"Thucydides Trap"!

“Can China and the United States transcend the so-called ‘Thucydides Trap’ and forge a new paradigm for major-power relations”- Xi Jinping, 14th May, 2026.

The US-China summit was historic, as the Chinese President raised a concern that nobody had expected him to raise publicly, even in their wildest dreams.

“It was the rise of Athens and the fear that this instilled in Sparta that made war inevitable,” Thucydides wrote in his book, The History of the Peloponnesian War.

Xi mentioned in his speech:

“The Taiwan question is the most important issue in China-US relations. If mishandled, the two nations could collide or even come into conflict, pushing the entire China-US relationship into a highly perilous situation.”

While raising the Taiwan issue and the Thucydides Trap simultaneously, China has made it clear about its red line, and the US has no alternative (to avoid conflict) but to reduce the reliance on TSMC and other supply chains that China controls (rare-earth).

As the summit ended, the global bond markets once again imploded, led by the Japanese Government Bond (JGB) market.

The yield on the 30Y JGB has now crossed a mind-boggling 4% while it has reached nearly 6% in the UK and 5.1% for the UST 30Y.

The bond vigilantes are running wild, and there is no escape for policymakers but to control inflation via fiscal and monetary tools.

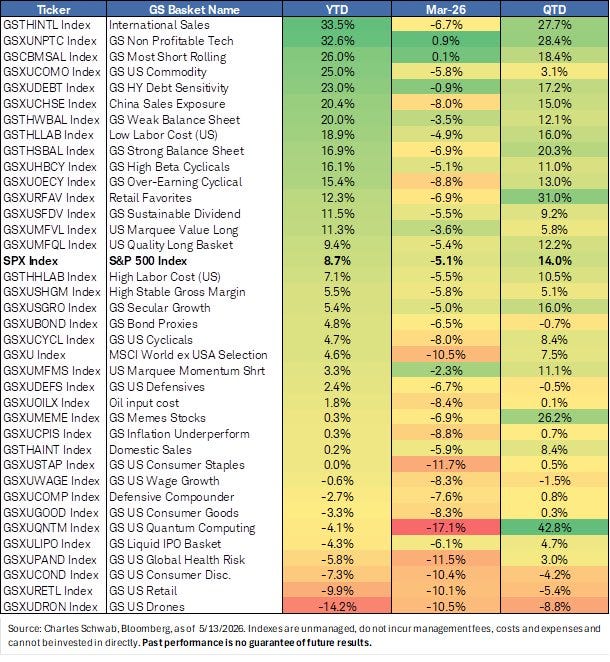

When we analyse performance across equity baskets (Data till 13th May) since the scorching rally began on 31st March, the biggest gainers are the most shorted: meme stocks, non-profitable tech, semis, and other speculative parts of the market.

The majority of market constituents have failed to outperform the index despite reporting better-than-expected earnings, as the rally has been super-narrow.

