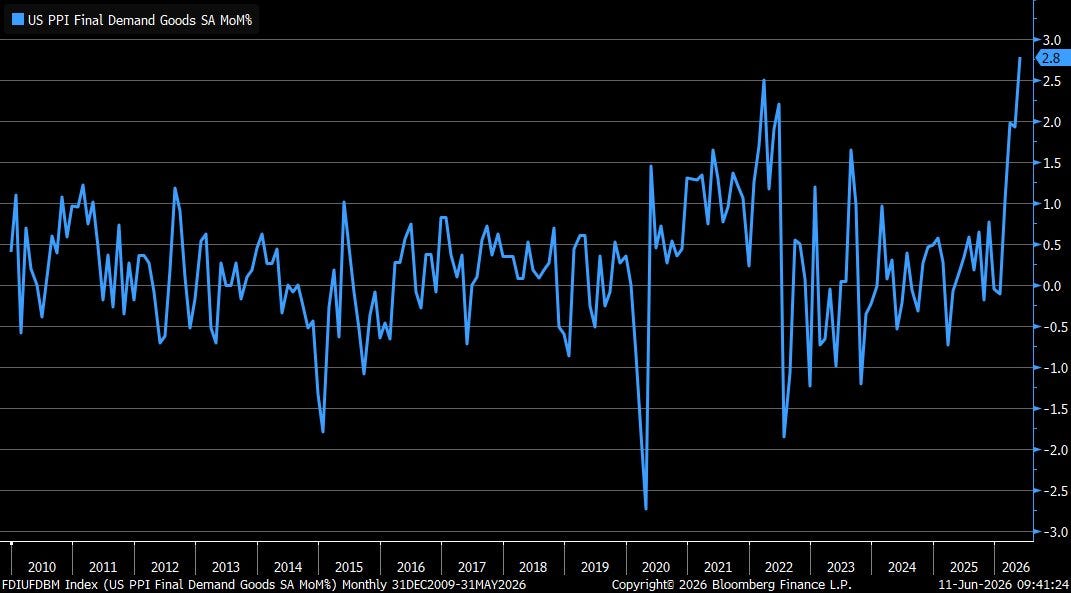

Final demand goods prices surged 2.8% in May—the largest monthly increase since the series began—and drove most of the acceleration in the PPI.

Higher PPI will eventually lead to higher CPI (albeit with a considerable lag) as firms gradually raise prices.

Small businesses are the backbone of the US economy, as they employ more than half of the workforce and contribute roughly 44% of the GDP.

Thus, we closely track the NFIB Small Business Survey.

