The Trump Vol Shock!

Welcome to the first edition of 2025 and the 174th edition of Marquee Finance By Sagar. Elevated volatility has been the common theme across assets in the first week of this year.

The first few days saw extremely volatile moves, especially in the FX markets, as the DXY surged to a fresh multi-month high before suddenly plunging and then again moving higher.

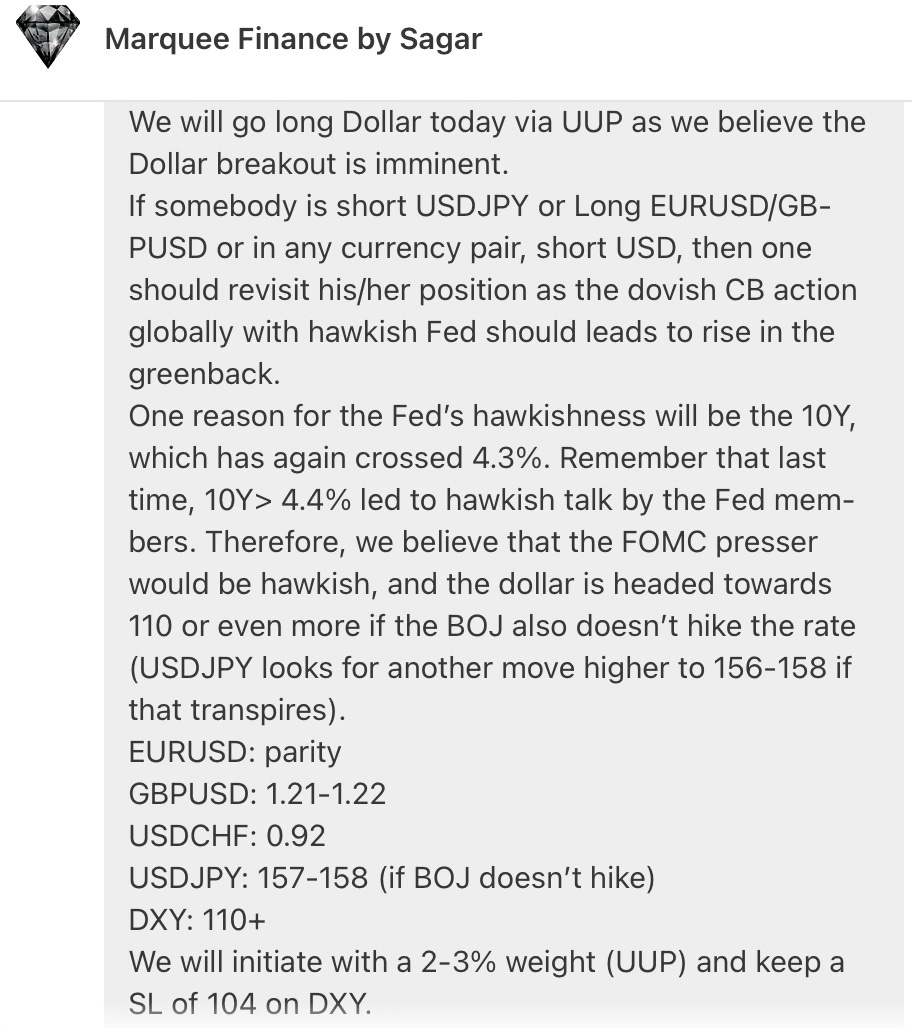

For our paid subscribers, the move in the greenback should not be a surprise. We explicitly mentioned and even initiated the long Dollar position last month before the Fed policy, with all our targets achieved except the EURUSD, which is very close.

On the contrary, yields on the USTs continue to surge unabated despite some softening in the US macro data indicating that bond vigilantes are in complete control of the bond market.

The extreme volatility results from the US President-Elect's statements and the signs of the time to come. Furthermore, the UK saw a repeat of the 2022 event as the yields surged along with the steep fall in the currency. Ironically, yields are now higher than in the 2022 event when GBPUSD reached parity and caused panic across the most traded market in the world (FX).

