The Great Unwind!

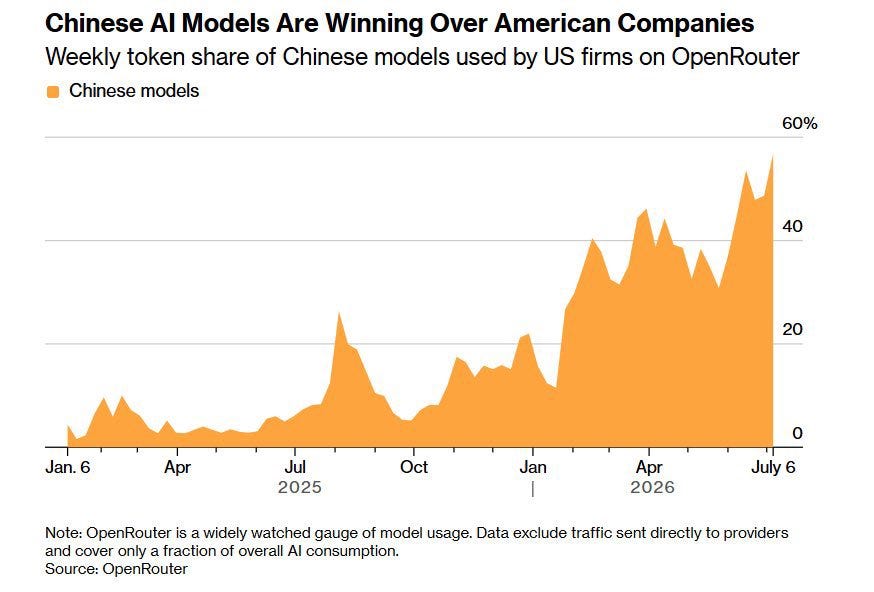

We have been flagging the risk to the AI story for the past few weeks, as Chinese models continue to gain unprecedented market share at the expense of US frontier LLMs.

According to OpenRouter, the weekly token share of “cheap” Chinese models has now surpassed 50% amid an insane rise in usage of Chinese open-source models.