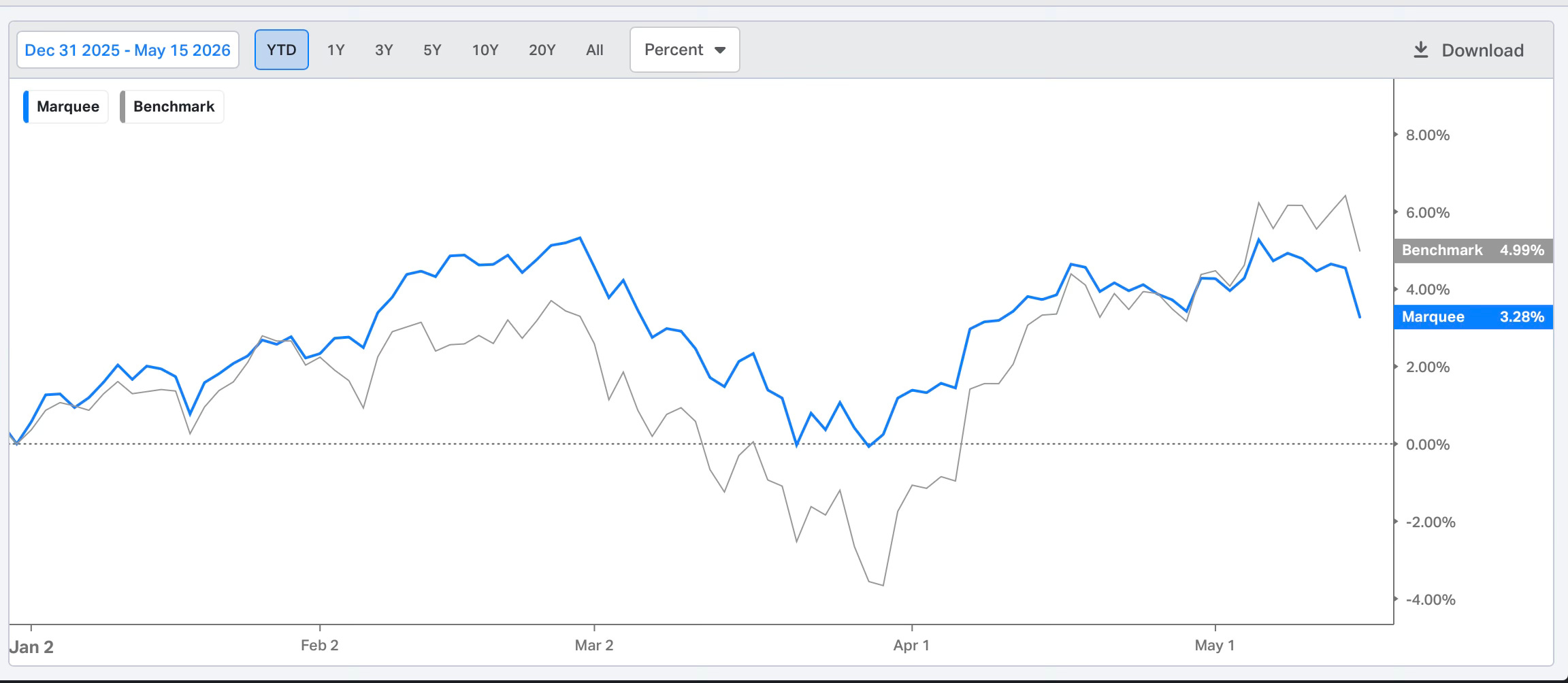

The PF underperformance, which began in the first week of May, continues due to the factors mentioned last week (shallow rally).

However, we expect to recoup the losses in the coming weeks and months.

Let’s take a deep dive into the macro universe and comprehend the cross-asset moves.

US/Equities/Bonds/Oil/Dollar/Gold!