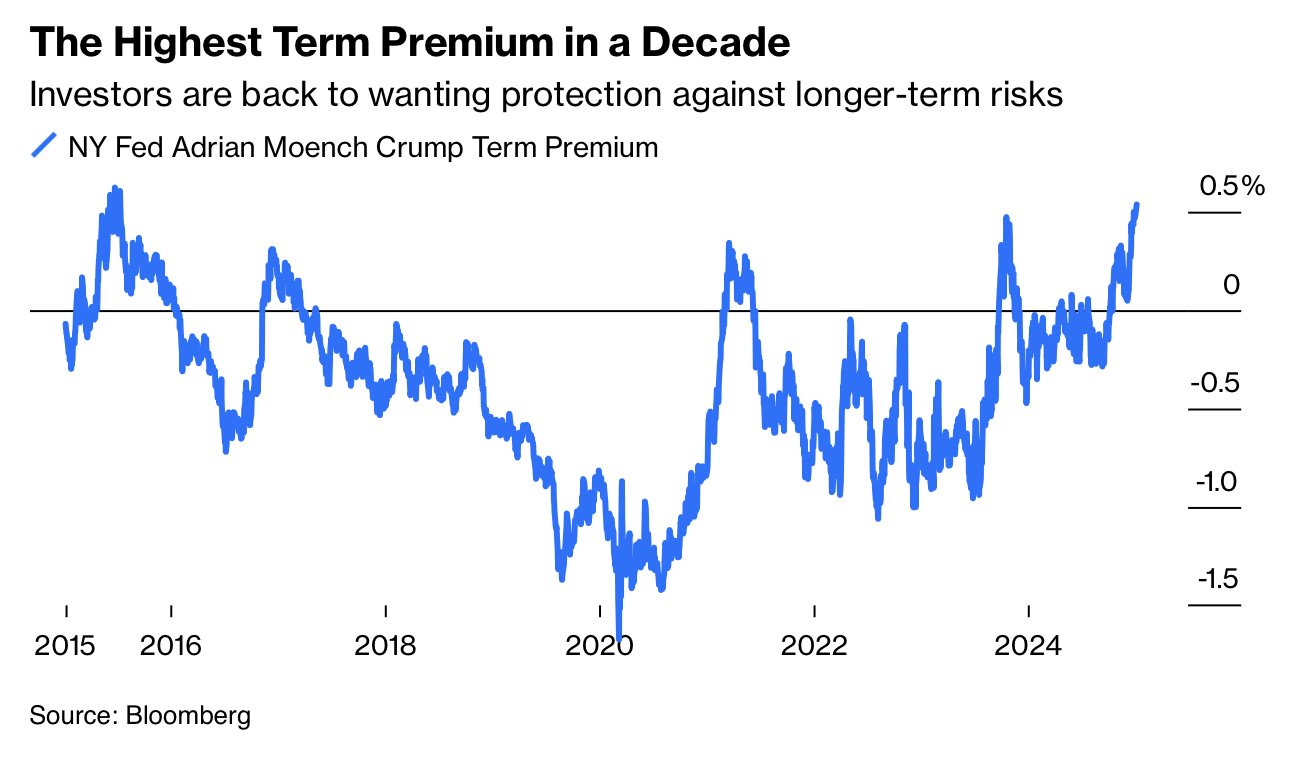

There is growing anger among market participants that the politicians in the West are not doing enough on the fiscal front (controlling deficits), resulting in higher-term premium demands from bond investors. Thus, yields are rising relentlessly despite weak/inline macro data.

In fact, the term premium in the US has shot to the highest in a decade as investors get uneasy about the upcoming Trump policies about inflation and higher structural deficits.

Let us examine the macro data in detail and share our thoughts about our guidance regarding global cross-asset moves.

US!

The first two months of every year have historically seen positive macro surprises, and this month was no exception except for one or two macro releases.

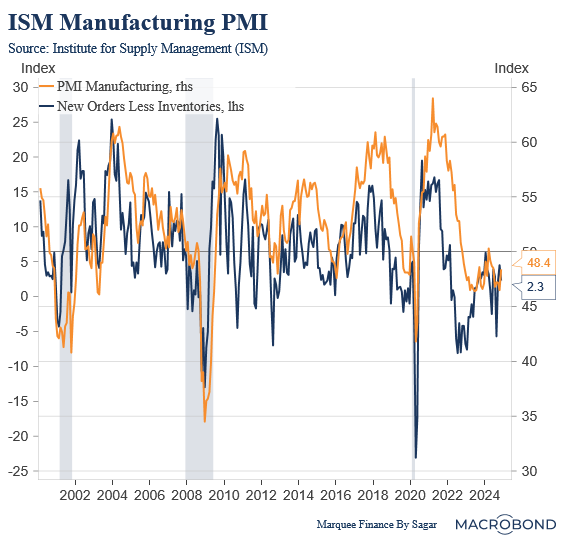

We began with our favourite macro indicator to track the cyclical activity in the US markets: ISM Manufacturing PMI.