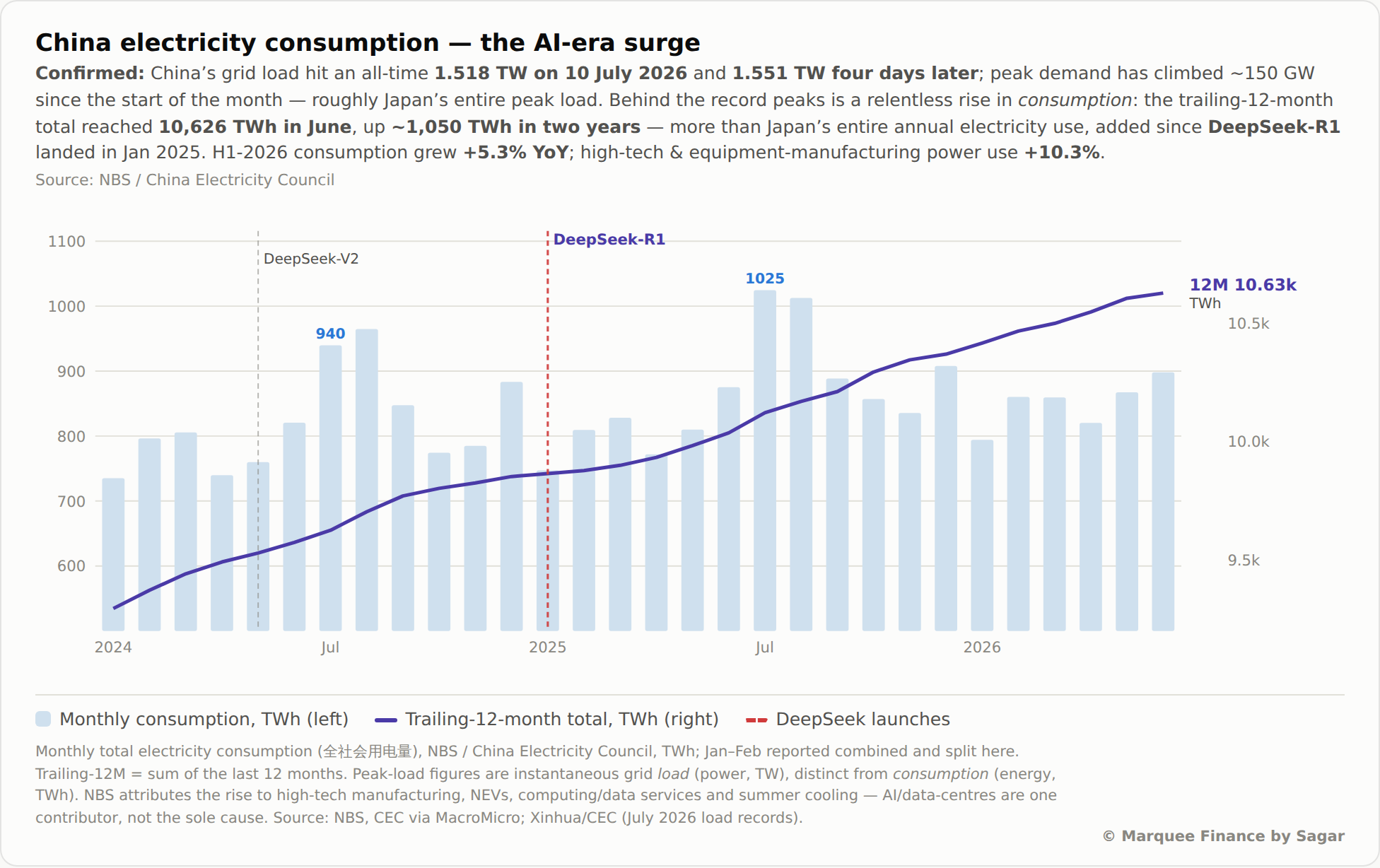

This has been possible due to the electricity infrastructure available in China. According to reports, China's power consumption hit a record 1.5138 terawatt-hours on July 10th.

Notably, the power load has increased by 150 gigawatts since the beginning of July (equivalent to Japan's entire load).