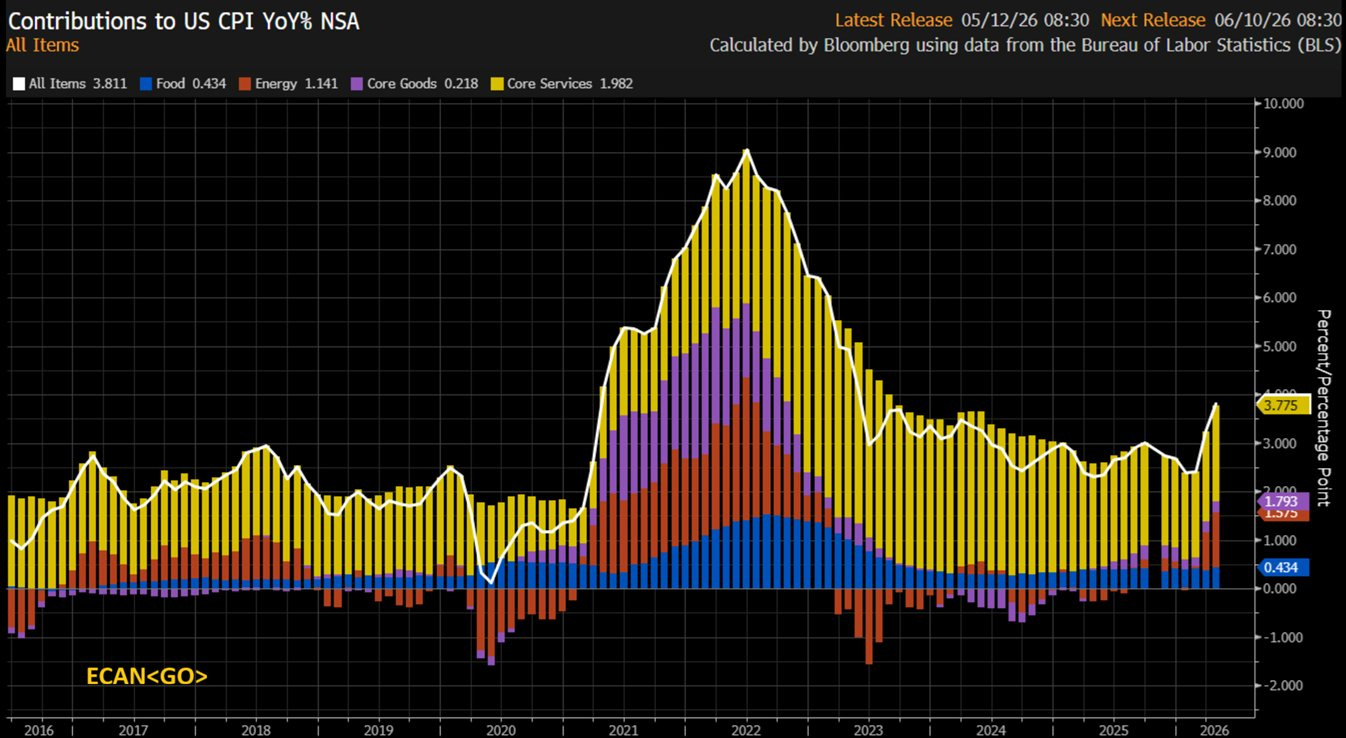

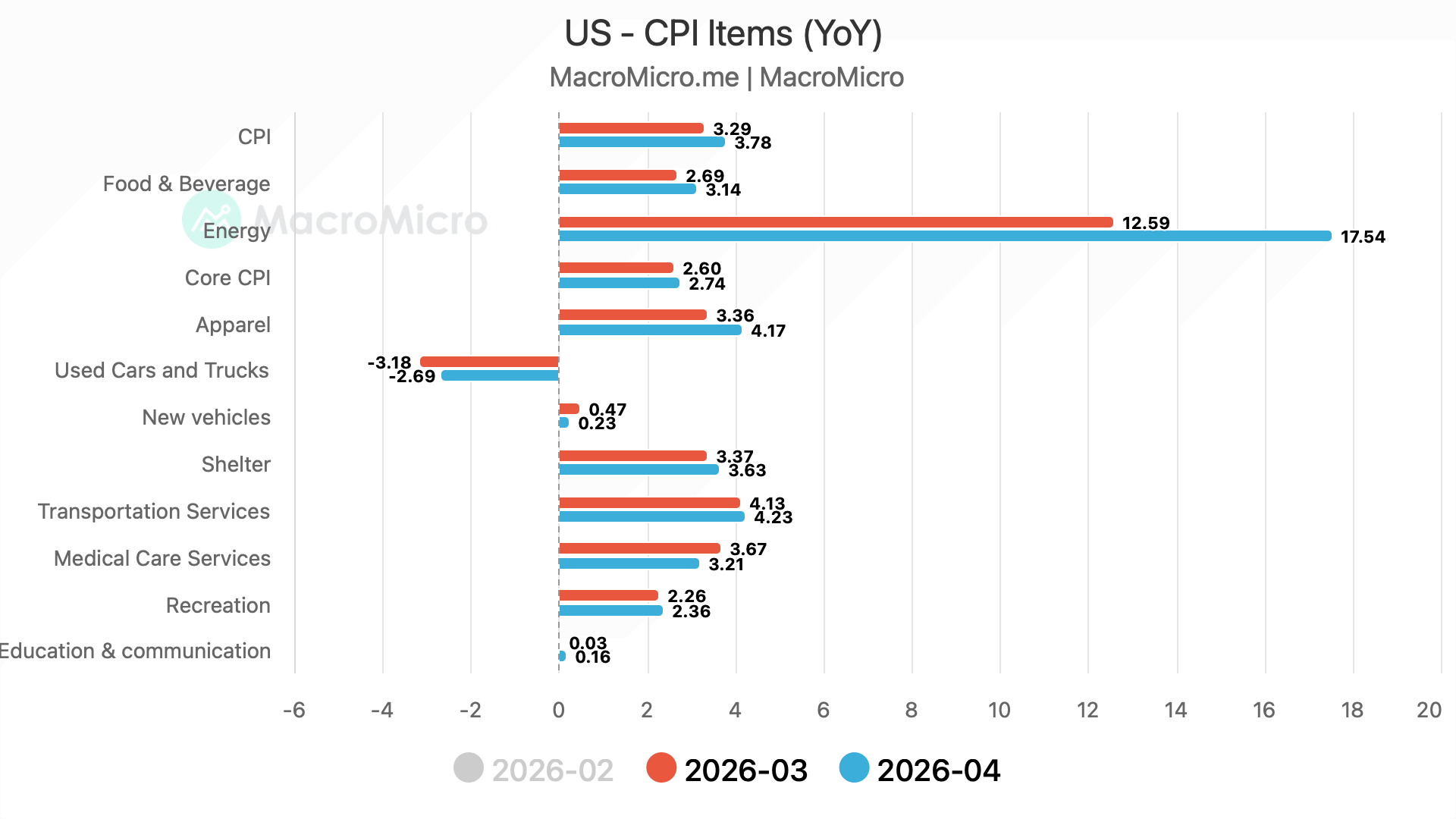

Two of the most-watched data points this week were the inflation measures: CPI and PPI, given that the full effect of higher oil prices was visible in April.

However, we believe we may achieve a full pass-through only by the end of Q3.

The headline CPI came in at 3.8% YoY v/s expected 3.7%, while the Core CPI (ex-food and energy) came in at 2.8% v/s expected 2.7%.

As one can observe, energy contribution has been the highest since the 2022 Russia-Ukraine war.

