The Last Hurrah!

Macro is the study of business cycles, as it’s a no-brainer that economic expansions are followed by contractions and so forth. The historical analysis of business cycles concludes that a slowdown/recession is necessary to unclutter the excesses that develop during the boom/expansion periods.

Nonetheless, the current business cycle has been extraordinarily distorted due to the various lags, disruptions caused by the pandemic and war-led supply chain shocks. To make matters worse, the world’s largest economy is pursuing a mind-boggling “fiscal dominance” policy, which has led to a 6-7% peacetime fiscal deficits.

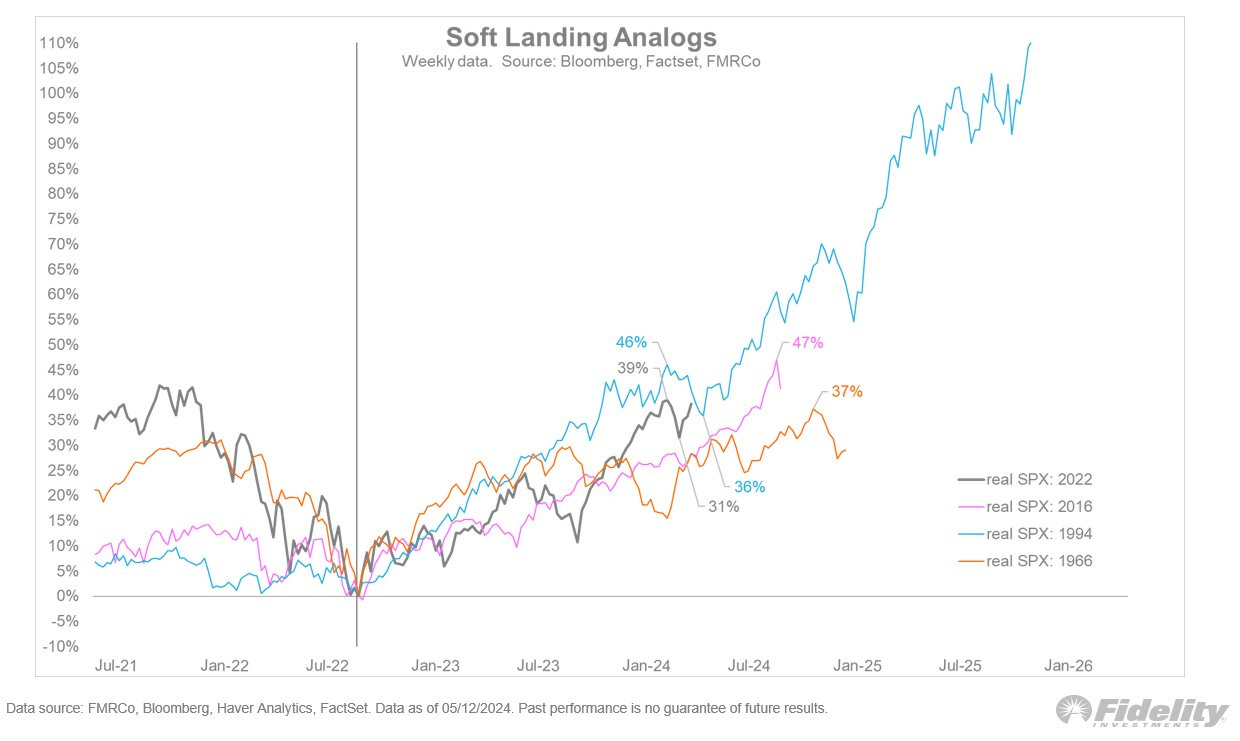

The “Last Hurrah” is officially known as the period where the economy is undergoing the late stages of an expansion, which in “months” is followed by a contraction. It is marked by euphoria and optimism about a soft landing in the economy.

We can’t deny that a soft landing is plausible (it transpired only in 1995). However, with the central bank’s extreme focus on the lagging indicators (CPI and Labour Market Data), one can be rest assured that the probability of a soft landing is always low.

As it happens during the “Last Hurrah” phase, risk assets seem to ignore the warning signs and continue their unabated rally on “optimism” about a soft landing.

A single tweet this week led to the animal spirits returning back to the so-called “meme” stocks, which rose by more than 1000% within days and caused enormous billions of dollars of losses to marquee hedge funds.

The meme stock mania, which first transpired in 2021 when liquidity was abundant across the financial system, calls into question how “restrictive” the monetary policy is despite one of the fastest tightenings ever.