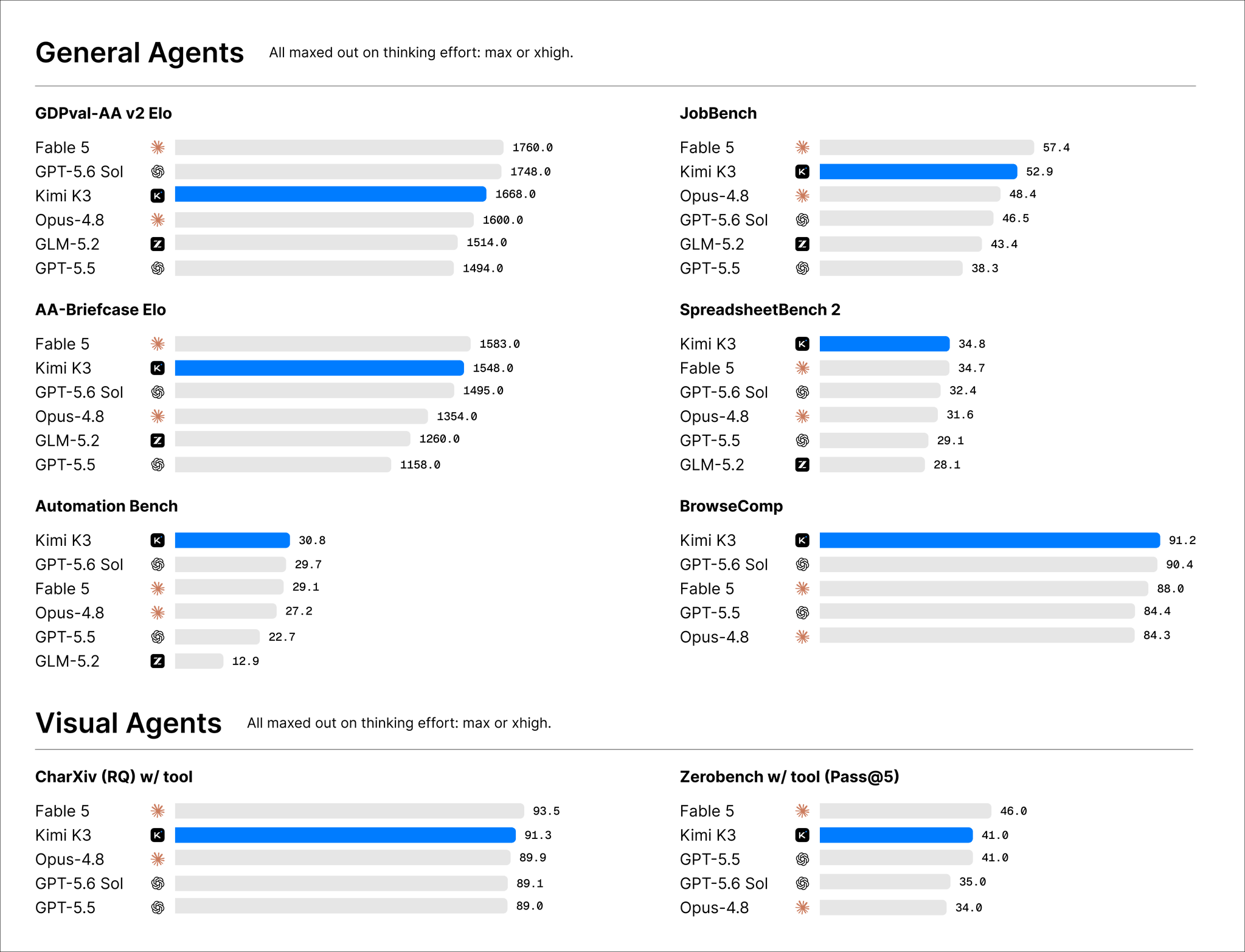

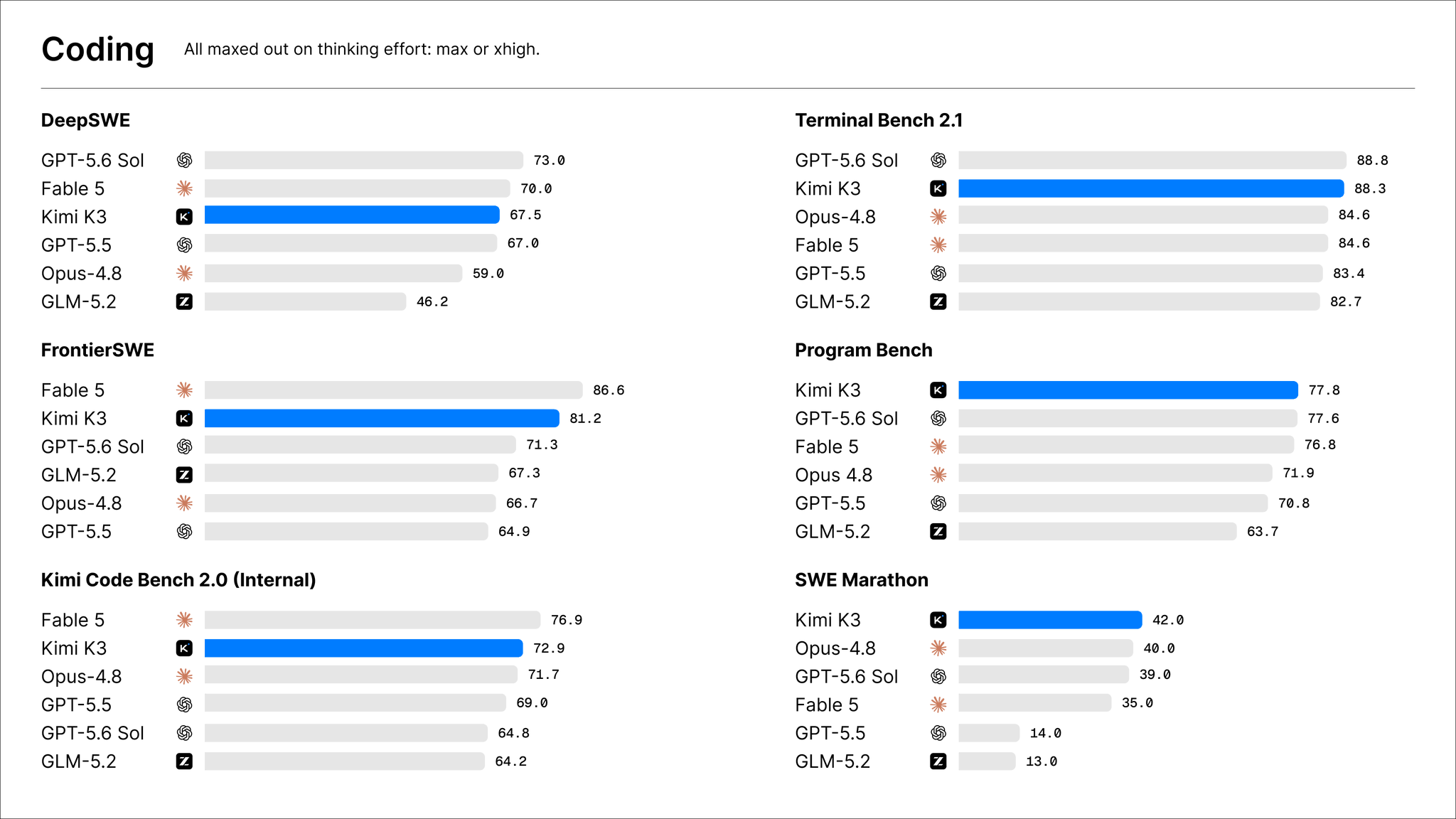

Furthermore, this week Moonshot released its most advanced model, Kimi K3, which stunned the whole world.

On various parameters, Kimi K3 scores higher than the most advanced models of OpenAI (GPT 5.6 Sol) and Anthropic (Fable 5).

There will be significant repercussions if Chinese models continue to advance at the current pace.

Nevertheless, we believe that higher AI adoption in the US will ultimately benefit US AI infrastructure players, especially cloud players such as AMZN, MSFT, and GOOGL.

It’s hard to predict what will transpire in the coming years, but one thing is certain: we are at an inflexion point in the history of technological advancement of the human race.