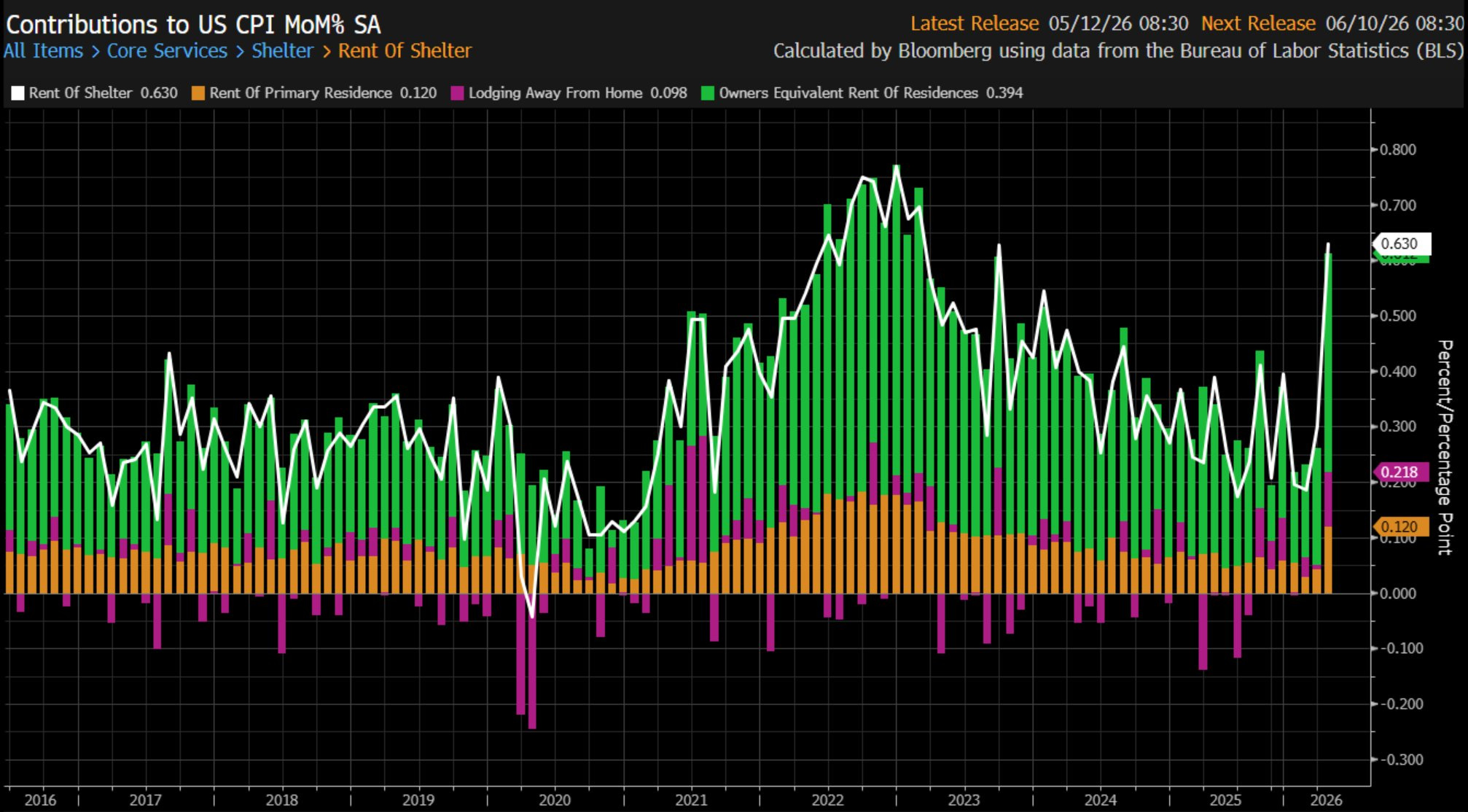

Furthermore, while core goods have been trending higher due to tariff-led inflation, we are now seeing pressure emerging even in Core Services.

Core Services was led higher by transportation services, while tariff inflation drove Apparel prices higher.

Shelter was significantly higher due to a one-time adjustment (double-counting) made for October, when the number was not reported because of the government shutdown.