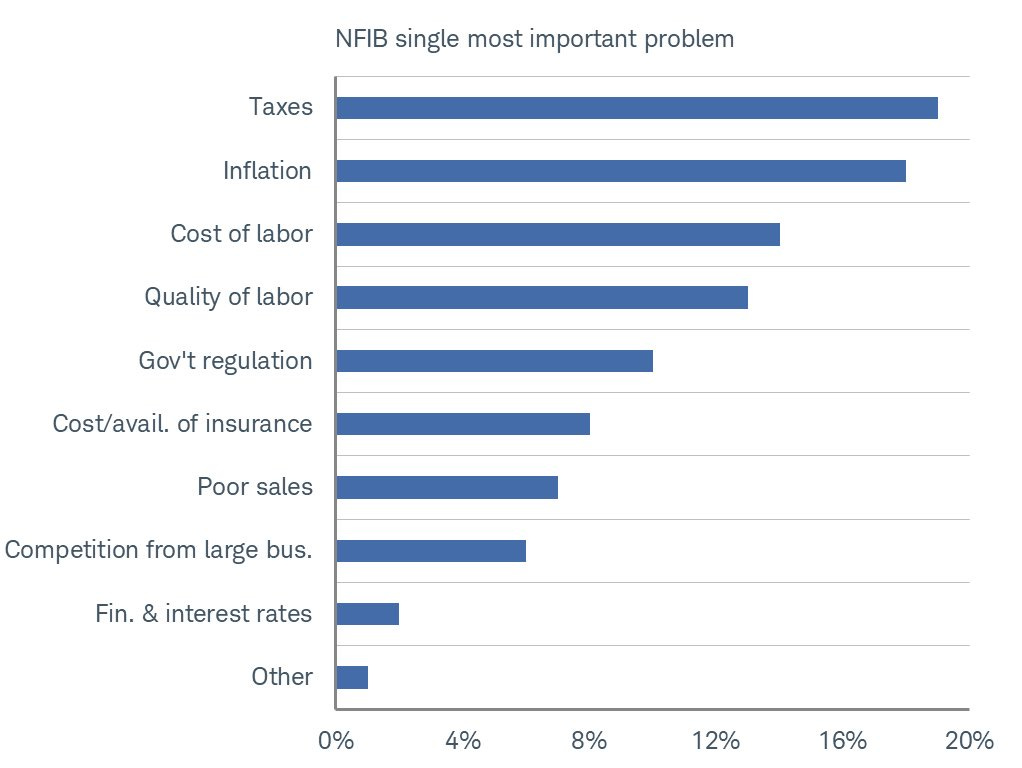

Since the tariffs were implemented, “taxes” have been NFIB's single most important problem for several months.

Inflation comes in close second, driven by higher fuel prices, which have increased firms' logistics costs.

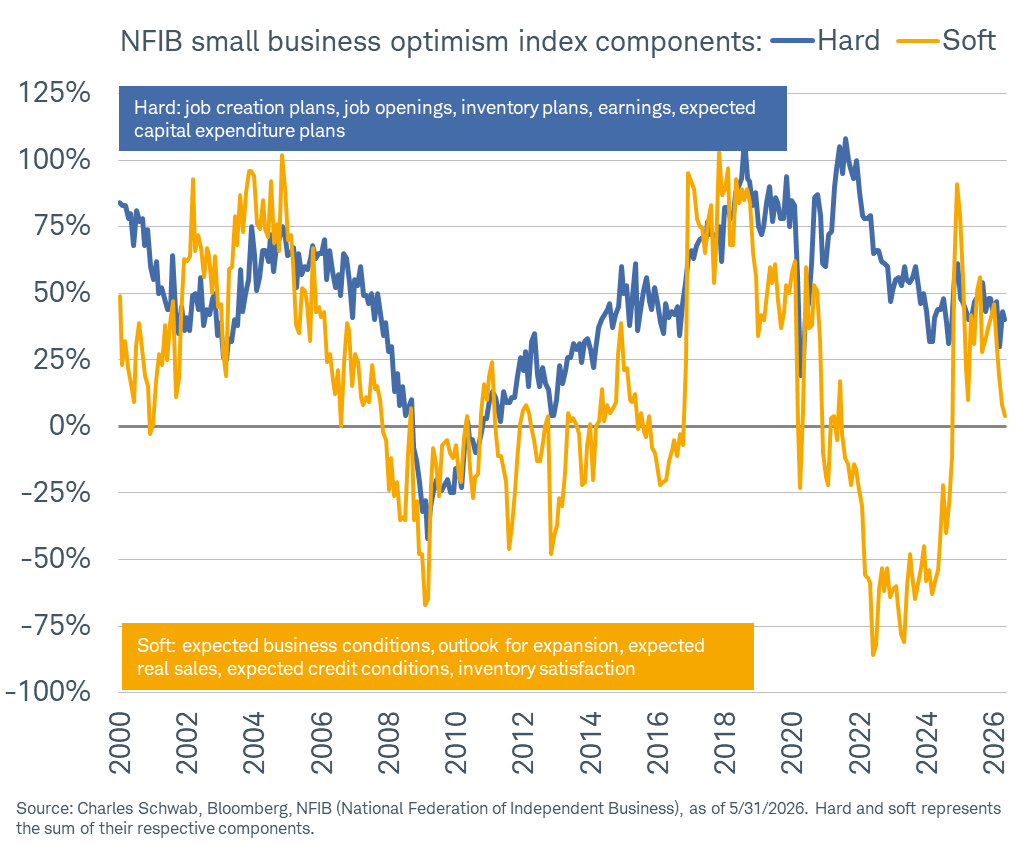

The Soft data in NFIB has been very volatile and has been trending down, while the hard data has been resilient.