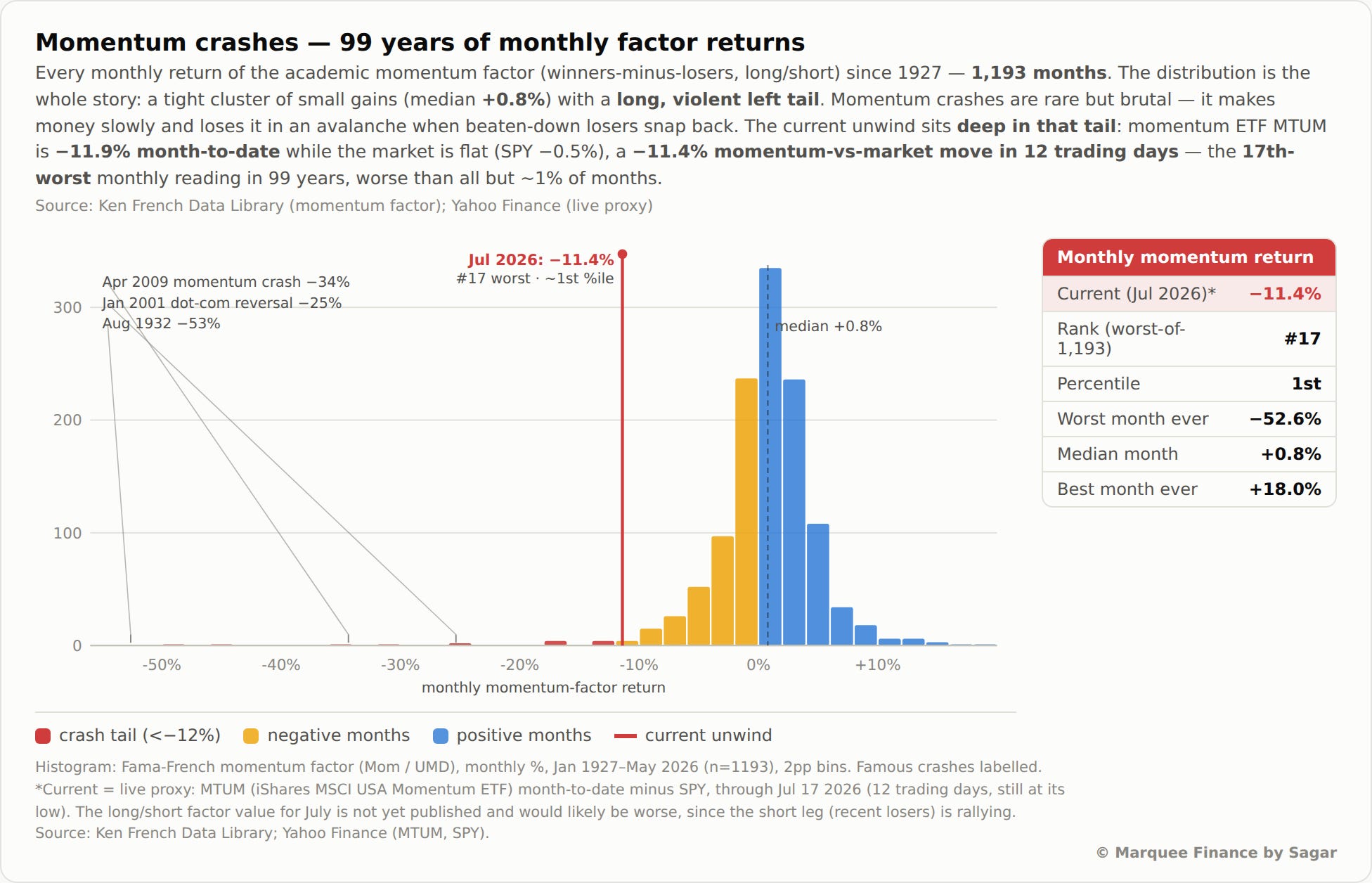

The overheated semi-space has witnessed carnage in July as the gigantic levered trade unwound, beginning in Korea where there were systematic margin calls across the retail crowd.

As a result, momentum has witnessed a historic rout.

The −11.4% momentum v/s SPX move sits at the 1.3rd percentile — 17th-worst month out of 1,193 since 1927.

We are announcing a price increase for our subscription plans, driven by significant new features and upcoming updates. Starting August 15th, the monthly plan will increase from $ 29.99 to $ 39.99, and the annual plan will increase from $ 299.99 to $ 399.

Existing subscribers will “NOT” see any changes and will remain on their current plans.s

Since early May, everything else sold off, and a parabolic rally began in the Semiconductors (global). As a result, we underperformed; however, we were confident that when the market heals, we would again outperform.

Our underperformance has now reduced to 9 bps.

PS: Benchmark is 60% MSCI ACWI and 40% BBG Global Aggregate.

Our target remains to deliver double-digit returns this year while outperforming the benchmark.

Let's take a deep dive into the macro universe and comprehend the cross-asset moves.

US/Equities/Bonds/Oil/Dollar/Gold!

We received a whole host of macro data in one of the busiest weeks of the month.