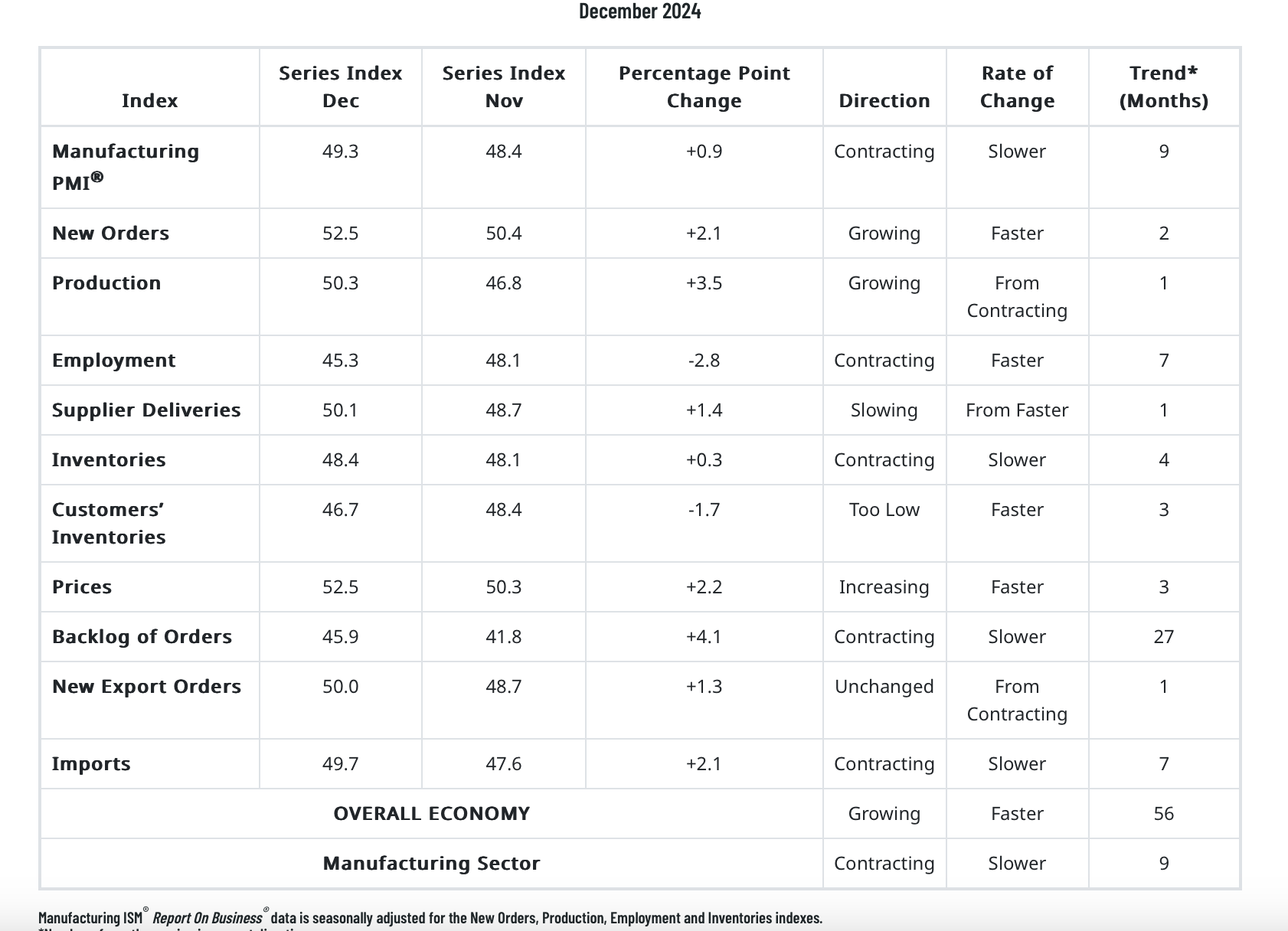

ISM Manufacturing came in above expectation but is still in the contraction zone.