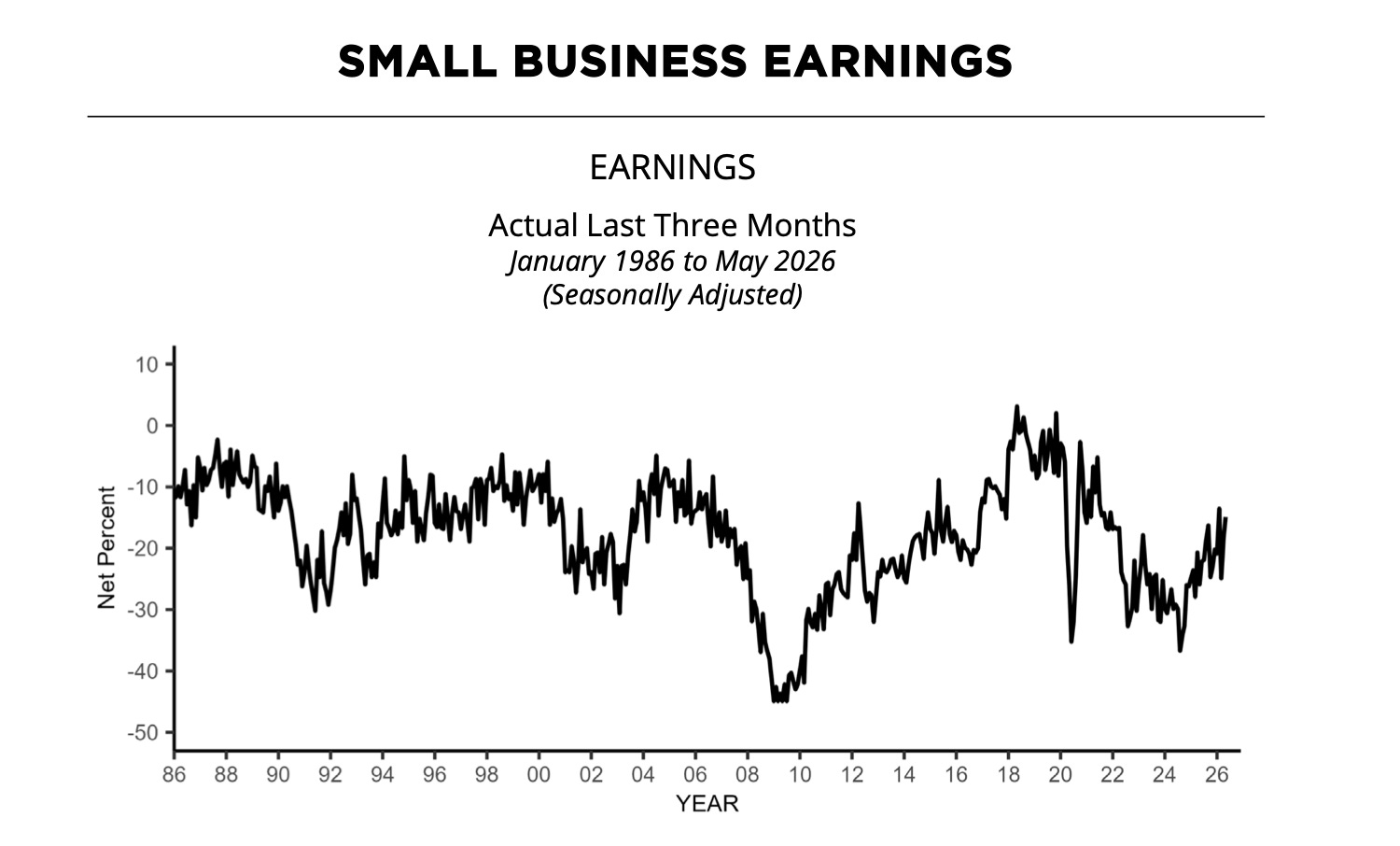

In fact, when you dig deeper, the small business earnings are trending up.

We believe that as soon as businesses are able to pass on rising costs to consumers, earnings will shoot up (no margin compression).