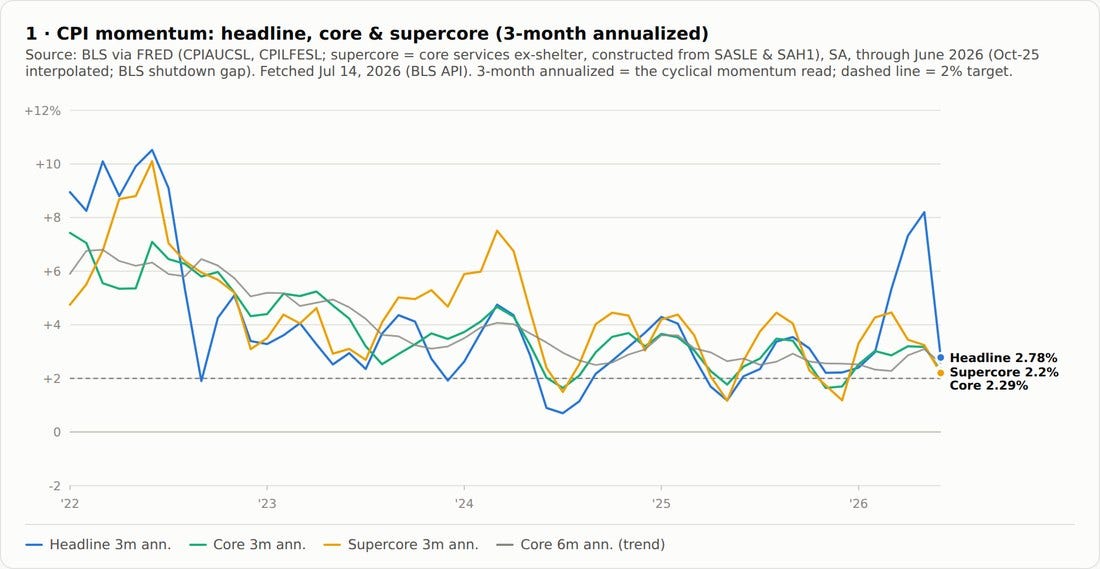

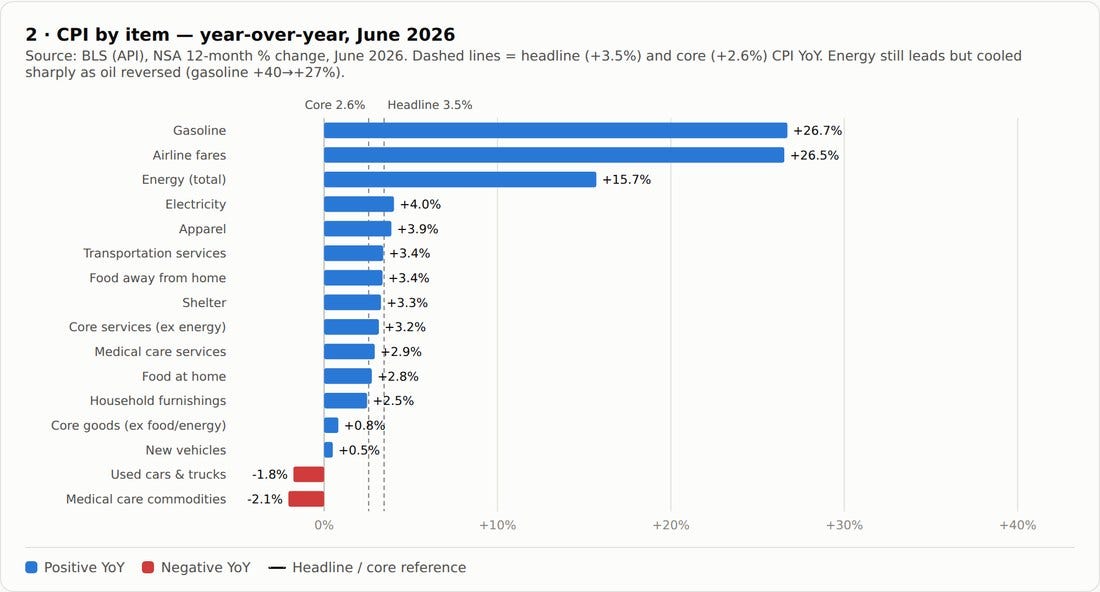

The CPI came as a pleasant surprise, with the headline CPI at -0.4% MoM v/s expected -0.1%.

On the other hand, Core CPI came in at 0% MoM v/s expected 0.2%.

The 3 Month Annualised headline CPI also collapsed to 2.78% while the Supercore CPI (which has been sticky) also moderated to 2.2%.

When we dig deeper, YoY inflation in gasoline, energy, and airfare is still in double digits.

However, softness is visible in Used Cars and Trucks (likely due to weak demand) and medical care commodities.