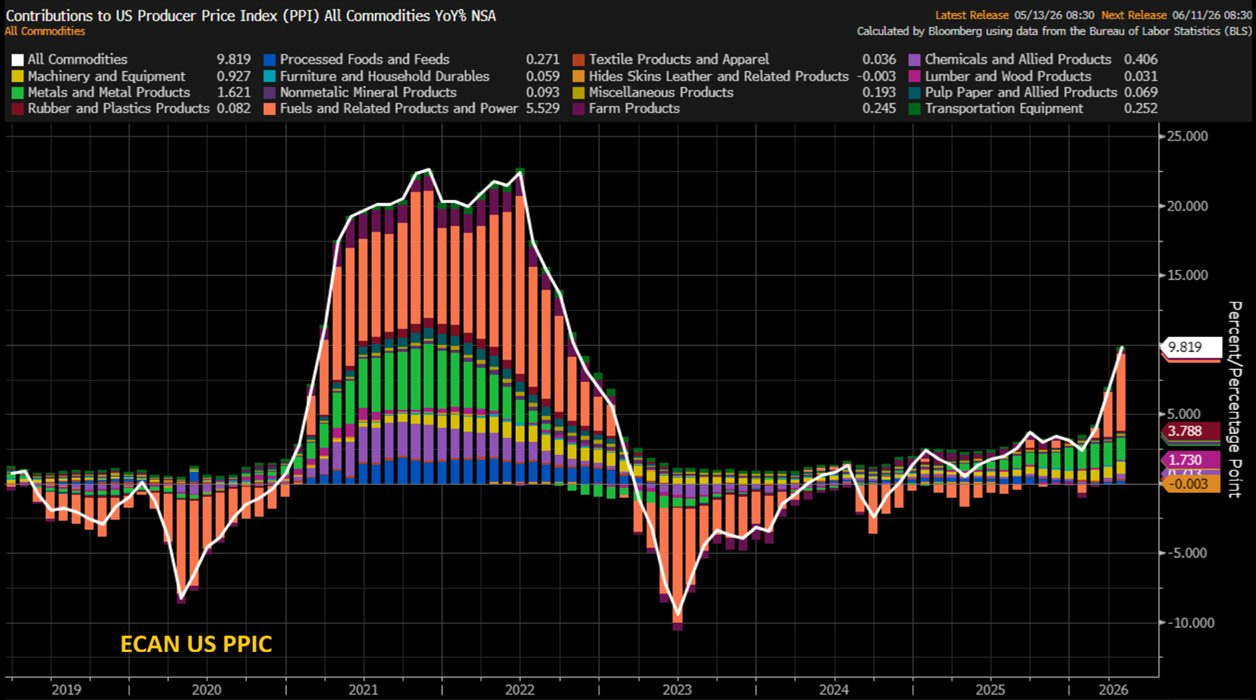

The shocker of the week was the PPI, which came in at 6%, significantly higher than the 4.8% estimate.

When we dig deeper, commodities led by fuels/power were the biggest contributor to the all-commodities basket of PPI.

Note that higher equity markets were partly responsible for the higher PPI (higher portfolio management component).

