The Million Dollar Question!

The Million Dollar Question:

Will we get a durable peace and ceasefire in the ME, or will the conflict once again rage?

Although the highest-level talks are underway between Iran and the US (incredible that no one from Israel is attending the talks), the gap between the demands of both sides is monumental.

Furthermore, there is no consensus on the Strait of Hormuz (SOH), which has been a bone of contention.

Everybody should watch the video below to understand the situation on the ground!

As per the IRGC:

All ships intending to transit the Strait of Hormuz are hereby notified that in order to comply with the principles of maritime safety and to be protected from possible collisions with sea mines...they should take alternative routes for traffic in the Strait of Hormuz.

Note that the circle in the chart represents the mined area shared by both Oman and Iran.

The routes represented by arrows are in Iranian waters and are small waterways of “a few kms”, effectively giving Iran control of global energy flows.

If you believe that Iran will give up its only leverage, and if you believe the Gulf states and the US will allow the “IRGC” to control 20% of the global energy flows, then my friend, you are highly mistaken.

Undoubtedly, there is much more to come before this war ends, and we will discuss the path forward in detail in the Geopolitics section (extensive analysis).

We are up 3.2% YTD compared to 1.56% YTD returns by the benchmark.

The next few days are crucial, and we may significantly underperform/outperform the benchmark due to the directional bets in our portfolio.

Let us begin today’s newsletter, where we will discuss in detail the oil market, macro data and cross-asset moves.

US/Geopolitics!