In its quest to provide liquidity to the broken markets (which seem to be waning), the duo of the US Treasury, led by Yellen, and the Fed, led by JayPo, has created multiple asset bubbles, which can grow bigger if not corrected soon.

Using our framework and various macro variables, we will examine today the path of inflation and growth and what lies ahead.

US!

The biggest release of the week was none other than the much-awaited CPI data, which came in as a sign of relief for the risk assets, which rallied on hopes of a “soft landing” of the economy.

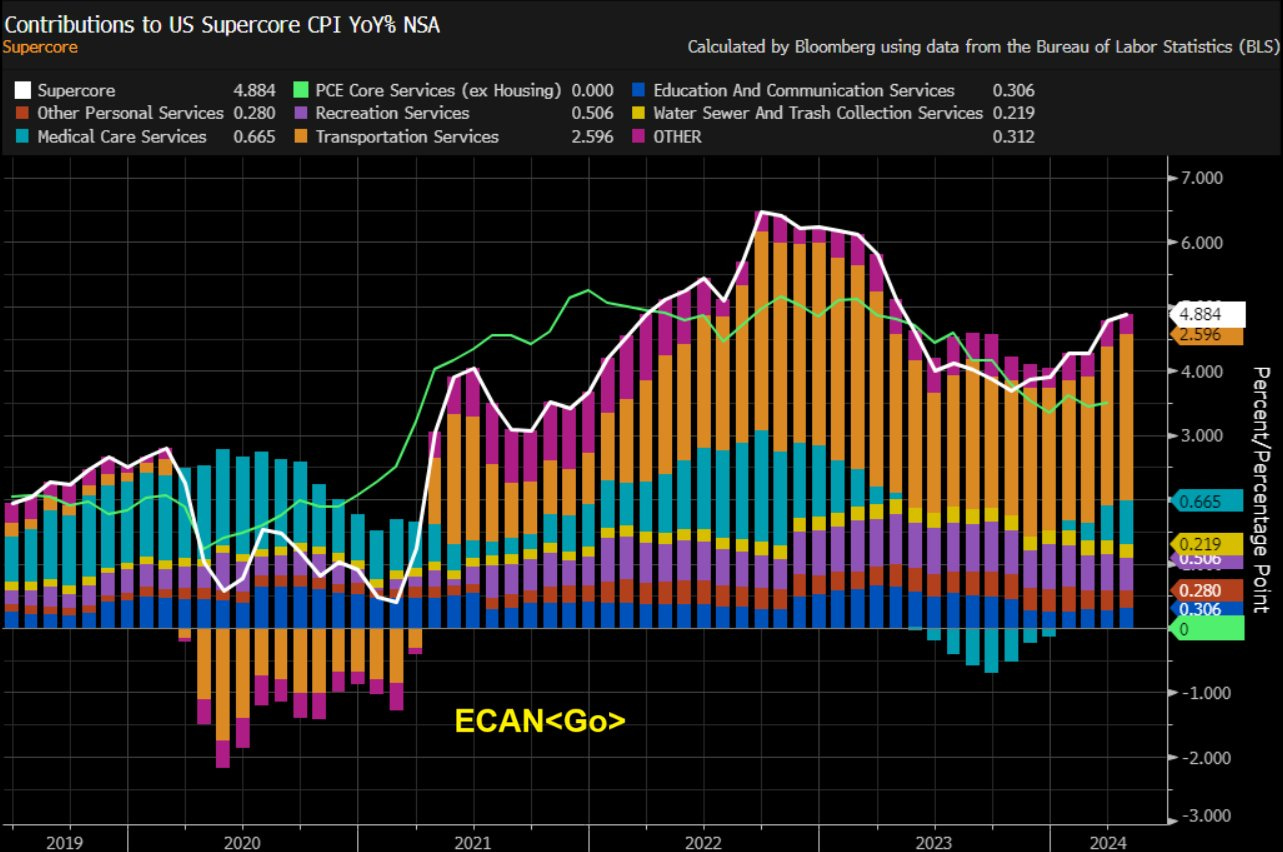

However, the internals of the CPI data were not encouraging, as JayPo's once favourite measure, the “Supercore” (Services Ex-Housing), which he used as a pretext for raising rates, has been trending higher since the beginning of the year.

The Supercore has moved higher to 4.88% YoY, led primarily by transportation services, which include auto insurance, and the prime rate-led inflation, which will only ease by H2 this year.