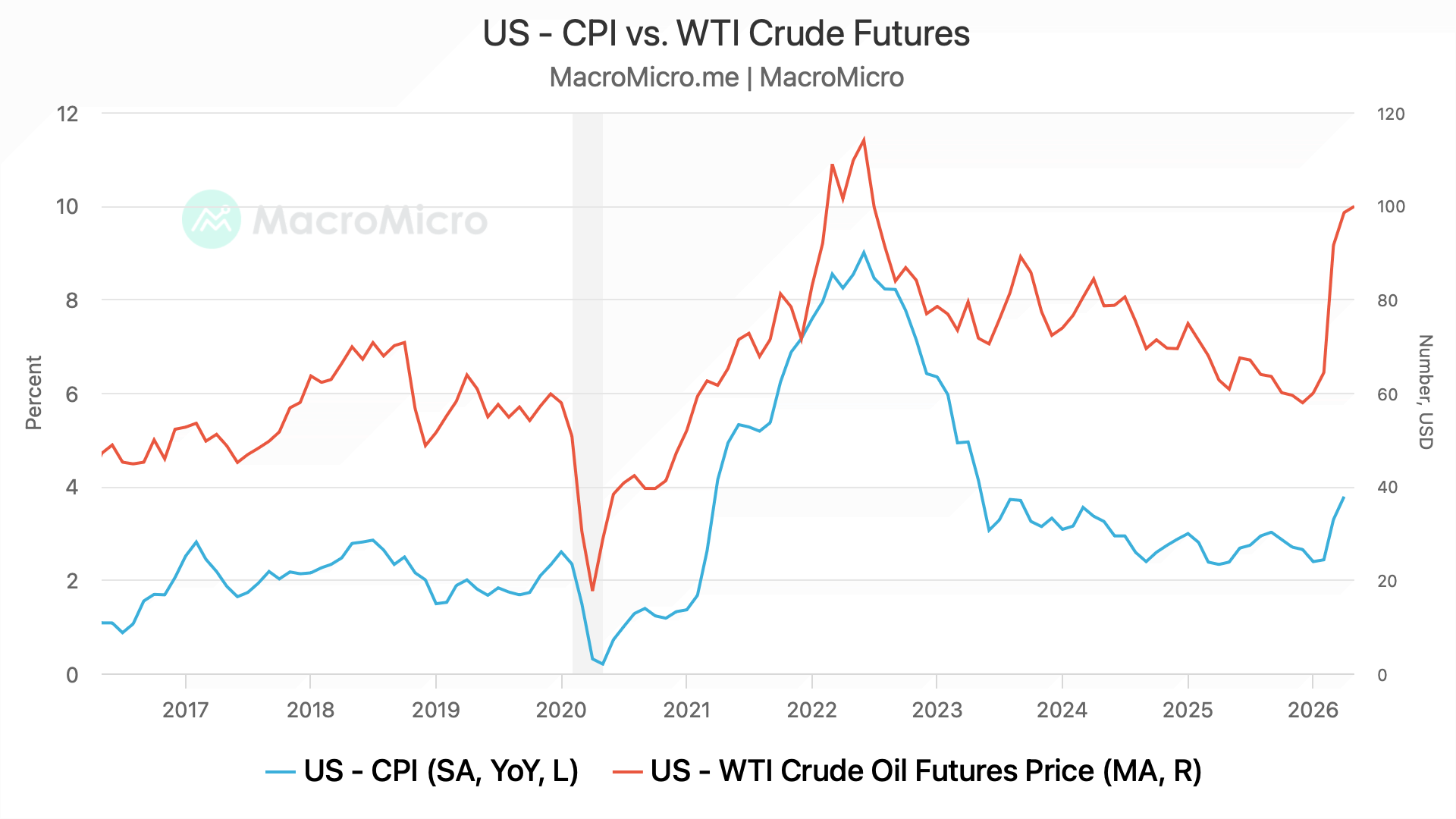

We believe CPI and PPI are headed significantly higher, as the correlation with CPI and WTI futures suggests.

If the oil prices stay above $90-95 for another 3-4 months, as market participants expect, we might see the headline CPI heading towards 5%.

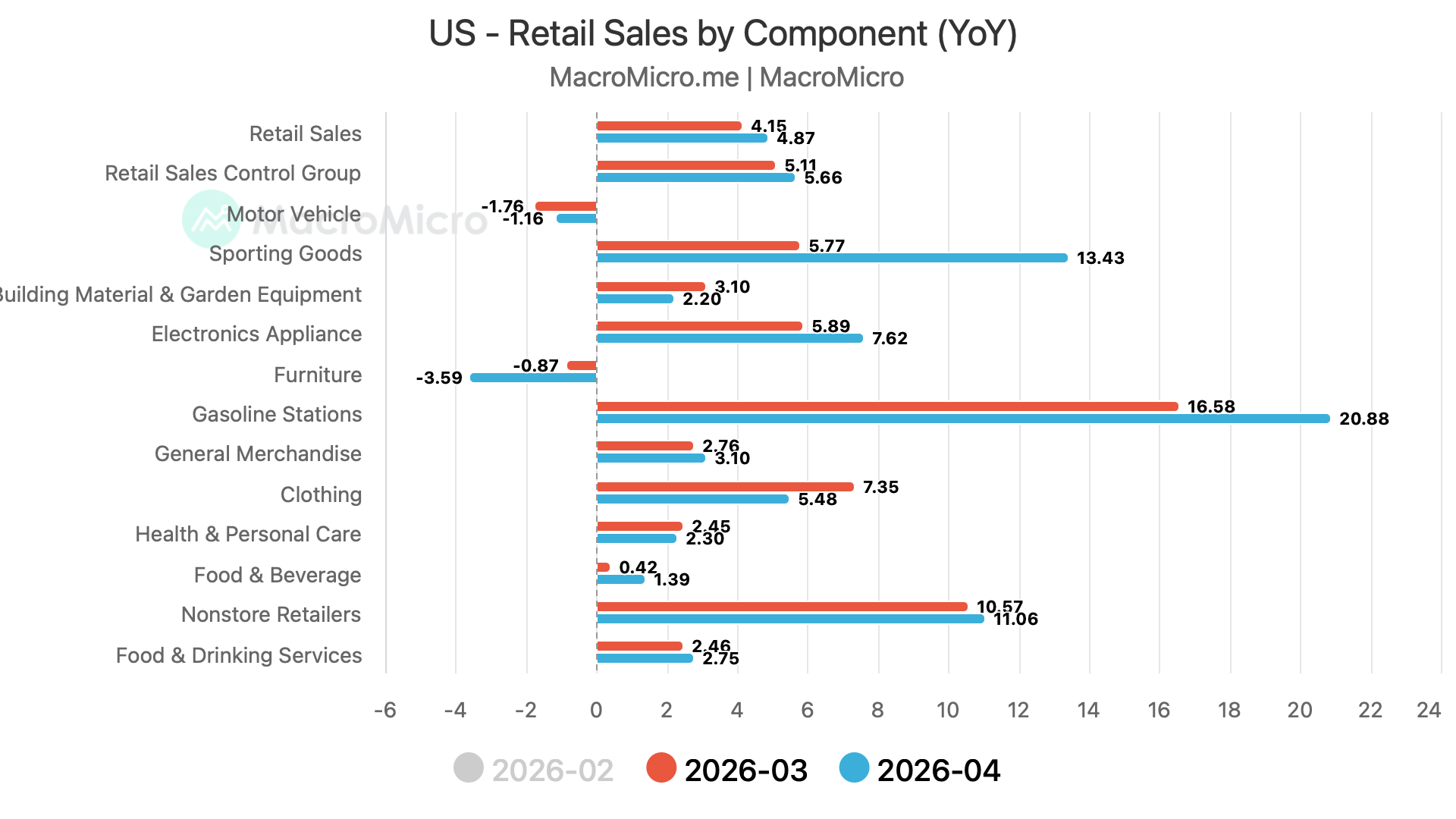

The Retail Sales came in line with estimates. The headline retail sales came in at 0.5% MoM v/s expected 0.5%, while the control group came in at 0.5% v/s expected 0.3%.