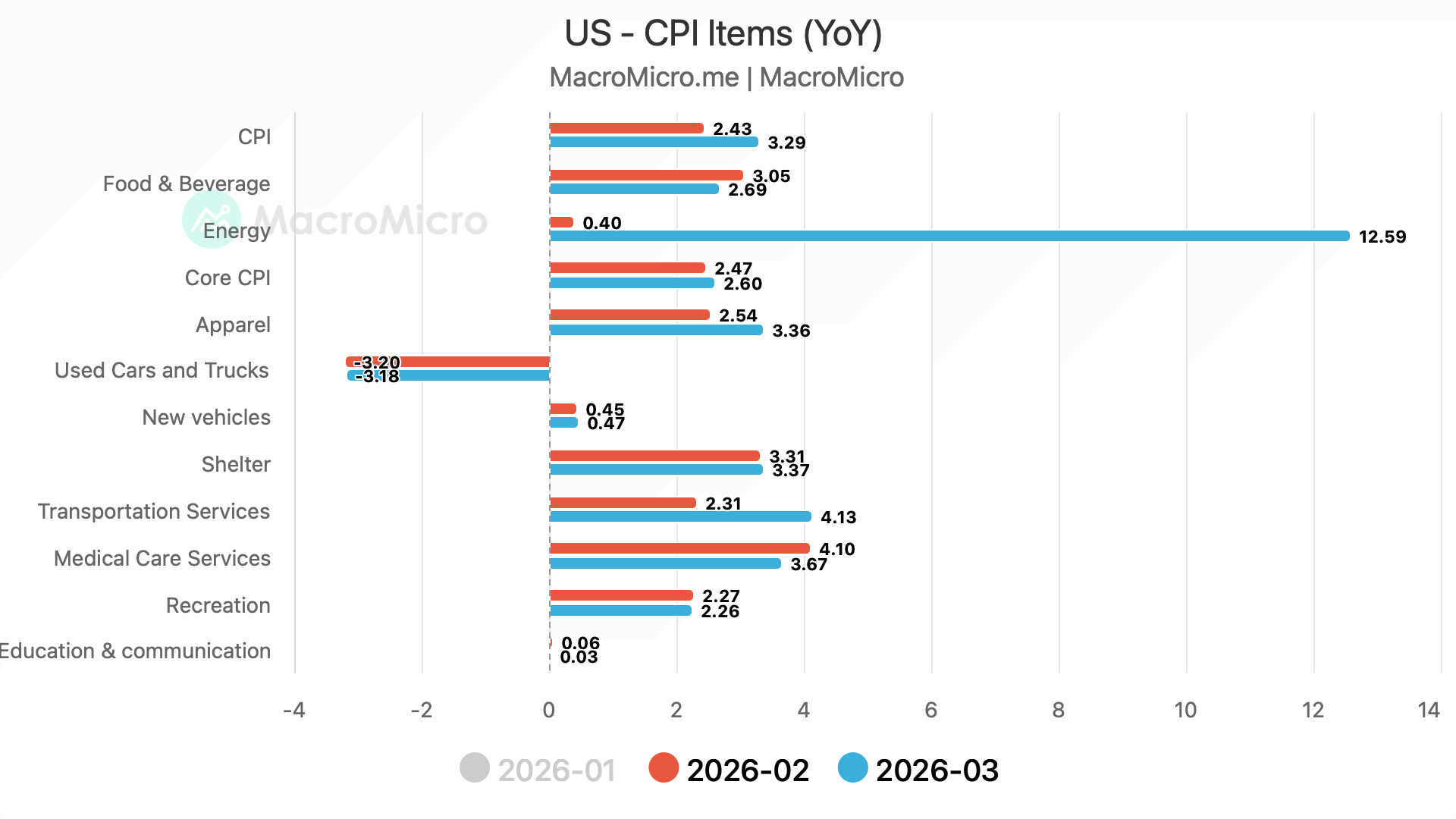

Since the war began on 28th February, we have received the first CPI report, which “partly” reflected the rise in oil prices.

The headline CPI came in at 3.3%, meeting expectations, while the Core CPI came in at 2.6% v/s expected 2.7%.

While energy prices were up 12.59% YoY, used car prices are exerting disinflationary pressure, with the measure down 3.18% YoY.

PS: We expect used car prices to reverse course and trend higher in the coming months, as evidenced by wholesale auction prices.

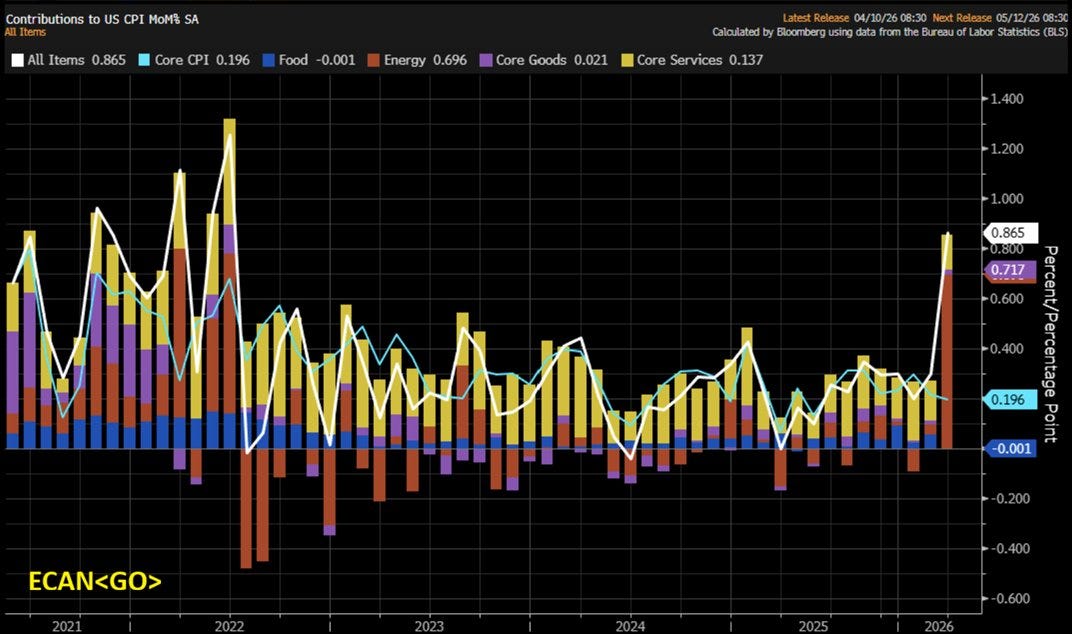

We have been articulating for the past few weeks that higher energy prices percolate into the CPI with a 2-3-quarter lag (higher goods inflation), as the CPI is a lagging indicator.

As of now, Core Goods inflation is benign at 0.021% MoM, and Core Services came in at 0.137% MoM.