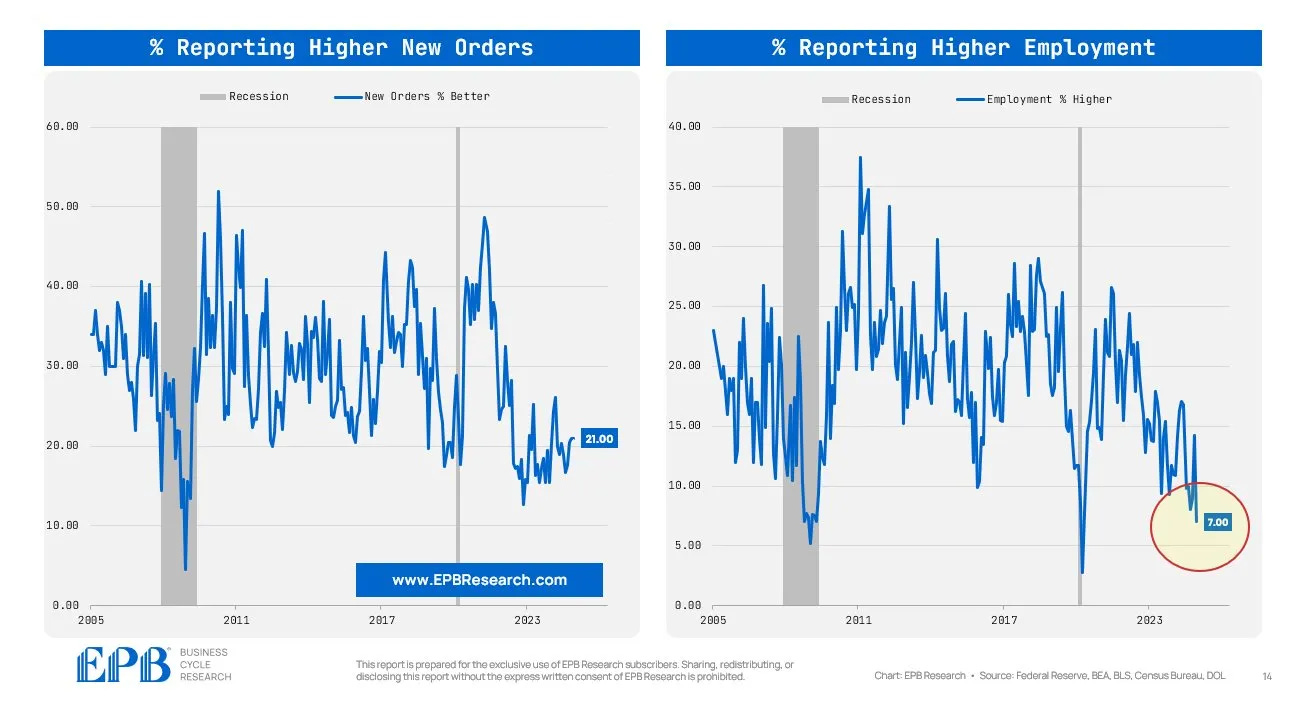

As we can see, except for Employment (contraction) and Prices (rising/ expansion), the report indicated an acceleration of economic activity, which has typically been the case for the past few years (January is good for macro data).

Furthermore, when we dig deeper, we find that only 7% of the respondents reported higher employment, a low number that transpires only during a “recession.”

Moreover, while new orders rose, the % reporting higher new orders is significantly off from the highs reported in the earlier business cycle expansion.

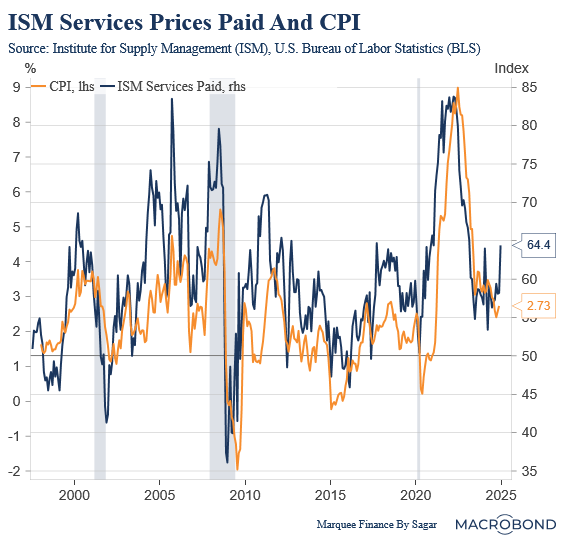

ISM Services also beat the estimates surprising positively with a big jump in the headline number to 54.1 indicating expansion (an overall healthy holiday season).

Nonetheless, the red flag was the Prices Paid, which jumped to 64.4.

As we can observe from the chart, Prices Paid and CPI had a tight correlation. If the trend persists in the ISM Services Prices Paid, we can expect the CPI to move higher in H1.

We also got multiple data points about the labour market which has garnered the Fed’s attention more than the CPI prints in the recent months.