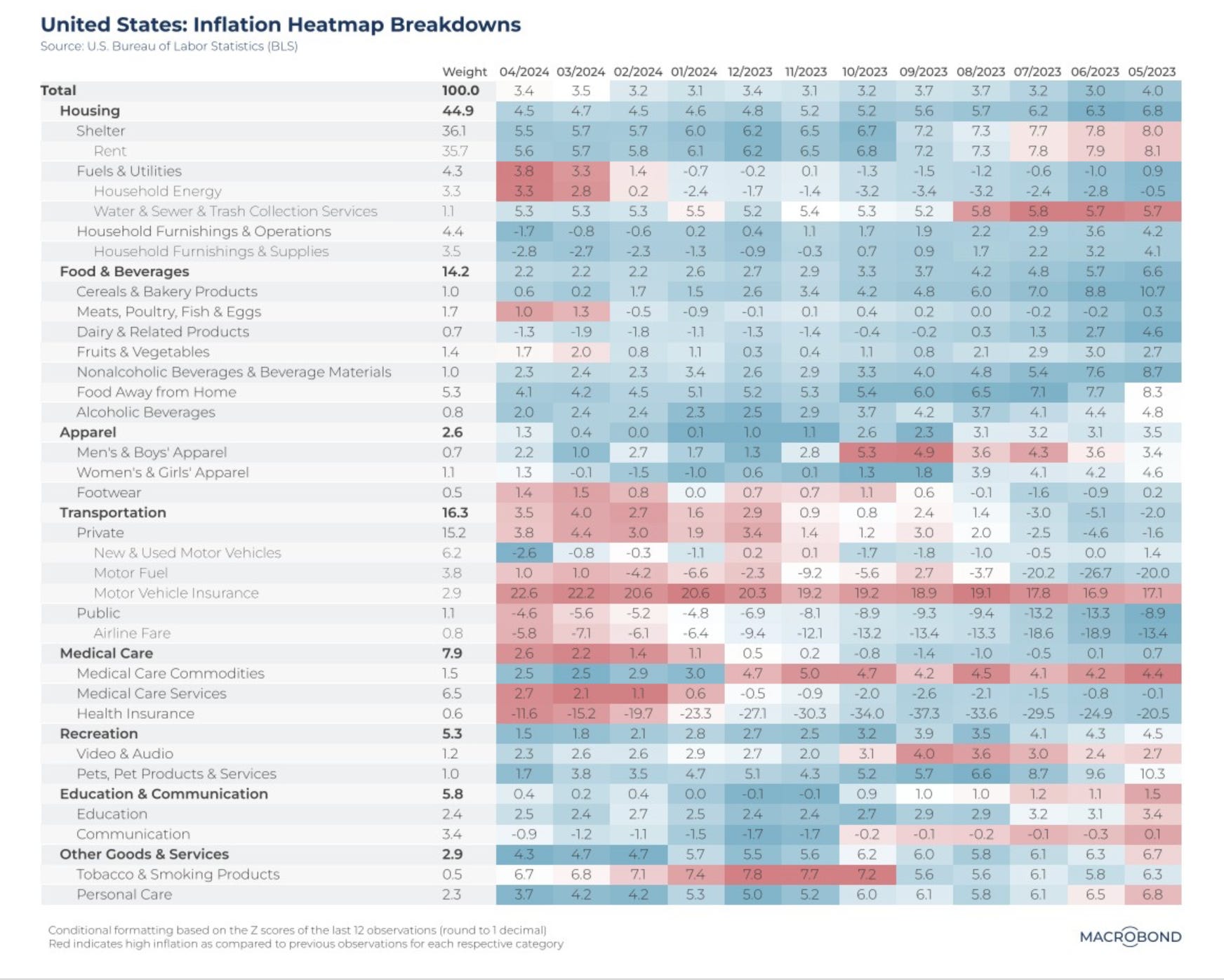

The headline number came in at 3.4%, which is still significantly higher than the 2% target rate. However, if inflation remains around the 3.5% level, we might say that the policy is restrictive with a Fed Funds Rate> 5%.

As we can observe, the shelter component, which JayPo termed “puzzling,” has now stabilised around 5.6%. However, we don’t expect it to fall significantly as the housing market remains “red” hot. Lower energy prices may keep inflation in check, and we might not hit our predicted number by July.

Remember that we shared this chart last month, according to which..