JayPo’s popularised inflation measure, the Supercore (Services Ex-Shelter), came in at 3.14% YoY, with most of the increase driven by Transportation Services and medical care services.

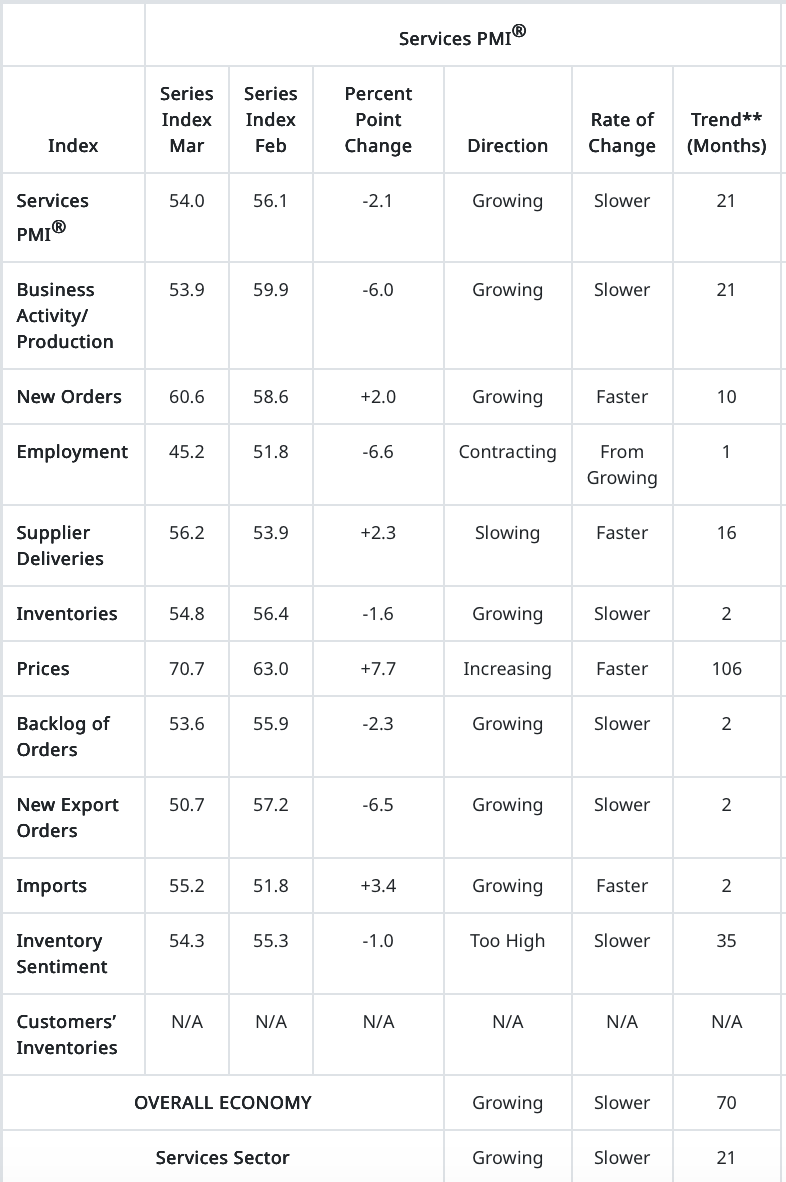

ISM Services came in at 54.0 v/s expected 54.9.

However, as usual, the devil lies in the details.