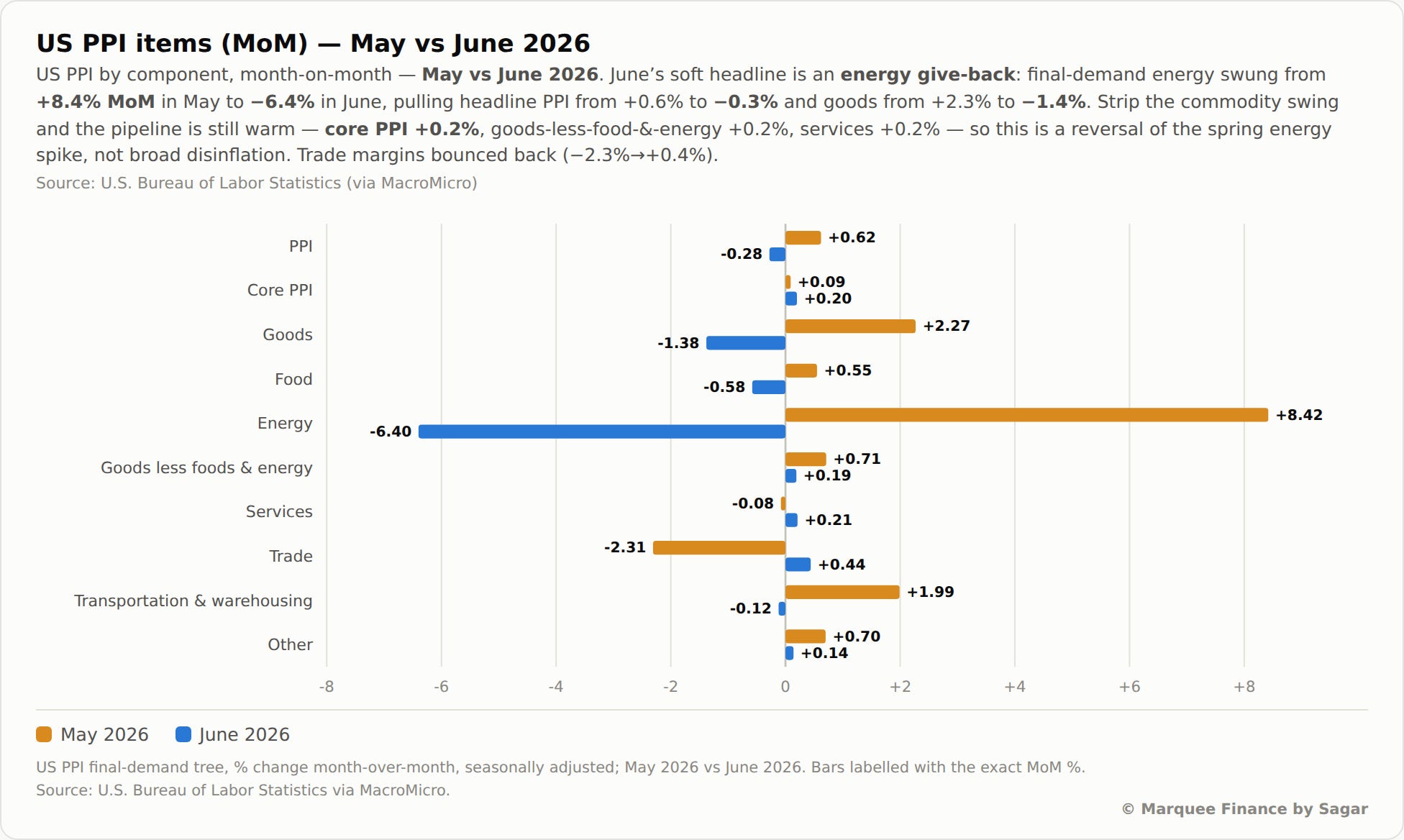

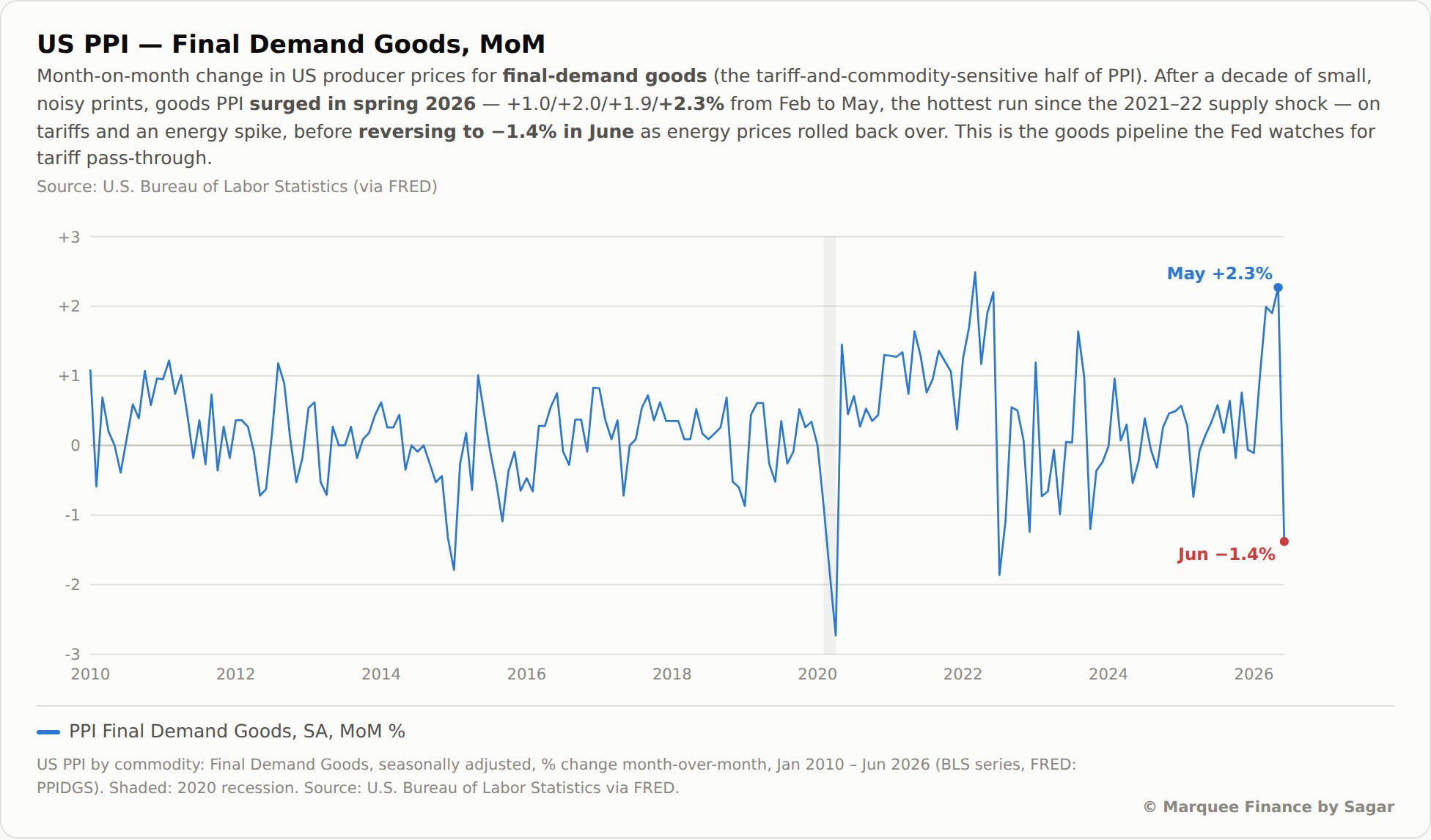

PPI also had a downside surprise, with the headline coming in at -0.3% MoM vs the expected 0%. The core PPI came in at 0.2% MoM v/s expected 0.3%.

The June story was all about energy as it came in at -6.4% v/s +8.42% MoM.

The starkest data in PPI was the PPI-final demand goods MoM, which crashed from a multi-year high of 2.3% in May to -1.4% in June.