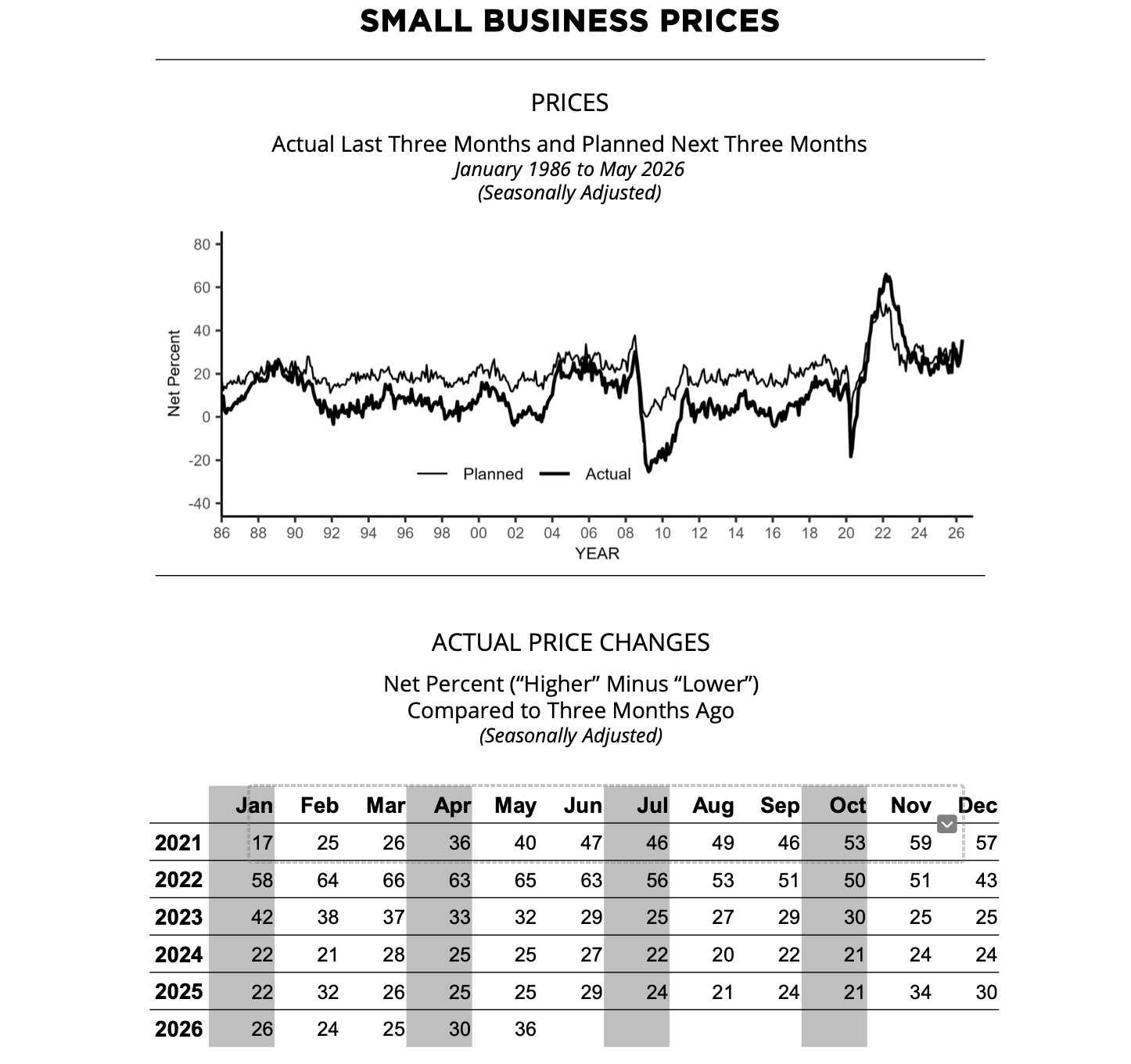

When we analyse small-business prices, we can infer that small businesses are facing extreme headwinds, with the highest input-cost pressures since early 2023.

Note that Net Percent (higher minus lower) has moved to 36 in May, last seen in March 2023.