Unsurprisingly, gasoline stations topped the chart with a 21% YoY gain, while the trend of degrowth in furniture (housing-related) and motor vehicles continues.

Note that while the nominal retail sales continue to be strong, inflation-adjusted numbers (real retail sales) have been subdued.

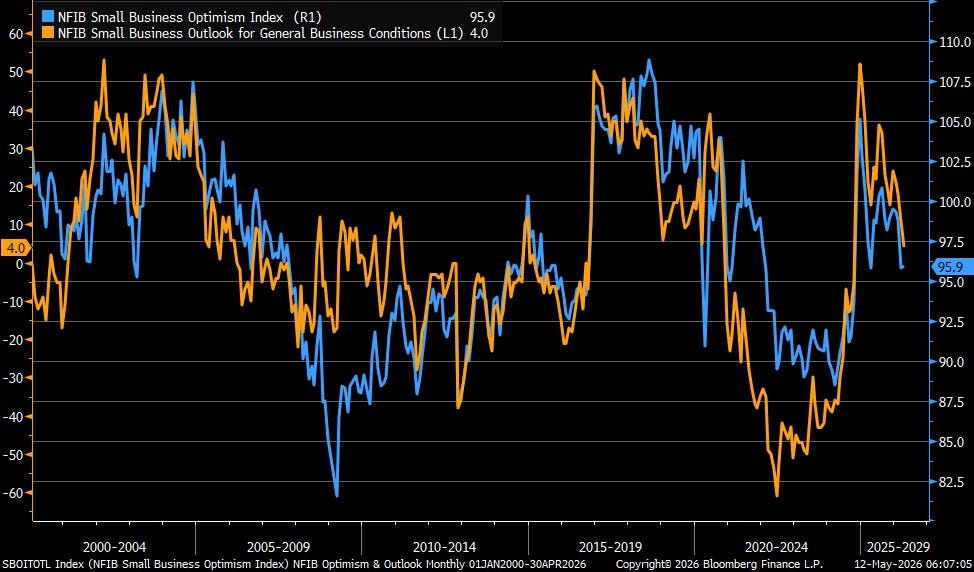

The NFIB Small Business Optimism Index fell as sentiment soured amid the war in the Middle East.