The wild swings, as we know, were due to volatile energy prices.

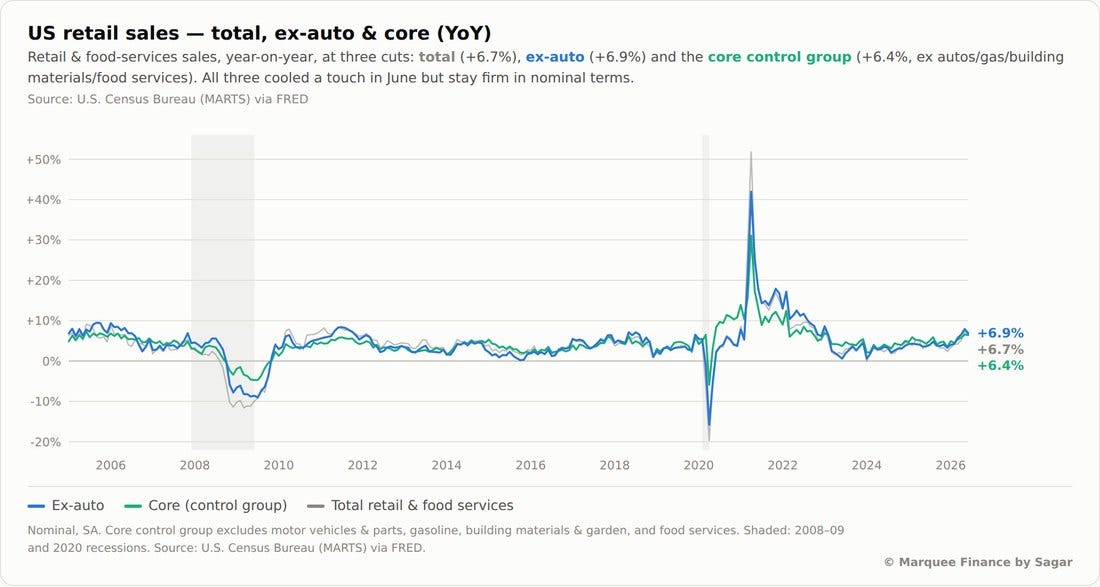

We also got the retail sales this week.

Headline retail sales came in at 0.2% v/s expected 0.2%.

Retail Sales ex-auto came in at -0.2% v/s expected -0.1% (slightly weaker), while Retail Sales control group came in at 0.5% v/s 0.5%.