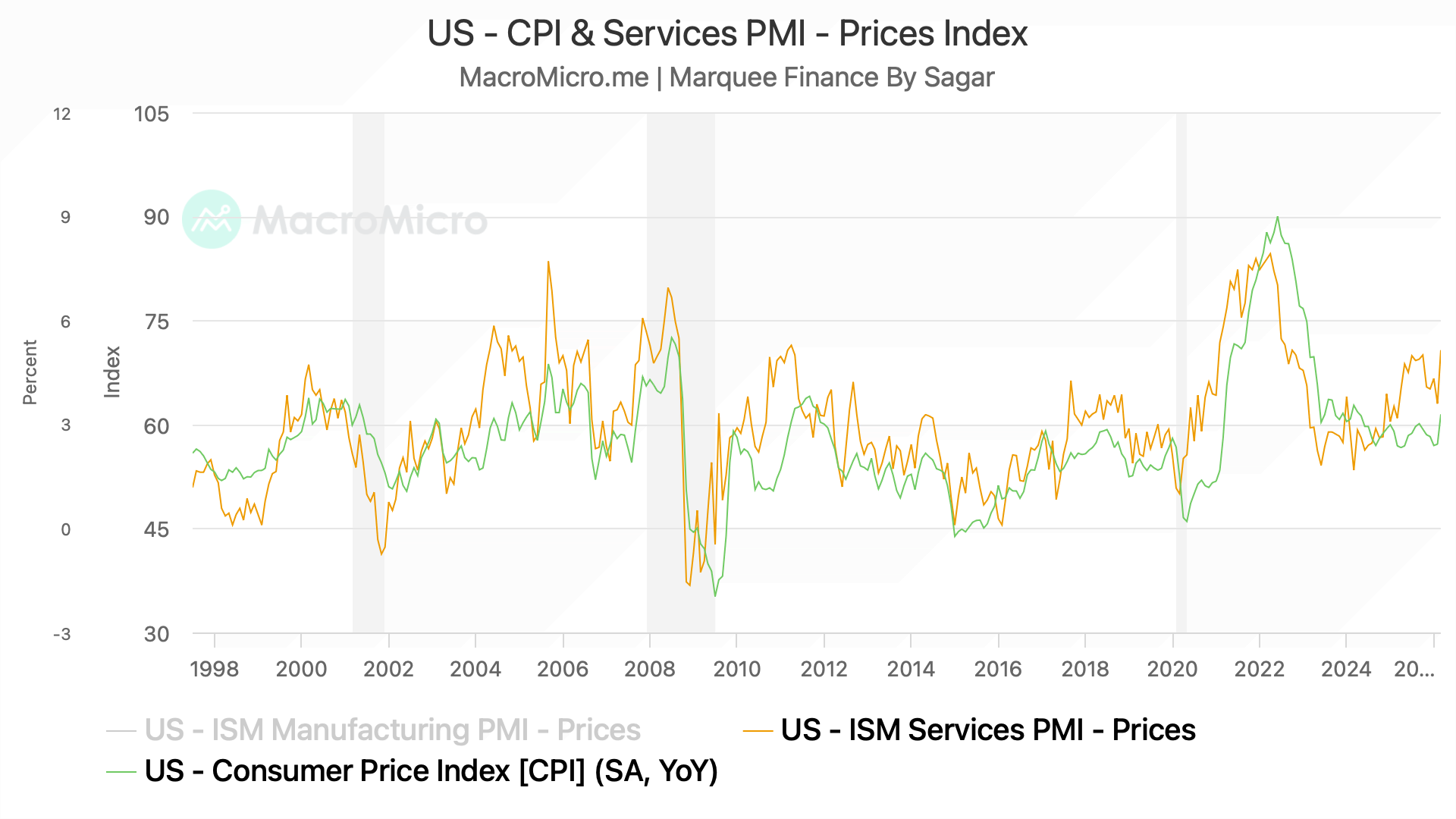

ISM Services Prices Paid came in scorching hot at 70.7, indicating that the CPI is going vertical in the next few months.

Furthermore, while Prices Paid came in at the highest level since 2022, the Employment PMI came in at 45.2, the lowest since 2023, indicating early stagflationary signals.

On the contrary, Services activity seems robust, with New Orders jumping to 60.6.

Nevertheless, the income data have been horrendous.

Excluding current transfers, the Real Personal Disposable Income (adjusted for inflation) is now flat since liberation day last year.

Note that this is before the oil shock hit the US economy.

Furthermore, the real PCE is significantly higher than real personal income, as Americans have been drawing down their savings (also partly due to higher asset prices, which fuel the positive wealth effect).

If the “real” incomes fail to grow, we expect an imminent slowdown in consumption in the coming months.

We reiterate that consumer health was totally different when the oil shock of 2022 hit the global economy, compared with today, when consumers are fragile amid a soft, low-hire, low-fire labour market.