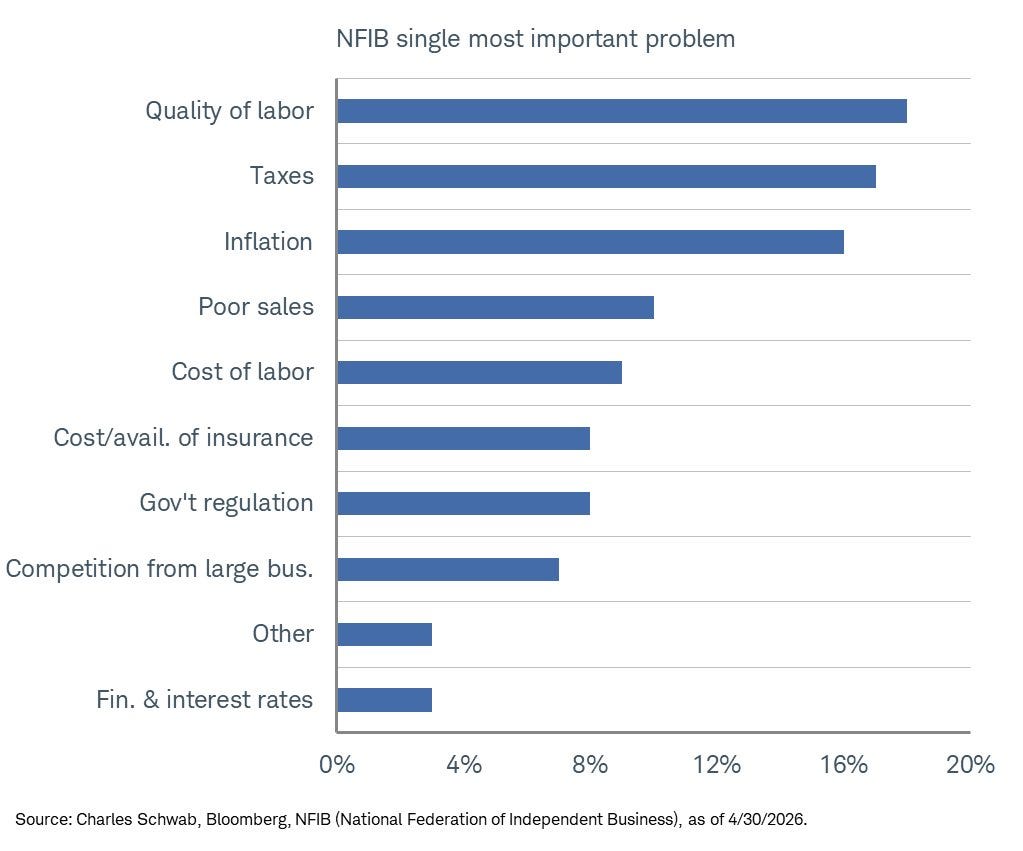

The top three single most important problems for small businesses remain Quality of Labour (thanks to a halt on illegal immigration), taxes (thanks to tariffs) and inflation (thanks to war).

It has been really tough for small businesses to navigate over the past 1.5 years due to multiple shocks, as mentioned above (immigration, tariffs, and war).

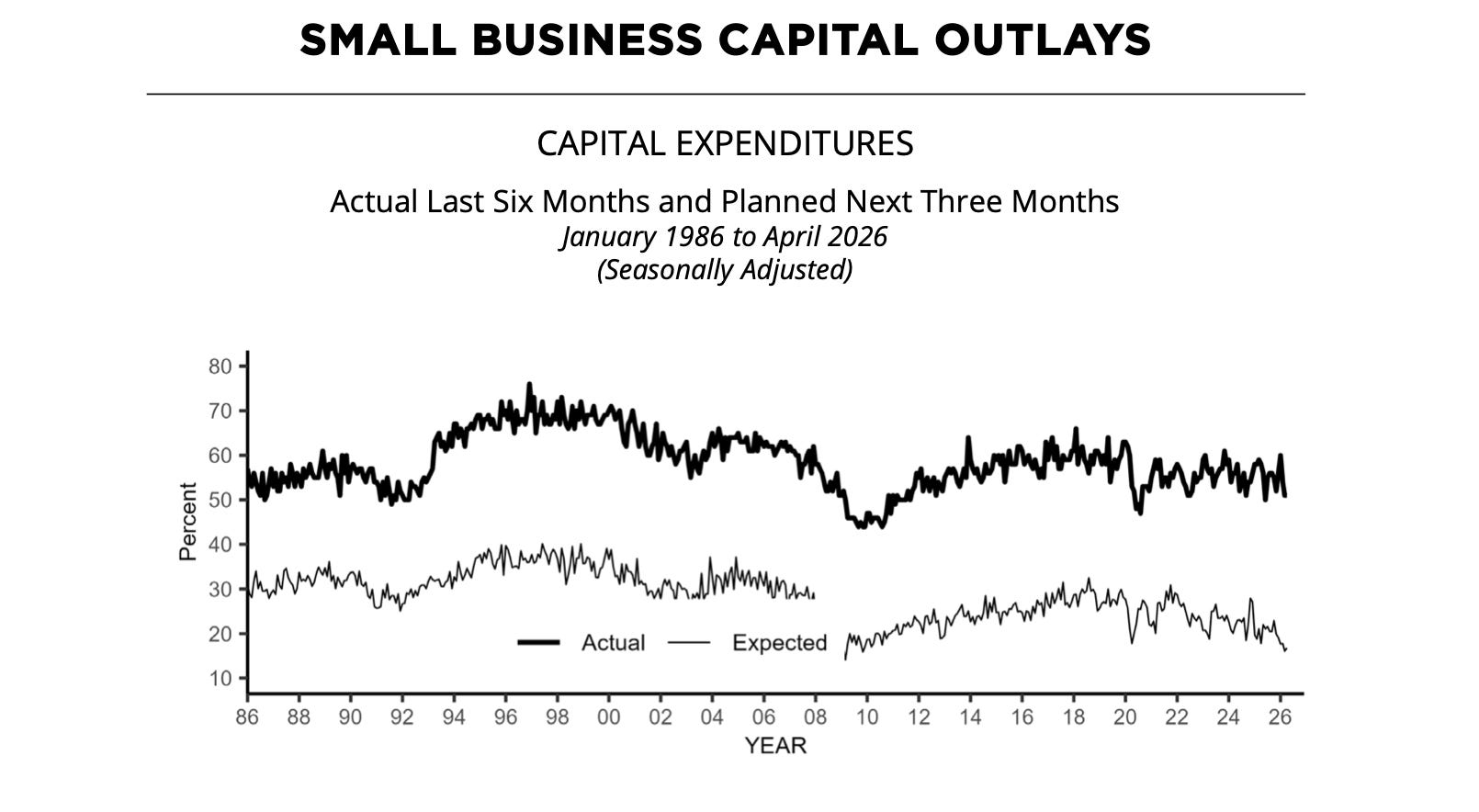

Furthermore, the expected capex outlays planned for the next three months are the lowest since the GFC (2008), indicating that the demand outlook is uncertain as they reel from multiple shocks.