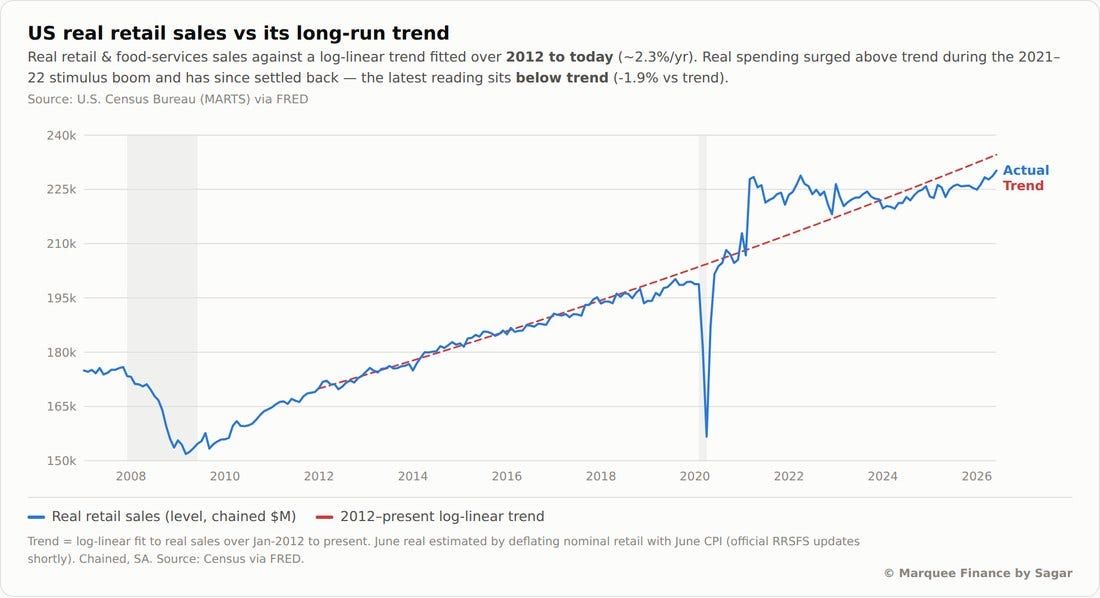

When we analyse the YoY data, the rise is entirely due to the “inflation” effect, as the nominal figure is higher, while real retail sales have been a dampener.

Real retail sales have been below the “long-run” trend since late 2023, indicating a broken US economy (K-shaped) due to persistently higher inflation since COVID-19.

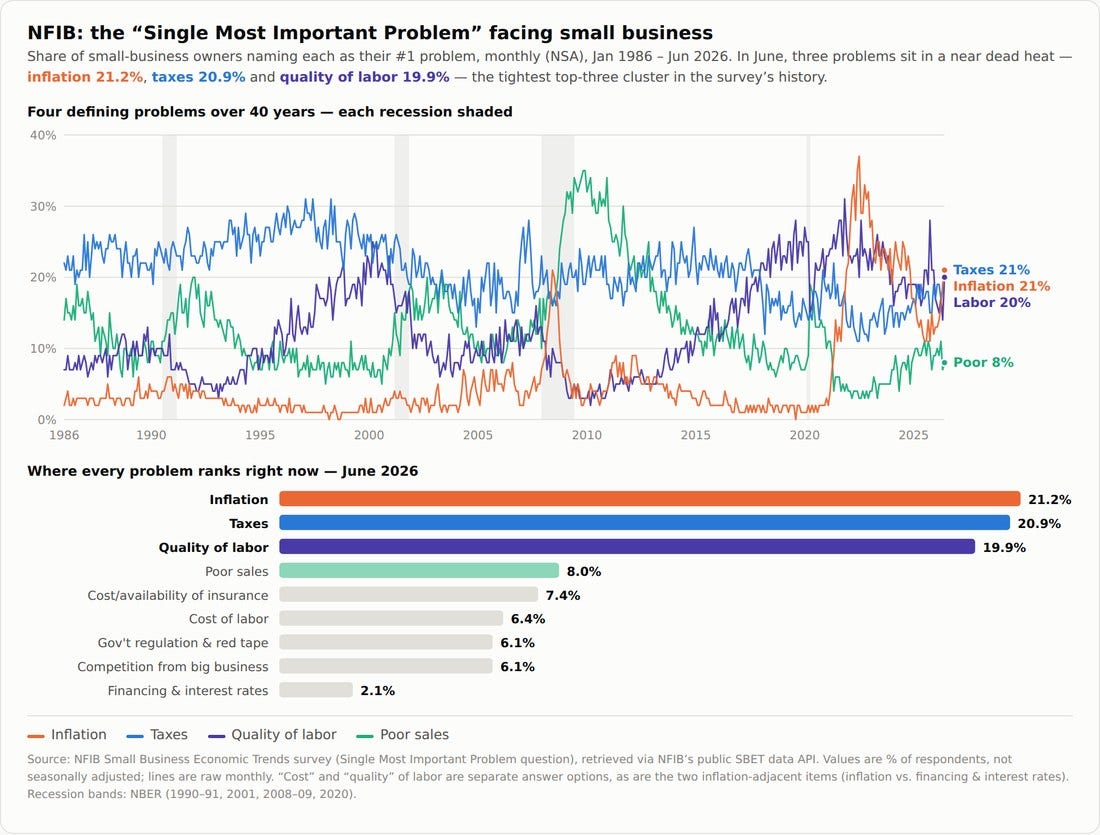

We also received the NFIB data.

The headline number came in stronger than expected at 97.4 v/s expected 95.7.

Interestingly, “Inflation” came in at the top as the single most important problem, with 21.2% of businesses reporting it.

Equities!

We mentioned last Saturday that